|

시장보고서

상품코드

1906890

인도의 일반 외과용 기기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2026-2031년)India General Surgical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

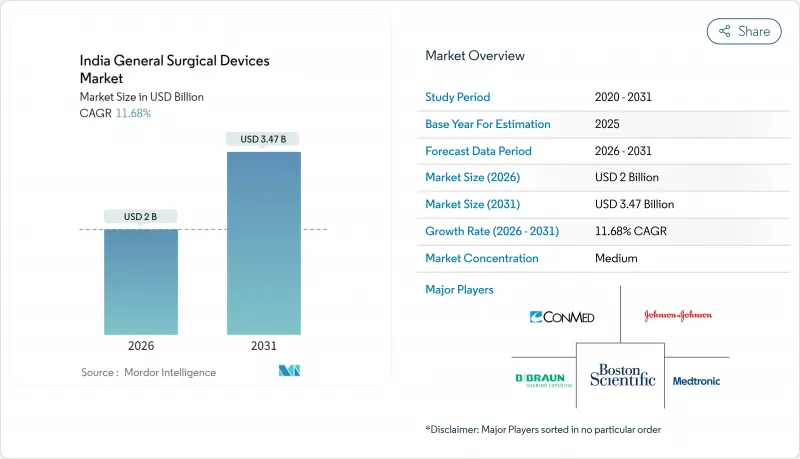

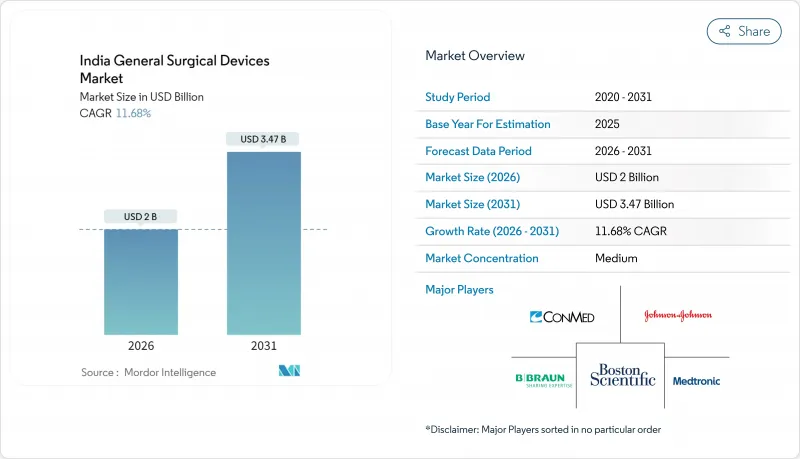

인도의 일반 외과용 기기 시장은 2025년 17억 9,000만 달러로 평가되었고, 2026년에는 20억 달러로 성장할 것으로 전망되며, 2026-2031년 CAGR 11.68%로 성장을 지속하여 2031년까지 34억 7,000만 달러에 달할 것으로 예측되고 있습니다.

이러한 견조한 성장은 의료 근대화 가속화, 지속적인 정부 인센티브, 대도시 지역 및 신흥 지방 도시의 수술 건수 증가를 반영합니다. 만성질환의 유병률을 높이는 인구 동태 변화, 아유슈만 바라트에 의한 국민 모두 보험의 단계적 도입, 그리고 지속적인 국제의료 여행자의 유입이 수요를 더욱 확대하고 있습니다. 인도의 일반 외과용 기기 시장은 프라단 맨토리 스워스야 슬락샤 요자나(PMSSY)에 의한 꾸준한 인프라 정비의 혜택도 받고 있습니다. 또한 비용 효율적인 로봇 플랫폼으로 대표되는 국내 혁신이 경쟁력을 높이고 있습니다. 한편, 첨단 기기에 대한 수입 의존, 상환의 지연, 환율 변동 등의 요인이 시장에 하강 압력을 가하고 있어, 제조업체는 신중하게 대응할 필요가 있습니다.

인도의 일반 외과용 기기 시장 동향 및 인사이트

저침습 수술 및 로봇 지원 수술 도입 확대

주요 도시의 병원에서는 현재 로봇 수술 및 복강경 수술이 일상적으로 도입되고 있으며, 국산 시스템은 기존의 비용 장벽을 축소하고 있습니다. 메릴사의 MISSO 로봇 무릎 관절 플랫폼(2024년 6월 승인)은 98%의 성공률을 보고하면서도 비용면에서 우위성을 나타내고 있습니다. 2024년 9월 데뷔한 AI 탑재 미조엔드 4000은 다전문 진료 대응 기능과 5G 원격 수술 기능을 추가하여 거리 제약을 축소했습니다. 델리의 AIIMS(인도의학연구소) 등의 학술기관에서는 복수의 다빈치 시스템을 도입하고 있으며, 야쇼다 그룹은 메드트로닉의 휴고 시스템을 25병원에 전개하는 등 폭넓은 기관에 의한 지지가 나타나고 있습니다. 그러나 동북 인도의 감사는 복강경 수술이 가능한 사례의 불과 28%에만 이 기술이 적용되고 있는 것으로 판명되어 미개척의 잠재적 가능성이 부각되었습니다. 이 때문에 연수 자금의 확충이나 벤더 지원형 파이낸스에 의해 특히 수요가 가장 급속히 높아지고 있는 지방 도시에서의 보급이 가속될 것으로 예측됩니다.

증가하는 만성 비감염성 질환의 부담

당뇨병은 7,700만 명 이상의 인도인 성인에 영향을 미치고, 심혈관 질환은 전 사망의 28.1%를 차지하고 있어 양동향이 복잡한 외과적 개입 수요를 촉진하고 있습니다. 연간 암 신규 증례 수는 2025년까지 139만 건에 달할 것으로 예측되어 종양학 서비스의 용량에 압력을 가해 정밀 기기 수요를 견인하고 있습니다. 내시경 기술의 보급과 간 이식 프로그램의 개시에 의해 소화기 및 간담췌 수술 건수도 확대하고 있습니다. 병행하여 진행되는 인구고령화(2050년까지 60세 이상이 국민의 19.5%를 차지할 전망)는 정형외과, 심장흉부외과, 신경외과의 수술 건수를 증가시키고, 한편 젊은층은 선택적 수술이나 의료 관광에 근거한 처치를 지지하고 있습니다. PMSSY 자금으로 2014년 이후 157개의 신설의과대학이 탄생하여 종합외과기기 세트를 필요로 하는 의료기관의 기반이 확대되고 있습니다. 가처분 소득 증가 및 보험 적용 범위 확대로 많은 환자들이 고급 임플란트와 에너지 플랫폼을 선택할 수 있게 되어 국내외 제품 투입이 촉진되고 있습니다.

첨단 의료 기기에 대한 지연 및 불균일한 상환

CGHS 등의 제도 하에서 6-12개월간의 지급 지연에 직면하는 병원은 고급 시스템의 구입을 선도하는 경향이 있어 시장 보급을 제약하고 있습니다. 민간 보험 회사는 엄격한 사전 승인 제도에 의해 수술 지연과 기기 사용 억제라는 마찰을 낳고 있습니다. 아유슈만 바라트 제도는 로봇 수술과 에너지 플랫폼의 비용을 충분히 반영하지 않는 보수적인 패키지 요금을 설정하고 있으며, 병원은 보조금의 지출이나 액세스 제한을 강요받고 있습니다. 주별 상환 규칙의 불균일성은 패치워크 형태 수요를 발생시키고 있습니다. 진보적인 카르나타카 주에서는 첨단 수술이 정기적으로 자금을 지원하는 반면, 다른 지역에서는 여전히 배제되고 있습니다. 통일된 의료 기술 평가 프로세스가 부족한 CDSCO(중앙 의약품 규제국)와 NPPA(국가 의약품 가격 관리국)는 가격 상한에 따라 다르지만, 혁신의 진정한 가치를 포착하지는 못합니다. 따라서 공급업체는 지속적인 지불 불확실성을 상쇄하기 위해 비용 효율적인 설계, 자금 조달 솔루션 및 임상 결과 자료를 결합해야 합니다.

부문 분석

복강경 수술 기기는 2025년 시점에서 인도 일반 외과용 기기 시장의 34.02%를 차지했고, 부인과, 소화기과 및 일반 외과의가 저침습 수술로 이행하는 가운데 수요를 지지하고 있습니다. 전기 수술 기구는 가장 급성장하고 있으며 2031년까지 연평균 복합 성장률(CAGR)12.25%를 기록해 다른 카테고리를 능가할 전망입니다. 이 동향은 수술 시간의 단축과 지혈 효과의 향상에 기인합니다. 공공병원이 PMSSY 자금으로 수술실 갱신을 진행하는 가운데, 이들 2부문에 있어서의 인도 일반 외과용 기기 시장 규모는 급속히 확대될 전망입니다. 일회용 트로카, 정밀 봉합사, 고급 상처 폐쇄 키트는 감염 관리 규정에 의한 일회용 제품 수요 증가를 배경으로 안정적인 판매 수량을 견인합니다. 메릴 사의 '뉴 엣지 봉합사'나 고성능 심장 밸브 등 국내 제품의 출시는 성능을 손상시키지 않고 수입품을 대체할 수 있는 현지 기술력을 나타내고 있습니다.

모든 개복 수술 및 저침습 수술에서 필수적인 기본 수술 기구에 대한 수요는 견조하게 지속되는 반면, 신흥 로봇용 액세서리는 고수익 라인을 창출하고 있습니다. CDSCO(중앙의약품규제관리청)에 의한 품질 분류의 갱신은 컴플라이언스 비용을 증가시키면서 특히 에너지 기반 플랫폼에서 구매자의 신뢰를 높이고 있습니다. 인도 일반 외과용 기기 시장에서 경쟁하는 공급업체는 고객 충성도를 확보하기 위해 서비스 계약 및 외과의사 훈련을 번들하는 경우가 증가하고 있습니다. 의료기기 제조업체가 이미지 통합 기능, 내비게이션 보조 장치, AI 분석 기능을 추가함으로써 병원별 총 거래 가치가 확대되고, 카테고리 횡단적인 시너지 효과가 현저합니다. 특히 지방도시에서는 신설 컬리지 병원과 사립 병원이 개별 구매가 아닌 통합 솔루션을 요구하는 경향이 강해져 플랫폼 지향 조달로의 전환을 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 저침습 수술 및 로봇 지원 수술 도입 확대

- 도로 교통사고 발생률 증가

- 만성 비감염성 질환 증가에 수반하는 부담 증대

- 민간 3차 의료시설 및 당일치기 외과 센터 확대

- 정부에 의한 아유슈만 바라트 보험 추진

- 인바운드 의료 투어리즘의 급증

- 시장 성장 억제요인

- 첨단 의료 기기에 대한 지연 및 부정합의 상환

- NPPA 가격 상한 설정에 따른 이익률 저하

- 제2 및 제3급 도시에서 숙련 복강경 외과의의 부족

- 수입 의존도의 높이 및 환율 연동형 공급 리스크

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 핸드헬드 기기

- 복강경 수술용 기기

- 전기수술 기기

- 상처 봉합 기기

- 트로카 및 액세스 장치

- 기타 제품

- 용도별

- 부인과 및 비뇨기과

- 심장병학

- 정형외과

- 신경학

- 소화기 및 간담췌 영역

- 기타 용도

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Applied Medical Resources Corp.

- B. Braun SE

- Boston Scientific Corporation

- CDR Medical Industries Ltd

- Commed Corporation

- ERBE Elektromedizin GmbH

- Getinge Medical India Pvt. Ltd

- Hindustan Syringes & Medical Devices Ltd

- Intuitive Surgical Inc.

- Johnson & Johnson(Ethicon)

- Medtronic plc

- Meril Life Sciences Pvt. Ltd

- Olympus Corporation

- Poly Medicare Ltd

- Smith & Nephew

- Stryker Corporation

- Surgical Holdings India

- Teleflex Incorporated

제7장 시장 기회 및 장래 전망

AJY 26.01.26The India general surgical devices market is expected to grow from USD 1.79 billion in 2025 to USD 2 billion in 2026 and is forecast to reach USD 3.47 billion by 2031 at 11.68% CAGR over 2026-2031.

This solid growth mirrors accelerating healthcare modernization, sustained government incentives, and rising procedure volumes across metropolitan and emerging secondary cities. Demand is amplified by demographic shifts that elevate chronic disease prevalence, the progressive roll-out of universal insurance through Ayushman Bharat, and persistent inflows of international medical travelers. The India general surgical devices market also benefits from steady infrastructure build-out under the Pradhan Mantri Swasthya Suraksha Yojana, while domestic innovation-epitomized by cost-efficient robotic platforms-adds competitive momentum. Simultaneously, import dependence for sophisticated equipment, delayed reimbursements, and foreign-exchange volatility place downward pressure that manufacturers must carefully navigate.

India General Surgical Devices Market Trends and Insights

Rising Adoption of Minimally Invasive and Robotic-Assisted Surgeries

Hospitals in major metros now routinely deploy robotic or laparoscopic techniques, and indigenous systems are narrowing past cost barriers. Meril's MISSO robotic knee platform, cleared in June 2024, reports 98% success while cost. The September 2024 debut of the AI-enabled Mizzo Endo 4000 added multi-specialty capability and 5G telesurgery functions that shrink distance constraints. Academic centers such as AIIMS Delhi have installed several da Vinci units, and the Yashoda Group is placing Medtronic's Hugo system across 25 hospitals, illustrating broad institutional endorsement. Still, a Northeast India audit found only 28% of surgeries that could be laparoscopic actually use the technique, underscoring untapped potential. Expanded training funds and vendor-backed financing are therefore expected to accelerate penetration, especially in secondary cities where demand is rising fastest.

Growing Burden of Chronic Non-Communicable Diseases

Diabetes affects more than 77 million Indian adults, and cardiovascular disorders contribute 28.1% of all deaths, both trends propelling demand for complex surgical interventions. Annual cancer incidence is projected to hit 1.39 million new cases by 2025, pressuring oncology service capacity and driving precision-instrument needs. Gastro-intestinal and hepato-biliary surgery volumes expand in tandem, boosted by endoscopic technology diffusion and nascent liver-transplant programs. Parallel demographic aging-19.5% of citizens will be over 60 by 2050-elevates orthopedic, cardiothoracic, and neurology volumes, while younger cohorts sustain elective and tourism-based procedures. PMSSY funding has created 157 new medical colleges since 2014, widening institutional footprints that require full suites of general surgical devices. Rising disposable income and broader insurance cover enable many patients to choose premium implants and energy platforms, stimulating domestic and multinational product launches.

Delayed and Inconsistent Reimbursement for Advanced Devices

Hospitals waiting six to twelve months for payment under programs such as CGHS often defer purchases of premium systems, constraining market diffusion. Private insurers add to friction through stringent pre-authorizations that delay cases and dampen device usage. Ayushman Bharat sets conservative package rates that may not fully reflect robotic or energy platform costs, compelling hospitals to either subsidize or ration access. Uneven reimbursement rules across states create patchwork demand, with progressive Karnataka routinely funding advanced procedures, while other regions still exclude them. Lacking a unified health technology assessment process, CDSCO and NPPA rely on price ceilings that rarely capture the true value of innovation. Vendors must therefore combine cost-efficient design, financing solutions, and clinical-outcomes dossiers to offset persistent payment uncertainty.

Other drivers and restraints analyzed in the detailed report include:

- Government Ayushman Bharat Insurance Boost

- Surge in Inbound Medical Tourism

- High Import Dependence and Forex-Linked Supply Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Laparoscopic devices captured 34.02% of India general surgical devices market share in 2025, anchoring demand as surgeons across gynecology, gastroenterology, and general surgery migrate toward minimally invasive practice. Electrosurgical tools are the fastest climber, recording a 12.25% CAGR that outpaces every other category through 2031, a trend tied to shorter operating times and enhanced hemostasis. India general surgical devices market size for these two segments is set to widen rapidly as public hospitals upgrade theaters under PMSSY funding. Disposable trocars, precision sutures, and advanced wound-closure kits add dependable volume, buoyed by infection-control mandates that favor single-use products. Domestic launches such as Meril's New Edge Suture and high-performance heart valves illustrate how local engineering can substitute imports without sacrificing performance.

Steady demand for handheld basic instruments persists, given their indispensability in every open or minimally invasive procedure, while emerging robotic accessories introduce premium revenue lines. CDSCO's updated quality classifications heighten compliance costs yet raise buyer confidence, particularly for energy-based platforms. Vendors competing in the India general surgical devices market increasingly bundle service contracts and surgeon training to lock in loyalty. Cross-category synergies are apparent as device makers add imaging integration, navigation aids, or AI analytics, thereby expanding total account value per hospital. Momentum is strongest in tier-2 cities where newly built colleges and private hospitals seek integrated solutions rather than piecemeal purchases, indicating a shift toward platform-oriented procurement.

The India General Surgical Devices Market Report is Segmented by Product (Handheld Devices, Laparoscopic Devices, Electrosurgical Devices, Wound-Closure Devices, Trocars & Access Devices, and Other Products), Application (Gynecology & Urology, Cardiology, Orthopedic, Neurology, Gastro-Intestinal & Hepato-Biliary, and Other Applications). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Applied Medical Resources

- B. Braun

- Boston Scientific

- CDR Medical Industries Ltd

- Conmed

- Erbe Elektromedizin

- Getinge

- Hindustan Syringes & Medical Devices

- Intuitive Surgical

- Johnson & Johnson

- Medtronic

- Meril Life Science

- Olympus

- Poly Medicare Ltd

- Smiths Group

- Stryker

- Surgical Holdings India

- Teleflex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Minimally-Invasive & Robotic-Assisted Surgeries

- 4.2.2 Increasing Incidence of Road-Traffic Injuries

- 4.2.3 Growing Burden of Chronic Non-Communicable Diseases

- 4.2.4 Expansion of Private Tertiary/Day-Care Surgical Centres

- 4.2.5 Government Ayushman Bharat Insurance Boost

- 4.2.6 Surge in Inbound Medical Tourism

- 4.3 Market Restraints

- 4.3.1 Delayed & Inconsistent Reimbursement for Advanced Devices

- 4.3.2 NPPA Price-Capping Eroding Margins

- 4.3.3 Shortage of Trained Laparoscopic Surgeons in Tier-2/3 Cities

- 4.3.4 High Import Dependence & Forex-Linked Supply Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Handheld Devices

- 5.1.2 Laparoscopic Devices

- 5.1.3 Electrosurgical Devices

- 5.1.4 Wound-Closure Devices

- 5.1.5 Trocars & Access Devices

- 5.1.6 Other Products

- 5.2 By Application

- 5.2.1 Gynecology & Urology

- 5.2.2 Cardiology

- 5.2.3 Orthopedic

- 5.2.4 Neurology

- 5.2.5 Gastro-intestinal & Hepato-biliary

- 5.2.6 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Applied Medical Resources Corp.

- 6.3.2 B. Braun SE

- 6.3.3 Boston Scientific Corporation

- 6.3.4 CDR Medical Industries Ltd

- 6.3.5 Conmed Corporation

- 6.3.6 ERBE Elektromedizin GmbH

- 6.3.7 Getinge Medical India Pvt. Ltd

- 6.3.8 Hindustan Syringes & Medical Devices Ltd

- 6.3.9 Intuitive Surgical Inc.

- 6.3.10 Johnson & Johnson (Ethicon)

- 6.3.11 Medtronic plc

- 6.3.12 Meril Life Sciences Pvt. Ltd

- 6.3.13 Olympus Corporation

- 6.3.14 Poly Medicare Ltd

- 6.3.15 Smith & Nephew

- 6.3.16 Stryker Corporation

- 6.3.17 Surgical Holdings India

- 6.3.18 Teleflex Incorporated

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment