|

시장보고서

상품코드

1906227

유럽의 파사드 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Facade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

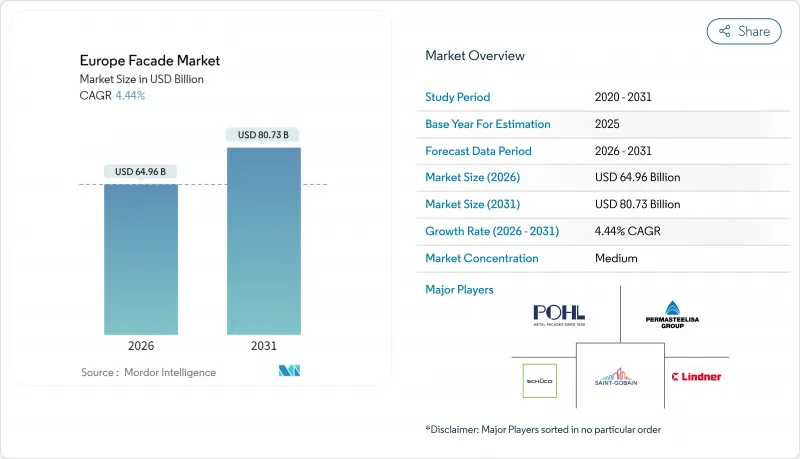

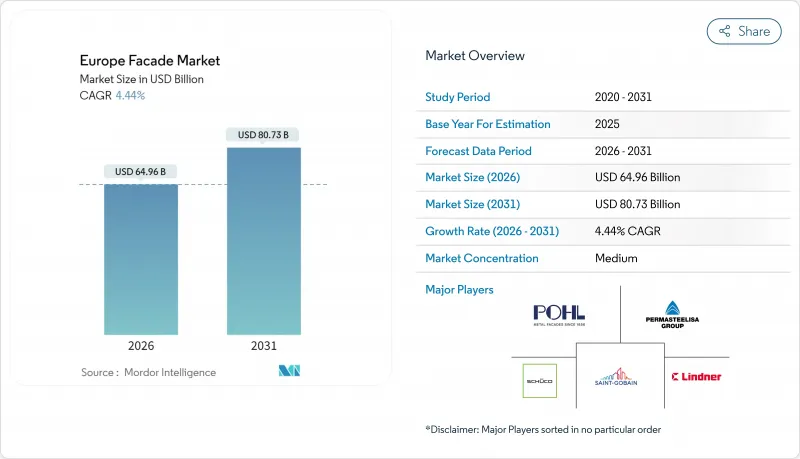

유럽의 파사드 시장은 2025년 622억 달러로 평가되었으며, 2026년 649억 6,000만 달러에서 2031년까지 807억 3,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 4.44%로 예상됩니다.

개보수 및 개조 수요가 주류를 차지하고 있으며 이는 그렌펠 타워 화재 이후 규제와 EU의 'Fit-for-55' 에너지 목표에 따라 건물의 외피 보수가 의무화되기 때문입니다. 상업 고객이 여전히 지출의 대부분을 차지하고 있지만, 하이퍼스케일 데이터센터 클러스터와 모듈식 오프사이트 건설이 주택 공급 체인을 재구축하는 가운데 주택 분야의 활동도 가속하고 있습니다. 경쟁은 규모보다는 기술적 차별화에 의해 정의되며, 파사드 전문 기업은 저탄소 알루미늄, 건축물 일체형 태양광 발전(BIPV), AI 대응 적응형 패널을 통합하여 제품화 탄소의 상한을 충족합니다. 재료비의 변동과 시공자 부족이 단기적인 기세를 억제하고 있지만, 지속적인 정책 압력으로 유럽의 주요 경제권 전체에서 수주 파이프라인은 견조하게 추이할 전망입니다.

유럽의 파사드 시장의 동향 및 인사이트

그렌펠 타워 화재 이후 EU 고층 건축물의 외벽 리모델링 급증

2017년의 비극 이후 방화 안전 규정이 강화되었고, 높이가 18m 이상인 건물의 소유자는 가연성 시스템을 교체해야만 했습니다. 보험사는 기존의 외피에 대한 보상을 제외하였기에 규제 준수는 필수 조건이 되었습니다. 독일은 2024년 발렌시아 아파트 화재 사고를 통해 영국의 자세를 본받고 프랑스는 건설 제품 규제의 갱신에 따라 파사드 시험을 강화하고 있습니다. 교체 의무화는 법적 책임이 비용 우려를 뛰어넘기 때문에 유럽의 파사드 시장을 건설업 전체의 하락으로부터 보호하고 개보수 주문의 안정성을 확보하고 있습니다.

'Fit for 55'에 근거한 2050년 넷 제로 외피 규제

건축물에 대한 에너지 성능 지침은 2030년까지 신축 건물에 대해 제로 에미션 기준 준수, 2050년까지 기존 건물의 대규모 개보수를 요구하고 있습니다. 프랑스의 RE2020은 640kg CO2eq/m2의 상한을 설정하였으며 이미 제품의 재설계 시기가 도래하였습니다. 리노베이션 물결은 3,500만 건물의 업그레이드를 목표로 하고 있으며, 파사드는 잠재적인 에너지 절약량의 약 35%를 담당하고 있습니다. 독일의 최신 건축 기준은 열교 현상이 없는 연결을 의무화하여 사양이 복잡해지고, 고급 커튼월과 통풍벽이 중요시되고 있습니다.

알루미늄 및 플로트 유리의 가격 변동

2024년 알루미늄은 1톤당 2,300-2,600달러로 거래되었으며, 플로트 유리의 가격은 10-15% 급등했습니다. 특수 점보 패널의 납기는 20주로 연장되어 프로젝트 스케줄에 지장을 주고 있습니다. 계약자는 비용 위험을 소유자에게 이전하는 에스컬레이션 조항을 계약에 통합하여 승인이 지연되고 이익률이 압박될 수 있습니다.

부문 분석

통기성 솔루션은 2025년 수익의 50.35%를 차지하였으며 4.78%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 이는 공기층을 형성하여 냉각 부하를 최대 25% 줄이기 때문입니다. 이 압도적인 점유율은 유럽의 파사드 시장이 성능과 규제 적합성을 통합하는 추세를 보여줍니다. 규제 당국이 열교 규제를 강화하는 가운데 자연 환기 및 습기 배출 기능을 갖춘 통풍 어셈블리는 고체 클래딩의 결로 문제를 극복합니다. BIPV 모듈과의 호환성이 매력을 높여 시공업체는 태양광 발전으로 인한 열을 방출하여 셀 효율을 보호할 수 있습니다. 비통기식 패널은 구조적 개입이 제한되는 역사적 건축물의 보수에 여전히 유용하지만, 성장률은 유럽의 파사드 시장 평균보다 낮습니다.

첨단 설계에는 스마트 루버, 동적 차광 시스템 및 센서 제어 기류 댐퍼가 포함되어 있습니다. 공장에서 생산되는 통기식 카세트는 오프사이트 동향에 맞추어 품질 보증 강화와 현장 공정 단축을 실현합니다. 방화 규제도 이러한 구조를 뒷받침하고 있습니다. 공동부가 열 완충재로서 기능해, 불꽃의 확산을 억제합니다. 이는 그렌펠 타워 화재 이후 특히 중시되는 특성입니다. 종합적으로, 이러한 구성은 사무실, 학교, 고층 주택에서 EU의 nZEB 기준 달성을 위한 최적의 선택으로 통기식 솔루션의 지위를 확고히 하고 있습니다.

커튼월 어셈블리는 2025년 44.60%의 시장 가치를 차지하였지만, 개보수 공사용으로 다기능 외장을 지정하는 건축가의 증가에 따라, 레인스크린 외장이 2031년까지 연평균 복합 성장률(CAGR) 4.83%로 추격할 전망입니다. 유럽의 레인스크린 외벽 시장은 세라믹 타일에서 도시의 생물 다양성을 높이는 이끼 착생용 바이오 수용성 콘크리트에 이르기까지 소재의 자유도가 높아지면서 성장하고 있습니다. 파노라마 유리 및 기밀성과 내진성이 요구되는 스카이라인 프로젝트에서는 커튼 월이 여전히 필수적입니다.

시장 혁신에는 일렉트로크로믹 유리, 통합형 태양광 발전, 현장에서 층고 높이의 패널 단위로 설치할 수 있는 단위화 시스템이 있습니다. ISO 12631 및 EN 13830 규격이 성능 시험을 주도하고 제조업체는 단열 및 차음 성능 향상을 요구받고 있습니다. 그 결과, 레인스크린 벤더는 모듈식 서브프레임과 재활용 가능한 브래킷을 실험하고 있으며, 이 범주를 단순한 비용 절감 방법이 아니라 지속가능성의 기반으로 자리매김하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- EU에서 고층 건축물에 대한 '그렌펠 화재 이후' 외피 개보수 급증

- 'Fit for 55'에 근거한 2050년 넷 제로 외피 규제

- 모듈식 오프사이트 파사드 제조의 보급 상황

- FLAP-D 클러스터의 하이퍼스케일 데이터센터 건설 붐

- 부가가치세(VAT) 경감 조치 및 고정가격임베디드제도(FIT)에 의한 BIPV 파사드의 보급 촉진

- CBAM(탄소국경조정제도)에 의한 저탄소 알루미늄의 국내 회귀

- 억제요인

- 알루미늄 및 플로트 유리의 가격 변동성

- 전문 파사드 시공자의 부족

- 가연성 시스템에 대한 보험 면책 조항

- EU 택소노미 및 지역 계획에 있어서의 매장 탄소량 상한

- 유럽의 파사드 구조 시스템 개요

- 가격 분석

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 공급자의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 소비자 행동 분석(건축가, 시공업자, 개발업자, 소유자)

- 지속가능성 동향

제5장 시장 규모 및 성장 예측

- 유형별

- 환기식

- 비환기식

- 기타

- 파사드 시스템 유형별

- 레인스크린 외벽

- 커튼월 시스템

- 기타

- 소재별

- 유리

- 금속

- 플라스틱 및 섬유

- 석재

- 기타

- 설치별

- 신축

- 개보수 및 개조 공사

- 최종 사용자별

- 상업

- 주택

- 기타

- 지역별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 북유럽 국가(스웨덴, 덴마크, 노르웨이, 핀란드)

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Permasteelisa Group

- Schuco International KG

- Saint-Gobain SA

- Lindner Group

- Reynaers Aluminium NV

- Kawneer(Arconic)Europe

- AluK Group

- Kingspan Group(Facade & Insulated Panels)

- Hydro Building Systems(Technal, Wicona)

- Yuanda Europe

- STO SE & Co. KGaA

- Etex Group-EOS Facades

- Sapa Building Systems

- Gartner(Permasteelisa)

- Trimo doo

- Glas Trosch Group

- AGC Glass Europe

- Focchi SpA

- Josef Gartner GmbH

- Alucraft Systems

제7장 시장 기회 및 미래 전망

CSM 26.01.21The Europe facade market was valued at USD 62.2 billion in 2025 and estimated to grow from USD 64.96 billion in 2026 to reach USD 80.73 billion by 2031, at a CAGR of 4.44% during the forecast period (2026-2031).

Renovation and retrofit demand dominate because post-Grenfell regulations and EU "Fit-for-55" energy targets impose mandatory envelope upgrades. Commercial clients still account for most spending, yet residential activity is accelerating as hyperscale data-center clusters and modular off-site construction reshape housing supply chains. Technological differentiation rather than raw scale defines competition, with facade specialists integrating low-carbon aluminum, building-integrated photovoltaics (BIPV), and AI-enabled adaptive panels to satisfy embodied-carbon caps. Material cost swings and installer shortages temper near-term momentum, but sustained policy pressure keeps the order pipeline resilient across core European economies.

Europe Facade Market Trends and Insights

Post-Grenfell Recladding Surge Across EU High-Rise Stock

Heightened fire-safety scrutiny after the 2017 tragedy forces owners of buildings above 18 m to replace combustible systems. Insurers have removed coverage for legacy cladding, making compliance non-negotiable. Germany mirrored the UK's stance following the 2024 Valencia apartment blaze, and France upgraded facade testing under Construction Products Regulation updates. The compulsory nature of replacement shields the Europe facade market from macro construction downturns because legal liability overrides cost concerns, ensuring steady retrofit orders.

Net-Zero-2050 Envelope Mandates Under "Fit-for-55"

The Energy Performance of Buildings Directive calls for all new structures to reach zero-emission status by 2030 and for deep retrofits of existing stock by 2050. France's RE2020 sets a 640 kg CO2eq/m2 ceiling that is already forcing product redesign. The renovation wave aims to upgrade 35 million buildings, with facades responsible for roughly 35% of potential energy savings. Germany's latest building code now requires thermal-bridge-free connections, raising specification complexity and favoring sophisticated curtain-wall and ventilated concepts.

Aluminum and Float-Glass Price Volatility

Aluminum traded between USD 2,300-2,600 per ton during 2024, while float-glass quotes soared 10-15%. Specialized jumbo-pane lead times stretched to 20 weeks, disrupting project schedules. Contractors incorporate escalation clauses that transfer cost risk to owners, which can stall approvals and compress margins.

Other drivers and restraints analyzed in the detailed report include:

- Modular Off-Site Facade Manufacturing Uptake

- Hyperscale Data-Center Build Boom in FLAP-D Clusters

- Certified Facade-Installer Labor Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ventilated solutions captured 50.35% of 2025 revenue and will expand at a 4.78% CAGR because they create an air cavity that lowers cooling loads by up to 25%. This dominant share underlines how the Europe facade market integrates performance and compliance. As regulators tighten thermal-bridge rules, ventilated assemblies, with natural airflow and moisture outflow, overcome condensation risks that plague solid claddings. Their compatibility with BIPV modules strengthens appeal, letting installers dissipate photovoltaic heat and protect cell efficiency. Non-ventilated panels still serve heritage retrofits where structural intervention is limited, but growth lags the Europe facade market average.

Advanced designs now embed smart louvers, kinetic shading, and sensor-driven airflow dampers. Factory-built ventilated cassettes dovetail with off-site trends, boosting quality assurance and shortening site programs. Fire-safety codes further support this architecture because the cavity acts as a thermal buffer that limits flame spread, a coveted attribute after Grenfell. Collectively, the configuration cements ventilated solutions as the go-to choice for meeting EU nZEB criteria in offices, schools, and high-rise housing.

Curtain-wall assemblies owned 44.60% of 2025 value, yet rainscreen cladding outpaces them with a 4.83% CAGR through 2031 as architects specify versatile skins for retrofits. The Europe facade market size for rainscreens is growing on the back of material freedom that stretches from ceramic tiles to bio-receptive concrete that nurtures moss for urban biodiversity. Curtain-wall incumbents remain indispensable in skyline projects that demand panoramic glazing, airtightness, and seismic tolerance.

Market innovations include electrochromic glazing, integrated photovoltaics, and unitized systems that arrive on site as complete story-height panels. ISO 12631 and EN 13830 standards steer performance testing, pushing makers to refine thermal and acoustic metrics. Consequently, rainscreen vendors now experiment with modular sub-frames and recyclable brackets, positioning the category as a sustainability platform rather than value engineering fallback.

The Europe Facade Market Report is Segmented by Type (Ventilated, Non-Ventilated, Others), Facade System Type (Rainscreen Cladding, Curtain-Wall Systems, Others), Material (Glass, Metal, Plastic & Fibers, and More), Installation (New Construction, Renovation & Retrofit), End-User (Commercial, Residential, Others), and Geography (Germany, UK, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Permasteelisa Group

- Schuco International KG

- Saint-Gobain S.A.

- Lindner Group

- Reynaers Aluminium NV

- Kawneer (Arconic) Europe

- AluK Group

- Kingspan Group (Facade & Insulated Panels)

- Hydro Building Systems (Technal, Wicona)

- Yuanda Europe

- STO SE & Co. KGaA

- Etex Group - EOS Facades

- Sapa Building Systems

- Gartner (Permasteelisa)

- Trimo d.o.o.

- Glas Trosch Group

- AGC Glass Europe

- Focchi SpA

- Josef Gartner GmbH

- Alucraft Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-Grenfell style recladding surge across EU high-rise stock

- 4.2.2 Net-zero-2050 envelope mandates under "Fit-for-55"

- 4.2.3 Modular off-site facade manufacturing uptake

- 4.2.4 Hyperscale data-centre build boom in FLAP-D clusters

- 4.2.5 VAT-relief & feed-in tariffs accelerating BIPV facades

- 4.2.6 CBAM-driven reshoring of low-carbon aluminium

- 4.3 Market Restraints

- 4.3.1 Aluminium & float-glass price volatility

- 4.3.2 Certified facade-installer labor shortage

- 4.3.3 Insurance exclusions for combustible systems

- 4.3.4 Embodied-carbon caps in EU taxonomy & local plans

- 4.4 Brief on Structural Systems Used in European Facades

- 4.5 Pricing Analysis

- 4.6 Value / Supply-Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

- 4.10 Consumer Behaviour Analysis (Architects, Contractors, Developers, Owners)

- 4.11 Sustainability Trends

5 Market Size & Growth Forecasts (Value, € billion)

- 5.1 By Type

- 5.1.1 Ventilated

- 5.1.2 Non-Ventilated

- 5.1.3 Others

- 5.2 By Facade System Type

- 5.2.1 Rainscreen Cladding

- 5.2.2 Curtain-Wall Systems

- 5.2.3 Others

- 5.3 By Material

- 5.3.1 Glass

- 5.3.2 Metal

- 5.3.3 Plastic & Fibres

- 5.3.4 Stone

- 5.3.5 Others

- 5.4 By Installation

- 5.4.1 New Construction

- 5.4.2 Renovation & Retrofit

- 5.5 By End-User

- 5.5.1 Commercial

- 5.5.2 Residential

- 5.5.3 Others

- 5.6 By Region

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Nordics (Sweden, Denmark, Norway, Finland)

- 5.6.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.4.1 Permasteelisa Group

- 6.4.2 Schuco International KG

- 6.4.3 Saint-Gobain S.A.

- 6.4.4 Lindner Group

- 6.4.5 Reynaers Aluminium NV

- 6.4.6 Kawneer (Arconic) Europe

- 6.4.7 AluK Group

- 6.4.8 Kingspan Group (Facade & Insulated Panels)

- 6.4.9 Hydro Building Systems (Technal, Wicona)

- 6.4.10 Yuanda Europe

- 6.4.11 STO SE & Co. KGaA

- 6.4.12 Etex Group - EOS Facades

- 6.4.13 Sapa Building Systems

- 6.4.14 Gartner (Permasteelisa)

- 6.4.15 Trimo d.o.o.

- 6.4.16 Glas Trosch Group

- 6.4.17 AGC Glass Europe

- 6.4.18 Focchi SpA

- 6.4.19 Josef Gartner GmbH

- 6.4.20 Alucraft Systems

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment