|

시장보고서

상품코드

1906252

올레오케미컬 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Oleochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

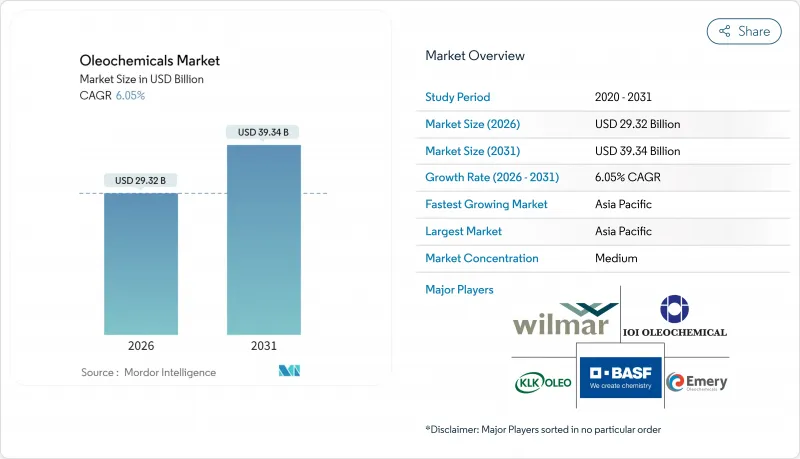

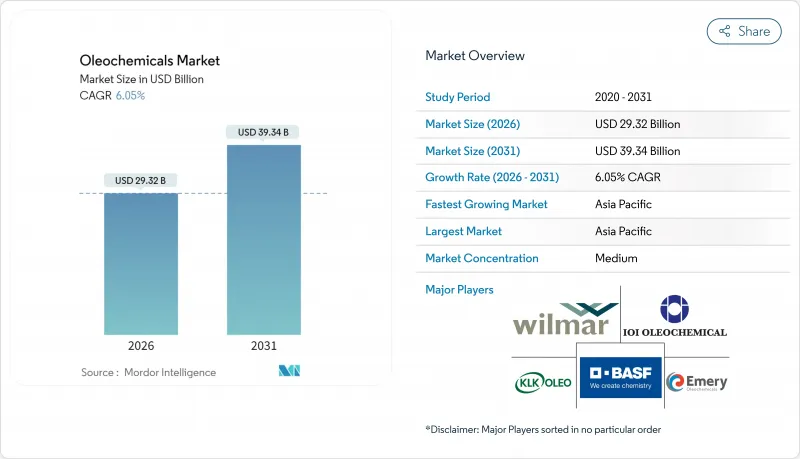

올레오케미컬 시장은 2025년 276억 5,000만 달러로 평가되었으며, 2026년 293억 2,000만 달러에서 2031년까지 393억 4,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 6.05%로 예상됩니다.

현재의 확대 경향은 정책 주도에 의한 바이오 계면활성제에 대한 수요, 바이오 디젤 혼합 의무화, 가정용 및 개인용 케어 제품 분야에서의 천연 성분에 대한 소비자 기호의 고조를 반영하고 있습니다. 인도네시아의 B40 프로그램에서만 1,500만 킬로리터 이상의 팜유 유래 메틸에스테르가 에너지 용도로 전환되어, 기존 화학 용도용 공급이 축소되고 있습니다. 동시에 유럽연합(EU)의 산림 파괴 방지 규제로 컴플라이언스 비용이 상승하고 추적성과 인증을 갖춘 공급망에 대한 투자가 촉진되고 있습니다. 당류나 메탄올을 지방산이나 알코올로 변환하는 합성 생물학적 수법이 대두되고 있어 원료의 다양화와 토지 이용에 대한 영향 축소가 기대되고 있습니다. 아시아태평양은 통합 팜유 인프라와 중국, 동남아시아에서 급성장하는 퍼스널케어 소비에 힘입어 생산과 수요에 초점을 맞추고 있습니다.

세계의 올레오케미컬 시장의 동향 및 전망

아시아태평양의 계면활성제 생산 능력 확대

중국, 인도네시아, 말레이시아의 계면활성제 제조 프로젝트가 급속히 확대되고 있으며, 이는 C12-C18 지방산 및 알코올의 기준선 수요를 밀어 올리고 있습니다. KLK OLEO사가 장가항에서 실시한 연간 20만 톤 증산은 동지역의 원료 조달과 물류면에서의 우위성을 나타내고 있습니다. 현지의 퍼스널케어 브랜드는 국내의 '클린 뷰티' 기준을 달성하기 위해, 천연 유래의 유화제를 도입하여 고급화를 진행하고 있습니다. 석유 가격 상승으로 인한 합성 계면활성제의 가격 상승으로 수출 지향 제조업체는 비용을 중시하는 유럽으로부터 수주를 획득하고 있습니다. 각국 정부는 부가가치 향상 로드맵 하에서 특수 화학제품의 촉진을 도모하고 있으며, 이는 새로운 올레오케미컬 플랜트의 입지를 더욱 뒷받침하고 있습니다. 이러한 시너지 효과는 올레오케미컬 시장의 기반 수요를 구조적으로 밀어 올리고 경기 변동의 영향을 완화하는 기반을 형성하고 있습니다.

확대하는 퍼스널케어 및 화장품 수요

2024년 세계의 스킨케어 제품 소매 매출액은 9% 증가했으며, 조제 화학자들은 식물 유래 연화제, 에스테르, 유화제를 지정하는 경향이 강해지고 있습니다. BASF사의 Verdesense 제품 라인은 왁스 모양의 식물성 폴리머가 마이크로플라스틱을 대체하면서 사용감을 손상시키지 않는 사례를 보여줍니다. 북미의 소비자는 구입 동기에 생분해성을 효과성에 이은 중요한 요소로 여기며, 이는 브랜드에게 기존 SKU(재고 관리 단위)의 배합 재검토를 촉구하고 있습니다. 아시아의 다국적 기업도 이 변화를 반영하여 주력 제품 라인에서 ECOCERT 및 COSMOS 인증 취득을 목표로 하고 있습니다. 람노리피드를 이용한 바이오 계면활성제의 상용화 시험은 두 자릿수 성장의 가능성을 나타내며 합성 에톡실레이트의 대체가 중기적으로 진행됨을 시사합니다. 프리미엄화와 지속가능성이 결합되어 특수 올레오케미칼의 가격탄력성은 계속 양호한 상태를 유지하고 있습니다.

원료 가격의 변동성

2024년, 엘니뇨 현상에 따른 수량 감소로 인해 팜 원유의 선물 가격은 톤당 780-970달러 사이에서 변동하여 분리업자와 증류업자의 이익을 압박했습니다. 필리핀 농원의 태풍 피해에 의해 코코넛유 가격도 급등하여 라우르산 유도체의 비용 상승 요인이 되었습니다. 북미 구매자는 브라질산 수지로 눈을 돌렸지만 수출량이 377% 급증함에 따라 현지 유지 가격은 18% 상승했습니다. 생산자는 계약 기간의 단축과 가격 상승 조항의 도입으로 대응했습니다. 지속적인 변동은 재고 계획을 복잡하게 만들고 비용이 최종 용도의 가격 수준을 초과하면 수요 파괴를 일으킬 수 있습니다.

부문 분석

2025년 지방산은 견조한 세제 및 퍼스널케어 수요를 배경으로 세계의 올레오케미컬 시장에서 37.65%의 점유율을 유지했습니다. 그러나 메틸에스테르의 올레오케미칼 시장 내 규모는 인도네시아, 브라질, EU의 바이오디젤 의무화 프로그램에 의해 CAGR 7.68%로 확대될 것으로 전망됩니다. 발효 기술에 의한 지방 알코올의 혁신은 비용 곡선의 재조정을 초래할 수 있지만, 상업 규모의 생산량은 2020년대 후반까지 제한되었습니다. 바이오디젤 생산에 수반되는 글리세린 공급 과잉은 가격 하락 압력을 낳고 의약품 및 식품 용도에서의 도입을 촉진하고 있습니다. 정책 주도의 에너지 수요는 가격 탄력성이 낮은 경향이 있기 때문에 경기 둔화기에서도 메틸에스테르의 수요는 유지됩니다. 한편 아젤라익산과 세바식산 등 특수지방산 유도체는 프리미엄 가격대에서 거래되어 제품별 부가가치화가 가능한 통합생산자에게 이익을 가져다줍니다.

메틸에스테르의 급성장에 의해 원료가 비누용 원료로부터 전용되기 때문에 소비재에 대해 가격 전가가 강요되는 경우도 나타나고 있습니다. 시장 진출 기업은 이러한 상황을 인식하고 시장 진입 경로의 시너지를 모색하고 있습니다. 압착, 바이오 디젤 및 올레오케미컬 자산을 보유한 통합 농업기업은 일상적인 자원 배분을 최적화하고 있습니다. 지방 알코올에 대한 수요는 황산염이 없는 화장품에 대한 동향의 확대와 교차하여 에스테르 수요의 가속화에도 불구하고 알코올의 중요성을 강화하고 있습니다. 결과적으로 제품 카테고리가 고립되어 운영되는 것이 아니라 보다 광범위한 올레오케미컬 시장에서 원료 및 제품별 경제성을 통해 상호 연계하는 복잡한 경쟁 구도가 형성되고 있습니다.

지역별 분석

아시아태평양은 2025년에 올레오케미컬 시장의 47.12%를 차지했으며, 통합된 팜 클러스터와 비용 효율적인 물류망을 통해 이 시장을 견인했습니다. 중국의 계면활성제 복합시설 가동 확대와 동남아시아의 가처분소득 증가에 따라 지역 CAGR은 7.92%로 지속될 전망입니다. 그러나 수출 중심 기업은 EU와 북미의 지속가능성 기준을 충족하지 못하면 이익률이 축소되는 할인 위험에 직면하게 됩니다. 인도네시아의 바이오디젤 도입은 원료의 유용성과 국내 정제소에 대한 투자를 촉진하여 현지에서의 가치 획득을 높이고 있습니다. 말레이시아의 특수화학 로드맵은 2030년까지 다운스트림 수익을 두 배로 높이는 것을 목표로 하고 있지만, 숙련 노동자의 부족이 실행을 방해할 수 있습니다. 남아시아에서는 비누 수요가 높아지고 있지만 품질 사양은 여전히 경제협력개발기구(OECD) 시장에 뒤처져 가격 실현을 억제하고 있습니다.

북미와 유럽은 성숙한 소비와 기술 혁신 간의 균형을 맞추고 있습니다. EU 정책은 ILUC 고위험 원료인 팜유를 금지하고 폐유 및 동물성 지방을 원료로 하는 올레오케미컬을 장려하고 있습니다. 한편, 발효 스타트업은 다국적 화장품 기업과의 판매계약을 확보하고 있습니다. 미국의 재생가능한 디젤의 성장은 수지 시장을 흡수하고, 지방의 올레오케미컬 제조업체는 운임 할증에도 불구하고 라우린 오일을 수입하게 되었습니다. 브라질이 주도하는 남미는 아시아태평양(APAC)에 이어 가장 급성장하고 있습니다. 압착능력 확대로 대두유 공급은 확보되고 있지만 국내 바이오디젤 수요가 상당한 비율을 차지하고 있습니다. 중동 및 아프리카는 생산 능력에 있어서 뒤처져 있지만 수요가 증가하고 있으며, 걸프 국가들은 해사 및 광업 분야에서 바이오 윤활유의 사용을 장려하고 있으며 수출업체에게 서서히 안정적인 수요를 창출하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 아시아태평양의 계면활성제 생산 능력 확대

- 확대하는 퍼스널케어 및 화장품 수요

- 지방산 메틸에스테르에 대한 바이오 디젤 의무화 정책

- 생분해성 및 식물 유래 화학제품으로의 이행

- 저비용 지방 알코올의 생물학적 합성 기술

- 억제요인

- 원료 가격의 변동성

- 지속 불가능한 팜유에 대한 NGO 및 규제 당국의 압력

- 벌크 용도에서의 석유화학제품의 경쟁

- 밸류체인 분석

- Porter's Five Forces

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 제품 유형

- 지방산

- 지방 알코올

- 메틸에스테르

- 글리세린

- 기타 제품 유형

- 원료 공급원

- 식물성 기름

- 동물성 지방

- 최종 사용자 산업

- 퍼스널케어 및 화장품

- 비누 및 세제

- 식품 및 음료

- 의약품

- 폴리머

- 기타 최종 사용자 산업

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- BASF

- Berg Schmidt GmbH & Co. KG

- Cargill Inc.

- Croda International Plc

- Emery Oleochemicals

- Evonik Industries AG

- Godrej Industries Group

- IOI Oleochemical

- Kao Corporation

- KLK OLEO

- Kraton Corporation

- Musim Mas Group

- Oleon NV

- Procter & Gamble

- PT Ecogreen Oleochemicals

- VVF Ltd.

- Wilmar International Ltd.

제7장 시장 기회 및 미래 전망

CSM 26.01.28The Oleochemicals Market was valued at USD 27.65 billion in 2025 and estimated to grow from USD 29.32 billion in 2026 to reach USD 39.34 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

Current expansion reflects policy-driven demand for bio-based surfactants, biodiesel blending mandates, and accelerating consumer preference for natural ingredients across home and personal care applications. Indonesia's B40 program alone redirects more than 15 Million kilolitres of palm-based methyl esters into energy use, tightening supply for conventional chemical uses. Concurrently, the European Union (EU) Deforestation Regulation raises compliance costs and spurs investment in traceable, certified supply chains. Synthetic-biology routes that convert sugars or methanol into fatty acids and alcohols are emerging, promising feedstock diversification and lower land-use impacts. Asia-Pacific remains the focus of production and demand, supported by integrated palm infrastructure and fast-growing personal-care consumption in China and Southeast Asia.

Global Oleochemicals Market Trends and Insights

Growing Surfactants Capacity in Asia-Pacific

Surfactant manufacturing projects in China, Indonesia, and Malaysia are scaling rapidly, lifting baseline demand for C12-C18 fatty acids and alcohols. KLK OLEO's recent 200 ktpa expansion in Zhangjiagang underscores the region's feedstock and logistics advantage. Local personal-care brands are moving upmarket, incorporating naturally derived emulsifiers to meet domestic "clean beauty" standards. Export-oriented producers capture cost-sensitive orders from Europe as petro-inflation raises synthetic surfactant prices. Governments are promoting specialty chemicals under value-addition roadmaps, further anchoring new oleochemical units. The cumulative effect is a structural uplift in baseline offtake that cushions the oleochemicals market against cyclical swings.

Expanding Personal-Care and Cosmetics Demand

Global retail skin-care sales rose 9% in 2024, and formulating chemists increasingly specify plant-based emollients, esters, and emulsifiers. BASF's Verdessence line illustrates how waxy plant polymers replace microplastics without compromising sensory profiles . North American consumers rank biodegradability second only to efficacy in purchase drivers, pushing brand owners to reformulate legacy stock keeping unit (SKUs). Asian multinationals mirror this shift, aiming for ECOCERT and COSMOS accreditation on flagship lines. Bio-surfactant commercial trials using rhamnolipids show double-digit growth potential, signalling a medium-term substitution of synthetic ethoxylates. Collectively, premiumisation and sustainability converge to keep price elasticity favourable for specialty oleochemicals.

Feedstock Price Volatility

Crude palm oil futures swung between USD 780 and USD 970 per ton in 2024 following El Nino-linked yield drops, eroding gross margins for splitters and distillers. Coconut oil prices also spiked after typhoon damage to Philippine plantations, pressuring lauric acid derivative costs. North American buyers turned to Brazilian tallow, but a 377% export surge lifted local fat prices by 18%. Producers responded by shortening contract tenors and introducing price-escalation clauses. Persistent volatility complicates inventory planning and can trigger demand destruction when costs overshoot end-use price points.

Other drivers and restraints analyzed in the detailed report include:

- Biodiesel Mandates for Fatty Acid Methyl Esters

- Shift Toward Biodegradable, Plant-Based Chemicals

- NGO and Regulatory Pressure on Unsustainable Palm Oil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Global fatty acids retained 37.65% Oleochemicals market share in 2025 on the back of solid detergent and personal-care demand. The Oleochemicals market size for methyl esters, however, is projected to rise at a 7.68% CAGR, supported by mandatory biodiesel programs across Indonesia, Brazil, and the EU. Fatty alcohol innovation through fermentation could recalibrate cost curves, yet commercial volumes will remain limited until late decade. Glycerine oversupply from biodiesel yields downward price pressure, encouraging its uptake in pharma and food applications. As policy-driven energy demand is largely price-inelastic, methyl ester offtake continues even during economic slowdowns. Conversely, specialty fatty acid derivatives such as azelaic and sebacic acids enjoy premium streams, benefiting integrated producers able to valorise by-products.

Methyl esters' rapid growth diverts feedstock away from soap noodles, occasionally forcing price pass-throughs in consumer staples. Market participants thus explore route-to-market synergies: integrated agribusinesses with crushing, biodiesel, and oleochemical assets optimise allocation daily. Fatty alcohol demand intersects with rising sulfate-free cosmetic trends, reinforcing alcohol's relevance despite ester acceleration. Net effect is a nuanced competitive landscape where product categories no longer operate in silos, but rather interlink through feedstock and coproduct economics within the wider Oleochemicals market.

The Oleochemicals Market Report is Segmented by Product Type (Fatty Acids, Fatty Alcohols, Methyl Esters, Glycerine, and More), Feedstock Source (Vegetable Oils and Animal Fats), End-User Industry (Personal Care and Cosmetics, Food and Beverages, Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 47.12% Oleochemicals market share in 2025, anchoring the Oleochemicals market courtesy of integrated palm clusters and cost-efficient logistics. Regional CAGR of 7.92% will continue as China's surfactant complexes ramp up and Southeast Asian disposable incomes climb. Yet export-centric players must meet EU and North American sustainability thresholds or risk margin-eroding discounts. Indonesian biodiesel uptake diverts feedstock and fosters domestic refinery investments that lift local value capture. Malaysia's specialty chemicals roadmap aims to double downstream revenue by 2030, though skilled-labour shortages could constrain execution. South Asia shows rising demand for soap noodles, but quality specifications still lag the Organization for Economic Cooperation and Development (OECD) markets, tempering price realization.

North America and Europe balance mature consumption with technological innovation. EU policy bans high-ILUC palm, incentivising waste-oil and animal fat-based oleochemicals, while venture-backed fermentation start-ups secure offtake agreements with cosmetic multinationals. US renewable diesel growth sequesters tallows, prompting local oleochemical players to import lauric oils despite freight premiums. South America, led by Brazil, grows fastest after Asia-Pacific (APAC); expanding crush capacity ensures ready soybean oil supply, although domestic biodiesel uptake absorbs a significant slice. Middle East and Africa lag in production capacity but present incremental demand, with Gulf states encouraging bio-lubricant uptake in marine and mining sectors, offering gradual yet stable pull for exporters.

- BASF

- Berg+Schmidt GmbH & Co. KG

- Cargill Inc.

- Croda International Plc

- Emery Oleochemicals

- Evonik Industries AG

- Godrej Industries Group

- IOI Oleochemical

- Kao Corporation

- KLK OLEO

- Kraton Corporation

- Musim Mas Group

- Oleon NV

- Procter & Gamble

- PT Ecogreen Oleochemicals

- VVF Ltd.

- Wilmar International Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Surfactants Capacity in Asia-Pacific

- 4.2.2 Expanding Personal-care and Cosmetics Demand

- 4.2.3 Biodiesel Mandates for Fatty Acid Methyl Esters

- 4.2.4 Shift Toward Biodegradable, Plant-based Chemicals

- 4.2.5 Synthetic-biology Routes to Low-cost Fatty Alcohols

- 4.3 Market Restraints

- 4.3.1 Feedstock Price Volatility

- 4.3.2 NGO and Regulatory Pressure on Unsustainable Palm Oil

- 4.3.3 Petrochemical Price Competition in Bulk Applications

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 Product Type

- 5.1.1 Fatty Acids

- 5.1.2 Fatty Alcohols

- 5.1.3 Methyl Esters

- 5.1.4 Glycerine

- 5.1.5 Other Product Types

- 5.2 Feedstock Source

- 5.2.1 Vegetable Oils

- 5.2.2 Animal Fats

- 5.3 End-user Industry

- 5.3.1 Personal Care and Cosmetics

- 5.3.2 Soap and Detergent

- 5.3.3 Food and Beverages

- 5.3.4 Pharmaceuticals

- 5.3.5 Polymers

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Berg+Schmidt GmbH & Co. KG

- 6.4.3 Cargill Inc.

- 6.4.4 Croda International Plc

- 6.4.5 Emery Oleochemicals

- 6.4.6 Evonik Industries AG

- 6.4.7 Godrej Industries Group

- 6.4.8 IOI Oleochemical

- 6.4.9 Kao Corporation

- 6.4.10 KLK OLEO

- 6.4.11 Kraton Corporation

- 6.4.12 Musim Mas Group

- 6.4.13 Oleon NV

- 6.4.14 Procter & Gamble

- 6.4.15 PT Ecogreen Oleochemicals

- 6.4.16 VVF Ltd.

- 6.4.17 Wilmar International Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Increased Use of Biofuels