|

시장보고서

상품코드

1906245

로드 뱅크 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Load Bank - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

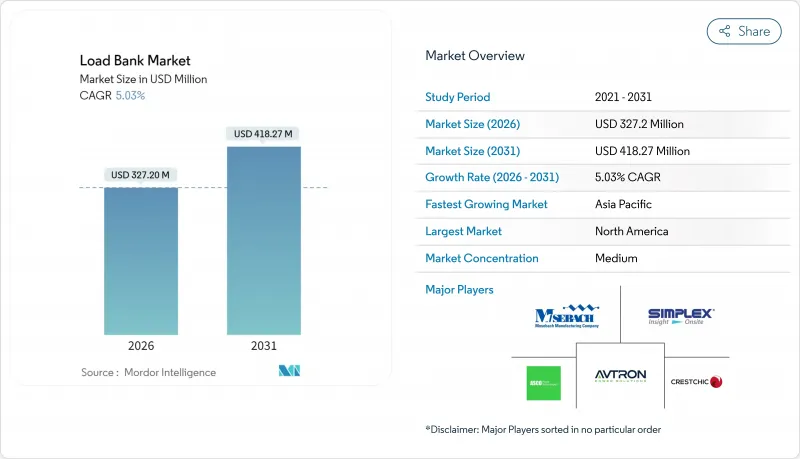

로드 뱅크 시장 규모는 2025년 3억 1,153만 달러로 평가되었고, 2026년에는 3억 2,720만 달러에 이르고, 2031년에는 4억 1,827만 달러로 성장할 것으로 예상됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.03%를 나타낼 전망입니다.

이러한 성장세는 하이퍼스케일 데이터센터의 확장, 안정성 검증이 필요한 재생에너지가 풍부한 전력망, 미션 크리티컬 시설에 대한 보다 엄격한 성능 요건에 기인합니다. 데이터센터 사업자는 전력밀도 기준을 늘리고 다단계 검증이 필요하며 로드 뱅크 서비스 제공업체의 대여 기회가 확대되고 있습니다. 신재생에너지의 통합은 풍력, 태양광, 에너지저장장치(ESS) 프로젝트의 동적 부하 프로파일을 시뮬레이션할 수 있는 저항성 및 리액티브 시스템 및 전자 시스템에 대한 수요를 추가하고 있습니다. 이에 반해 제조업체는 시험 에너지의 최대 96%를 회수하는 회생 설계로 대응하고 있어, 이 기능은 신규 전력 회사나 마이크로그리드 조달에 있어서 점점 요구되고 있습니다. 동시에 원재료 가격 상승과 프로젝트 단기 납기로 많은 구매자가 자산 경량형 렌탈 모델로 전환하고 있으며 로드 뱅크 시장 전체의 경쟁 전략에 영향을 미치고 있습니다.

세계 로드 뱅크 시장 동향과 인사이트

데이터센터의 급속한 용량 확장

2024년 데이터센터 건설 지출은 연간 315억 달러에 이르렀으며, 세계의 새로운 공간 파이프라인은 5,000만 평방 피트에 육박하고 있습니다. 하이퍼스케일 사업자는 현재 공장 출시부터 통합 시스템 검증까지 지속적인 수락 시험을 요구하고 있으며, 렌탈 로드 뱅크 이용률이 크게 상승하고 있습니다. 서비스 수준 계약을 유지하기 위해 유지 보수 기간 동안 일시적인 함대가 정기적으로 재배포되어 지속적인 수익을 창출합니다. AI 워크로드는 전력 밀도를 높이고 시설은 몇 메가 와트의 부하 테스트가 필요한 고용량 예비 발전기 시운전을 강요합니다. 코로케이션 스페이스의 조기 사전 리스는 시운전 스케줄을 가속화하고, 시험 기간을 단축하고, 신속한 배치가 가능한 로드 뱅크 시장용 제품에 대한 프리미엄을 높이고 있습니다.

신재생에너지 급증에 따른 계통 안정화의 필요성

풍력과 태양광을 통합하는 전력회사는 IEEE 1547-2018 계통 연계 프로토콜을 준수해야 합니다. 이 프로토콜은 유효 전력 관리와 주파수 응답을 중시하고 있습니다. 브라질의 모로 도스 벤토스 풍력 발전소 프로젝트에서는 계통 연계 전에 3.3MVA 로드 뱅크를 사용하여 145MW의 터빈 출력을 검증했습니다. 태양광 발전 설비에서는 변화하는 일사량 프로파일 하에서의 출력 억제 시험이 필수가 되어, 급격한 부하 변동을 재현 가능한 프로그램식 전자 유닛 수요가 높아지고 있습니다. 에너지 저장 시스템은 시나리오를 복잡하게 하며, 배터리 방전과 발전기 백업 간의 원활한 전환은 하이브리드 부하 테스트에서 검증됩니다. 아시아와 남미의 전력회사는 복수의 변전소에 대응 가능한 휴대형 대용량 장치를 요구하고 있어 대응 가능한 로드 뱅크 시장의 확대에 기여하고 있습니다.

단기 프로젝트 사이클이 구매보다 렌탈을 유리하게

시운전 팀은 로드 뱅크를 몇 주 단위로 조달하는 경향이 커지고 장비 구매의 합리성이 저하됩니다. 보관 및 보수 및 감가상각 비용이 라이프사이클 경제성을 렌탈에 유리하게 일하게 하고, 특히 복수 프로젝트가 병행하여 진행하는 경우에 현저합니다. 대기업 대여 기업은 OEM과의 대량 구매 할인을 활용하여 단독 제조업체의 이익률을 압박하고 있습니다. 시설 관리 부서는 시험을 에너지 인프라 계약에 통합한 포괄 서비스 계약을 선호하기 때문에 직접적인 장비 수요가 감소하고 있습니다. 이 서비스 지향의 구조적 전환에 의해 로드 뱅크 시장 전체의 수익은 증가하는 것, 단체 판매 수량은 억제될 전망입니다.

부문 분석

2025년 시점에서 저항 소자와 무효 전력 소자를 단일 하우징에 통합한 하이브리드 유닛이 로드 뱅크 시장의 44.60%를 차지했습니다. 이를 통해 계약자는 단일 임대 장비로 광범위한 시운전 작업을 완료할 수 있습니다. 설치 베이스는 작은 것, 전자 시스템은 2031년까지 연평균 복합 성장률(CAGR)7.78%가 전망되고 있습니다. 재생가능한 아키텍처는 흡수 에너지의 최대 96%를 전력망으로 환원시켜 테스트 사이클의 운영 비용 절감과 현장에서의 배열 수요 저감을 실현합니다. 순수한 저항 제품은 역률 보정이 필요없는 단순한 발전기 풀다운 검사를 위한 엔트리 레벨 제품으로 자리매김합니다. 반면, 리액티브 모델은 모터 제어 및 UPS 검증을 위한 정밀한 유도성 또는 용량성 부하를 제공합니다.

전자 카테고리는 냉각 부하 억제 및 정전 시간 단축이 필수적인 하이퍼스케일 데이터센터 내에서 가장 급속하게 보급되고 있습니다. 운영자는 건물 관리 소프트웨어와 연동하는 랙 수준의 회생 유닛을 통합하는 경우가 증가하고 있습니다. 한편, 하이브리드 설계는 렌탈 플릿으로 인기를 유지하고 있어, 단일 스키드로 실효 성분과 무효 성분을 시뮬레이션할 수 있기 때문에 가동률 향상과 물류 코스트 삭감을 실현합니다. 순수한 리액티브 제품은 역률 보상 장치를 검증하는 전력 회사를 위한 틈새 시장으로 남아 있습니다. 텍트로닉스사가 2024년 4월에 EA Elektro-Automatik을 인수함으로써 왕복 효율 96% 이상의 3.8MW 재생 플랫폼을 확충하여 고효율로 디지털 제어된 솔루션에 업계의 수렴을 강조했습니다.

2,000kW를 초과하는 유닛은 연 CAGR 6.62%로 확대되어 100MW를 초과하는 전력 공급이 필요한 하이퍼스케일 시설의 급증을 반영하고 있습니다. 이러한 시설은 몇 메가와트급 발전기 스트링과 단일 풀다운으로 전체 시스템을 테스트할 수 있는 동등한 로드 뱅크를 요구합니다. 한편, 500kW 미만의 장치는 2025년 수익의 39.30%를 유지하고 있으며, 병원과 상업 건물에서 정기적인 UPS 및 비상 발전기의 점검 수요가 지원하고 있습니다. 501-2,000kW 기기의 로드 뱅크 시장 규모는 중규모 데이터센터 증가에 따라 꾸준히 확대되고 있지만, 양극단의 규모에 비해 성장률은 완만합니다.

규모의 경제성으로 인해 고용량 스키드의 제조가 유리하지만, 운송 물류와 현장에서의 취급 제약이 여전히 제한 요인이 되고 있습니다. 소형 플랫폼은 저비용과 이동의 용이성으로부터 수요를 유지하고 있으며, 특히 분산된 고객 기반에 대응하는 렌탈 플릿에서 두드러집니다. 최소 부문와 최대 부문의 양극화는 업계별로 서로 다른 조달 기준을 돋보이게 하고 있으며, 경쟁적인 필요성으로 제품 포트폴리오의 다양화를 강화하고 있습니다.

로드 뱅크 시장 보고서는 유형별(하이브리드 로드 뱅크, 전자로드 뱅크 등), 부하 용량별(500KW 이하, 2,000KW 초과 등), 설치 형태별(포터블형, 랙마운트/모듈러형 등)), 용도별(데이터센터 및 클라우드, 신재생에너지 통합 및 마이크로그리드 등), 최종사용자별(유틸리티, 렌탈 및 서비스 제공업체 등), 지역별(북미, 유럽, 아시아태평양 등)으로 분류되어 있습니다.

지역별 분석

북미는 2025년 수익의 35.10%를 차지했으며, 슈나이더 일렉트릭사가 2027년까지 7억 달러를 투자하여 제조 능력을 확대할 계획이 이를 지원하고 있습니다. 이를 통해 데이터센터 및 유틸리티을 위한 국내 공급망을 강화할 수 있습니다. NFPA 110과 같은 규제 프레임워크는 핵심 인프라를 위한 발전기의 전체 부하 시험을 의무화하고 있으며, 이는 기준선 수요를 지원합니다. 구리 관세는 비용 압력을 높이고 리드 타임 단축으로 이어지는 현지 조달화의 움직임을 촉진하고 있습니다. 성숙한 임대 생태계는 신속한 도입을 지원하고 지역의 서비스 능력을 차별화합니다.

아시아태평양은 도쿄, 시드니, 뭄바이, 서울 등 주요 도시권에서 데이터센터 설비 용량이 연간 22% 증가하여 2,996MW에 이르기 때문에 7.45%라는 가장 빠른 CAGR이 전망됩니다. AI와 클라우드 도입을 촉진하는 국가 전략이 백업 전원 투자를 뒷받침하는 한편, 다양한 기후 조건에 의해 고습도나 급격한 온도 변화에 견디는 기기가 요구되고 있습니다. 중국의 새로운 데이터센터의 에너지 효율 규제와 싱가포르의 프로젝트 재개가 결합되어 첨단 재생에너지 유닛의 조달을 촉진하고 있습니다.

유럽에서는 엄격한 환경 정책을 기반으로 한 꾸준한 진전을 볼 수 있습니다. 지침 2000/14/EC는 옥외 설비의 소음 배출을 규제하고 OEM 제조업체는 개량형 배플과 저회전 팬 설계의 통합을 추진하고 있습니다. REPowerEU의 재생에너지 용량 목표는 분산 에너지 자원의 송전망 지원 시험을 가속화하고 적용 범위를 확대하고 있습니다. 시장 진출기업은 도시의 소음 규제와 설치 면적의 제약에 대응하는 모듈러 컨테이너 솔루션을 활용해, 광범위한 친환경 인프라 구상에 따른 대처를 진행하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 데이터센터용량의 급속한 증가

- 재생에너지 급증에 따른 계통 안정성의 필요성

- 미션 크리티컬 시설에 대한 복원력 의무 강화

- 렌탈/일시적 전력설비 확대

- 원격지에서의 하이브리드 AC-DC 마이크로그리드의 상승

- 연료 소비 억제에 의한 재생형 로드 뱅크 선호 증가

- 시장 성장 억제요인

- 프로젝트 사이클이 짧기 때문에 구입보다 렌탈이 선호되는

- 원재료 가격의 변동성(구리, 스테인리스 스틸)

- OEM간의 상호 운용성 기준의 부족

- 도시에서의 소음 및 방열 규제의 준수 과제

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 저항 로드 뱅크

- 리액티브 로드 뱅크

- 하이브리드 로드 뱅크

- 전자 로드 뱅크

- 부하 용량별(kW 정격)

- 500kW 미만

- 501-1,000kW

- 1,001-2,000kW

- 2,000kW 초과

- 설치 형태별

- 휴대용

- 트레일러 탑재형/이동식

- 고정식

- 랙 장착형/모듈형

- 용도별

- 발전 및 시운전

- 데이터센터와 및 클라우드

- 제조업 및 산업

- 해양 및 조선

- 석유 및 가스 및 석유화학

- 신재생에너지 통합과 마이크로그리드

- 방위 및 항공우주 분야에 있어서의 지상 지원

- 의료 및 기타 중요한 시설

- 최종 사용자별

- 유틸리티

- 상업 및 산업 소유자

- 렌탈 및 서비스 제공업체

- 방위 및 정부 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 북유럽 국가

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(M&A, 파트너십, PPA)

- 시장 점유율 분석(주요 기업의 시장 순위 및 점유율)

- 기업 프로파일

- ASCO Power Technologies(Schneider Electric)

- Crestchic Loadbanks

- Avtron Power Solutions(Vertiv)

- Simplex(Cummins)

- Mosebach Manufacturing

- Load Banks Direct

- Eagle Eye Power Solutions

- Kaixiang Power

- Sephco Industries

- Powerohm Resistors(AMETEK)

- Hillstone Products

- Tatsumi Ryoki

- Shenzhen KSTAR

- ComRent International

- Hitec Power Protection

- Nordhavn Power Solutions

- Pite Tech

- Johnson Controls(Load Bank Division)

- Trystar Load Banks

- Pacific Power Source

- Powerhaul International

제7장 시장 기회와 장래의 전망

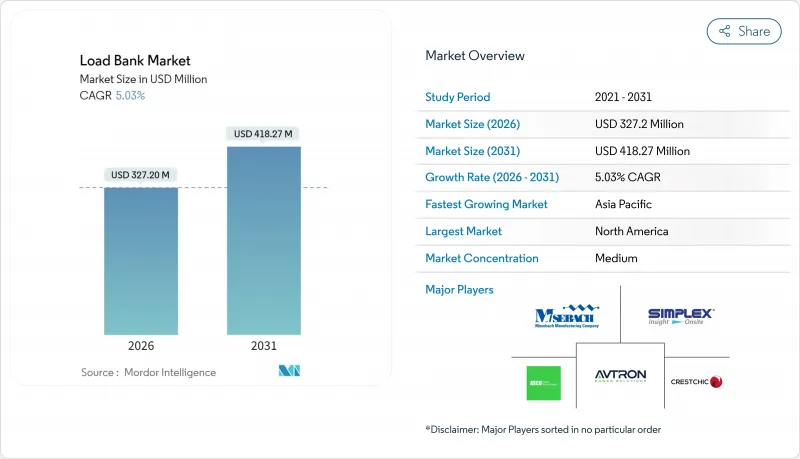

SHW 26.01.22Load Bank Market size in 2026 is estimated at USD 327.2 million, growing from 2025 value of USD 311.53 million with 2031 projections showing USD 418.27 million, growing at 5.03% CAGR over 2026-2031.

Momentum originates from hyperscale data-center build-outs, renewable-rich grids requiring stability validation, and stricter performance mandates for mission-critical facilities. Data-center operators are raising power-density benchmarks, prompting multi-stage validation that expands rental opportunities for load-bank service providers. Renewable integration adds demand for resistive-reactive and electronic systems that can simulate dynamic load profiles for wind, solar, and storage projects. Manufacturers respond with regenerative designs that recover up to 96% of test energy, a feature increasingly requested in new utility and microgrid procurements. At the same time, raw-material inflation and short project timelines pivot many buyers toward asset-light rental models, influencing competitive strategy across the load bank market.

Global Load Bank Market Trends and Insights

Rapid Data-Center Capacity Additions

Annual data-center construction spending stood at USD 31.5 billion in 2024, and the global pipeline is nearing 50 million ft2 of new space. Hyperscale operators now demand sequential acceptance tests that start at the factory and end with integrated system validation, significantly lifting the utilization of rental load banks. Temporary fleets are routinely redeployed during maintenance windows to sustain service-level agreements, generating recurring revenue. AI workloads lift power density, forcing facilities to commission higher-capacity standby generators that require multi-megawatt load tests. Early pre-leasing of colocation space accelerates the commissioning schedule, compressing test timelines and elevating the premium on fast-deploy load bank market offerings.

Grid-Stability Needs Amid Renewable Surge

Utilities integrating wind and solar must show compliance with IEEE 1547-2018 interconnection protocols, which emphasize active power management and frequency response.Wind-farm projects such as Brazil's Morro Dos Ventos used a 3.3 MVA load bank to validate 145 MW of turbine output before grid tie-in. Photovoltaic installations now include curtailment testing under varying irradiance profiles, driving demand for programmable electronic units that can replicate rapid load ramps. Energy-storage systems complicate scenarios; seamless transition between battery discharge and generator backup is verified through hybrid load tests. Utilities in Asia and South America seek portable high-capacity rigs to service multiple substations, bolstering the addressable load bank market.

Short Project Cycles Favor Rentals Over Purchases

Commissioning teams increasingly source load banks for only a few weeks, undermining the case for capital purchases. Storage, maintenance, and depreciation costs tilt life-cycle economics toward renting, especially when multiple projects run concurrently. Large rental houses leverage volume-purchase discounts with OEMs, tightening margin pressure on standalone manufacturers. Facilities management groups prefer bundled service contracts that fold testing into wider energy-infrastructure deals, reducing direct equipment demand. This structural swing toward services constrains unit volumes as overall load bank market revenues grow.

Other drivers and restraints analyzed in the detailed report include:

- Resiliency Mandates for Mission-Critical Facilities

- Expansion of Rental/Temporary Power Fleet

- Volatility in Raw-Material Prices (Copper, Stainless Steel)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid units held 44.60% of the load bank market share in 2025 by combining resistive and reactive elements inside one enclosure, allowing contractors to complete a wider range of commissioning tasks with a single rental. Though smaller in installed base, electronic systems are forecast for an 7.78% CAGR through 2031 as their regenerative architecture returns up to 96% of absorbed energy to the grid, trimming test-cycle operating costs and lowering on-site heat rejection needs. Pure resistive products remain the entry-level option for straightforward generator pull-down checks where power-factor correction is unnecessary, while reactive models provide precise inductive or capacitive loading for motor-control and UPS validation.

The electronic category is gaining ground fastest inside hyperscale data halls that must limit cooling loads and shorten outage windows; operators increasingly embed rack-level regenerative units that synchronize with building-management software. Meanwhile, hybrid designs stay popular with rental fleets because a single skid can simulate real and reactive components, improving utilization and cutting logistics. Pure reactive offerings persist as a niche for utilities that verify power-factor compensation banks. Tektronix's April 2024 acquisition of EA Elektro-Automatik expanded its regenerative platform to 3.8 MW with >=96% round-trip efficiency, underscoring industry convergence on high-efficiency, digitally controlled solutions.

Units above 2,000 kW will expand at a 6.62% CAGR, mirroring the surge of hyperscale campuses exceeding 100 MW utility feeds. These facilities require multi-megawatt generator strings and commensurate load banks capable of full-system testing in a single pull-down. Conversely, sub-500 kW devices maintained 39.30% of 2025 revenue, underpinned by routine UPS and standby-generator checks in hospitals and commercial buildings. The load bank market size for 501-2,000 kW equipment advances steadily as mid-tier data-centers proliferate, though growth moderates relative to extremes at both ends.

Economies of scale favor manufacturing higher-capacity skids, but transport logistics and site-handling constraints remain limiting factors. Smaller platforms preserve demand due to low cost and ease of mobility, particularly in rental fleets that service distributed customer bases. Polarization between the smallest and largest segments underscores divergent procurement criteria across industries, reinforcing product-portfolio diversification as a competitive necessity.

The Load Bank Market Report is Segmented by Type (Hybrid Load Banks, Electronic Load Banks, and More), Load Capacity (Up To 500 KW, Above 2, 000 KW, and More), Form Factor (Portable, Rack-Mounted/Modular, and More), Application (Data Centres and Cloud, Renewable-Energy Integration and Microgrids, and More), End-User (Utilities, Rental and Service Providers, and More), and Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America controlled 35.10% of 2025 revenue, underpinned by Schneider Electric's USD 700 million manufacturing expansion pledge through 2027, which enhances domestic supply chains serving data centers and utilities. Regulatory frameworks such as NFPA 110 prescribe full-load generator tests for critical infrastructure, sustaining baseline demand. Tariffs on copper raise cost pressure and prompt localization moves that shorten lead times. Mature rental ecosystems support rapid deployment, differentiating the region's service capability.

Asia-Pacific is projected to have the quickest 7.45% CAGR thanks to a 22% annual increase in data-center inventory reaching 2,996 MW across metro hubs like Tokyo, Sydney, Mumbai, and Seoul. National strategies encouraging AI and cloud adoption elevate backup-power investments, while diverse climates necessitate equipment able to endure high humidity and wide temperature swings. China's new data-center energy-efficiency rules and Singapore's restart of the project collectively stimulate the procurement of advanced regenerative units.

Europe exhibits steady progression anchored in stringent environmental policy. Directive 2000/14/EC caps noise emissions for outdoor equipment, pushing OEMs to integrate improved baffling and low-RPM fan designs. Renewable-capacity targets under REPowerEU accelerate grid-support trials for distributed energy resources, widening the application scope. Market participants leverage modular container solutions compatible with urban noise and footprint constraints, aligning with broader green-infrastructure ambitions.

- ASCO Power Technologies (Schneider Electric)

- Crestchic Loadbanks

- Avtron Power Solutions (Vertiv)

- Simplex (Cummins)

- Mosebach Manufacturing

- Load Banks Direct

- Eagle Eye Power Solutions

- Kaixiang Power

- Sephco Industries

- Powerohm Resistors (AMETEK)

- Hillstone Products

- Tatsumi Ryoki

- Shenzhen KSTAR

- ComRent International

- Hitec Power Protection

- Nordhavn Power Solutions

- Pite Tech

- Johnson Controls (Load Bank Division)

- Trystar Load Banks

- Pacific Power Source

- Powerhaul International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid data-centre capacity additions

- 4.2.2 Grid-stability needs amid renewable surge

- 4.2.3 Resiliency mandates for mission-critical facilities

- 4.2.4 Expansion of rental/temporary power fleet

- 4.2.5 Rise of hybrid AC-DC microgrids in remote sites

- 4.2.6 Growing preference for regenerative load banks to curb fuel burn

- 4.3 Market Restraints

- 4.3.1 Short project cycles favour rentals over purchases

- 4.3.2 Volatility in raw-material prices (copper, stainless steel)

- 4.3.3 Limited interoperability standards across OEMs

- 4.3.4 Noise & heat-dissipation compliance hurdles in urban sites

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Resistive Load Banks

- 5.1.2 Reactive Load Banks

- 5.1.3 Hybrid Load Banks

- 5.1.4 Electronic Load Banks

- 5.2 By Load Capacity (kW Rating)

- 5.2.1 Up to 500 kW

- 5.2.2 501 to 1,000 kW

- 5.2.3 1,001 to 2,000 kW

- 5.2.4 Above 2,000 kW

- 5.3 By Form Factor

- 5.3.1 Portable

- 5.3.2 Trailer-Mounted/Mobile

- 5.3.3 Stationary

- 5.3.4 Rack-Mounted/Modular

- 5.4 By Application

- 5.4.1 Power Generation and Commissioning

- 5.4.2 Data Centres and Cloud

- 5.4.3 Manufacturing and Industrial

- 5.4.4 Marine and Shipbuilding

- 5.4.5 Oil and Gas and Petrochemical

- 5.4.6 Renewable-Energy Integration and Microgrids

- 5.4.7 Defence and Aerospace Ground Support

- 5.4.8 Healthcare and Other Mission-Critical Facilities

- 5.5 By End-user

- 5.5.1 Utilities

- 5.5.2 Commercial and Industrial Owners

- 5.5.3 Rental and Service Providers

- 5.5.4 Defence and Government

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 NORDIC Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ASCO Power Technologies (Schneider Electric)

- 6.4.2 Crestchic Loadbanks

- 6.4.3 Avtron Power Solutions (Vertiv)

- 6.4.4 Simplex (Cummins)

- 6.4.5 Mosebach Manufacturing

- 6.4.6 Load Banks Direct

- 6.4.7 Eagle Eye Power Solutions

- 6.4.8 Kaixiang Power

- 6.4.9 Sephco Industries

- 6.4.10 Powerohm Resistors (AMETEK)

- 6.4.11 Hillstone Products

- 6.4.12 Tatsumi Ryoki

- 6.4.13 Shenzhen KSTAR

- 6.4.14 ComRent International

- 6.4.15 Hitec Power Protection

- 6.4.16 Nordhavn Power Solutions

- 6.4.17 Pite Tech

- 6.4.18 Johnson Controls (Load Bank Division)

- 6.4.19 Trystar Load Banks

- 6.4.20 Pacific Power Source

- 6.4.21 Powerhaul International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment