|

시장보고서

상품코드

1906191

폴리에스터 타이어 코드 원단 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Polyester Tire Cord Fabrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

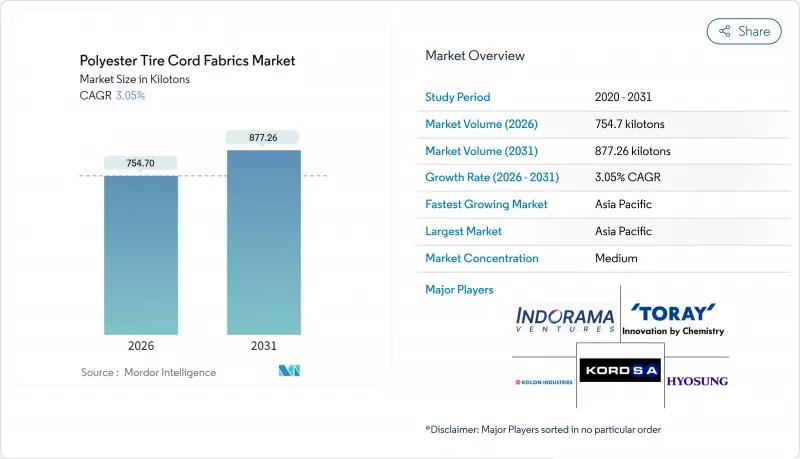

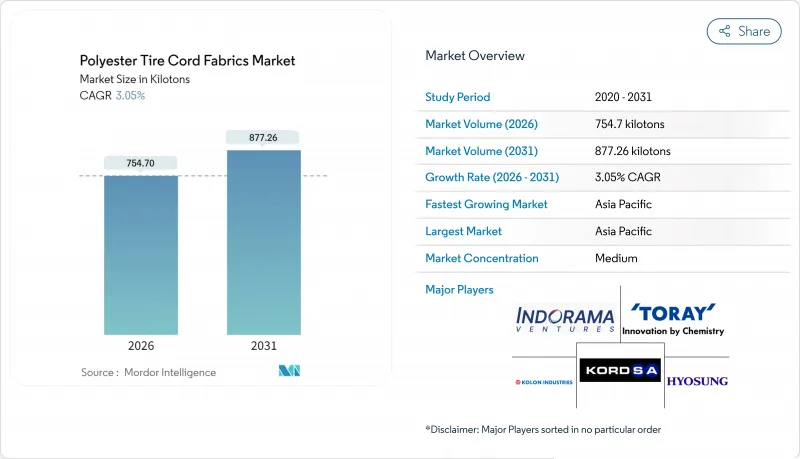

폴리에스터 타이어 코드 원단 시장 규모는 2026년에 754.7킬로톤으로 추정되고 있습니다. 2025년 732.37킬로톤에서 성장했으며 2031년에는 877.26킬로톤에 이를 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 3.05%로 성장이 전망되고 있습니다.

아시아태평양 지역에서의 레이디얼 타이어 보급률 증가, 고탄성 저수축(HMLS) 원사로의 가속화된 전환, 그리고 전기차(EV) 생산량 확대가 이러한 꾸준한 성장세를 뒷받침하고 있습니다. 효성과 코론의 거의 완전한 공장 가동률, 만성적인 PTA/MEG 가격 변동, 그리고 EU와 미국의 포름알데히드 규제 강화는 비용 구조와 경쟁 전략을 재편하고 있습니다. 공급은 재활용 PET 능력을 갖춘 통합 생산자로 기울어지고 있는 반면, 소규모 변환업체들은 규제 승인을 확보하기 위해 포름알데히드 프리 접합에 집중하고 있습니다. 지역별 수요 핫스팟으로는 인도의 급증하는 트럭 레이디얼 타이어 전환과 베트남의 수출 지향형 승용차 타이어 클러스터가 있으며, 이로 인해 다른 지역의 바이어스 타이어 수요 감소에도 불구하고 HMLS 폴리에스터 물량이 증가하고 있습니다.

