|

시장보고서

상품코드

1906255

헬스케어 규정 준수 소프트웨어 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Healthcare Compliance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

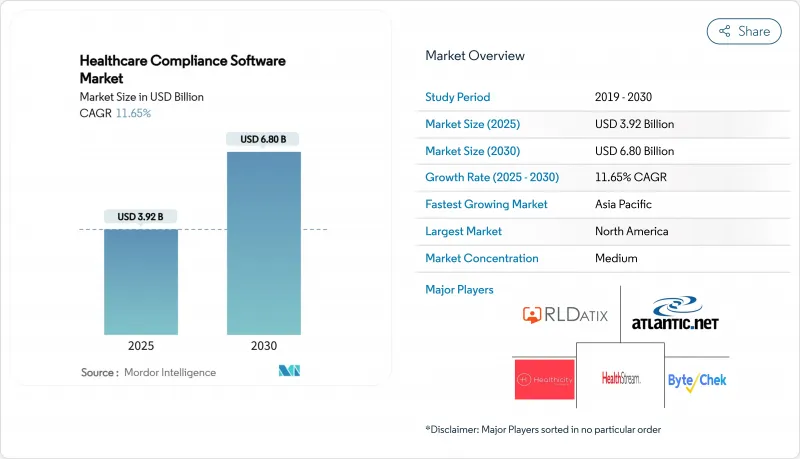

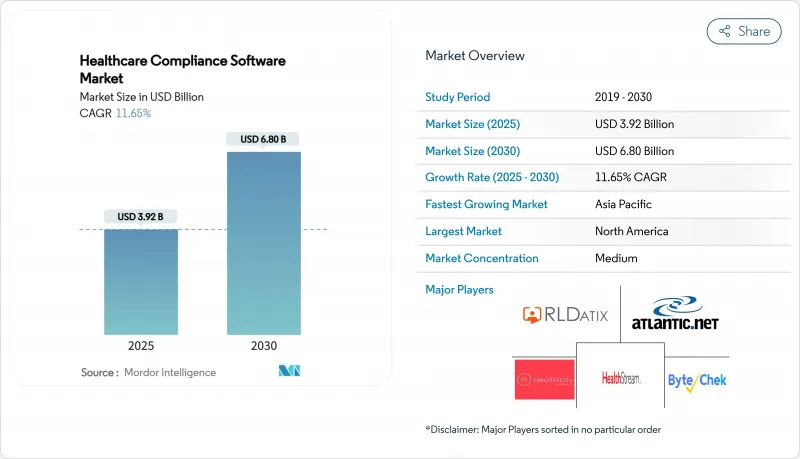

헬스케어 규정 준수 소프트웨어 시장은 2025년 39억 2,000만 달러로 평가되었고, 2026년 43억 7,000만 달러에서 2031년까지 75억 1,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 11.47%를 나타낼 전망입니다.

임상 워크플로우의 급속한 디지털화, 원격의료 확대, AI 기반 감사 기능은 규정 준수 플랫폼을 단순한 규제 체크리스트가 아닌 위험 완화를 위한 전략적 도구로 자리매김하게 합니다. 규칙 변경을 감지하고 감사 추적을 자동화하기 위해 자연어 처리 기술을 통합한 벤더들은 시장 점유율을 확보하고 있습니다. 병원들은 도입 후 업무량이 최대 50%까지 감소했다고 보고하기 때문입니다. 클라우드 제공 모델은 여전히 선호되는 선택으로, 의료 기관들이 자본 지출 없이도 용량을 확장할 수 있게 하면서도 엄격한 HIPAA 및 GDPR 보안 요건을 충족시킵니다. 아시아태평양 지역은 중국, 인도, 일본의 데이터 개인정보 보호법 강화 및 의료 제공자 네트워크 디지털화로 인해 연평균 18.47%의 성장률을 기록하며 가장 빠르게 성장하는 지역 시장으로 부상하고 있으며, 이는 자동화된 규정 준수 솔루션의 적극적인 도입을 촉진하고 있습니다.

세계의 헬스케어 규정 준수 소프트웨어 시장 동향 및 인사이트

HIPAA 호환 플랫폼이 필요한 원격 헬스케어 확대

가속화된 원격의료 도입으로 가상 진료가 팬데믹 이전 5%에서 현재 미국 전체 진료의 3분의 1을 차지하게 되었습니다. 이에 의료 시스템은 주간 진료 위험을 완화하기 위해 종단간 암호화, 다중 요소 사용자 인증, 자동화된 주간 면허 확인 기능을 내장한 규정 준수 제품군을 요구합니다. 실시간 영상 통화 암호화 및 디지털 동의 관리로 차별화하는 벤더들은 통합 의료 네트워크에서 더 높은 채택률을 보이고 있습니다. 이러한 플랫폼은 보안 API를 활용해 전자건강기록(EHR) 포털과 연동함으로써 원격 처방 및 후속 치료 계획이 종단적 환자 기록에 직접 반영되도록 합니다. 이 추세는 외래 진료소 및 정신건강 서비스 제공자 등 기존에 도입 속도가 느렸던 기관들도 대형 병원과 동일한 HIPAA 보호 장치를 요구하게 되면서 헬스케어 규정 준수 소프트웨어 시장을 확대하고 있습니다.

환자 중심의 케어에 중점화

규제 기관들은 점점 더 환급을 품질 및 형평성 지표와 연계하여, 정책 준수와 측정 가능한 환자 결과 간의 상관관계를 입증할 수 있는 컴플라이언스 도구를 요구하고 있습니다. 현대적 플랫폼은 임상 지표와 함께 환자 보고 만족도 점수를 수집하여 가치 기반 계약에 대한 컴플라이언스 영향력을 보여주는 대시보드를 생성합니다. 선도적인 책임의료기관(ACO)들은 이러한 대시보드를 인구 건강 관리 엔진과 통합하여 위험을 계층화하고 표적 개입을 촉발합니다. 정책 실행과 재입원률 및 사망률을 연결하는 분석 기능을 내장한 소프트웨어 기업들은 단일 화면 가시성을 추구하는 최고 품질 책임자(CQO)들 사이에서 선호도를 얻고 있습니다. 가치 기반 모델이 확대됨에 따라 이러한 연계는 의료 컴플라이언스 소프트웨어 시장을 벌금 회피에서 성과 최적화로 전환시키고 있습니다.

전문 진료소의 인지 부족과 IT 자원의 제약

전문 진료소는 종종 소규모 기술 팀으로 운영되며, 때로는 5명 미만의 직원이 모든 IT 기능을 담당하기도 합니다. 이러한 역량 격차는 EHR 및 지불자 포털과의 통합이 필요한 완전한 기능의 컴플라이언스 도구 도입을 지연시킵니다. 벤더들은 몇 시간 내 배포 가능한 모듈형 클라우드 네이티브 애플리케이션으로 대응하며 피부과, 종양학, 행동 건강 분야용 사전 구성 템플릿을 제공합니다. 그러나 많은 클리닉은 여전히 해당 분야별 규제 세부사항을 인지하지 못한 채, 감사 위험에 노출되는 구식 수기 기록에 의존합니다. 인식 제고 캠페인과 간소화된 솔루션이 확대되기 전까지, 이러한 제약은 분산된 외래 환자 부문에서의 헬스케어 규정 준수 소프트웨어 시장 침투를 제한할 것입니다.

부문 분석

클라우드 플랫폼은 2025년 헬스케어 규정 준수 소프트웨어 시장 점유율의 52.19%를 차지했으며, 이는 공급업체들이 확장성과 원격 접근성을 우선시한 결과입니다. 해당 부문의 17.42% 예상 연평균 복합 성장률(CAGR)은 온프레미스 시스템을 상회하는데, 이는 구독형 가격 정책이 자본 지출을 예측 가능한 운영 비용으로 전환하고 몇 주 내로 신속한 구현을 가능하게 하기 때문입니다. 주요 공급업체들은 자동화된 백업 및 재해 복구 기능을 번들로 제공하여, 2024년 미국 내 다수 병원을 대상으로 발생한 사이버 사고 속에서도 데이터 복원력을 보장합니다. 클라우드 호스팅은 지속적인 규정 업데이트도 간소화합니다. 규정이 변경되면 공급자는 다운타임 없이 패치를 수신할 수 있으며, 이는 현지 IT 개입이 필요한 기존 설치 방식과 대비됩니다. 동시에 HIPAA 및 GDPR과 같은 규제 프레임워크는 인증된 클라우드 공급자가 보안 요건을 충족할 수 있음을 명확히 하는 지침을 발표하여 규정 준수 담당자의 신뢰도를 높이고 있습니다.

클라우드 공급업체는 현지 서버에서 실행하기에는 자원이 많이 소모되는 실시간 이상 탐지를 위한 AI 마이크로서비스를 내장함으로써 차별화를 더욱 강화하고 있습니다. 이러한 분석 기술을 활용하는 병원들은 감사 주기 시간이 두 자릿수 감소했다고 보고합니다. 인도의 ABDM 디지털 헬스 프로그램과 일본의 의료 정보 시스템 인프라를 포함한 국가 차원의 이니셔티브들은 클라우드 아키텍처를 참조함으로써 지역적 수요를 강화하고 있습니다. 결과적으로, 클라우드 배포는 2031년까지 헬스케어 규정 준수 소프트웨어 시장을 주도하는 주요 동력으로 남아 있을 것이며, 특히 여러 지역에 걸쳐 통합된 감독을 추구하는 다중 사이트 의료 시스템에서 그러할 것입니다.

지역별 분석

북미는 HIPAA, HITECH 및 허위 청구 법(False Claims Act)의 엄격한 시행에 힘입어 2025년 헬스케어 규정 준수 소프트웨어 시장 점유율의 44.68%를 유지했습니다. 클라우드의 광범위한 채택은 소프트웨어 배포를 가속화하고 있으며, 설문조사에 따르면 현재 미국 병원의 91%가 인프라의 일부를 클라우드에서 운영하고 있습니다. CMS의 2030년까지 완전한 책임의료(Accountable Care) 참여 추진은 문서화 및 품질 보고 요건을 더욱 강화하여 통합 규정 준수 플랫폼에 대한 투자를 촉진합니다. 의료 제공 기관들은 EHR 업그레이드와 규정 준수 모듈을 점점 더 묶어 제공함으로써 교차 판매 기회를 창출하고 있습니다. 2024년 여러 고위급 집행 조치 이후 이사회 차원의 사기 및 낭비 감시가 강화되면서 AI 기반 감사 기능이 주목받고 있습니다.

아시아태평양 지역은 18.12%의 연평균 복합 성장률(CAGR)로 가장 높은 성장률을 기록하며 세계의 평균을 크게 상회할 전망입니다. 중국의 개인정보보호법과 인도의 디지털 개인 데이터 보호법은 엄격한 처벌을 부과하여 의료 제공자들이 벌금을 피하기 위해 자동화된 모니터링을 도입하도록 유도합니다. 일본과 호주의 공공-민간 파트너십은 농촌 지역 원격의료 확장에 자금을 지원하며, 각 사업은 환자 데이터 전송 보안을 위한 컴플라이언스 기술이 필요합니다. 해당 지역에서 운영 중인 다국적 생명과학 기업들은 반부패, 약물감시, 데이터 프라이버시 통제를 통합하기 위해 통합 플랫폼을 도입하며, 이는 의료 컴플라이언스 소프트웨어 시장 규모를 더욱 확대할 전망입니다.

유럽은 GDPR 벌금이 사상 최고치를 기록하며 꾸준한 수요를 창출하고 있으며, 2024년에는 데이터 유출로 인해 여러 병원이 수백만 달러의 벌금을 부과받았습니다. 공급업체들은 의료 특화 규정을 광범위한 데이터 보호 의무와 통합하여 감독 기관에 대한 보고를 간소화하는 솔루션을 우선시합니다. 중동·아프리카 및 남미는 여전히 신흥 시장이지만, 아랍에미리트, 사우디아라비아, 브라질, 콜롬비아에 위치한 3차 의료기관에서 채택률이 증가하고 있습니다. 모바일 친화적 규정 준수 앱은 현장 직원이 저대역폭 환경에서도 체크리스트를 완료할 수 있게 하여, 고정 네트워크가 부족한 지역에서의 점진적 시장 침투를 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- HIPAA 준수 플랫폼이 필요한 원격의료 확대

- 환자 중심의 헬스케어에 중점화

- 수동 헬스케어 규정 준수 방식에서 자동화 규정 준수 소프트웨어로의 전환

- 수동 업무량 감소시키는 AI 기반 감사 통합

- 가치에 기초한 헬스케어의 대두가 청구 규정 준수 자동화를 추진

- 강력한 규정 준수 모니터링을 촉발하는 증가하는 사이버 보안 위협

- 시장 성장 억제요인

- 전문 진료소의 인식 부족과 IT 자원의 제약

- 규정 준수를 비용 센터로 인식하여 구매 우선순위 하락

- 높은 구현 비용

- 여러 관할 구역에 걸친 규제 요건의 복잡성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액은 미화)

- 전개 모드별

- 클라우드 기반

- 온프레미스

- 웹 기반

- 솔루션 모듈별

- 정책 및 절차 관리

- 감사 도구

- 교육 관리 및 진행 상황 추적

- 헬스케어 청구 및 코딩

- 라이선스, 증명서 및 계약서 관리

- 사고 관리

- 인증 관리

- 기타 모듈

- 최종 사용자별

- 병원

- 전문 외래 및 외래 진료소

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- RLDatix

- Healthicity LLC

- HealthStream Inc.

- Compliancy Group LLC

- Atlantic.Net

- VielSun

- Accountable HQ Inc.

- Complinity Technologies Pvt Ltd

- Radar Healthcare

- ConvergePoint Inc.

- Beacon Healthcare Systems

- Sprinto

- NAVEX Global

- ByteChek, Inc.

- Verge Health

- MedTrainer

- Protenus

- Intraprise Health

- Symplr

- Accruent(Connectiv)

제7장 시장 기회와 장래의 전망

HBR 26.01.26The Healthcare Compliance Software Market was valued at USD 3.92 billion in 2025 and estimated to grow from USD 4.37 billion in 2026 to reach USD 7.51 billion by 2031, at a CAGR of 11.47% during the forecast period (2026-2031).

Rapid digitization of clinical workflows, telehealth expansion, and AI-enabled auditing position compliance platforms as strategic tools for risk mitigation rather than mere regulatory checklists. Vendors that integrate natural language processing to flag rule changes and automate audit trails are capturing share because hospitals report up to 50% workload reductions after deployment. Cloud delivery models remain the preferred choice, enabling provider organizations to scale capacity without incurring capital expenditures while meeting stringent HIPAA and GDPR security mandates. Asia-Pacific emerges as the fastest-growing regional opportunity, fueled by 18.47% CAGR as China, India, and Japan tighten data-privacy laws and digitize provider networks, prompting aggressive adoption of automated compliance solutions.

Global Healthcare Compliance Software Market Trends and Insights

Expansion of Telehealth Requiring HIPAA-Compliant Platforms

Accelerated telehealth uptake now positions virtual visits to account for one-third of all U.S. encounters, compared with 5% before the pandemic. Health systems therefore demand compliance suites that embed end-to-end encryption, multi-factor user authentication, and automated cross-state licensure verification to mitigate interstate practice risk. Vendors differentiating with real-time video-call encryption and digital consent management see stronger adoption among integrated delivery networks. Leveraging secure APIs, these platforms link to electronic health record (EHR) portals so that remote prescriptions and follow-up plans feed directly into longitudinal patient files. The trend broadens the healthcare compliance software market because ambulatory clinics and behavioral health providers, historically slower adopters, now require the same HIPAA safeguards as large hospitals.

Emphasis on Patient-Centered Care

Regulators increasingly tie reimbursement to quality and equity metrics, compelling compliance tools to correlate policy adherence with measurable patient outcomes. Modern platforms capture consumer-reported satisfaction scores alongside clinical indicators to generate dashboards demonstrating compliance impact on value-based contracts. Leading accountable-care organizations integrate these dashboards with population-health engines that stratify risk and trigger targeted interventions. Software firms embedding analytics that link policy execution with readmission and mortality rates earn preference among chief quality officers seeking single-pane visibility. As value-based models expand, this linkage transforms the healthcare compliance software market from penalty avoidance to performance optimization.

Lack of Awareness & Limited IT Resources among Specialty Clinics

Specialty practices often operate with lean technology teams, sometimes fewer than five staff covering all IT functions. This capacity gap delays adoption of full-featured compliance tools that require integration with EHRs and payer portals. Vendors are responding with modular, cloud-native applications that deploy in hours and offer pre-configured templates for dermatology, oncology, and behavioral health. Yet many clinics remain unaware of regulatory nuances specific to their disciplines, relying on outdated manual logs that expose them to audit risk. Until awareness campaigns and simplified offerings scale, this restraint will temper healthcare compliance software market penetration in fragmented outpatient segments.

Other drivers and restraints analyzed in the detailed report include:

- Shift from Manual Healthcare Compliance Methods to Automated Compliance Software

- Integration of AI-Enabled Auditing Reducing Manual Workload

- Perception of Compliance as a Cost Center Lowering Procurement Priority

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud platforms commanded 52.19% of the healthcare compliance software market share in 2025 as providers prioritized scalability and remote access. The segment's 17.42% forecast CAGR exceeds on-premise systems because subscription pricing converts capital expenditure to predictable operating costs and speeds implementation within weeks. Leading vendors bundle automated backup and disaster recovery, ensuring data resilience amid cyber incidents that targeted multiple U.S. hospitals in 2024. Cloud hosting also simplifies continuous rule updates; once a regulation changes, providers receive patches without downtime, unlike traditional installations that require local IT intervention. In parallel, regulatory frameworks such as HIPAA and GDPR publish guidance clarifying that certified cloud providers can meet security mandates, boosting confidence among compliance officers.

Cloud vendors further differentiate by embedding AI micro-services for real-time anomaly detection, which would be resource-intensive to run on local servers. Hospitals leveraging these analytics report double-digit reductions in audit cycle times. Country-level initiatives, including India's ABDM digital-health program and Japan's Medical Information System infrastructure, reference cloud architectures, strengthening regional demand. Consequently, cloud deployments will remain the primary engine driving the healthcare compliance software market through 2031, especially among multi-site health systems seeking unified oversight across geographies.

The Healthcare Compliance Software Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, Web-Based), Solution Module (Policy & Procedure Management, Auditing Tools, and More), End User (Hospitals, Specialty & Out-Patient Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved 44.68% of the healthcare compliance software market share in 2025, supported by rigorous enforcement of HIPAA, HITECH, and the False Claims Act. Widespread cloud adoption accelerates software deployment; surveys reveal 91% of U.S. hospitals now run portions of their infrastructure in the cloud. CMS's push toward total accountable-care participation by 2030 further elevates documentation and quality-reporting requirements, compelling investment in integrated compliance platforms. Provider organizations increasingly bundle compliance modules with EHR upgrades, driving cross-selling opportunities. AI-powered audit capabilities gain traction as board-level scrutiny of fraud and waste intensifies after multiple high-profile enforcement actions in 2024.

Asia-Pacific records the highest growth, forecast at 18.12% CAGR, significantly outpacing the global average. China's Personal Information Protection Law and India's Digital Personal Data Protection Act impose strict penalties, motivating providers to deploy automated monitoring to avoid fines. Public-private partnerships in Japan and Australia fund telehealth expansion in rural regions, and each initiative requires compliance technology to secure patient data transmissions. Multinational life-science firms operating across the region adopt unified platforms to harmonize anti-bribery, pharmacovigilance, and data-privacy controls, further scaling the healthcare compliance software market size.

Europe contributes steady demand as GDPR fines reach new highs, with several hospitals ordered to pay multi-million-dollar penalties for data breaches in 2024. Providers prioritize solutions that consolidate healthcare-specific regulations with broader data-protection mandates, streamlining reporting to supervisory authorities. Middle East & Africa and South America remain emerging markets but post rising adoption in tertiary centers located in the United Arab Emirates, Saudi Arabia, Brazil, and Colombia. Mobile-friendly compliance apps enable frontline staff to complete checklists in low-bandwidth settings, supporting incremental market penetration where fixed networks are sparse.

- RLDatix

- Healthicity LLC

- HealthStream Inc.

- Compliancy Group LLC

- Atlantic.Net

- VielSun

- Accountable HQ Inc.

- Complinity Technologies Pvt Ltd

- Radar Healthcare

- ConvergePoint Inc.

- Beacon Healthcare Systems

- Sprinto

- NAVEX Global

- ByteChek, Inc.

- Verge Health

- MedTrainer

- Protenus

- Intraprise Health

- Symplr

- Accruent (Connectiv)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Tele-health Requiring HIPAA-Compliant Platforms

- 4.2.2 Emphasis on Patient-Centered Care

- 4.2.3 Shift from Manual Healthcare Compliance Methods to Automated Compliance Software

- 4.2.4 Integration of AI-Enabled Auditing Reducing Manual Workload

- 4.2.5 Rise of Value-Based Care Driving Billing-Compliance Automation

- 4.2.6 Increasing Cybersecurity Threats Prompting Robust Compliance Monitoring

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness & Limited IT Resources among Specialty Clinics

- 4.3.2 Perception of Compliance as a Cost Center Lowering Procurement Priority

- 4.3.3 High Implementation Costs

- 4.3.4 Complexity of Multi-Jurisdictional Regulatory Requirements

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Web-Based

- 5.2 By Solution Module

- 5.2.1 Policy & Procedure Management

- 5.2.2 Auditing Tools

- 5.2.3 Training Management & Tracking

- 5.2.4 Medical Billing & Coding

- 5.2.5 License, Certificate & Contract Tracking

- 5.2.6 Incident Management

- 5.2.7 Accreditation Management

- 5.2.8 Other Modules

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty & Out-Patient Clinics

- 5.3.3 Other Healthcare Facilities

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 RLDatix

- 6.3.2 Healthicity LLC

- 6.3.3 HealthStream Inc.

- 6.3.4 Compliancy Group LLC

- 6.3.5 Atlantic.Net

- 6.3.6 VielSun

- 6.3.7 Accountable HQ Inc.

- 6.3.8 Complinity Technologies Pvt Ltd

- 6.3.9 Radar Healthcare

- 6.3.10 ConvergePoint Inc.

- 6.3.11 Beacon Healthcare Systems

- 6.3.12 Sprinto

- 6.3.13 NAVEX Global

- 6.3.14 ByteChek, Inc.

- 6.3.15 Verge Health

- 6.3.16 MedTrainer

- 6.3.17 Protenus

- 6.3.18 Intraprise Health

- 6.3.19 Symplr

- 6.3.20 Accruent (Connectiv)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment