|

시장보고서

상품코드

1906280

하드우드 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Hardwood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

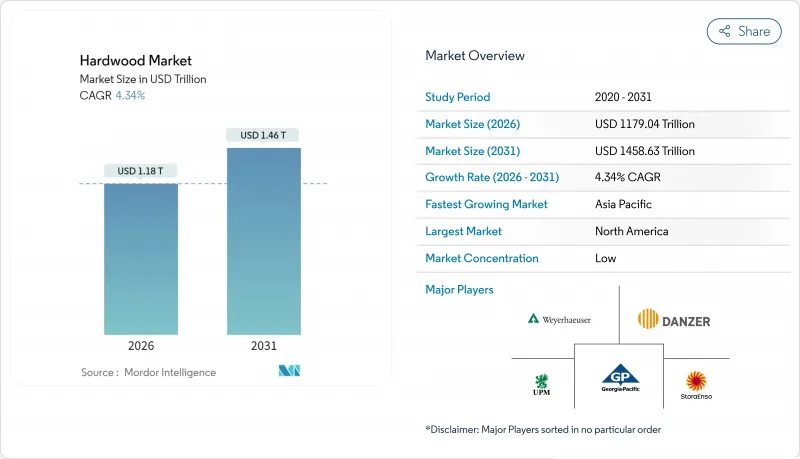

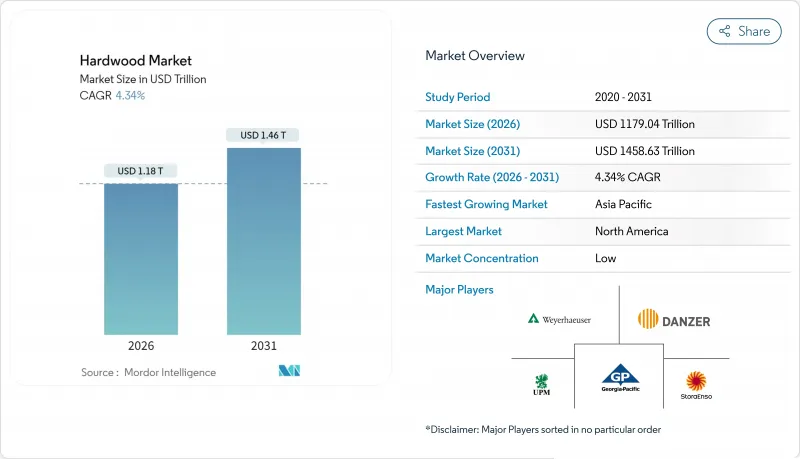

하드우드 시장은 2025년 1조 1,300억 달러로 평가되었으며, 2026년 1조 1,790억 4,000만 달러에 이르고, 2031년까지 1조 4,586억 3,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 4.34%를 나타낼 것으로 예상됩니다.

성장의 배경은 유럽연합 산림파괴방지규칙(EUDR)을 비롯한 지속가능성 규제의 강화와 건설 및 바닥재 및 고급 가구 분야에 있어서의 견고한 최종 용도 수요가 있습니다. 시장 리더 기업은 원료 조달 위험을 줄이기 위해 수직 통합 공급망에 대한 투자를 추진하고 있으며, 불법 벌채에 대한 세계 단속 강화는 컴플라이언스 비용을 밀어 올리는 반면 인증 목재의 프리미엄 가치를 더욱 높이고 있습니다. 아시아태평양의 성장 속도는 진행 중인 도시화와 중산 계급의 소비 확대에 힘입어 북미와 유럽의 약간 둔화되고 있는 아직도 규모가 큰 소비 기반과 균형을 유지하고 있습니다. 공급면에서는 제재소의 자동화에 의한 효율성 향상, 디지털 추적성의 광범위한 도입, 국내 벌채 가속을 위한 미국의 정책 동향 등 모든 것이 규율 있는 생산성 주도의 성장 시대를 시사하고 있습니다.

세계의 하드우드 시장 동향과 인사이트

세계의 친환경 빌딩 프로젝트에서 인증된 지속가능한 하드우드 소재 수요 증가

2025년 시점에서 약 2억 8,000만 헥타르의 숲이 PEFC(삼림 인증 제도 승인 프로그램) 또는 FSC(삼림 관리 협의회) 인증을 받았으며, 제3자 인증은 마케팅 부가가치가 아니라 진입 요건으로 변화하고 있습니다. 2024년 12월에 발효된 EU 삼림파괴방지규칙(EUDR)은 수출업체에게 출하별 지리위치정보를 제시할 것을 의무화하고 공급업체에 단편화된 업무 전체에서 디지털 추적성의 정비를 강요하고 있습니다. 이에 대해 FSC는 컴플라이언스 부담 경감을 위한 전용 「규제 모듈」을 도입했습니다. 인증프리미엄은 유럽역외로 확대되고 있으며, 동아시아 및 동남아시아의 수입업체도 경제협력개발기구(OECD) 시장에 대한 하류 액세스 보호를 위해 검증된 원산지 증명을 요구하는 경향이 강해지고 있습니다. 뷰로 베리타스는 FSC, PEFC, 합법성 검사를 단일 현지 조사에서 통합하는 다중 방식 감사가 현저하게 증가하고 있음을 확인하여 컴플라이언스 중복 비용을 절감할 수 있습니다.

세계 중산 계급에 의한 고급 목제 가구에 대한 지출 확대

아시아태평양의 소득 증가는 원목 가구에 대한 수요를 재활성화했지만 단기 판매는 주거 거래 동향에 따라 변동하고 있습니다. 윌리엄 블레어사의 분석에 따르면 중고주택거래와 가구 매출에는 강한 상관관계가 인정되고 장기적인 기반은 건전함에도 불구하고 판매량이 늘어나고 있는 이유를 설명하고 있습니다. 운임 상승과 디플레이션 경향의 가격 동향이 계속 이익률을 압박하고 있습니다만, 재택 근무 환경의 질 향상이라고 하는 인구 동태의 추풍에 의해 4-6%의 안정 성장대가 유지되고 있습니다. 2024년 초에 미국산 하드우드재의 인도용 수출액은 287만 달러에 이르렀으며, 화이트 오크, 히코리, 레드 오크가 견인했습니다. 이는 인도의 수입 기반이 낮지 만 고급 하드 우드 종에 대한 잠재적 수요가 있음을 보여줍니다.

국제적 불법 벌채 방지 규제(EUDR, 레이시법) 강화에 의한 공급 불안정화

EU 산림 파괴 방지 규칙과 미국 레이시법을 포함한 엄격한 규제는 국경을 넘는 하드우드의 전체 적하에 대해 엔드 투 엔드 추적이 의무화되어 각 거래에 서류 작성 및 검증 부담이 증가하고 있습니다. 이 추가적인 심사는 수입업체 및 수출업체 양쪽에 비용 상승을 가져오고, 합법 벌채의 증명이 곤란한 지역으로부터의 발주를 축소하는 구매자도 이미 나타났습니다. 유럽 위원회의 2025년 4월 지침에서는 연례 실사 보고서가 인정되었지만, 출하 단위의 지리 데이터 제출은 여전히 의무화되고 있으며, 다양한 조달 대상을 다루는 공급업체의 고정비 증가로 이어지고 있습니다.

부문 분석

오크재는 2025년 소비량의 27.74%를 차지했고, 하드우드 시장에서 최대의 점유율을 획득했습니다. 펜실베니아주와 미주리주의 입목가격 보고서에서는 화이트 오크 단판재의 천장가격이 현저하게 고가를 보였으나 혼합제재용 통나무의 평균가격은 천보드피트당 약 260달러로 침착하여 등급간 가격차 확대가 부각되었습니다. 고급 가구나 음향 패널 용도에 견인된 호두재는 5.71%의 연평균 복합 성장률(CAGR)이 하드우드 시장 전체의 성장을 웃돌아 큰 점유율 획득이 전망됩니다. 마호가니는 멸종위기종 국제거래조약(CITES) 지정에 의한 생산능력제약이 계속되고 있는 한편, 체리재는 유행 사이클의 침정화로 평평한 상태입니다. 튤립 우드나 너도밤나무 등의 2차 수종은 인증 프리미엄을 배경으로 틈새 프로젝트 사양으로 채택이 진행되는 것, 오크나 호두 정도의 규모에는 이르지 않습니다. 다양한 수종 포트폴리오를 보유한 통합기업은 지역간의 가격차를 활용하여 수익을 평준화하고 기후 변화에 따른 수종 분포 변화에 대한 헤지 효과를 얻고 있습니다.

소비자는 심미성뿐만 아니라 투명성에 대한 신뢰성에서도 수종을 선택하는 경향이 강해지고, 트레이서블한 밸류체인의 전략적 가치가 높아지고 있습니다. 이 선순환은 산림관리협의회(FSC) 및 산림인증제도추진 프로그램(PEFC) 감사에 투자하는 산림 소유자에게 보상하여 감사 및 관리연쇄(CoC) 비용을 상쇄하는 가격차를 지속하고 있습니다.

지역별 분석

북미는 광대한 산림 자원, 성숙한 인프라, 인증 임업을 촉진하는 규제 환경으로 2025년 매출의 36.55%를 차지했습니다. 2025년 3월 미국 대통령령에 의한 벌채 확대는 산화사 대책의 강화와 수입 의존도의 저감을 목적으로 하고 있습니다만, Canfor사의 사우스캐롤라이나주 공장 폐쇄(3억 5,000만 보드 피트의 생산 능력 삭감) 등 제재소의 폐쇄 사례는 시장 사이클이 정책적 의도보다 더 강력한 영향력을 미칠 수 있음을 보여줍니다. 미국 주요 공급국으로서의 캐나다의 역할은 여전히 매우 중요합니다. 잠재적 상쇄 관세는 국경을 넘어서는 무역 흐름을 재구성하며 중서부 및 북동부의 프로젝트의 경제성에 영향을 미칠 수 있습니다. 멕시코는 USMCA에 의한 무관세 접근을 활용하고 있지만 가공 규모가 부족하기 때문에 미국 국경 부근의 지역 가구 클러스터에 기여하는 것으로 제한됩니다.

아시아태평양 회랑은 연평균 CAGR 5.42%로 확대되어 하드우드 시장의 주요 성장 엔진이 되고 있습니다. 중국은 2024년 998만 입방미터의 하드우드 원목을 평균 277달러/입방미터로 수입해 건설활동 전체가 저조임에도 불구하고 고급수종으로 전환하고 있습니다. 인도의 하드우드 시장은 여전히 잠재적인 성장 여지가 크고 미국산재의 수입 구성비는 불과 5%에 머물고 있습니다. 물류와 관세 마찰이 완화되면 수종 다양화를 위한 큰 성장 여지가 기대됩니다. 동남아시아 수출국, 특히 베트남은 세계 가구 수주를 채우고 있지만, 인도네시아의 합판 부문은 수요감퇴에 직면하고 있으며, 지역 내 실적 격차가 부각되고 있습니다.

유럽에서는 인증기준에 근거한 안정적인 수요가 계속되는 한편, EU목재규제(EUDR)를 통한 공급망의 재구축이 진행되어 견고한 관리기록을 가진 국내 및 북유럽 산업자에게 유리한 상황이 태어나고 있습니다. 독일의 침엽수 수입 급감(2024년-34%)은 구조적인 대체품으로의 전환을 시사하고 있으며, 이 경향은 하드우드 시장에도 파급될 가능성이 있습니다. 중동 및 아프리카에서는 국가 규모의 대형 프로젝트에 의한 수요 증가가 전망되지만, 불안정한 물류와 한정된 건조로 용량이 단기적인 하드우드 전개를 제약하고 있습니다. 한편, 지역 기준이 탄소 긍정적인 건축자재를 추진하는 동안 장기적인 전망은 유망합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 글로벌 친환경 건축 프로젝트 내 인증된 지속 가능한 하드우드재 수요 증가

- 전 세계 중산층의 프리미엄 원목 가구 지출 확대

- 하드우드 베니어를 이용한 엔지니어드우드 제조의 성장

- 세계의 주택 보수에 있어서의 하드우드 바닥재의 채택 증가

- 수확 및 제재에 있어서의 기술 혁신에 의한 수량과 공급 효율의 향상

- 시장 성장 억제요인

- 국제적인 불법 벌채 규제 강화(EUDR, 레이시법)에 의한 공급 변동성

- 세계 시장에 있어서의 저렴한 침엽수재 및 복합재 대체품에 의한 가격 압력

- 무역혼란과 관세 불확실성이 하드우드 수출 흐름에 미치는 영향

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장의 최신 동향과 혁신에 관한 인사이트

- 시장의 최근 동향(신제품 발매, 전략적 이니셔티브, 투자, 제휴, 합작 사업, 사업 확대, M&A 등)에 대한 인사이트

제5장 시장 규모와 성장 예측

- 종속별

- 참나무

- 단풍나무

- 벚나무

- 호두나무

- 마호가니

- 기타

- 용도별

- 바닥재

- 가구

- 건설

- 인테리어 디자인 및 장식

- 산업용 포장 및 팔레트

- 목공 제품

- 기타 용도

- 유통 채널별

- 직접 판매

- 리셀러/도매업체

- 소매(오프라인 및 온라인)

- 기타 유통 채널

- 지역별

- 북미

- 캐나다

- 미국

- 멕시코

- 남미

- 브라질

- 페루

- 칠레

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 북유럽 국가(덴마크, 핀란드, 아이슬란드, 노르웨이, 스웨덴)

- 기타 유럽

- 아시아태평양

- 인도

- 중국

- 일본

- 호주

- 한국

- 동남아시아(싱가포르, 말레이시아, 태국, 인도네시아, 베트남, 필리핀)

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Weyerhaeuser Company

- Georgia-Pacific LLC

- Danzer Group

- Baillie Lumber Co.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Mohawk Industries, Inc.

- Armstrong Flooring, Inc.

- Rougier Afrique International

- Samling Group

- Greenply Industries Ltd.

- Arauco

- Sumitomo Forestry Co., Ltd.

- Dongwha International

- Columbia Forest Products

- Century Plyboards Ltd.

- Norbord Inc.

- Kronospan Limited

- Mannington Mills, Inc.

- Roseburg Forest Products

- Holzindustrie Schweighofer(HS Timber Group)

- Stella-Jones Inc.

제7장 시장 기회와 장래의 전망

SHW 26.01.22The Hardwood Market was valued at USD 1130 billion in 2025 and estimated to grow from USD 1179.04 billion in 2026 to reach USD 1458.63 billion by 2031, at a CAGR of 4.34% during the forecast period (2026-2031).

Growth is underpinned by tightening sustainability regulations-most notably the European Union Deforestation Regulation (EUDR)-and by resilient end-use demand in construction, flooring, and high-end furniture. Market leaders are funding vertically integrated supply chains to de-risk raw-material availability, while tighter global enforcement against illegal logging is raising compliance costs yet reinforcing the premium for certified wood. Asia-Pacific's pace, buoyed by ongoing urbanization and rising middle-class spending, balances the cooler but still sizable consumption base in North America and Europe. On the supply side, efficiency-boosting sawmill automation, wider deployment of digital traceability, and U.S. policy moves to accelerate domestic harvesting all point to an era of disciplined, productivity-led growth.

Global Hardwood Market Trends and Insights

Rising Demand for Certified Sustainable Hardwood in Global Green Building Projects

Roughly 280 million hectares of forests carried either PEFC (Programme for the Endorsement of Forest Certification systems) or Forest Stewardship Council (FSC) certification in 2025, turning third-party validation into an entry requirement rather than a marketing add-on . The EU Deforestation Regulation (EUDR), effective December 2024, forces exporters to present geolocation data for every shipment, pushing suppliers to retrofit digital traceability across fragmented operations. FSC reacted with a dedicated "Regulatory Module" to ease compliance . The certification premium is migrating beyond Europe, as importers in East and South-East Asia increasingly ask for verified provenance to protect their downstream access to Organisation for Economic Co-operation and Development (OECD) markets. Bureau Veritas confirms a marked rise in multi-scheme audits that bundle FSC, PEFC, and legality checks into one field mission, thereby trimming compliance overlap costs.

Expanding Middle-Class Expenditure on Premium Hardwood Furniture Worldwide

Income gains across Asia-Pacific have reset aspirations toward solid-wood furniture, yet short-term sales fluctuate with housing turnover. An assessment by William Blair shows a tight correlation between existing-home transactions and furniture receipts, explaining subdued volumes despite intact long-term fundamentals. Freight rates and deflationary price trends continue to squeeze margins, though demographic tailwinds-such as remote-work configurations that elevate home-office quality-anchor a 4%-6% steady-state growth band. Early-2024 U.S. hardwood exports to India reached USD 2.87 million, led by white oak, hickory, and red oak, underscoring the gap between India's low import base and its latent appetite for premium hardwood species.

Supply Volatility Due to Stricter International Anti-Illegal Logging Regulations (EUDR, Lacey Act)

Stringent rules, including the EU Deforestation Regulation and the U.S. Lacey Act, now demand end-to-end tracking for every load of hardwood that crosses a border, adding layers of paperwork and verification to each transaction. The extra scrutiny raises costs for importers and exporters alike and has already pushed some buyers to scale back orders from regions where proving a legal harvest is difficult. The European Commission's April 2025 guidance allows annual due diligence filings but still demands shipment-level geodata, raising fixed costs for suppliers handling diverse sourcing pools.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Engineered Wood Manufacturing Utilizing Hardwood Veneers

- Increasing Adoption of Hardwood Flooring in Residential Renovations Globally

- Price Pressure from Cheaper Softwood and Composite Substitutes in Global Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oak controlled 27.74% of 2025 consumption, giving it the single-largest slice of the hardwood market. Pennsylvania and Missouri stumpage reports reveal impressive ceiling prices for white oak veneer, yet mixed sawlog averages settled near USD 260 per thousand board feet, spotlighting widening value bands across grades. Walnut, propelled by luxury furniture and acoustic-panel applications, is set to capture an outsized wallet share as its 5.71% CAGR outstrips overall hardwood market growth. Mahogany remains capacity-constrained under CITES (Convention on International Trade in Endangered Species) listing, while cherry treaded water after fashion cycles cooled. Secondary species, including tulipwood and beech, ride certification premiums into niche project specifications but lack the scale of oak or walnut. Diversified species portfolios allow integrated firms to exploit regional price differentials, smoothing earnings and hedging against climate-induced shifts in species distribution.

Consumers increasingly choose species not only for aesthetics but also for transparency credentials, amplifying the strategic value of traceable supply chains. That virtuous loop rewards forest owners investing in Forest Stewardship Council or Programme for the Endorsement of Forest Certification audits, sustaining a price delta that compensates for audit and chain-of-custody costs.

The Hardwood Market is Segmented by Species (Oak, Maple, and More), Application (Flooring, Furniture, and More), Distribution Channel (Direct Sales, Distributors/Wholesalers, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 36.55% of 2025 turnover thanks to expansive forest inventories, mature infrastructure, and a regulatory environment conducive to certified forestry. The March 2025 U.S. executive order to expand harvesting aims to fortify wildfire mitigation and reduce import reliance, although sawmill closures such as Canfor's South Carolina operations-which will remove 350 million board feet of capacity-underscore how market cycles can still override policy intent. Canada's role as a top U.S. supplier remains pivotal; potential countervailing duties could reshape cross-border trade flows and influence project economics across the Midwest and Northeast. Mexico leverages USMCA tariff-free access but lacks processing scale, limiting its upside to regional furniture clusters near the U.S. border.

The Asia-Pacific corridor, growing at 5.42% CAGR, is the hardwood market's chief momentum engine. China imported 9.98 million m3 of hardwood logs in 2024 at an average USD 277 per m3, pivoting toward premium species despite overall tepid construction activity. India's hardwood market remains under-indexed; U.S. lumber constitutes just 5% of its import mix, leaving significant runway for species diversification once logistics and tariff frictions ease. Southeast Asian exporters-Vietnam, particularly-are filling global furniture orders, yet Indonesia's plywood segment wrestles with demand slumps, pointing to heterogeneous performance across the region.

Europe delivers stable, certification-led demand but is rewriting supply chains through the EUDR filter, effectively favoring domestic and Nordic producers with robust chain-of-custody records. Germany's softwood import collapse (-34% in 2024) hints at structural substitution into engineered products, likely to spill over into hardwood patterns. The Middle East and Africa pool gains from sovereign mega-projects; however, volatile logistics and limited kiln-dry capacity restrict near-term hardwood roll-outs, while long-term visibility remains promising as local standards embrace carbon-positive building materials.

- Weyerhaeuser Company

- Georgia-Pacific LLC

- Danzer Group

- Baillie Lumber Co.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Mohawk Industries, Inc.

- Armstrong Flooring, Inc.

- Rougier Afrique International

- Samling Group

- Greenply Industries Ltd.

- Arauco

- Sumitomo Forestry Co., Ltd.

- Dongwha International

- Columbia Forest Products

- Century Plyboards Ltd.

- Norbord Inc.

- Kronospan Limited

- Mannington Mills, Inc.

- Roseburg Forest Products

- Holzindustrie Schweighofer (HS Timber Group)

- Stella-Jones Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Certified Sustainable Hardwood in Global Green Building Projects

- 4.2.2 Expanding Middle-Class Expenditure on Premium Hardwood Furniture Worldwide

- 4.2.3 Growth of Engineered Wood Manufacturing Utilizing Hardwood Veneers

- 4.2.4 Increasing Adoption of Hardwood Flooring in Residential Renovations Globally

- 4.2.5 Technological Advancements in Harvesting & Sawmilling Enhancing Yield and Supply Efficiency

- 4.3 Market Restraints

- 4.3.1 Supply Volatility Due to Stricter International Anti-Illegal Logging Regulations (EUDR, Lacey Act)

- 4.3.2 Price Pressure from Cheaper Softwood and Composite Substitutes in Global Markets

- 4.3.3 Trade Disruptions and Tariff Uncertainties Impacting Hardwood Export Flows

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Species

- 5.1.1 Oak

- 5.1.2 Maple

- 5.1.3 Cherry

- 5.1.4 Walnut

- 5.1.5 Mahogany

- 5.1.6 Others

- 5.2 By Application

- 5.2.1 Flooring

- 5.2.2 Furniture

- 5.2.3 Construction

- 5.2.4 Interior Design & Decoration

- 5.2.5 Industrial Packaging & Pallets

- 5.2.6 Millwork

- 5.2.7 Other Applications

- 5.3 By Distribution Channel

- 5.3.1 Direct Sales

- 5.3.2 Distributors/Wholesalers

- 5.3.3 Retailers (offline and online)

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East And Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Weyerhaeuser Company

- 6.4.2 Georgia-Pacific LLC

- 6.4.3 Danzer Group

- 6.4.4 Baillie Lumber Co.

- 6.4.5 Stora Enso Oyj

- 6.4.6 UPM-Kymmene Oyj

- 6.4.7 Mohawk Industries, Inc.

- 6.4.8 Armstrong Flooring, Inc.

- 6.4.9 Rougier Afrique International

- 6.4.10 Samling Group

- 6.4.11 Greenply Industries Ltd.

- 6.4.12 Arauco

- 6.4.13 Sumitomo Forestry Co., Ltd.

- 6.4.14 Dongwha International

- 6.4.15 Columbia Forest Products

- 6.4.16 Century Plyboards Ltd.

- 6.4.17 Norbord Inc.

- 6.4.18 Kronospan Limited

- 6.4.19 Mannington Mills, Inc.

- 6.4.20 Roseburg Forest Products

- 6.4.21 Holzindustrie Schweighofer (HS Timber Group)

- 6.4.22 Stella-Jones Inc.

7 Market Opportunities & Future Outlook

- 7.1 Demand for Sustainable and Certified Hardwood

- 7.1.1 Custom and Modular Furniture Trends