세계의 폴리에스터 타이어 코드 원단 시장 동향과 전망

아시아태평양의 레이디얼 타이어 보급률 급증

2024년 아시아태평양 지역의 승용차는 레이디얼 타이어를 광범위하게 채택하여 전년 대비 상당한 증가를 기록했습니다. 이러한 변화는 주로 중국과 인도 OEM 업체들이 구름저항 시험에서 바이어스 타이어 설계를 불리하게 만드는 연비 규제를 수용하면서 촉진되었습니다. 높은 공기압을 관리하기 위해 바이어스 타이어보다 더 많은 폴리에스터 코드가 필요한 레이디얼 타이어는 결과적으로 바이어스 타이어 물량이 감소하는 상황에서도 고탄성 저수축(HMLS) 폴리에스터 수요를 증가시켰습니다. 중동 지역에서는 신규 타이어 생산 시설이 전적으로 레이디얼 라인에 투자하면서 폴리에스터 소비량의 장기적 증가가 보장되고 있습니다. 아세안 국가들의 상용차 플리트는 도입 속도가 더딘 편이지만, 급등하는 디젤 가격으로 인해 레이디얼 타이어의 총소유비용(TCO) 측면에서 채택이 가속화되고 있습니다. 이러한 추세는 폴리에스터 타이어 코드 직물 시장이 개발도상 지역의 후발 도입국들로부터 꾸준히 혜택을 볼 수 있는 기반을 마련하고 있습니다.

OEM 제조업체의 급속한 HMLS 실로의 전환 및 PCI 제거

타이어 제조사들은 표준 인장 강도 폴리에스터에서 HMLS 등급으로 전환하고 있습니다. 이 신소재는 카카스 플라이 절단을 통해 무게를 줄일 수 있습니다. HMLS 원사의 낮은 열 수축성은 후경화 팽창(PCI) 공정을 생략하는 생산 라인을 지원하여 공장 에너지 사용을 절감하고 사이클 시간을 단축합니다. 브리지스톤과 미쉐린은 PCI 없는 라인을 시범 운영 중이지만, 폐기율 관리가 가능한 개량형 RFL 화학물질의 대량 생산이 광범위한 도입의 관건입니다. 고강도 원사와 PCI 제거가 결합되면 타이어당 비용과 지속가능성 지표가 개선되어 OEM의 HMLS 폴리에스터 선호도가 강화됩니다.

PTA/MEG 원료 가격 변동성

브렌트유 가격은 폴리에스터 원가의 약 70%를 차지하는 PTA와 MEG에 큰 영향을 미쳐, 변환업체의 마진이 몇 달 만에 급변하게 만듭니다. 2024년 아시아 PTA 현물 가격은 큰 변동을 겪으며 비통합 컨버터의 예산을 교란시켰습니다. 효성 같은 통합 기업은 자체 생산 단량체를 활용해 이러한 변동성을 완화하지만, 중소 기업들은 OEM과 분기별로 재협상해야 하는 상황에 직면해 확장 계획이 지연되고 연구개발 지출이 감소하고 있습니다.

부문 분석

레이디얼 타이어는 2025년 수요의 57.31%를 차지했으며, 2031년까지 4.05% 성장할 것으로 예상되어 바이어스 타이어 생산량 증가율을 앞지르며 해당 부문의 폴리에스터 타이어 코드 직물 시장 규모를 확대할 것입니다. 레이디얼 타이어는 순항 속도에서 15-20°C 더 낮은 온도를 유지하여, EV 플랫폼이 카카스에 추가 중량을 가하지 않고도 배터리로 인한 열 부하를 관리할 수 있게 합니다. 바이어스 타이어는 농업 및 오프로드 틈새 시장에서 여전히 우위를 점하고 있으나, 초기 가격이 낮다는 장점만으로는 도로 주행 시 높은 연료 소비량을 상쇄하지 못합니다. 중국에서는 승용차의 레이디얼 타이어 채택률이 상당한 수준을 넘어섰습니다. 한편 2024년까지 상용차 시장에서도 상당한 보급률을 달성했습니다. 이러한 전환은 각각 타이어당 코드 사용량 증가로 이어졌으며, 이는 증가한 공기압에 기인합니다. 이러한 변화는 폴리에스터 타이어 코드 직물 시장 성장의 가장 중요한 물량 촉진요인으로 작용합니다.

성숙 경제권에서는 바이어스 타이어 물량이 감소하는 반면, 총비용보다 수리 가능성을 우선시하는 사하라 이남 아프리카에서는 증가하고 있습니다. 그럼에도 중동 지역의 신규 공장들이 레이디얼 전용 라인을 지정함에 따라 세계의 바이어스 타이어 점유율은 계속 감소하고 있습니다. 한국타이어의 iON 타이어는 화학적으로 재생된 HMLS(고분자 고밀도 폴리에스터) 원사와 스틸 벨트를 결합해 지속가능성과 강도 사이의 균형을 이루며, 하이브리드 구조가 장거리 운송 분야에서 레이디얼 타이어의 프리미엄을 어떻게 낮출 수 있는지 보여줍니다. 이러한 혁신은 레이디얼 타이어의 성장을 지속시키는 동시에 주류 속도 등급에서 폴리에스터가 아라미드에 의해 대체되는 것을 방지합니다.

폴리에스터 타이어 코드 원단 시장 보고서는 타이어 유형(레이디얼 타이어 및 바이어스 타이어), 용도(승용차, 상용차, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양 지역은 2025년 세계의 물량의 49.07%를 차지했으며, 2031년까지 3.95% 성장할 전망입니다. 이러한 성장은 주로 중국 승용차 타이어 공장의 높은 가동률과 인도의 주요 자동차 시장 부상에 의해 주도되고 있습니다. 코론의 최근 베트남 투자는 금호, 세일런, 브리지스톤 등 업계 거대 기업들의 수요에 부응하기 위한 공장 생산 능력 증대를 목표로 합니다. 베트남의 승용차 타이어 수출과 연간 폴리에스터 코드 소비량은 폴리에스터 타이어 코드 원단 시장에서의 중요성을 부각시킵니다.

북미와 유럽은 세계의 생산량에서 상당한 비중을 차지하지만 성장 속도가 둔화되고 있습니다. 이러한 정체는 차량 주행 거리 정체와 트레드 수명 연장에 기인합니다. EU의 포름알데히드 규제에 대응해 포름알데히드 무첨가 접착제로의 전환이 두드러지며, 코쿤이 이를 주도하고 있습니다. 공급망 지역화 추세를 반영해 금호타이어는 USMCA 원산지 규정에 부합하기 위해 유럽 내 그린필드 부지 확보를 검토 중입니다. 한편 콘티넨탈의 지속가능 폴리에스터 추진은 현지 변환업체들에게 재생 소재 인증을 요구하며 시장 환경을 복잡하게 만들지만, 동시에 폴리에스터 타이어 코드 원단 시장의 진입 장벽을 높이고 있습니다.

남미, 중동, 아프리카는 안정적인 성장세를 보이며 상당한 시장 점유율을 차지하고 있습니다. 피렐리는 사우디아라비아에 공장을 설립했으며, 모로코 센투리 공장도 추가 타이어 생산에 기여할 예정입니다. 이러한 생산 증가로 HMLS 코드 수요를 충족시킬 것으로 전망됩니다. 2024년 터키의 코르드사는 인근 OEM 업체를 전략적으로 겨냥한 폴리에스터 원사 생산 라인을 공개했습니다. 브라질의 타이어 생산은 회복세에 있지만, 국내 코드 생산 능력 부족으로 대만의 포모사 태페타(Formosa Taffeta)에 대한 수입 의존도가 높습니다. 이러한 지역 간 역학 관계는 타이어 생산량이 적은 지역에서도 지역적 공급 부족이 폴리에스터 타이어 코드 원단 시장을 확대시킬 수 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 특히 아시아태평양 지역에서 급증하는 레이디얼 타이어 보급률

- 고강도 HMLS PET 원사로의 OEM 전환 가속화

- 저회전저항 카카스 수요를 촉진하는 전기차 생산 증가

- 후경화 인플레이션(PCI) 제거를 통한 에너지 절감 효과

- 재활용/바이오 기반 PET 코드에 대한 OEM의 지속가능성 의무

- 시장 성장 억제요인

- PTA/MEG 원료 가격의 변동성

- EU 및 미국에서의 접착제(RFL) 포름알데히드 규제 강화

- 초고속 적용 분야에서의 아라미드 코드 대비 성능 격차

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 타이어 유형별

- 레이디얼 타이어

- 바이어스 타이어

- 용도별

- 승용차

- 상용차

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 튀르키예

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- Bekaert

- Century Enka Limited

- CORDENKA GmbH & Co. KG

- Far Eastern New Century Corporation

- Firestone Fibers & Textiles

- FORMOSA TAFFETA CO., LTD.

- HYOSUNG

- Indorama Ventures Public Company Limited

- Jiangsu Taiji Industry New Materials Co., Ltd.

- Junma Group

- Kolon Industries Inc.

- KORDARNA Plus as

- Kordsa Teknik Tekstil AS

- Madura Industrial Textiles Ltd.

- Shandong Helon Polytex Chemical Fibre

- SRF Limited

- TEIJIN FRONTIER(USA),INC.

- TORAY INDUSTRIES,INC.

- Zhejiang Hailide New Material Co., Ltd.

제7장 시장 기회와 장래의 전망

HBR 26.01.26Polyester Tire Cord Fabrics Market size in 2026 is estimated at 754.7 kilotons, growing from 2025 value of 732.37 kilotons with 2031 projections showing 877.26 kilotons, growing at 3.05% CAGR over 2026-2031.

Rising radial-tire penetration across Asia-Pacific, the accelerating shift to high-modulus low-shrinkage (HMLS) yarns, and expanding electric-vehicle (EV) output underpin this steady headline growth. Hyosung's and Kolon's near-full plant utilization, along with chronic PTA/MEG price swings, and the tightening of EU and U.S. formaldehyde rules are reshaping cost structures and competitive strategies. Supply is tilting toward integrated producers with recycled-PET capability, while smaller converters focus on formaldehyde-free bonding to secure regulatory clearance. Regional demand hot spots include India's surging truck radial conversion and Vietnam's export-oriented passenger-tire cluster, each lifting HMLS polyester volumes despite bias-tire contraction elsewhere.

Global Polyester Tire Cord Fabrics Market Trends and Insights

Surging Radial-Tire Penetration in Asia-Pacific

In 2024, passenger cars in the Asia-Pacific region widely adopted radial tires, marking a significant increase from previous years. This shift was largely driven by Chinese and Indian OEMs adapting to fuel-economy regulations that penalized bias designs in rolling-resistance tests. Radial tires, requiring more polyester cord than their bias counterparts to manage heightened inflation pressures, have consequently boosted demand for High Modulus Low Shrinkage (HMLS) polyester, even as bias tire volumes decline. In the Middle East, greenfield tire projects have committed exclusively to radial lines, ensuring a long-term increase in polyester consumption. While commercial vehicle fleets in ASEAN nations have been slow to adopt, surging diesel prices are making a compelling case for the total cost of ownership in favor of radial tires. This trend positions the polyester tire cord fabrics market to steadily benefit from late adopters in developing regions.

Rapid OEM Shift to HMLS Yarns and PCI Elimination

Tire manufacturers are shifting from standard-tenacity polyester to HMLS grades. These new grades allow for carcass-ply cuts that reduce weight. The lower thermal shrinkage of HMLS yarns also supports production lines that skip post-cure inflation (PCI), cutting plant energy use and shortening cycle times. Bridgestone and Michelin have piloted PCI-free lines, but widespread rollout hinges on scaling modified RFL chemistries that control scrap rates. Combined, higher-tenacity yarns and PCI elimination improve cost per tire and sustainability metrics, reinforcing OEM preference for HMLS polyester.

Volatile PTA/MEG Feedstock Prices

Brent crude prices heavily influence PTA and MEG, which together account for nearly 70% of polyester costs, causing converter margins to fluctuate within months. In 2024, Asian PTA spot prices experienced significant changes, disrupting budgets for non-integrated converters. While integrated players like Hyosung mitigate this volatility using captive monomers, smaller firms find themselves renegotiating quarterly with OEMs, leading to stalled expansion plans and reduced research and development spending.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating EV Production Demanding Low-Rolling-Resistance Carcasses

- OEM Sustainability Mandates for Recycled/Bio-Based PET Cords

- Formaldehyde Restrictions and Performance Limits in Premium Tires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radial designs represented 57.31% of 2025 demand and are expected to grow at 4.05% to 2031, outpacing the growth of bias output, thereby increasing the size of the polyester tire cord fabrics market for this segment. Radials run 15-20 °C cooler at cruising speed, enabling EV platforms to manage battery-induced heat loads without adding extra weight to the carcass. Bias tires continue to dominate in agricultural and off-road niches, yet their lower upfront price fails to offset the higher fuel consumption on the road. In China, passenger cars have seen radial adoption surpassing a significant level. Meanwhile, by 2024, commercial vehicles reached a notable penetration rate. Each of these transitions has led to an increase in cord usage per tire, attributed to heightened inflation pressure. This shift stands as the most significant volume driver for the growth of the polyester tire cord fabrics market.

Bias volumes are contracting in mature economies but growing in sub-Saharan Africa, where repairability is prioritized over total cost. Even so, the global bias share continues to shrink as Middle East greenfield plants specify radial-only lines. Hankook's iON tire combines chemically recycled HMLS yarn with steel belts to strike a balance between sustainability and strength, demonstrating how hybrid constructions can reduce the radial premium in long-haul applications. Such innovations sustain radial growth while preventing the displacement of polyester by aramid in mainstream speed ratings.

The Polyester Tire Cord Fabrics Market Report is Segmented by Tire Type (Radial Tire and Bias Tire), Application (Passenger Cars, Commercial Vehicles, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific contributed 49.07% of global volume in 2025 and is expanding at 3.95% to 2031. This growth is largely driven by China's passenger-tire plants operating at high capacity and India emerging as a major car market. Kolon's recent investment in Vietnam aims to boost the plant's capacity, aligning with the demands of industry giants like Kumho, Sailun, and Bridgestone. Vietnam's passenger tire exports and its annual consumption of polyester cord underscore the market's significance for polyester tire cord fabrics.

North America and Europe together represent a notable share of the global volume but are experiencing slower growth. This stagnation is attributed to plateauing vehicle miles and extended tread life. In response to the EU's formaldehyde caps, there's a noticeable shift towards formaldehyde-free adhesives, with Cokoon leading the charge. Reflecting a trend of supply-chain regionalization, Kumho is eyeing a greenfield site in Europe to align with USMCA's rules of origin. Meanwhile, Continental's ambition for sustainable polyester is pushing local converters to authenticate their recycled content, complicating the landscape but simultaneously raising entry barriers in the polyester tire cord fabrics market.

South America, the Middle East, and Africa collectively hold a significant market share, with steady growth. Pirelli has established a facility in Saudi Arabia, while Morocco's Sentury factory is set to contribute additional tire production. This surge in production is expected to meet the demand for HMLS cord. In 2024, Turkey's Kordsa unveiled a polyester yarn line, strategically catering to nearby OEMs. Although Brazil's tire production is on the mend, the country struggles with insufficient domestic cord capacity, resulting in a reliance on imports from Taiwan's Formosa Taffeta. Such inter-regional dynamics highlight how localized shortages can amplify the polyester tire cord fabrics market, even in regions with modest tire production.

- Bekaert

- Century Enka Limited

- CORDENKA GmbH & Co. KG

- Far Eastern New Century Corporation

- Firestone Fibers & Textiles

- FORMOSA TAFFETA CO., LTD.

- HYOSUNG

- Indorama Ventures Public Company Limited

- Jiangsu Taiji Industry New Materials Co., Ltd.

- Junma Group

- Kolon Industries Inc.

- KORDARNA Plus a.s.

- Kordsa Teknik Tekstil A.S.

- Madura Industrial Textiles Ltd.

- Shandong Helon Polytex Chemical Fibre

- SRF Limited

- TEIJIN FRONTIER(U.S.A.),INC.

- TORAY INDUSTRIES,INC.

- Zhejiang Hailide New Material Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging radial-tire penetration, especially in Asia-Pacific

- 4.2.2 Rapid OEM shift to high-tenacity HMLS PET yarns

- 4.2.3 Accelerating EV production demanding low-rolling-resistance carcasses

- 4.2.4 Energy-saving potential from eliminating post-cure inflation (PCI)

- 4.2.5 OEM sustainability mandates for recycled / bio-based PET cords

- 4.3 Market Restraints

- 4.3.1 Volatile PTA/MEG feed-stock prices

- 4.3.2 Adhesive (RFL) formaldehyde restrictions tightening in EU and U.S.

- 4.3.3 Performance gap vs. aramid cords for ultra-high-speed applications

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Tire Type

- 5.1.1 Radial Tire

- 5.1.2 Bias Tire

- 5.2 By Application

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.2.3 Other Application

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Century Enka Limited

- 6.4.3 CORDENKA GmbH & Co. KG

- 6.4.4 Far Eastern New Century Corporation

- 6.4.5 Firestone Fibers & Textiles

- 6.4.6 FORMOSA TAFFETA CO., LTD.

- 6.4.7 HYOSUNG

- 6.4.8 Indorama Ventures Public Company Limited

- 6.4.9 Jiangsu Taiji Industry New Materials Co., Ltd.

- 6.4.10 Junma Group

- 6.4.11 Kolon Industries Inc.

- 6.4.12 KORDARNA Plus a.s.

- 6.4.13 Kordsa Teknik Tekstil A.S.

- 6.4.14 Madura Industrial Textiles Ltd.

- 6.4.15 Shandong Helon Polytex Chemical Fibre

- 6.4.16 SRF Limited

- 6.4.17 TEIJIN FRONTIER(U.S.A.),INC.

- 6.4.18 TORAY INDUSTRIES,INC.

- 6.4.19 Zhejiang Hailide New Material Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment