|

시장보고서

상품코드

1906262

유럽의 경질 플라스틱 포장 시장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Rigid Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

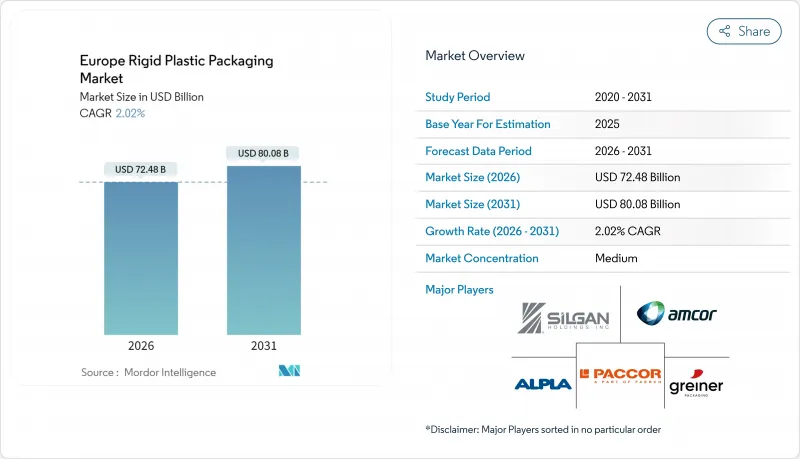

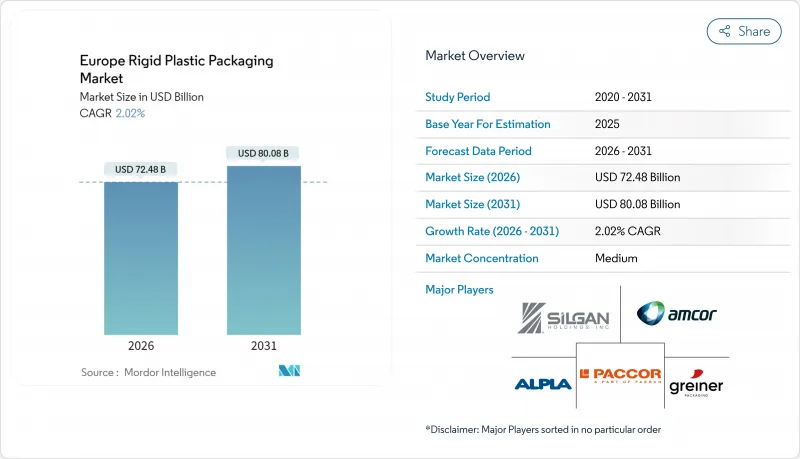

유럽의 경질 플라스틱 포장 시장은 2025년의 710억 4,000만 달러에서 2026년에는 724억 8,000만 달러로 성장할 것으로 보이며, 2026-2031년에 걸쳐 CAGR2.02%로 성장을 지속하여, 2031년에는 800억 8,000만 달러에 이를 전망입니다.

더 엄격한 수거 목표, 최소 재활용 함량 기준, 그리고 자재세는 설계 선택, 조달 전략, 자본 배분을 재편하고 있습니다. 보증금 반환 제도(DRS)는 증가하는 재활용 PET 수요를 뒷받침하는 한편, 에너지 가격 변동성과 원료 인플레이션은 운영 효율화 프로그램을 가속화합니다. 대형 가공업체들은 규정 준수 자원을 통합하기 위해 합병을 추진하고 있으며, 폐쇄형 순환 인프라에 조기 투자한 생산자들은 음료, 식품, 의료 브랜드 소유주들과의 상업적 우위를 확보하고 있습니다. 섬유 기반 대체재로 인한 소재 대체 압박은 경쟁을 심화시키고 있지만, 경량화 유인보다 높은 차단성, 재사용성 또는 충격 저항성 요구 사항이 우선시되는 분야에서는 경질 포맷이 여전히 방어 가능한 위치를 유지하고 있습니다.

유럽의 경질 플라스틱 포장 시장 동향 및 인사이트

음료 분야에서 재생 가능 경질 PET 병 수요 급증

독일에서 이미 90% 이상의 회수율을 달성한 보증금 반환 제도는 유럽 전역에 유사한 도입을 촉진하며 식품 등급 rPET 원료 수요를 끌어올리고 있습니다. 포르투갈 시범 사업은 일일 역판매기당 1,281개 포장재 회수라는 기술적 실현 가능성을 입증했으며, 투명 청색 PET가 반환의 대부분을 차지하여 색상 표준화가 분류 효율화에 미치는 영향력을 강조했습니다. 2025년까지 PET 병에 25%, 2030년까지 30%의 재활용 함량을 의무화하는 EU 규정은 유럽의 300만 톤 세척 및 140만 톤 펠릿 생산 능력에도 불구하고 공급 부족 상태의 2차 원료 풀을 창출합니다. 따라서 브랜드 소유자들은 양자 간 구매 계약을 체결하여 세척 라인과 압출 반응기의 개조를 촉진하고 있습니다. 그 결과, PET 병은 가장 빠르게 성장하는 경질 포맷으로 남아 있으며 향후 수지 재활용 투자의 절반 이상을 차지할 전망입니다.

급성장하는 전자상거래, 보호용 경질 포맷 수요 증대

2024년 유럽 전체 상품 판매에서 온라인 유통 비중이 22%를 넘어섬에 따라, 다단계 물류망에서도 손상되지 않는 내충격성 용기에 대한 수요가 증가하고 있습니다. 경질 드럼, 페일, 적층형 통은 소포가 자동 분류 허브를 통과할 때 파손률과 보증 청구를 줄여주며, 제품 손상 감소로 인한 비용 절감이 중량 불이익을 상쇄할 경우 유통업체들은 소량의 재료 증가를 수용합니다. 2030년까지 1인당 포장 폐기물 발생량이 209kg에 달할 것으로 예상됨에 따라 규제 당국은 이제 적정 크기 설계 증명을 요구하고 있습니다. 그럼에도 불구하고 보호용 경질 솔루션은 수명 주기상 손상 방지 측면에서 종종 우위를 점하며, 전자상거래 대응 설계를 목표로 하는 변환업체들의 단기적 성장세를 유지하고 있습니다.

일회용 플라스틱세와 확대 생산자 책임 제도

2025년부터 시행되는 환경 조정 요금은 재활용성이 제한된 경질 포장재에 불이익을 주어 기존 디자인의 규정 준수 비용을 증가시킵니다. 이탈리아의 폴리스티렌 트레이에 부과되는 톤당 800유로(866달러)와 프랑스의 단일 소재 PET에 부과되는 톤당 456유로(494달러) 같은 차등 과세는 포맷 전환을 촉진하고 SKU 합리화를 유도합니다. 대형 가공업체는 규모의 경제를 통해 비용을 흡수하지만, 소규모 성형업체는 마진 축소 또는 퇴출 위험에 직면하여 업계 통합이 가속화됩니다.

부문 분석

병 및 항아리는 2025년 유럽 경질 플라스틱 포장 시장 규모의 43.22%에 해당하는 307억 1,000만 달러를 차지했으며, 2031년까지 연평균 2.74%의 가장 빠른 성장률을 유지할 전망입니다. 이러한 성장 동력은 음료 산업의 DRS 호환 PET 포맷 의존도와 제약 산업의 멸균 가능 HDPE 알약 용기 수요에서 비롯됩니다. 트레이 및 용기 수요는 냉장식품 유통에서 안정적이지만, PFAS 금지 조치로 인해 차단 코팅 기술 혁신이 촉진되고 있습니다. 캡 및 마개는 2024년 7월까지 모든 일회용 음료 포장재에 의무화되는 연결형 디자인으로 진화하며, 마개 공급업체 전반에 걸쳐 금형 업그레이드를 촉진하고 있습니다.

중간 벌크 컨테이너 및 드럼은 화학 물류 분야에서 탄력적인 틈새 시장을 형성했으나, 전자상거래 소포 밀도가 유연 라이너의 광범위한 교체를 정당화하기에는 아직 미흡합니다. 고밀도 폴리에틸렌 데크를 재생하는 순환 풀 운영업체에 힘입어 팔레트 및 기타 경질 액세서리는 점진적 성장을 유지합니다. 따라서 제품 구성은 여전히 병에 중점을 두어, PET와 HDPE가 유럽 경질 플라스틱 포장 시장의 수지 소비를 주도할 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 음료 분야에서 재생 가능한 경질 PET 병 수요 급증

- 전자상거래 붐으로 인한 보호용 경질 포장재 수요 증가

- EU 보증금 반환 제도 확대로 인한 회수 인프라 가속

- 리필 및 재사용 매장 시범 운영으로 HDPE 병 재설계 촉진

- 유럽의 바이오플라스틱 생산 능력 급속한 확대

- 의약품 콜드체인 확대에 따른 고 배리어성 경질 포장재 수요

- 시장 성장 억제요인

- 일회용 플라스틱 세금 및 생산자 책임 확대(EPR) 비용

- 경량화를 위한 종이 및 유연한 대체품으로의 이행

- 변동성 있는 rPET 및 rHDPE 가격으로 인한 가공업체 마진 압박

- 에너지 가격의 급등의 압출 성형 및 사출 성형 비용 상승

- 업계 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 병 및 항아리

- 트레이 및 용기

- 캡 및 마개

- 중간 벌크 컨테이너(IBC)

- 드럼

- 팔레트

- 기타 제품 유형

- 소재별

- 폴리에틸렌(PE)

- 폴리에틸렌테레프탈레이트(PET)

- 폴리프로필렌(PP)

- 폴리스티렌(PS) 및 발포 폴리스티렌(EPS)

- 폴리염화비닐(PVC)

- 기타 경질 플라스틱 재료

- 최종 사용자 업계별

- 식품

- 음료

- 헬스케어

- 화장품 및 퍼스널케어

- 산업

- 건축 및 건설

- 자동차

- 기타 최종 사용자 산업

- 국가별

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 폴란드

- 네덜란드

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Alpla Werke Alwin Lehner GmbH & Co KG

- Mauser Packaging Solutions Holding Company

- Amcor plc

- Greiner Packaging International GmbH

- Greif, Inc.

- PACCOR Packaging GmbH(Faerch Group)

- Plastipak Holdings, Inc.

- Schoeller Allibert Services BV

- Silgan Holdings Inc.

- Albea Group

- Coda Plastics Ltd.

- Frapak Packaging BV

- Schutz GmbH & Co. KGaA

- WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- ACTI PACK SAS

- RETAL Industries Ltd.

- RIKUTEC Group

- AST Kunststoffverarbeitung GmbH

- Robinson plc

- Esterform Packaging Ltd.

제7장 시장 기회와 장래의 전망

HBR 26.01.26The Europe rigid plastic packaging market is expected to grow from USD 71.04 billion in 2025 to USD 72.48 billion in 2026 and is forecast to reach USD 80.08 billion by 2031 at 2.02% CAGR over 2026-2031.

Stricter collection targets, minimum recycled-content thresholds, and material taxes are reshaping design choices, procurement strategies, and capital allocation. Deposit-return schemes (DRS) underpin rising recycled PET demand, while energy-price volatility and feedstock inflation accelerate operational efficiency programs. Large converters pursue mergers to pool compliance resources, and producers that invest early in closed-loop infrastructure secure commercial advantages with beverage, food, and healthcare brand owners. Material substitution pressures from fiber-based alternatives intensify competition, yet rigid formats retain defensible positions wherever high barrier, reusability, or impact resistance requirements outweigh lightweighting incentives.

Europe Rigid Plastic Packaging Market Trends and Insights

Surging Demand for Recyclable Rigid PET Bottles in Beverages

Deposit-return schemes already deliver collection rates above 90% in Germany and inspire similar adoption across the bloc, lifting demand for food-grade rPET feedstock. Portugal's pilot proved technical viability with 1,281 packages captured per reverse-vending unit daily, and transparent blue PET accounted for most returns, underlining the power of color standardization to streamline sorting. The EU obligation for 25% recycled content in PET bottles by 2025 and 30% by 2030 creates an undersupplied secondary-material pool despite Europe's 3 million-tonne washing and 1.4 million-tonne pellet capacity. Brand owners therefore lock in bilateral offtake agreements, stimulating retrofits of washing lines and extrusion reactors. As a result, PET bottles remain the fastest-growing rigid format and anchor more than half of the upcoming resin recycling investments.

Booming E-commerce Boosting Protective Rigid Formats

Online retail penetration exceeded 22% of total European goods sales in 2024, heightening the need for impact-resistant containers that survive multi-node fulfillment chains. Rigid drums, pails, and stackable tubs reduce breakage rates and warranty claims as parcels transit automated sorting hubs, and retailers accept marginal material increases when product-damage savings offset weight penalties. With packaging waste generation projected at 209 kg per capita by 2030, regulators now demand right-sizing evidence; nonetheless, protective rigid solutions often score favorably on life-cycle damage avoidance, sustaining a near-term boost for converters targeting e-commerce-ready designs.

Single-Use Plastic Taxes and Extended Producer Responsibility Fees

Eco-modulated fees, effective from 2025, penalize rigid packs with limited recyclability, inflating compliance outlays for legacy designs. Differential levies-EUR 800/ton (USD 866/ton) on polystyrene trays in Italy versus EUR 456/ton (USD 494/ton) on mono-material PET in France, drive format migration and prompt SKU rationalization. Large converters absorb charges via scale efficiencies, but small molders risk margin erosion or exit, accelerating sector consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Growth of EU Deposit-Return Schemes Accelerating Collection Infrastructure

- Rapid Scale-up of European Bioplastics Capacity

- Shift Toward Paper and Flexible Substitutes for Lightweighting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bottles and jars contributed USD 30.71 billion, equal to 43.22% of Europe's rigid plastic packaging market size in 2025, and will keep expanding fastest at a 2.74% CAGR to 2031. This momentum stems from beverage-sector reliance on DRS-compatible PET formats and pharma demand for sterilizable HDPE pill containers. Tray and container demand hold steady in chilled-food distribution, yet PFAS bans compel barrier-coating innovation. Caps and closures evolve toward tethered designs, mandated on all single-use beverage packs by July 2024, spurring tooling upgrades across closure suppliers.

Intermediate bulk containers and drums carved a resilient niche in chemical logistics; however, e-commerce parcel density has yet to justify the broad replacement of flexible liners. Pallets and other rigid accessories maintain incremental growth, driven by circular pool operators that refurbish high-density polyethylene decks. The product mix thus remains weighted toward bottles, ensuring that PET and HDPE dominate resin off-take in the European rigid plastic packaging market.

The Europe Rigid Plastic Packaging Market Report is Segmented by Product Type (Bottles and Jars, Trays and Containers, Caps and Closures, Intermediate Bulk Containers, and More), Material (Polyethylene (PE), Polyethylene Terephthalate (PET), Polypropylene (PP), and More), End-User Industry (Food, Beverage, Healthcare, Cosmetics and Personal Care, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Alpla Werke Alwin Lehner GmbH & Co KG

- Mauser Packaging Solutions Holding Company

- Amcor plc

- Greiner Packaging International GmbH

- Greif, Inc.

- PACCOR Packaging GmbH (Faerch Group)

- Plastipak Holdings, Inc.

- Schoeller Allibert Services B.V.

- Silgan Holdings Inc.

- Albea Group

- Coda Plastics Ltd.

- Frapak Packaging B.V.

- Schutz GmbH & Co. KGaA

- WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- ACTI PACK S.A.S.

- RETAL Industries Ltd.

- RIKUTEC Group

- AST Kunststoffverarbeitung GmbH

- Robinson plc

- Esterform Packaging Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for recyclable rigid PET bottles in beverages

- 4.2.2 Booming e-commerce boosting protective rigid formats

- 4.2.3 Growth of EU deposit-return schemes accelerating collection infrastructure

- 4.2.4 Refill-and-reuse store pilots driving HDPE bottle redesigns

- 4.2.5 Rapid scale-up of European bioplastics capacity

- 4.2.6 Pharma cold-chain expansion needing high-barrier rigid packs

- 4.3 Market Restraints

- 4.3.1 Single-use-plastic taxes and Extended Producer Responsibility fees

- 4.3.2 Shift toward paper and flexible substitutes for lightweighting

- 4.3.3 Volatile rPET and rHDPE prices squeezing converter margins

- 4.3.4 Energy-price shocks raising extrusion and injection costs

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bottles and Jars

- 5.1.2 Trays and Containers

- 5.1.3 Caps and Closures

- 5.1.4 Intermediate Bulk Containers (IBCs)

- 5.1.5 Drums

- 5.1.6 Pallets

- 5.1.7 Other Product Types

- 5.2 By Material

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polyethylene Terephthalate (PET)

- 5.2.3 Polypropylene (PP)

- 5.2.4 Polystyrene (PS) and Expanded PS (EPS)

- 5.2.5 Polyvinyl Chloride (PVC)

- 5.2.6 Other Rigid Plastic Materials

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare

- 5.3.4 Cosmetics and Personal Care

- 5.3.5 Industrial

- 5.3.6 Building and Construction

- 5.3.7 Automotive

- 5.3.8 Other End-user Industries

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Poland

- 5.4.7 Netherlands

- 5.4.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alpla Werke Alwin Lehner GmbH & Co KG

- 6.4.2 Mauser Packaging Solutions Holding Company

- 6.4.3 Amcor plc

- 6.4.4 Greiner Packaging International GmbH

- 6.4.5 Greif, Inc.

- 6.4.6 PACCOR Packaging GmbH (Faerch Group)

- 6.4.7 Plastipak Holdings, Inc.

- 6.4.8 Schoeller Allibert Services B.V.

- 6.4.9 Silgan Holdings Inc.

- 6.4.10 Albea Group

- 6.4.11 Coda Plastics Ltd.

- 6.4.12 Frapak Packaging B.V.

- 6.4.13 Schutz GmbH & Co. KGaA

- 6.4.14 WERIT Kunststoffwerke W. Schneider GmbH & Co. KG

- 6.4.15 ACTI PACK S.A.S.

- 6.4.16 RETAL Industries Ltd.

- 6.4.17 RIKUTEC Group

- 6.4.18 AST Kunststoffverarbeitung GmbH

- 6.4.19 Robinson plc

- 6.4.20 Esterform Packaging Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment