|

시장보고서

상품코드

1906202

자궁내막증 치료 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Endometriosis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

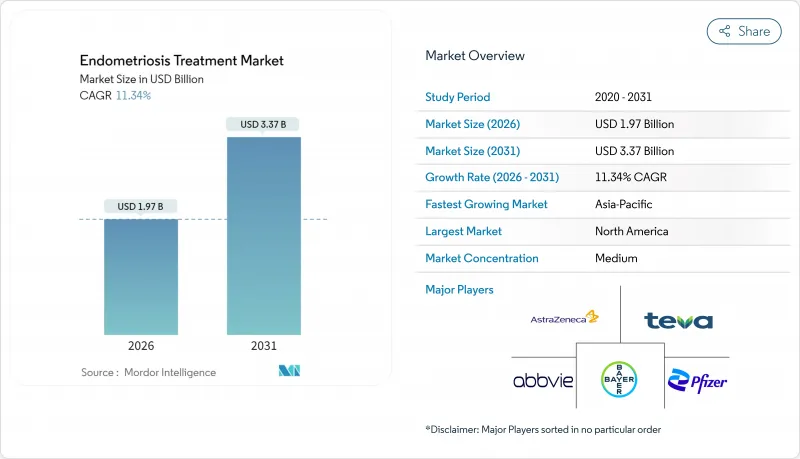

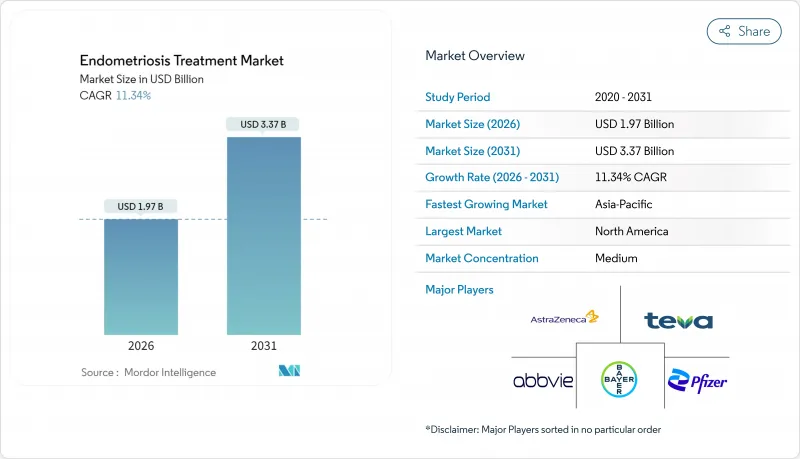

자궁내막증 치료 시장은 2025년 17억 7,000만 달러에서 2026년에는 19억 7,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 11.34%로 성장을 지속하여 2031년까지 33억 7,000만 달러에 달할 전망입니다.

질병 유병률 증가, 지속적인 공중 보건 캠페인, 경구성 성선자극호르몬 방출 호르몬(GnRH) 길항제의 잇따른 승인이 새로운 치료 기준을 수립했습니다. 비호르몬계 파이프라인으로의 벤처 캐피탈 유입, 펨텍 플랫폼의 보급, 정부 자금에 의한 행동 계획이 환자의 접근을 확대하는 동시에 경쟁 전략의 재구축을 촉진하고 있습니다. 한편, 진단 지연, 평생 비용, 전문의 부족이 계속 보급을 억제하고 있으며, 접근 격차를 해소하는 디지털 트리아지 툴과 저침습 진료지침에 대한 대처가 혁신자의 관심을 모으고 있습니다.

세계의 자궁내막증 치료 시장의 동향 및 인사이트

가임기 여성의 유병률 증가

현재 세계적으로 1억 9,000만명 이상의 여성이 자궁내막증을 갖고 생활하고 있으며, 아시아 지역에서의 이환율은 약 15%로, 유럽의 보고치인 5-10%를 현저하게 웃돌고 있습니다. 노산이라는 인구동태적 동향과 도시 생활양식의 변화가 함께 신흥 시장에서의 위험군 인구 기반을 확대하고 있습니다. 생산성 손실과 과도한 건강 관리 이용은 2,000억 달러에 이르는 세계적인 경제적 부담을 형성하고 있으며, 제약 기업이 여성 건강 전문 부문을 설립하는 계기가 되고 있습니다. 프탈레이트에 대한 노출과 증상 악화를 연관시키는 환경 조사는 새로운 대사 의학 및 환경 의학적 접근을 촉진합니다. 이해관계자는 지역 중심지를 정량화하기 위해 역학적 모니터링을 강화하고 있으며, 이 전략은 장기적으로 시장 진입의 의사결정을 정밀화할 것으로 기대되고 있습니다.

증가하는 인지도 및 조기 진단 노력

공공 부문의 계발 활동으로 진단까지의 기간이 기존의 7년에서 단축되고 있습니다. 호주에서는 8,719만 달러를 투자한 국가 행동 계획을 통해 전문의 진료소와 환자 교육 프로그램을 확대하고 있습니다. 세계보건기구(WHO)가 2024년 자궁내막증을 우선질환으로 지정함으로써 유럽과 북미에서는 정책의 조화와 보험코드 개정이 가속화되고 있습니다. Lyv의 앱과 같은 디지털 증상 추적기는 고위험 프로파일을 경고하고 사용자가 전문의의 진료를 받도록 안내합니다. 머신러닝 알고리즘은 트리아지의 정확도를 높입니다. 또한 의과대학의 커리큘럼에 최초로 자궁내막증 교육이 포함되어, 오진이나 치료 부족 현상의 감소가 기대됩니다. 이러한 대책이 더하여 치료 대상 인구가 확대되고 처방전 발행수가 증가하고 있습니다.

평생 치료비 및 수술비의 높은 부담

환자의 부담액은 진단 전 단계에서는 중앙값 4,318달러였지만, 진단 후 6개월 이내에 1만 7,230달러로 300% 증가해, 가계나 보험 제도에 큰 부담을 가하는 것으로 나타났습니다. 월 1,000달러를 넘는 치료법에 대한 보험 적용 범위의 부족은 불평등을 심각화시키고 있지만, 가치 기반 계약이나 제조업체 지원 기금이 자가 부담금을 일부 상쇄하고 있습니다. 5년 이내의 수술 재발률이 40%에 육박하므로 재수술 비용이 발생하고, 또 응급 외래 진찰의 빈도는 대조군에 비해 60% 높아지고 있습니다. 이러한 상황은 적극적인 치료를 방해하고 임상 효과가 입증되었음에도 불구하고 고가의 치료법의 단기 보급을 제한할 수 있습니다.

부문 분석

2025년, 성선자극호르몬 방출 호르몬 요법은 자궁내막증 치료 시장에서 51.62%의 점유율을 차지했습니다. 이는 주사 장벽을 제거하고 우수한 증상 관리를 실현한 경구 길항제의 블록버스터적 진입에 뒷받침된 결과입니다. 북미 및 유럽에서 견조한 지불자의 수용이 프리미엄 가격을 유지하고 수익 측면에서 주도적 지위를 강화했습니다. 그러나 젊은 환자가 임신성 유지와 부작용 프로파일 감소를 선호하는 경향으로 인해 경구 피임약은 12.22%의 연평균 복합 성장률(CAGR)로 성장을 가속화하고 있습니다. 게다가, 질병 개질 효과는 제한적이지만 우선적으로 통증 완화를 제공하는 NSAIDs(비스테로이드성 항염증제)도 시장 확대에 기여하고 있습니다. 저에스트로겐 부작용을 완화하는 병용 요법으로의 전환은 호르몬과 비호르몬 기반 개발기업 간의 전략적 제휴를 촉진하고 경쟁 환경의 재균형이 도래하고 있음을 시사합니다.

향후 전망으로는 프로락틴 수용체 길항제, 대사 조절제, 칸나비노이드 제제 등 혁신적인 파이프라인이 주목받고 있습니다. 이들은 전신의 호르몬 억제 없이 질병 통제를 실현할 잠재력을 가지고 있습니다. HMI-115 및 디클로로아세트산염과 같은 약물을 둘러싼 임상적 진전은 치료 옵션의 다양화를 가져오고, 궁극적으로 GnRH 제제가 직면하는 위험을 감소시킬 수 있습니다. 골밀도에 대한 우려가 관리 가능한 범위로 수렴하면 자궁내막증 치료 시장은 증상 중증도, 임신 희망 유무, 병존 질환 프로파일에 따라 다양한 치료 포트폴리오를 유지할 것으로 예측됩니다.

2025년에는 진단 사례의 41.86%가 표층성 복막 병변이었으며 정기적인 복강경 검사에 의한 조기 발견이 이를 뒷받침했습니다. 동시에 영상 진단 프로토콜의 개선에 의해 심부 침윤성 질환의 인식도도 향상되어 정교화된 MRI 병기 분류와 전문적인 수술 기술의 뒷받침으로 11.71%의 연평균 복합 성장률(CAGR)로 진전하고 있습니다. 제약기업은 병변의 깊이를 바탕으로 임상시험을 층별화하여 표현형별 효능의 차이를 입증하고 있습니다.

자궁내막종은 재발 위험이 높기 때문에 수술 건수가 안정적이지만, 고강도 집속 초음파나 표적 나노입자 절제 등의 비침습적 치료법이 연구 중입니다. 수많은 병변 중에서도 골반외 병변은 정밀 진단의 대처에 의해 새로운 주목을 받고 있으며 바이오마커에 근거한 치료 선택의 시험적 기반을 제공합니다. 교차 부문 데이터 통합은 예후 알고리즘을 정교화하여 향후 규제 당국에 대한 신청에 도움이 될 것으로 기대됩니다.

지역별 분석

북미는 2025년 수익의 41.58%를 차지하였으며, 선진적인 환급 제도, 강력한 지원 네트워크, 경구 GnRH 길항제의 조기 도입에 뒷받침되고 있습니다. 바이든 행정부의 여성 건강 연구에 대한 2억 달러 투자는 정밀의료의 기초 정비를 가속화하고 있습니다. 그러나 보험 격차는 여전히 존재하며, 흑인 환자는 자궁내막증 관련 통증과 병존 질환에 대한 처방을 적게 받고 있기 때문에 지속적인 공정성 과제가 부각되고 있습니다. 원격 의료는 지방 격차를 축소하고 있지만, 인프라 격차가 완전한 보급을 방해하고 있습니다.

아시아태평양은 가장 성장이 현저한 시장으로 의료 시스템 확대, 도시로의 인구 이동, 계발활동 강화를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 13.05%로 확대될 전망입니다. 15%에 가까운 유병률은 치료되지 않은 환자층이 여전히 크고 현대 생식 의료 동향에 의해 더욱 확대되고 있음을 나타냅니다. 일본, 한국, 호주에서는 규제 경로의 조화가 진행되고 승인 사이클이 단축되고 있는 한편, 중국에서는 전통적인 한방 프로토콜과 의약품 치료를 통합하여 문화에 맞는 의료 모델이 제공되고 있습니다. 다국적 기업과 현지 제조업체와의 전략적 제휴에 의해 지방 도시(Tier 2 도시)에서의 유통이 확대되고 있습니다.

유럽에서는 광범위한 접근이 특징인 각국의 의료 예산이 제약이 되는 성숙한 수요 구조가 유지되고 있습니다. 유럽 의약품청(EMA)은 회원국 간의 의약품 접근을 효율화하고 있지만, 환급 정책의 차이로 인해 국가별 출시 시기가 지연될 가능성이 있습니다. 영국의 EU 탈퇴(브렉시트)는 영국과 유럽 대륙 간의 규제 무결성을 계속 복잡하게 하고 있으며, 기업은 이중 신청 전략을 유지할 수밖에 없습니다. 중동 및 아프리카에서는 민간 보험 가입률 상승과 걸프 국가에서의 신흥 전문 의료 센터 프로그램을 통해 점진적인 성장이 나타나고 있습니다. 브라질을 필두로 하는 남미에서는 치료 비용을 줄이고 보급을 촉진하는 중앙 조달 모델이 전개되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 가임기 여성에서의 유병률의 상승

- 높아지는 의식과 조기 진단 대처

- GnRH 길항제의 발매

- 펨텍 원격 모니터링 플랫폼의 도입 급증

- 비호르몬계 연구개발 및 파이프라인에 대한 벤처 자금 조달

- 정부의 자궁내막증 대책

- 억제요인

- 평생 치료비 및 수술비의 높은 부담

- 부작용 및 장기 호르몬 사용에 의한 골밀도 저하

- 처방전에 대한 접근에서 인종적, 사회 경제적 격차

- 전문 외과의 부족으로 12개월 이상의 대기 기간 발생

- 규제 상황

- 파이프라인 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 약제 계열별

- 비스테로이드성 항염증제(NSAIDs)

- 경구 피임약

- 성선자극호르몬 방출 호르몬

- 기타 약제 계열

- 자궁내막증 유형별

- 표층성 복막 자궁내막증

- 자궁내막종

- 심부 침윤성 자궁내막증

- 기타 유형

- 치료 유형별

- 통증 관리제

- 호르몬 요법

- 투여 경로별

- 경구

- 주사제

- 기타

- 유통 채널별

- 병원 약국

- 소매점 및 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AbbVie Inc.

- Bayer AG

- Pfizer Inc.

- Myovant Sciences/Sumitomo Pharma

- Organon & Co.

- Eli Lilly & Co.

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

- Cipla Ltd.

- TerSera Therapeutics

- AstraZeneca

- Takeda Pharmaceutical

- Neurocrine Biosciences

- ObsEva SA

- Gedeon Richter Plc

- Sandoz AG

제7장 시장 기회 및 미래 전망

CSM 26.01.21The Endometriosis Treatment Market market is expected to grow from USD 1.77 billion in 2025 to USD 1.97 billion in 2026 and is forecast to reach USD 3.37 billion by 2031 at 11.34% CAGR over 2026-2031.

Rising disease prevalence, sustained public-health campaigns, and a wave of regulatory approvals for oral gonadotropin-releasing hormone (GnRH) antagonists are setting a new treatment standard. Venture-capital inflows into non-hormonal pipelines, the proliferation of FemTech platforms, and government-funded action plans are expanding patient reach while reshaping competitive strategies. Meanwhile, diagnostic delays, high lifetime costs, and specialist shortages continue to temper uptake, steering innovators toward digital triage tools and minimally invasive care pathways that can bridge access gaps.

Global Endometriosis Treatment Market Trends and Insights

Rising Prevalence Among Reproductive-Age Women

More than 190 million women now live with endometriosis worldwide, and prevalence among Asian populations stands near 15%, markedly higher than the 5-10% range reported in Western cohorts. The demographic trend toward delayed parenthood, coupled with urban lifestyle shifts, is enlarging the at-risk population base in emerging markets. Productivity losses and excess healthcare utilization frame a USD 200 billion global economic burden that has prompted pharmaceutical enterprises to create dedicated women's-health divisions. Environmental research linking phthalate exposure to symptom aggravation is incentivizing new metabolic and environmental-medicine approaches. Stakeholders are intensifying epidemiological surveillance to quantify sub-regional hotspots, a strategy expected to refine market-entry decisions over the long term.

Growing Awareness and Earlier Diagnosis Initiatives

Public-sector outreach is compressing the historic seven-year diagnostic lag. Australia's National Action Plan, backed by AUD 87.19 million, is scaling specialist GP clinics and patient-education programs. The World Health Organization's 2024 declaration elevating endometriosis to priority-condition status has galvanized policy harmonization and insurance-coding revisions across Europe and North America. Digital symptom trackers such as Lyv's app flag high-risk profiles and direct users toward specialist care, with machine-learning algorithms boosting triage accuracy. Medical-school curricula are integrating endometriosis modules for the first time, a move likely to diminish misdiagnosis and under-treatment. Collectively, these measures are enlarging the treated population and stimulating prescription volumes.

High Lifetime Treatment and Surgery Cost Burden

Median patient spending rises from USD 4,318 in the pre-diagnosis phase to USD 17,230 within six months post-diagnosis, a 300% escalation that strains household budgets and payer systems. Coverage gaps for therapies priced above USD 1,000 per month intensify inequities, although value-based contracts and manufacturer assistance funds are partly offsetting out-of-pocket exposure. Surgical recurrence rates approaching 40% within five years add repeat procedure costs, while emergency-room visits occur 60% more frequently than in matched controls. These dynamics deter aggressive management and may limit near-term uptake of premium therapies despite demonstrable clinical benefits.

Other drivers and restraints analyzed in the detailed report include:

- Launch of GnRH Antagonist Class

- Surge in FemTech Remote-Monitoring Platforms

- Limited Specialist Surgeons Driving Wait-Times to More Than 12 Months

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gonadotropin-releasing hormone therapies captured 51.62% of Endometriosis treatment market share in 2025, buoyed by the blockbuster entry of oral antagonists that removed injection barriers and delivered superior symptom control. Robust payer acceptance in North America and Europe sustained premium pricing, reinforcing revenue leadership. However, oral contraceptives are accelerating at a 12.22% CAGR as younger patients prioritize fertility preservation and lower adverse-event profiles. Market expansion is additionally shaped by NSAIDs providing first-line pain relief despite limited disease-modifying effect. The shift toward combination regimens that temper hypoestrogenic side effects is fostering strategic alliances between hormonal and non-hormonal developers, signaling an impending competitive re-balancing.

Looking ahead, innovation pipelines spotlight prolactin-receptor antagonists, metabolic modulators, and cannabinoid formulations, all of which promise disease control without systemic hormone suppression. Clinical momentum around agents such as HMI-115 and dichloroacetate could diversify therapeutic options, ultimately reducing the class risk faced by GnRH incumbents. Should bone-density concerns remain manageable, the Endometriosis treatment market is expected to maintain a heterogeneous portfolio that caters to symptom severity, fertility intent, and co-morbid profile.

Superficial peritoneal lesions constituted 41.86% of diagnosed cases in 2025, benefiting from earlier detection through routine laparoscopy. Improved imaging protocols have simultaneously elevated recognition of deeply infiltrating disease, which is advancing at an 11.71% CAGR on the back of refined MRI staging and specialized surgical techniques. Pharmaceutical sponsors are stratifying clinical trials by lesion depth to document differential efficacy across phenotypes.

Endometriomas maintain steady surgical volumes due to high recurrence risk, yet non-invasive modalities such as high-intensity focused ultrasound and targeted nanoparticle ablation are under investigation. Rare extrapelvic manifestations, though numerically small, are receiving newfound attention through precision-diagnostic initiatives, offering a test-bed for biomarker-based treatment assignment. Cross-type data integration is anticipated to refine prognostic algorithms and inform future regulatory submissions.

The Endometriosis Treatment Market Report is Segmented by Drug Class (NSAIDs, Gonadotropin Releasing Hormone, and More), Endometriosis Type (Superficial Peritoneal, and More), Treatment Type (Pain Management Drugs, and More), Route of Administration (Oral, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 41.58% of 2025 revenue, buoyed by advanced reimbursement frameworks, strong advocacy networks, and early adoption of oral GnRH antagonists. The Biden administration's USD 200 million investment in women's-health research is fast-tracking precision-medicine conduits. Yet insurance disparities persist, with Black patients receiving fewer prescriptions for endometriosis-related pain and comorbid conditions, highlighting an ongoing equity challenge. Telehealth is narrowing rural gaps, although infrastructure gaps restrain full penetration.

Asia-Pacific is the fastest-growing arena, advancing at a 13.05% CAGR through 2031 on the back of healthcare system expansion, urban migration, and heightened awareness campaigns. Prevalence standing near 15% underscores a large untreated pool that modern fertility trends continue to enlarge. Harmonized regulatory pathways in Japan, South Korea, and Australia are shortening approval cycles, while China's integration of traditional herbal protocols with pharmaceutical regimens offers culturally attuned care models. Strategic collaborations between multinational firms and local manufacturers are scaling distribution across tier-two cities.

Europe retains a mature demand profile characterized by broad access but constrained national health budgets. The European Medicines Agency streamlines drug access across member states, yet divergent reimbursement policies can lengthen country-level launch timelines. Brexit continues to complicate regulatory alignment between the United Kingdom and continental Europe, prompting companies to maintain dual submission strategies. Middle East and Africa show incremental gains driven by rising private insurance coverage and emerging center-of-excellence programs in the Gulf. South America, led by Brazil, is rolling out centralized procurement models that lower therapy costs and stimulate uptake.

- Abbvie

- Bayer

- Pfizer

- Myovant Sciences / Sumitomo Pharma

- Organon

- Eli Lilly and Company

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Cipla

- TerSera Therapeutics

- AstraZeneca

- Takeda Pharmaceuticals

- Neurocrine Biosciences

- ObsEva SA

- Gedeon Richter Plc

- Sandoz Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Among Reproductive-Age Women

- 4.2.2 Growing Awareness and Earlier Diagnosis Initiatives

- 4.2.3 Launch of GnRH Antagonist Class

- 4.2.4 Surge in FemTech Remote-Monitoring Platforms

- 4.2.5 Venture Funding for Non-Hormonal R&D Pipelines

- 4.2.6 Government Endometriosis Action Plans

- 4.3 Market Restraints

- 4.3.1 High Lifetime Treatment and Surgery Cost Burden

- 4.3.2 Adverse Effects / Bone-Density Loss from Long-Term Hormone Use

- 4.3.3 Racial and Socio-Economic Disparities in Prescription Access

- 4.3.4 Limited Specialist Surgeons Driving Wait-Times to More Than 12 Months

- 4.4 Regulatory Landscape

- 4.5 Pipeline Analysis

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Drug Class

- 5.1.1 NSAIDs

- 5.1.2 Oral Contraceptives

- 5.1.3 Gonadotropin Releasing Hormone

- 5.1.4 Other Drug Classes

- 5.2 By Endometriosis Type

- 5.2.1 Superficial Peritoneal Endometriosis

- 5.2.2 Endometriomas

- 5.2.3 Deeply Infiltrating Endometriosis

- 5.2.4 Other Types

- 5.3 By Treatment Type

- 5.3.1 Pain Management Drugs

- 5.3.2 Hormone Therapy

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Injectable

- 5.4.3 Others

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail and Drugstores

- 5.5.3 Online Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Bayer AG

- 6.3.3 Pfizer Inc.

- 6.3.4 Myovant Sciences / Sumitomo Pharma

- 6.3.5 Organon & Co.

- 6.3.6 Eli Lilly & Co.

- 6.3.7 Sun Pharmaceutical Industries

- 6.3.8 Teva Pharmaceutical Industries

- 6.3.9 Cipla Ltd.

- 6.3.10 TerSera Therapeutics

- 6.3.11 AstraZeneca

- 6.3.12 Takeda Pharmaceutical

- 6.3.13 Neurocrine Biosciences

- 6.3.14 ObsEva SA

- 6.3.15 Gedeon Richter Plc

- 6.3.16 Sandoz AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment