|

시장보고서

상품코드

1906273

안구 감염 치료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Eye Infection Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

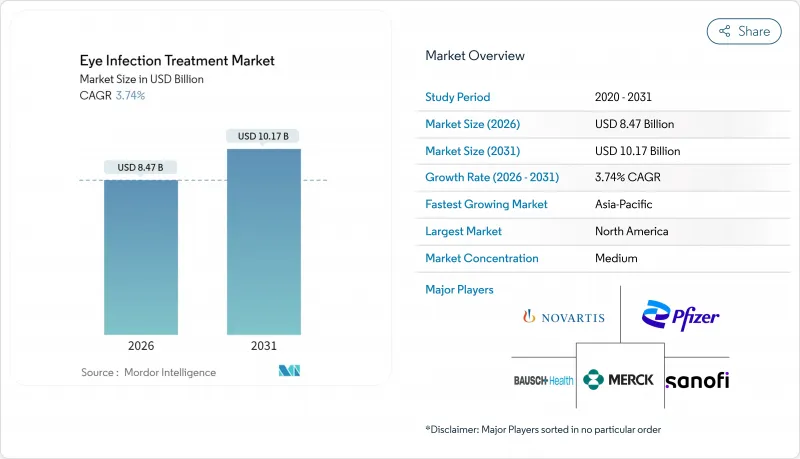

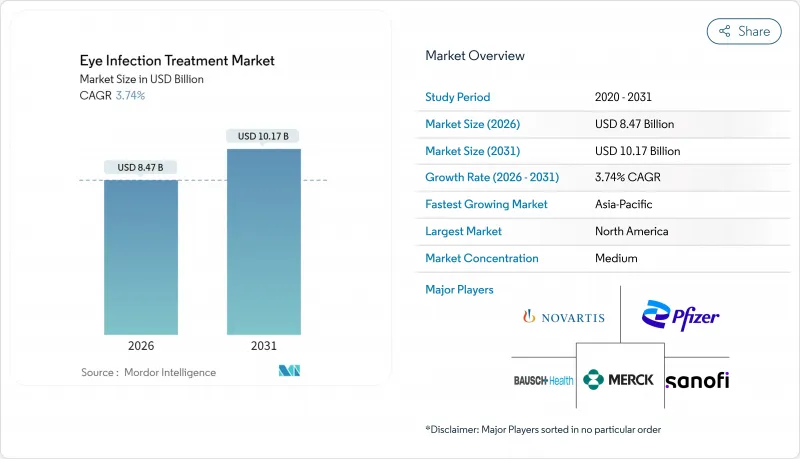

안구 감염 치료 시장은 2025년 81억 6,000만 달러에서 2026년에는 84억 7,000만 달러로 성장할 것으로 예측되고, 2026-2031년에 걸쳐 CAGR 3.74%로 성장을 지속하여 2031년까지 101억 7,000만 달러에 달할 것으로 예측됩니다.

기존 항생제가 제네릭 압박에 직면하는 가운데, 지속 방출 전달 기술의 혁신과 고령 및 당뇨병 환자층의 증가가 점진적 성장을 뒷받침하며 중등도의 시장 확대가 이루어지고 있습니다. 항생제 내성 억제를 위한 지속적인 노력은 새로운 작용 기전과 복합 요법에 대한 수요를 높이는 한편, 투여 빈도를 줄이고 복약 순응도를 개선하는 약물에 대한 프리미엄 가격 책정 기회가 부상하고 있습니다. 세계의적으로 수술 건수가 지속적으로 증가하면서 예방적 치료 부문이 확대되고 프리미엄 예방 치료의 채택이 지속되고 있습니다. 경쟁 강도는 특허 만료, 지적 재산권을 통합하는 기업 인수, 획기적 치료제 지정을 위한 신속한 규제 경로에 의해 정의됩니다.

세계의 안구 감염 치료 시장 동향 및 인사이트

세계의 안구 감염의 부담 증가

감염성 안구 질환 발생률은 눈물막을 약화시키고 병원체의 침투 경로를 생성하는 디지털 기기 사용과 함께 증가하고 있습니다. 기후 변동성은 병원체 분포를 변화시켜 곰팡이 각막염을 이전 온대 지역으로 확산시키고 있습니다. 과소진단되던 모낭충성 안검염은 전문 클리닉 방문 환자의 57.7%에게 영향을 미치며 새로운 살충제 치료 수요를 촉진합니다. 위생 교육이 도입 속도를 따라가지 못하는 신흥 경제국에서 콘택트렌즈 착용률이 증가하며 세균성 각막염 사례가 늘고 있습니다. 백내장 및 굴절 수술 건수 증가로 수술 후 예방 치료 시장이 확대되는 한편, 농촌 지역의 이동 안과 진료소는 기존에 숨겨진 감염 누적 사례를 드러내고 있습니다.

고령화 및 당뇨병 환자 증가

세계적 고령화로 면역력이 약화된 수백만 명의 소비자가 안구 감염에 취약해지고 있으며, 당뇨병 유병률 증가로 수술 및 주사 노출 환자 집단이 확대되고 있습니다. 2024년 당뇨병성 망막병증 관련 세계의 실명 환자는 107만 명, 시각 장애 환자는 328만 명에 달했으며, 남미와 카리브해 지역이 6.95%로 가장 높은 유병률을 보였습니다. 메디케어 기록에 따르면 당뇨성 황반부종에 대한 항-VEGF 사용률은 2009년부터 2018년 사이 16%에서 35%로 증가했습니다. 반복적인 안구 내 시술은 감염 위험을 높이고 예방적 항생제 수요를 확대합니다. 2050년까지 1,400만 건으로 증가할 것으로 예상되는 노인성 황반변성 환자는 엄격한 감염 예방이 필요한 환자 기반을 확대합니다.

특허 만료과 격화하는 제네릭 경쟁

2022-2024년 사이 블록버스터 항생제 특허가 만료되었으며, 현재 미국 안과 처방의 91%를 제네릭이 차지하고 있습니다. 도르졸라미드-티몰롤 사례에서 보듯, 제네릭 제조사 통합으로 인한 공급 부족이 치료 연속성을 방해하고 있습니다. FDA의 제품별 지침은 추가 제네릭 승인을 가속화하여 혁신 기업의 가격 실현을 압박하고 있습니다. 브랜드 소유사들은 서방형 제제 및 고정 용량 복합제로 대응하고 있으나, 점진적 혁신 주장에 대한 심사를 받고 있습니다.

부문 분석

항생제는 2025년 안구 감염 치료 시장의 매출에서 43.02%를 차지했으며, 이는 세균성 결막염 및 각막염에 대한 확고한 사용을 반영합니다. 동시에 항바이러스제는 중합효소연쇄반응(PCR) 진단법이 바이러스성 원인을 보다 신뢰성 있게 검출하고 헤르페스 각막염 예방이 일상화됨에 따라 2031년까지 연평균 5.54%의 가장 빠른 성장률을 기록할 것으로 전망됩니다. 항진균제는 틈새 시장을 유지하지만, 진균성 각막염이 높은 실명 위험을 초래하는 열대 지역에서는 여전히 필수적입니다. 항히스타민제와 코르티코스테로이드는 염증성 동반 질환에 사용되며, 최근 승인된 1일 1회용 알레시온 크림은 복용 순응도 한계를 타깃으로 합니다. 부문 혁신은 감염과 염증을 동시에 억제하는 고정 복합제를 선호하는 추세로, 이는 항바이러스제와 코르티코스테로이드 복합제 모두를 강화할 것으로 예상됩니다. 항생제 기반 안구 감염 치료 시장 규모는 소폭 성장할 것으로 예상되나, 항바이러스제는 낮은 기반에도 불구하고 비례하지 않는 증가 가치를 창출할 것입니다.

임상 도입 동향에 따르면 연구 중인 리포글리코펩타이드와 순환펩타이드가 10년 후반까지 진료 현장에 도입되어 새로운 제품군을 창출할 수 있습니다. 동시에 펩타이드 결합 나노입자 플랫폼은 안구 생체이용률을 높여 안구 감염 치료 시장 내 항생제 점유율을 소폭 확대할 수 있습니다. 현재 포트폴리오 전략은 특히 병원성 각막염 분야에서 내성 극복 구조적 계열을 강조하는 한편, 국소 면역조절제는 숙주 반응 조절을 목표로 하여 안구 감염 치료 산업 전반에 걸쳐 수익원을 더욱 다각화하고 있습니다.

지역별 분석

북미는 2025년 안구 감염 치료 시장 매출의 38.40%를 차지했으며, 이는 강력한 보험 적용 범위, 높은 수술 처리량, 로틸라네르(lotilaner)와 같은 혁신적 승인 제품의 빠른 도입을 반영합니다. 메디케어 청구 데이터는 유리체강 내 주사 건수가 증가하고 있음을 보여주며, 이는 예방적 항생제 사용을 강화하고 새로운 지속 방출 장치의 문을 열어줍니다. 그러나 지불자의 압박과 공격적인 제네릭 진입은 가격 탄력성을 제한하는 반면, 항생제 내성으로 인해 더 비싼 2차 치료 옵션이 필요해지고 있습니다.

아시아태평양은 고령화, 당뇨병 유병률 상승, 중산계급의 선택적 안과 의료에 대한 접근 확대에 힘입어 2031년까지 4.51%라는 최고 CAGR을 달성할 것으로 예측됩니다. 중국과 인도는 수술 건수 증가를 주도하고 있으며, 인도의 고효율 백내장 센터는 예방약 수요를 확대하는 확장 가능한 의료 모델을 실증하고 있습니다. 그러나 의사 부족(지역의 46.2% 국가만이 10,000명당 1명의 안과의 비율을 충족함)이 원격 진단 및 약국 주도 제제에 대한 잠재적인 수요를 야기하며, 이는 시판약과 처방약의 병용 요법을 지원하는 생태계를 형성하고 있습니다.

유럽은 보편적 의료보험이 광범위한 접근을 장려하며 꾸준한 성장을 보이지만, 재정 규율이 제네릭 의약품 사용을 선호합니다. EU 항생제 관리 정책은 광범위 항생제 사용을 제한하는 동시에 좁은 스펙트럼 또는 병원체 표적 약물에 대한 관심을 가속화합니다. 라틴 아메리카 및 카리브해 지역은 세계의에서 당뇨성 망막병증 실명 유병률이 가장 높아 평균 이상의 감염 예방 수요를 창출하지만, 경제적 제약으로 인해 고가 제품 채택은 제한됩니다.

중동, 아프리카 및 남미는 여전히 시장 침투율이 낮으나, 원격 안과 진료 및 이동형 수술 장비의 보급 확대로 장기적 성장 잠재력을 지닌다. 사우디아라비아와 브라질의 현지 생산 인센티브는 제네릭 조달 패턴을 변화시키고 구매 비용을 낮출 수 있습니다. 공동 마케팅 또는 위탁 생산 계약을 통해 진출하는 다국적 기업들은 현지 복약 순응도에 맞춰 포장 규모와 용량을 조정함으로써 초기 시장 점유율을 확보할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 안구 감염의 세계적 부담 증가

- 고령화 및 당뇨병 환자 증가

- 안과용 항감염제의 연구개발 투자 가속

- 국소 복합 요법 채택 확대

- 신흥 경제국에서 안과 의료에 대한 접근 확대

- 지속 방출형 약물 전달 플랫폼의 발전

- 시장 성장 억제요인

- 특허 만료와 심화되는 제네릭 경쟁

- 안과용 항감염제의 부작용 및 금기 사항

- 항균제 내성에 대한 우려 증가

- 엄격한 규제 장벽과 가격 압력

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 약물 종류별

- 항생제

- 항바이러스제

- 항진균제

- 항히스타민제

- 코르티코스테로이드

- 글루코코르티코이드

- 적응증별

- 결막염

- 각막염

- 안구내염

- 안검염

- 밀립종

- 포도막염

- 봉와직염

- 안부 헤르페스

- 제형별

- 점안액

- 정제/캡슐

- 안연고

- 기타 제형

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Novartis AG

- Alcon AG

- Pfizer Inc.

- Bausch Health Companies Inc.

- Santen Pharmaceutical Co., Ltd.

- Merck & Co., Inc.

- Sanofi SA

- Allergan Plc(AbbVie)

- Johnson & Johnson Vision Care

- Gilead Sciences Inc.

- Regeneron Pharmaceuticals Inc.

- Roche Holding AG

- Leadiant Biosciences

- Xellia Pharmaceuticals

- Aurolab

- Aerie Pharmaceuticals Inc.

- Sun Pharma Industries Ltd.

- Akorn Operating Co. LLC

- Nicox SA

- Kala Pharmaceuticals Inc.

제7장 시장 기회와 장래의 전망

HBR 26.01.26The eye infection treatment market is expected to grow from USD 8.16 billion in 2025 to USD 8.47 billion in 2026 and is forecast to reach USD 10.17 billion by 2031 at 3.74% CAGR over 2026-2031.

This moderate expansion occurs while established antibiotics confront growing generic pressure, yet innovations in sustained-release delivery and a rising pool of elderly and diabetic patients support incremental growth. Ongoing efforts to contain antimicrobial resistance elevate demand for new mechanisms of action and combination regimens, while premium pricing opportunities emerge for drugs that cut dosing frequency and improve adherence. Surgical volumes continue increasing worldwide, creating larger prophylactic segments and sustaining premium prophylactic therapy uptake. Competitive intensity is defined by patent expiries, corporate acquisitions that consolidate intellectual property, and faster regulatory pathways for breakthrough designations.

Global Eye Infection Treatment Market Trends and Insights

Rising Global Burden of Ocular Infections

Incidence of infectious eye disease now rises in tandem with digital device use that weakens the tear film and creates entry points for pathogens. Climate variability changes pathogen distribution, pushing fungal keratitis into previously temperate regions. Demodex blepharitis, once under-diagnosed, affects 57.7% of patients visiting specialist clinics and fuels demand for novel acaricidal therapies. Contact lens wear climbs across emerging economies were hygiene education trails adoption, raising bacterial keratitis cases. Growing cataract and refractive surgery volumes enlarge postoperative prophylaxis segments, while mobile ophthalmology camps in rural areas reveal previously hidden infection backlogs.

Increasing Geriatric and Diabetic Populations

Global aging adds millions of immune-compromised consumers prone to ocular infection, while diabetes prevalence enlarges the surgical and injection-exposed cohort. Worldwide blindness linked to diabetic retinopathy reached 1.07 million persons in 2024 and visually impaired cases hit 3.28 million, with South America and the Caribbean bearing the highest 6.95% prevalence. Medicare records show anti-VEGF usage for diabetic macular edema climbing from 16% to 35% between 2009-2018. Repeated intraocular procedures heighten infection risk and expand prophylactic antibiotic demand. Projected rise to 14 million age-related macular degeneration cases by 2050 widens the patient base needing stringent infection prevention.

Patent Cliffs and Intensifying Generic Competition

Blockbuster antibiotic patents expired between 2022-2024, and generics now account for 91% of ophthalmic prescriptions in the United States. Consolidated generic manufacturing has triggered shortages, as seen with dorzolamide-timolol, disrupting care continuity. FDA product-specific guidance accelerates additional generic approvals, squeezing price realization for innovators. Brand owners respond with sustained-release and fixed-dose combinations but face scrutiny over incremental innovation claims.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating R&D Investments in Ophthalmic Anti-Infectives

- Growing Adoption of Topical Combination Therapies

- Escalating Antimicrobial Resistance Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Antibiotics accounted for 43.02% of 2025 revenue in the eye infection treatment market, reflecting entrenched use in bacterial conjunctivitis and keratitis. Concurrently, antivirals are forecast to register a 5.54% CAGR to 2031, the fastest among classes, as polymerase-chain-reaction diagnostics more reliably detect viral etiologies and as herpes keratitis prophylaxis becomes routine. Antifungals retain a niche, yet they remain indispensable in tropical belts where fungal keratitis imposes high blindness risk. Antihistamines and corticosteroids serve inflammatory comorbidities; recent approval of once-daily Alesion cream targets compliance limitations. Segment innovation favors fixed combinations that suppress infection and inflammation together, a theme expected to bolster antivirals and corticosteroid-laden hybrids alike. The eye infection treatment market size for antibiotics is expected to grow modestly, but antivirals will contribute disproportionate incremental value despite a lower base.

Clinical adoption trends indicate that lipoglycopeptides and cyclic peptides under investigation may enter practice circles by late decade, creating fresh product categories. In tandem, peptide-bound nanoparticle platforms could lift ocular bioavailability and marginally expand the antibiotic share within the eye infection treatment market. Portfolio strategies now emphasize resistance-breaking structural classes, especially in hospital-acquired keratitis, while topical immunomodulators aim to modulate host response, further diversifying revenue streams across the eye infection treatment industry.

The Eye Infection Treatment Market Report is Segmented by Drug Class (Antibiotics, Antivirals, and More), Indication (Conjunctivitis, Keratitis, and More), Dosage Form (Eye Drops, Tablets/Capsules, Ophthalmic Ointments, and Other Dosage Forms), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 38.40% of 2025 revenue in the eye infection treatment market, reflecting robust insurance coverage, high surgical throughput, and rapid uptake of breakthrough approvals like lotilaner. Medicare claims data show rising intravitreal injection numbers, which intensify prophylactic antibiotic usage and open the door for novel sustained-release devices. However, payer pressure and aggressive generic entry restrain price elasticity, even as antimicrobial resistance forces costlier second-line options.

Asia-Pacific is expected to deliver the highest 4.51% CAGR through 2031, buoyed by aging populations, escalating diabetes prevalence, and expanding middle-class access to elective eye care. China and India drive surgical volume gains; Indian high-throughput cataract centers demonstrate scalable care models that amplify prophylactic drug demand. However, practitioner shortages-only 46.2% of regional countries meet the 1:10,000 optometrist ratio-create latent demand for remote diagnosis and pharmacy-led dispensing, an ecosystem supportive of combination over-the-counter therapies.

Europe posts steady growth as universal healthcare encourages broad access, but fiscal discipline favors generics. EU antimicrobial stewardship limits broad-spectrum use, yet it simultaneously accelerates interest in narrow-spectrum or pathogen-targeted drugs. Latin America and the Caribbean record the highest diabetic retinopathy blindness prevalence worldwide, generating above-average infection prophylaxis demand, though economic constraints temper premium adoption.

The Middle East & Africa and South America remain under-penetrated but represent long-term upside as tele-ophthalmology and portable surgical units expand reach. Local production incentives in Saudi Arabia and Brazil could shift generic sourcing patterns and lower acquisition costs. Multinational firms entering via co-marketing or contract-manufacturing arrangements may capture early share by tailoring packaging sizes and dosing to local compliance behavior.

- Novartis

- Alcon

- Pfizer

- Bausch Health

- Santen Pharmaceuticals

- Merck

- Sanofi

- Allergan Plc (AbbVie)

- Johnson & Johnson Vision Care

- Gilead Sciences

- Regeneron Pharmaceuticals

- Roche

- Leadiant Biosciences

- Xellia Pharmaceuticals

- Aurolab

- Aerie Pharmaceutical

- Sun Pharma Industries Ltd.

- Akorn Operating Co. LLC

- Nicox S.A.

- Kala Pharmaceuticals Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Burden of Ocular Infections

- 4.2.2 Increasing Geriatric and Diabetic Populations

- 4.2.3 Accelerating R&D Investments in Ophthalmic Anti-Infectives

- 4.2.4 Growing Adoption of Topical Combination Therapies

- 4.2.5 Expanding Access to Eye Care In Emerging Economies

- 4.2.6 Advancements in Sustained-Release Drug Delivery Platforms

- 4.3 Market Restraints

- 4.3.1 Patent Cliffs and Intensifying Generic Competition

- 4.3.2 Adverse Effects And Contraindications Of Ocular Anti-Infectives

- 4.3.3 Escalating Antimicrobial Resistance Concerns

- 4.3.4 Stringent Regulatory Hurdles And Pricing Pressures

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Antibiotics

- 5.1.2 Antivirals

- 5.1.3 Antifungals

- 5.1.4 Antihistamines

- 5.1.5 Corticosteroids

- 5.1.6 Glucocorticoids

- 5.2 By Indication

- 5.2.1 Conjunctivitis

- 5.2.2 Keratitis

- 5.2.3 Endophthalmitis

- 5.2.4 Blepharitis

- 5.2.5 Stye (Hordeolum)

- 5.2.6 Uveitis

- 5.2.7 Cellulitis

- 5.2.8 Ocular Herpes

- 5.3 By Dosage Form

- 5.3.1 Eye Drops

- 5.3.2 Tablets / Capsules

- 5.3.3 Ophthalmic Ointments

- 5.3.4 Other Dosage Forms

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Novartis AG

- 6.3.2 Alcon AG

- 6.3.3 Pfizer Inc.

- 6.3.4 Bausch Health Companies Inc.

- 6.3.5 Santen Pharmaceutical Co., Ltd.

- 6.3.6 Merck & Co., Inc.

- 6.3.7 Sanofi S.A.

- 6.3.8 Allergan Plc (AbbVie)

- 6.3.9 Johnson & Johnson Vision Care

- 6.3.10 Gilead Sciences Inc.

- 6.3.11 Regeneron Pharmaceuticals Inc.

- 6.3.12 Roche Holding AG

- 6.3.13 Leadiant Biosciences

- 6.3.14 Xellia Pharmaceuticals

- 6.3.15 Aurolab

- 6.3.16 Aerie Pharmaceuticals Inc.

- 6.3.17 Sun Pharma Industries Ltd.

- 6.3.18 Akorn Operating Co. LLC

- 6.3.19 Nicox S.A.

- 6.3.20 Kala Pharmaceuticals Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment