|

시장보고서

상품코드

1906199

중동 및 아프리카의 이동통신망사업자(MNO) 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Middle East And Africa Telecom MNO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

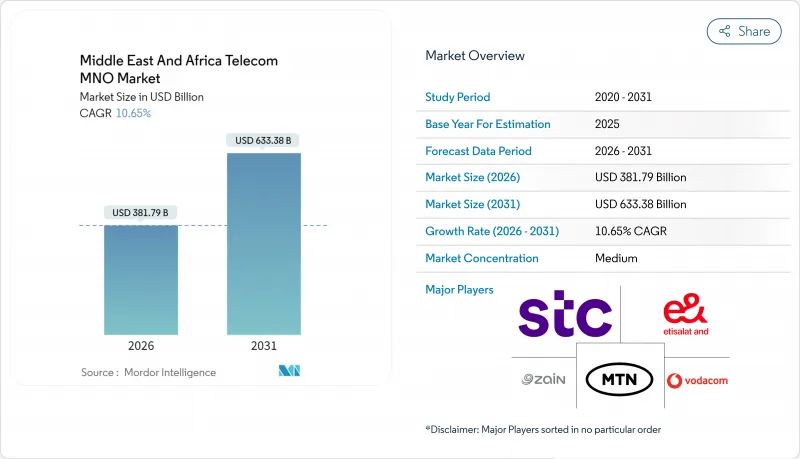

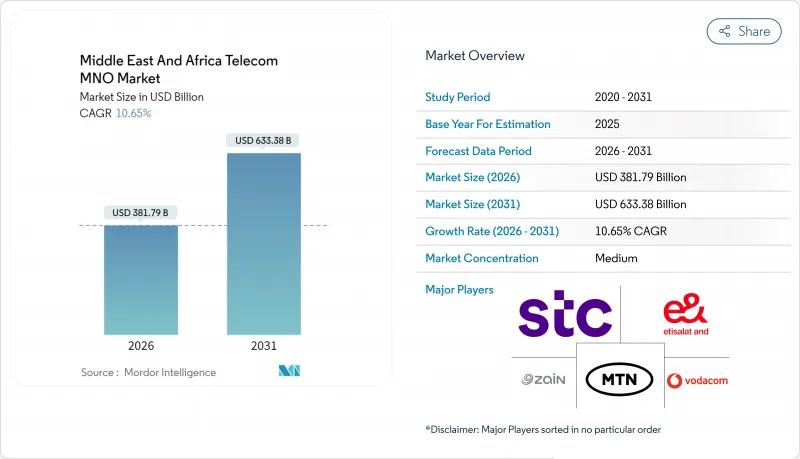

중동 및 아프리카의 이동통신망사업자(MNO) 시장의 규모는 2026년 3,817억 9,000만 달러에 달할 것으로 예측되고 있습니다.

2025년의 3,450억 4,000만 달러에서 성장하여 2031년에는 6,333억 8,000만 달러에 이를 전망으로, 2026년부터 2031년에 걸쳐 CAGR 10.65%로 확대할 것으로 전망되고 있습니다.

급속한 5G 전개, 확대하는 광섬유 백홀, 높아지는 스마트폰 보급률이 더해 이 지역은 구조적으로 높은 성장 궤도를 유지하고 있습니다. 투자 의욕은 계속 높은 수준에 있으며, 이집트는 최초의 5G 라이선스에 1억 5,000만 달러를 투자하였고, 사우디아라비아는 2025년 5G 고정 무선 액세스(FWA)의 커버리지를 78%까지 확대했습니다. 모로코는 2025년 5G 커버리지 25% 달성을 위해 4억 7,500만 달러를 투입했으며 이는 차세대 액세스에 대한 정책적인 중점을 강조하고 있습니다. 저궤도(LEO) 위성 광대역에 의한 경쟁 압력이나 홍해 케이블 회랑 주변의 지정학적 리스크가 시장 심리를 억제하는 한편, 기업의 디지털화나 모바일 머니에 의한 ARPU 향상에 의해 상쇄될 전망입니다.

중동 및 아프리카의 이동통신망사업자(MNO) 시장의 동향 및 인사이트

동영상 중심 앱으로 모바일 데이터 트래픽의 폭발적인 성장

동영상 시청으로 인해 사용자가 음성 통화 및 SMS에서 고화질 스트리밍으로 전환함에 따라 이동통신사업자의 수익 아키텍처를 재구성합니다. 걸프 지역의 SMS 수익은 2013년 43억 달러에서 2018년 32억 달러로 감소한 것으로 나타난 반면 동기간 모바일 데이터 양은 180% 증가했습니다. 이에 대해 사업자는 5G 스몰셀의 밀도 향상으로 대응하고 있습니다. 중동 및 북아프리카의 스몰셀 시장은 2030년까지 4억 1,254만 달러(CAGR 40.9%)에 이를 것으로 예측됩니다. 월 약 70달러의 FWA 계약은 새로운 광섬유 추가 없이 가정의 스트리밍 트래픽을 수익화합니다. 네트워크 계획 담당자는 현재 대규모 MIMO 업그레이드 비용과 프리미엄 사용자의 기가비트 패키지 구매 의향 증가세를 비교하고 있습니다. 사하라 이남 아프리카에서는 2030년까지 사용자당 월간 데이터 사용량이 3배인 14GB에 이를 것으로 예측되고, 스펙트럼과 백홀 모두에 대한 병행 투자가 요구되고 있습니다.

지원 주파수 경매로 가속화되는 4G 및 5G 배포

걸프 국가와 북아프리카의 규제 당국은 현재 일시적 소득인 경매 수수료보다 커버리지 목표를 강조하고 있습니다. 사우디아라비아의 '2025-2027년 주파수 전망'에서는 비지상파 네트워크 및 FWA용으로 새로운 주파수대를 할당해, 간이 라이선싱 제도에 의해 사업자 시장 투입까지의 시간을 대폭 단축하고 있습니다. 남아프리카의 2025년 국가 무선 주파수 계획도 마찬가지로 산업용 5G를 촉진하는 전용 프라이빗 네트워크용 스펙트럼을 확보하고 있습니다. UAE에서는 이미 7,000개의 5G 기지국이 가동하고 있으며, 2025년까지 500개의 캠퍼스 내 사설망을 정비할 방침입니다. 바레인, 요르단, 쿠웨이트, 사우디아라비아에서 일괄적인 2G 및 3G 중단으로 5G용 저대역 스펙트럼을 확보하여 스펙트럼 효율을 더욱 향상시킵니다. 이러한 이니셔티브는 지역의 광대역 보급을 가속화하고 비트당 전송 비용을 감소시킵니다. 이는 중동 및 아프리카의 이동통신망사업자(MNO) 시장의 수익 기반을 유지하는 데 매우 중요합니다.

격렬한 경쟁과 SIM 등록 의무화가 ARPU를 억제

생체 인증을 통한 SIM 등록 의무화로 컴플라이언스 비용이 증가하는 반면, 케냐, 가나 등 시장에서는 신규 참가자가 가격 경쟁을 일으키고 있습니다. 인플레이션이 소비자의 지출 능력을 저하시키는 이중 압박 요인이 되는 가운데, 규제 당국은 가계 보호를 위해 요금 인상을 억제하고 있습니다. 사업자 측은 컨텐츠 번들이나 멤버십 앱으로 대응하고 있지만, 규제 환경이 분단되고 있기 때문에 실시 상황에 편차가 발생하고 중동 및 아프리카의 MNO 시장에서 수익화가 억제되고 있습니다.

부문 분석

데이터 통신 및 인터넷 플랜은 2025년 수익의 39.35%를 차지하였으며 중동 및 아프리카의 MNO 시장에서 가장 큰 수익원이 되었습니다. IoT 및 M2M은 특히 현저한 동향이며 2031년까지 중동 및 아프리카의 MNO 시장 규모에서 CAGR 10.74%로 확대될 전망입니다. 음성 및 메시징은 OTT 플랫폼으로의 이용자 이동에 따라 25% 미만으로 하락할 전망입니다. 이에 대해, 통신사업자는 동영상 서비스의 제로 레이팅이나 유료 TV의 번들화에 의해 고객 유지를 도모합니다. 엣지 컴퓨팅 노드와 API 수익화는 데이터 계획을 보완하는 새로운 수익원으로 부각되고 있습니다.

예측 기간 동안, 서비스형 앱(Apps-as-a-Service) 모델은 5G 독립형 코어에 의존하여 게임 및 원격 의료에서 저지연 이용 사례를 창출할 전망입니다. 한때 주기적인 변동을 보인 로밍 및 도매 트래픽은 아프리카 내 무역 흐름이 확대됨에 따라 안정화될 전망입니다. 평균 데이터 가격은 하락세를 지속하지만 데이터량의 강한 탄력성에 의해 상쇄되어 중동 및 아프리카의 MNO 시장 규모의 확대를 뒷받침합니다.

중동 및 아프리카의 MNO 시장은 서비스 유형(음성 서비스, 데이터 및 인터넷 서비스, 메시징 서비스, IoT 및 M2M 서비스, OTT 및 유료 TV 서비스, 기타 서비스), 최종 사용자(기업, 소비자), 지역별로 세분화됩니다. 시장 예측은 금액(달러) 및 수량(가입자 수)으로 제공됩니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 규제 및 정책 틀

- 스펙트럼 환경과 경쟁적 보유 상황

- 통신산업의 생태계

- 거시 경제적 요인과 외부 요인

- Porter's Five Forces 분석

- 경쟁 기업 간 경쟁 관계

- 신규 참가업체의 위협

- 공급자의 협상력

- 구매자의 협상력

- 대체품의 위협

- 주요 MNO의 주요 성과 평가 지표(2020-2025년)

- 독특한 모바일 가입자 수와 보급률

- 모바일 인터넷 이용자 수와 보급률

- 액세스 기술별 및 보급률별 SIM 연결수

- 모바일 IoT 및 M2M 접속

- 광대역 연결(모바일 및 고정)

- ARPU(사용자당 평균 수익)

- 계약자 1인당 평균 데이터 사용량(GB/월)

- 촉진요인

- 동영상 중심 애플리케이션에 의한 모바일 데이터 트래픽의 폭발적 증가

- 지원적인 주파수 경매에 의해 4G 및 5G의 전개 가속화

- 기업 디지털화가 IoT 및 M2M 연결 수요를 견인

- 사하라 이남 아프리카 전역에서 젊은 층이 주도하는 스마트폰 보급

- 국경을 넘은 모바일 머니 상호 운용성이 ARPU를 향상

- 메가 프로젝트 및 스마트 시티용 개인 5G 네트워크 슬라이싱

- 억제요인

- 격렬한 경쟁과 SIM 등록 의무로 ARPU 억제

- 지정학적 불안정에 의한 인프라 투자 지연

- LEO 위성 광대역이 지방의 대체 수단으로 대두

- 내륙 아프리카 국가에서의 광섬유 백홀 부족 현상

- 기술 전망

- 통신 부문의 주요 비즈니스 모델 분석

- 가격 모델과 가격 설정 분석

제5장 시장 규모 및 성장 예측(가치, 수량)

- 종합 통신수익 및 ARPU

- 서비스 유형

- 음성 서비스

- 데이터 및 인터넷 서비스

- 메시징 서비스

- IoT 및 M2M 서비스

- OTT 및 유료 TV 서비스

- 기타 서비스(부가가치 서비스, 로밍, 법인용 및 도매 서비스 등)

- 최종 사용자

- 법인

- 소비자

- 지역

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동(카타르, 쿠웨이트, 바레인, 오만, 요르단, 이라크, 레바논, 이스라엘, 기타)

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카(이집트, 모로코, 알제리, 튀니지, 가나, 탄자니아, 세네갈, 에티오피아, 우간다, 케냐, 기타)

- 중동

제6장 경쟁 구도

- 시장 집중도

- 주요 벤더의 전략적 동향 및 투자 동향(2023-2025년)

- 2024년 이동통신망사업자(MNO) 시장의 점유율 분석

- 모바일 네트워크 서비스 제품 벤치마킹 분석

- MNO 스냅샷(구독자, 이탈률, ARPU 등)

- 이동통신망사업자(MNO) 시장의 기업 프로파일

- e&(Etisalat Group)

- STC Group

- Ooredoo Group

- Zain Group

- MTN Group

- Vodacom Group

- Orange Middle East and Africa

- Airtel Africa

- Safaricom PLC

- Maroc Telecom SA

- Telecom Egypt(WE)

- Globacom Limited(Glo Mobile)

- 9mobile(EMTS)

- Telkom SA SOC Limited

- Cell C

- Omantel

- Batelco(Beyon Group)

- du(EITC)

- Sudan Telecom Group Limited(Sudatel)

- Ethio Telecom

- AXIAN Telecom

- Econet Wireless Zimbabwe

- MTC Namibia

제7장 시장 기회 및 미래 전망

CSM 26.01.21Middle East And Africa Telecom MNO Market size in 2026 is estimated at USD 381.79 billion, growing from 2025 value of USD 345.04 billion with 2031 projections showing USD 633.38 billion, growing at 10.65% CAGR over 2026-2031.

Rapid 5G deployments, expanding fiber backhaul, and rising smartphone penetration combine to keep the region on a structurally high-growth trajectory. Investment intensity remains elevated: Egypt paid USD 150 million for its first 5G license, while Saudi Arabia pushed 5G Fixed Wireless Access (FWA) to 78% population coverage in 2025. Morocco committed USD 475 million to reach 25% 5G coverage by end-2025, underscoring a broad policy focus on next-generation access. Competitive pressure from low-earth-orbit (LEO) satellite broadband and geopolitical risks around the Red Sea cable corridor temper sentiment, but are offset by enterprise digitalization and mobile-money-driven ARPU gains.

Middle East And Africa Telecom MNO Market Trends and Insights

Explosive growth in mobile data traffic from video-centric apps

Video viewing reshapes operator revenue architecture as users pivot from voice and SMS to high-definition streaming. SMS revenue in the Gulf fell from USD 4.3 billion in 2013 to a projected USD 3.2 billion in 2018, while mobile data volumes rose 180% in the same span . Operators respond by densifying 5G small cells; the MENA small-cell market is projected to reach USD 412.54 million by 2030, a 40.9% CAGR . FWA subscriptions, priced near USD 70 each month, monetize in-home streaming traffic without fresh fiber builds. Network planners now weigh the cost of massive-MIMO upgrades against the rising willingness of premium users to pay for gigabit packages. In Sub-Saharan Africa, monthly data usage is forecast to triple to 14 GB per user by 2030, demanding parallel investment in both spectrum and backhaul.

Accelerated 4G and 5G roll-outs enabled by supportive spectrum auctions

Regulators across the Gulf and North Africa now favor coverage targets over windfall auction fees. Saudi Arabia's 2025-2027 Spectrum Outlook sets aside new bands for non-terrestrial networks and FWA via light licensing, slashing time-to-market for operators. South Africa's draft 2025 National Radio Frequency Plan similarly carves out dedicated private-network spectrum that encourages industrial 5G . The UAE already operates 7,000 5G sites, with a policy aiming for 500 on-campus private networks by 2025. Concurrent 2G/3G switch-offs in Bahrain, Jordan, Kuwait, and Saudi Arabia release low-band spectrum for 5G, further boosting spectral efficiency. The collective result is faster rural broadband coverage and lower per-bit delivery cost, crucial for sustaining the Middle East and Africa telecom MNO market's profit pool.

Aggressive price competition and SIM registration curbing ARPU

Mandatory biometric SIM registration raises compliance costs even as new entrants trigger price wars in markets like Kenya and Ghana. Inflation adds a second squeeze by eroding consumer spend capacity, while regulators cap tariff hikes to protect households. Operators counter with content bundles and loyalty apps, but execution is uneven in fragmented regulatory environments, restraining monetization in the Middle East and Africa telecom MNO market.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise digitization fueling IoT/M2M connectivity demand

- Youth-driven smartphone adoption across Sub-Saharan Africa

- Geopolitical instability delaying infrastructure investment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Data and Internet plans accounted for 39.35% of 2025 revenue, making them the single largest contributor to the Middle East and Africa telecom MNO market. IoT/M2M is the standout, expanding at a CAGR of 10.74% in the Middle East and Africa telecom MNO market size by 2031. Voice and messaging together will slip below 25% as OTT platforms cannibalize usage. Operators respond by zero-rating video services and bundling PayTV to sustain stickiness. Edge computing nodes and API monetization emerge as adjacent revenue streams that complement data plans.

Over the forecast horizon, Apps-as-a-Service models will lean on 5G standalone cores, opening low-latency use cases in gaming and telemedicine. Roaming and wholesale traffic, once cyclical, stabilize as intra-Africa trade flows broaden. Average data pricing will continue its southward drift but remain offset by strong volume elasticity, supporting the Middle East and Africa telecom MNO market size expansion.

The Middle East and Africa Telecom MNO Market is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, Iot and M2M Services, OTT and PayTV Services, and Other Services), End User (Enterprises, Consumer), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

List of Companies Covered in this Report:

- e& (Etisalat Group)

- STC Group

- Ooredoo Group

- Zain Group

- MTN Group

- Vodacom Group

- Orange Middle East and Africa

- Airtel Africa

- Safaricom PLC

- Maroc Telecom SA

- Telecom Egypt (WE)

- Globacom Limited (Glo Mobile)

- 9mobile (EMTS)

- Telkom SA SOC Limited

- Cell C

- Omantel

- Batelco (Beyon Group)

- du (EITC)

- Sudan Telecom Group Limited (Sudatel)

- Ethio Telecom

- AXIAN Telecom

- Econet Wireless Zimbabwe

- MTC Namibia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Regulatory and Policy Framework

- 4.3 Spectrum Landscape and Competitive Holdings

- 4.4 Telecom Industry Ecosystem

- 4.5 Macroeconomic and External Drivers

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Competitive Rivalry

- 4.6.2 Threat of New Entrants

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Bargaining Power of Buyers

- 4.6.5 Threat of Substitutes

- 4.7 Key MNO KPIs (2020-2025)

- 4.7.1 Unique Mobile Subscribers and Penetration Rate

- 4.7.2 Mobile Internet Users and Penetration Rate

- 4.7.3 SIM Connections by Access Technology and Penetration

- 4.7.4 Cellular IoT / M2M Connections

- 4.7.5 Broadband Connections (Mobile and Fixed)

- 4.7.6 ARPU (Average Revenue Per User)

- 4.7.7 Average Data Usage per Subscription (GB/month)

- 4.8 Market Drivers

- 4.8.1 Explosive growth in mobile data traffic from video-centric apps

- 4.8.2 Accelerated 4G and 5G roll-outs enabled by supportive spectrum auctions

- 4.8.3 Enterprise digitization fueling IoT/M2M connectivity demand

- 4.8.4 Youth-driven smartphone adoption across Sub-Saharan Africa

- 4.8.5 Cross-border mobile-money interoperability boosting ARPU

- 4.8.6 Private 5G network slicing for mega-projects and smart cities

- 4.9 Market Restraints

- 4.9.1 Aggressive price competition and SIM registration curbing ARPU

- 4.9.2 Geopolitical instability delaying infrastructure investment

- 4.9.3 LEO satellite broadband emerging as rural substitute

- 4.9.4 Limited fiber backhaul in land-locked African nations

- 4.10 Technological Outlook

- 4.11 Analysis of key business models in Telecom Sector

- 4.12 Analysis of Pricing Models and Pricing

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Overall Telecom Revenue and ARPU

- 5.2 Service Type

- 5.2.1 Voice Services

- 5.2.2 Data and Internet Services

- 5.2.3 Messaging Services

- 5.2.4 IoT and M2M Services

- 5.2.5 OTT and PayTV Services

- 5.2.6 Other Services (VAS, Roaming, Enterprise and Wholesale, etc.)

- 5.3 End-user

- 5.3.1 Enterprises

- 5.3.2 Consumer

- 5.4 Geography

- 5.4.1 Middle East

- 5.4.1.1 Saudi Arabia

- 5.4.1.2 United Arab Emirates

- 5.4.1.3 Rest of the Middle East (Qatar, Kuwait, Bahrain, Oman, Jordan, Iraq, Lebanon, Israel, and Others)

- 5.4.2 Africa

- 5.4.2.1 South Africa

- 5.4.2.2 Nigeria

- 5.4.2.3 Rest of Africa (Egypt, Morocco, Algeria, Tunisia, Ghana, Tanzania, Senegal, Ethiopia, Uganda, Kenya, and Others)

- 5.4.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Investments by key vendors, 2023-2025

- 6.3 Market share analysis for MNOs, 2024

- 6.4 Product Benchmarking Analysis for mobile network services

- 6.5 MNO snapshot (subscribers, churn rate, ARPU, etc.)

- 6.6 Company Profiles* of MNOs (Includes Business Overview | Service Portfolio | Financials | Business Strategy and Recent Developments | SWOT Analysis)

- 6.6.1 e& (Etisalat Group)

- 6.6.2 STC Group

- 6.6.3 Ooredoo Group

- 6.6.4 Zain Group

- 6.6.5 MTN Group

- 6.6.6 Vodacom Group

- 6.6.7 Orange Middle East and Africa

- 6.6.8 Airtel Africa

- 6.6.9 Safaricom PLC

- 6.6.10 Maroc Telecom SA

- 6.6.11 Telecom Egypt (WE)

- 6.6.12 Globacom Limited (Glo Mobile)

- 6.6.13 9mobile (EMTS)

- 6.6.14 Telkom SA SOC Limited

- 6.6.15 Cell C

- 6.6.16 Omantel

- 6.6.17 Batelco (Beyon Group)

- 6.6.18 du (EITC)

- 6.6.19 Sudan Telecom Group Limited (Sudatel)

- 6.6.20 Ethio Telecom

- 6.6.21 AXIAN Telecom

- 6.6.22 Econet Wireless Zimbabwe

- 6.6.23 MTC Namibia

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment