|

시장보고서

상품코드

1906211

산업용 베어링 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Industrial Bearings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

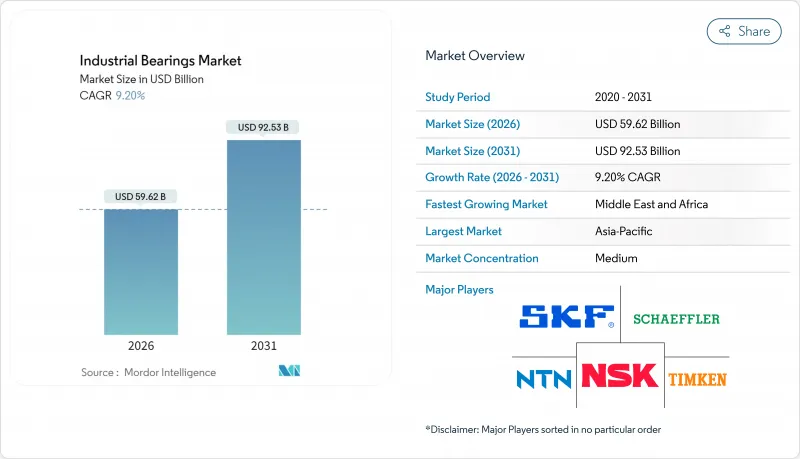

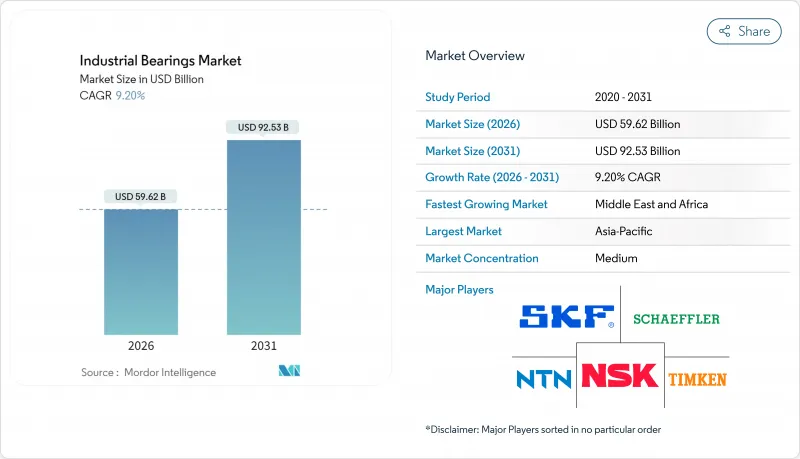

산업용 베어링 시장은 2025년 546억 달러에서 2026년에는 596억 2,000만 달러로 성장할 것으로 예측되고, 2026-2031년에 걸쳐 CAGR 9.2%로 성장을 지속하여 2031년까지 925억 3,000만 달러에 이를 전망입니다.

이 성장은 운송 및 공장 장비 전반에 걸친 전기화 확대, 가속화되는 자동화 도입, 그리고 고성능 기계 부품이 요구되는 인프라 업그레이드를 반영합니다. 센서, 소형 전자 장치 및 무선 연결 기능을 갖춘 스마트 베어링은 유지보수를 사후 대응형에서 예측형으로 전환하여 자산 가동 시간을 높이고 계획되지 않은 가동 중단을 줄입니다. 제조업체들은 또한 전기차와 산업용 로봇의 에너지 효율을 개선하기 위해 경량 소재와 저마찰 설계를 추구하고 있습니다. 풍력, 수소 및 반도체 프로젝트에 대한 지속적인 자본 지출은 세계의적으로 더 가혹하고 빠르며 청정한 환경에서 작동하는 특수 고하중·고정밀 베어링 수요를 더욱 증가시킵니다.

세계의 산업용 베어링 시장 동향 및 인사이트

자동차 및 EV 생산의 회복 경향

세계의 경차 생산 대수는 2025년 8,960만대까지 증가할 것으로 예측되고 있으며, 전기차 모델이 판매량의 25%를 차지할 것으로 예상됩니다. 전기차 트랙션 모터에는 잔류 전류 침식을 완화하는 전기 절연 베어링이 필요합니다. 듀폰의 베스펠(Vespel) 폴리이미드 인서트는 완전 세라믹 하이브리드 대비 비용을 절감하면서도 고온을 견딥니다. 내연기관(ICE) 및 전기차 베어링을 위한 이중 생산 라인을 구축한 제조사는 기존 수요를 안정적으로 유지하면서 새로운 전기 파워트레인 물량을 확보할 수 있습니다.

예측 유지보수 지원 스마트 베어링의 급속한 채택

하우징에 통합된 무선 센서 패키지가 진동, 온도, 윤활 상태를 지속적으로 모니터링합니다. 셰플러의 OPTIME 생태계는 수동 점검을 줄이고 회전 자산에 대한 물리적 접근을 제한해 안전성을 높이는 변화를 보여줍니다. AI 분석과 결합 시, 협동 로봇 도입으로 조립 시간 30% 단축과 품질 15% 향상을 보고하는 공장들이 있습니다. 데이터 중심 제품으로의 전환은 반복적 서비스 수익을 창출하는 동시에 저가 모방업체의 진입 장벽을 높입니다.

합금 및 에너지 가격의 변동이 이익률을 압박

니켈 가격 급등과 에너지 할증료 변동은 원자재 비용 변동성을 가속화하여, 할증료가 4년 만에 최저 수준임에도 불구하고 총마진을 잠식하고 있습니다. 중국 수입 화물에 부과되는 컨테이너 할증료는 운송비를 상승시키는 반면, 미국 철강 관세는 현물 구매 옵션을 제한하고 제철소 납기 기간을 연장시킵니다. 다중 공급처 계약과 헤지된 에너지 공급을 보유한 기업들은 단일 공급처 경쟁사보다 우수한 성과를 내고 있습니다.

부문 분석

볼 베어링은 자동차 부품, 산업용 모터 및 가전제품에 폭넓게 적용 가능하여 2025년 산업용 베어링 시장의 41.55%를 차지했습니다. 롤러 베어링은 충격 하중이 주를 이루는 광산 및 건설 기계 분야에서 여전히 선호됩니다. 플레인 베어링은 부식성 해양 및 화학 환경에서 사용됩니다. 자기 베어링은 무유식 작동으로 마모를 제거하고 수소 압축기 및 eVTOL 터빈에서 더 높은 회전 속도를 가능하게 하여 17.85%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 틈새 시장을 대표합니다. NSK의 도시 항공 이동성용 가스터빈 발전기 솔루션은 항공우주 분야 초기 진출을 부각합니다(ns.com). 업윙 에너지의 수동형 자기 방사형 설계는 금속 간 접촉을 제거해 지하 펌프 수명을 연장하며, 산업 간 적용 가능성을 보여줍니다

마찰 없는 시스템에 대한 수요 증가가 자기 부상 부문의 매출 급증을 뒷받침하지만, 소재 비용과 정교한 제어 전자장치 요구사항으로 인해 프리미엄 응용 분야를 넘어선 광범위한 보급은 여전히 제한적입니다. OEM이 상태 모니터링 센서를 통합함에 따라, 자기 유닛은 전류, 온도 및 진동 데이터를 장비 제어 루프에 직접 내장할 수 있어 기계 및 전자 기술 모두를 숙달한 공급업체가 더 높은 마진을 확보할 수 있습니다.

합금강은 2025년 산업용 베어링 시장의 67.10%를 차지했으며, 경쟁력 있는 비용으로 세계의 용해 능력, 가공성 및 피로 저항성의 혜택을 받았습니다. 세라믹 제품의 산업용 베어링 시장 규모는 여전히 작지만, 전기차 절연 수요와 고속 스핀들 요구에 힘입어 2031년까지 연평균 13.85% 성장률을 기록할 전망입니다. 연구에 따르면 첨단 금속 기질 복합재 정압 베어링은 우수한 열전도성을 제공하여 경량화되면서도 초정밀 가공을 지원합니다.

하이브리드 강-세라믹 설계는 실리콘 질화물 구름체와 경화강 레이스를 결합해 비용과 성능의 균형을 이루며, 전기 부식이 문제인 풍력 터빈 발전기에서의 채택을 가속화하고 있습니다. 폴리머 및 복합 케이지는 화학 세척을 견디고 외부 윤활을 제거하여 위생 규정을 준수하기 때문에 식품 등급 펌프 및 제약 믹서 시장에서 점유율을 확대하고 있습니다.

지역별 분석

아시아태평양 지역은 중국의 대규모 OEM 기반과 인도의 인프라 확장에 힘입어 2025년 산업용 베어링 시장 점유율 46.60%를 유지했습니다. SKF의 닝보 공장 확장 및 R&D 허브 구축과 같은 현지화 전략은 리드 타임을 단축하고 지역 표준에 맞춰 설계를 맞춤화합니다. 일본은 전자제품 조립 및 수술용 로봇에 필요한 소형화 및 고정밀 베어링 분야에서 리더십을 유지하는 반면, 한국과 대만은 반도체 메가팹 투자로 수요를 촉진합니다. 기업들이 비용 경쟁력 있는 노동력과 새로 체결된 지역 무역 협정을 활용함에 따라 아세안(ASEAN)의 성장이 가속화됩니다.

북미는 1조 4,000억 달러 규모의 회귀투자와 CHIPS법 및 인프라법 등의 공공 부문 지원을 배경으로 세계 평균을 웃도는 성장을 보이고 있습니다. 국내 생산자들은 규모를 확대하지만 기술 인력 부족으로 가동 일정 연장이 불가피한 가운데, 멕시코 수입품이 일시적 공급 공백을 메우고 있습니다. 유럽은 지속가능성과 고효율 기계 장비를 우선시하지만, 독일의 산업 주문 부진으로 단기 물량이 위축됩니다. EU 정책은 순환경제형 베어링을 촉진하며, SKF의 레이저 재도금 순환 성능 시리즈가 이를 입증합니다.

중동 및 아프리카는 걸프 국가들이 석유화학, 알루미늄, 재생에너지 프로젝트로 다각화함에 따라 연평균 12.45% 성장률을 전망합니다. UAE의 자유무역지대 유통업체들은 지역 통합 허브 역할을 수행하며, 사우디아라비아의 현지화 목표는 합작 투자 기회를 열어줍니다. 남미는 광업 주도형 수요 지역을 제공하지만, 통화 변동성과 정치적 위험으로 유연한 가격 책정 및 신용 조건이 필요합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차 및 전기자동차(EV) 생산의 회복세

- 예측 유지보수 대응형 스마트 베어링의 급속한 보급

- 아시아태평양 및 유럽의 육상 풍력 터빈 확대

- 북미의 산업기기 공급망의 국내 회귀

- 수소 압축기용 자성 및 세라믹 베어링의 틈새 수요(보고 부족)

- 저마찰 소형 베어링이 필요한 로봇 및 협동 로봇의 급증(보고 부족)

- 시장 성장 억제요인

- 변동성 있는 합금 및 에너지 가격으로 인한 마진 압박

- 자동차 ICE-EV 전환으로 인한 엔진 관련 베어링 수요 감소

- 미국 및 EU의 중국산 베어링에 대한 지적재산권 기반 수입 제한(보고 부족)

- 항공우주 산업에서 소형 롤러 베어링을 대체하는 적층제조 부싱(보고 부족)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 베어링 유형별

- 볼 베어링

- 롤러 베어링

- 플레인 베어링

- 자기 베어링

- 기타 베어링

- 소재별

- 합금강

- 세라믹

- 폴리머/복합재료

- 하이브리드

- 최종 사용자 업계별

- 자동차

- 항공우주

- 에너지(풍력, 석유 및 가스, 수력)

- 광업 및 금속

- 건설 및 중기

- 식품 및 음료

- 자재관리 및 물류

- 기타 산업

- 용도별

- 회전 기기(모터, 펌프)

- 직동 시스템

- 엔진, 변속기 및 구동 시스템

- 섀시 및 휠 허브

- 정밀 기기 및 계측 기기

- 판매 채널별

- OEM

- 애프터마켓/MRO

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AB SKF

- NSK Ltd.

- NTN Corporation

- The Timken Company

- JTEKT Corporation

- MinebeaMitsumi Inc.

- Regal Rexnord Corporation

- RBC Bearings Inc.

- THB Bearings Co., Ltd.

- HKT Bearings Ltd.

- Schaeffler AG

- Nachi-Fujikoshi Corp.

- CandU Group Co., Ltd.

- Federal-Mogul LLC(DRiV)

- THK Co., Ltd.

- SKF Motion Technologies

- Harbin HRB Bearing Group Co., Ltd.

- LYC Bearing Corporation

- KG International FZCO

- Others(validated)

제7장 시장 기회와 장래의 전망

HBR 26.01.26The industrial bearings market is expected to grow from USD 54.6 billion in 2025 to USD 59.62 billion in 2026 and is forecast to reach USD 92.53 billion by 2031 at 9.2% CAGR over 2026-2031.

Growth reflects rising electrification across transport and factory equipment, accelerating automation adoption, and infrastructure upgrades that demand higher-performance mechanical components. Smart bearings equipped with sensors, miniaturised electronics and wireless connectivity shift maintenance from reactive to predictive, raising asset uptime and reducing unplanned downtime. Manufacturers also pursue lightweight materials and low-friction designs to improve energy efficiency in electric vehicles and industrial robots. Sustained capital expenditure in wind, hydrogen and semiconductor projects further increases demand for specialised, high-load and high-precision bearings that operate in harsher, faster and cleaner environments worldwide.

Global Industrial Bearings Market Trends and Insights

Rising Automotive & EV Production Rebound

Global light-vehicle output is forecast to edge up to 89.6 million units in 2025, with electric models accounting for 25% of sales. EV traction motors require electrically insulated bearings that mitigate stray-current erosion; DuPont's Vespel polyimide inserts lower cost versus full ceramic hybrids while tolerating high temperatures. Producers that build dual-capability lines for ICE and EV bearings benefit from steady legacy demand while capturing new e-powertrain volumes.

Rapid Adoption of Predictive-Maintenance-Ready Smart Bearings

Wireless sensor packages integrated into housings now monitor vibration, temperature and lubrication regimes continuously. Schaeffler's OPTIME ecosystem illustrates the shift, cutting manual inspection and raising safety by limiting physical access to rotating assets. When paired with AI analytics, factories report 30% assembly-time reduction and 15% quality gains from collaborative-robot deployments. The move to data-rich products creates recurring service revenue while raising qualification hurdles for low-cost imitators.

Volatile Alloy & Energy Prices Squeezing Margins

Nickel price spikes and energy-surcharge swings push input-cost volatility that erodes gross margins despite surcharges peaking at four-year lows. Container surcharges on inbound Chinese shipments inflate freight costs, while US steel tariffs limit spot options and lengthen mill lead times. Firms with multi-sourcing contracts and hedged energy supply outperform single-source competitors.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of On-Shore Wind Turbines

- Re-shoring of Industrial Equipment Supply Chains

- Automotive ICE-to-EV Transition Reducing Engine-Related Bearing Volumes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ball bearings held 41.55% of the industrial bearings market in 2025 thanks to broad suitability for automotive accessories, industrial motors and consumer appliances. Roller bearings remain preferred in mining and construction machinery where shock loads dominate. Plain bearings serve corrosive marine and chemical duties. Magnetic bearings represent the fastest-growing niche at 17.85% CAGR as oil-free operation eliminates wear and enables higher rotational speeds in hydrogen compressors and eVTOL turbines. NSK's gas-turbine generator solution for urban air mobility highlights early aerospace traction nsk.com. Upwing Energy's passive magnetic radial design extends downhole pump life by removing metal-to-metal contact, illustrating cross-industry adoption potential.

Growing demand for friction-less systems underpins the magnetic segment's revenue leap, although material cost and sophisticated control-electronics requirements still limit widespread deployment beyond premium applications. As OEMs integrate condition-monitoring sensors, magnetic units can embed current, temperature and vibration data directly into equipment control loops, positioning suppliers that master both mechanics and electronics for higher margins.

Alloy steel comprised 67.10% of the industrial bearings market in 2025, benefiting from global melt capacity, machinability and fatigue resistance at competitive cost. The industrial bearings market size for ceramic products remains smaller but climbs at 13.85% CAGR through 2031 on the back of EV insulation needs and high-speed spindle requirements. Research shows advanced metal-matrix-composite hydrostatic bearings deliver superior thermal conductivity, supporting ultraprecision machining at reduced weight.

Hybrid steel-ceramic designs blend silicon-nitride rolling elements with hardened-steel races to balance cost and performance, accelerating uptake in wind-turbine generators where electrical corrosion is problematic. Polymer and composite cages gain share in food-grade pumps and pharmaceutical mixers because they endure chemical washdowns and eliminate external lubrication, complying with hygiene codes.

The Industrial Bearings Market Report is Segmented by Bearing Type (Ball Bearings, Roller Bearings, Plain Bearings, and More), Material (Alloy Steel, Ceramic, Polymer/Composite, Hybrid), End-User Industry (Automotive, Aerospace, Energy, and More), Application (Rotating Equipment, Linear Motion Systems, Engine/Transmission/Driveline, and More), Sales Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 46.60% industrial bearings market share in 2025, propelled by China's large-scale OEM base and India's infrastructure build-out. Localization strategies such as SKF's expanded Ningbo plant and R&D hub shorten lead times and customise designs for regional standards. Japan sustains leadership in miniaturised and high-accuracy bearings needed for electronics assembly and surgical robotics, while South Korea and Taiwan boost demand via semiconductor megafab investments. ASEAN growth accelerates as companies leverage cost-competitive labour and newly inked regional trade pacts.

North America grows above global average on the back of USD 1.4 trillion reshoring commitments and public-sector incentives like the CHIPS and Infrastructure acts. Domestic producers scale up, yet skill shortages lengthen ramp-up schedules; meantime, imports from Mexico fill interim supply gaps. Europe prioritises sustainability and high-efficiency machinery, but industrial order softness in Germany tempers near-term volume. EU policy pushes circular-economy bearings, evidenced by SKF's laser-reclad circular performance series.

The Middle East & Africa present 12.45% CAGR prospects as Gulf nations diversify into petrochemical, aluminium and renewable projects. Free-zone distributors in UAE serve as regional consolidation hubs, while localisation goals in Saudi Arabia open joint-venture opportunities. South America offers mining-driven pockets of demand, although currency volatility and political risk require flexible pricing and credit terms.

- AB SKF

- NSK Ltd.

- NTN Corporation

- The Timken Company

- JTEKT Corporation

- MinebeaMitsumi Inc.

- Regal Rexnord Corporation

- RBC Bearings Inc.

- THB Bearings Co., Ltd.

- HKT Bearings Ltd.

- Schaeffler AG

- Nachi-Fujikoshi Corp.

- CandU Group Co., Ltd.

- Federal-Mogul LLC (DRiV)

- THK Co., Ltd.

- SKF Motion Technologies

- Harbin HRB Bearing Group Co., Ltd.

- LYC Bearing Corporation

- KG International FZCO

- Others (validated)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising automotive and EV production rebound

- 4.2.2 Rapid adoption of predictive-maintenance?ready smart bearings

- 4.2.3 Expansion of on-shore wind turbines in APAC and Europe

- 4.2.4 Re-shoring of industrial equipment supply chains in North America

- 4.2.5 Niche demand for magnetic and ceramic bearings in hydrogen compressors (under-reported)

- 4.2.6 Surge in robotics and cobots requiring low-friction miniature bearings (under-reported)

- 4.3 Market Restraints

- 4.3.1 Volatile alloy and energy prices squeezing margins

- 4.3.2 Automotive ICE-to-EV transition reducing engine-related bearing volumes

- 4.3.3 IP-driven import restrictions on Chinese bearings in U.S. and EU (under-reported)

- 4.3.4 Additive-manufactured bushings replacing small roller bearings in aerospace (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Bearing Type

- 5.1.1 Ball Bearings

- 5.1.2 Roller Bearings

- 5.1.3 Plain Bearings

- 5.1.4 Magnetic Bearings

- 5.1.5 Other Bearings

- 5.2 By Material

- 5.2.1 Alloy Steel

- 5.2.2 Ceramic

- 5.2.3 Polymer / Composite

- 5.2.4 Hybrid

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace

- 5.3.3 Energy (Wind, Oil and Gas, Hydro)

- 5.3.4 Mining and Metals

- 5.3.5 Construction and Heavy Equipment

- 5.3.6 Food and Beverage

- 5.3.7 Material Handling and Logistics

- 5.3.8 Other Industries

- 5.4 By Application

- 5.4.1 Rotating Equipment (Motors, Pumps)

- 5.4.2 Linear Motion Systems

- 5.4.3 Engine, Transmission and Driveline

- 5.4.4 Chassis and Wheel Hubs

- 5.4.5 Precision and Instrumentation

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket / MRO

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AB SKF

- 6.4.2 NSK Ltd.

- 6.4.3 NTN Corporation

- 6.4.4 The Timken Company

- 6.4.5 JTEKT Corporation

- 6.4.6 MinebeaMitsumi Inc.

- 6.4.7 Regal Rexnord Corporation

- 6.4.8 RBC Bearings Inc.

- 6.4.9 THB Bearings Co., Ltd.

- 6.4.10 HKT Bearings Ltd.

- 6.4.11 Schaeffler AG

- 6.4.12 Nachi-Fujikoshi Corp.

- 6.4.13 CandU Group Co., Ltd.

- 6.4.14 Federal-Mogul LLC (DRiV)

- 6.4.15 THK Co., Ltd.

- 6.4.16 SKF Motion Technologies

- 6.4.17 Harbin HRB Bearing Group Co., Ltd.

- 6.4.18 LYC Bearing Corporation

- 6.4.19 KG International FZCO

- 6.4.20 Others (validated)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment