|

시장보고서

상품코드

1906913

라틴아메리카의 페인트 및 코팅 : 시장 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Latin America Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

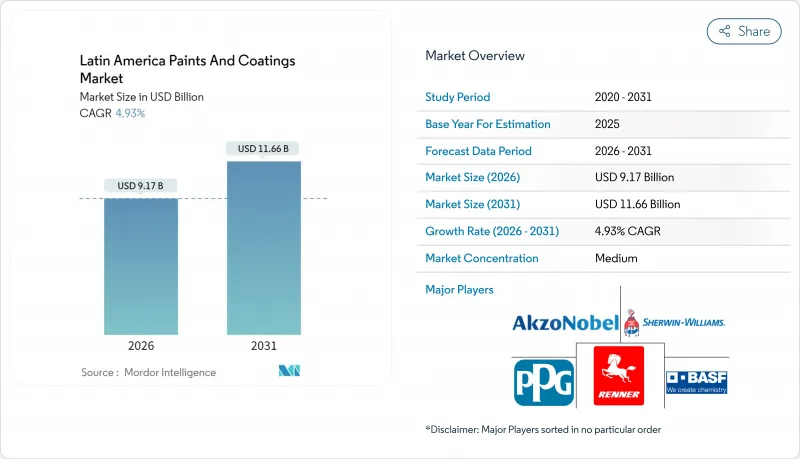

라틴아메리카의 페인트 및 코팅 시장 규모는 2026년 91억 7,000만 달러로 평가되었습니다.

이는 2025년 87억 4,000만 달러에서 성장한 수치이며, 2031년에는 116억 6,000만 달러에 이를 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 4.93%로 성장이 전망됩니다.

확장은 부활하는 건설 활동, 가속화되는 자동차 생산, 다국적 인프라 재건과 맞물립니다. 브라질은 다각화된 산업 기반을 통해 수요를 견인하는 반면, 멕시코는 근거리 아웃소싱 투자와 수출 지향적 제조 회랑 구축으로 추진력을 얻고 있습니다. 저휘발성 유기화합물(VOC) 및 자외선 경화 기술로의 포트폴리오 업그레이드는 석유화학 가격 변동 속 공급업체의 마진 방어에 기여합니다. 다국적 기업들이 현지 제조 및 유통 기반을 확대함에 따라 경쟁 강도가 높아지는 반면, 지역 전문 기업들은 비용 유연성과 긴밀한 고객 관계를 활용해 시장 점유율을 유지하고 있습니다.

라틴아메리카의 페인트 및 코팅 시장 동향 및 인사이트

주택 및 상업건설활동 회복

건설 지출이 팬데믹 이전 수준으로 회복되어 라틴아메리카의 페인트 및 코팅 시장 전체의 건축용 페인트 판매량이 증가하고 있습니다. 브라질 북동부의 신규 주택 프로젝트와 멕시코 시티에서 지연되었던 상업용 타워 재개공으로 고객 기반이 확대됩니다. 개발사들은 강화된 건축 규정을 충족하기 위해 저VOC 실내 페인트를 지정함에 따라 제조사들은 수성 페인트 혁신을 가속화하고 있습니다. 소비자 신뢰 회복으로 소매 재도장 주기가 단축되면서 얼룩 방지 기능을 갖춘 프리미엄 실내 마감재 수요가 증가합니다. 생산업체들은 급성장하는 2차 도시에 가까운 곳에 착색 시설을 배치하여 공급망을 최적화하고 있습니다.

자동차 산업의 수요 증가

멕시코의 자동차 조립은 세계의 OEM 제조업체가 USMCA의 관세 우대를 활용하기 위해 플랫폼을 이전함으로써 과거 최고 수준에 가까워지고 있습니다. 이 급증으로 OEM용 기반 코트 수요와 충돌 수리용 재도장 수요가 확대되어 라틴아메리카의 페인트 시장을 주도하고 있습니다. 전기자동차 배터리 하우징에는 열 관리 코팅이 필수가 되어 새로운 고이익률 틈새 시장이 창출되고 있습니다. 브라질의 자동차 산업 클러스터는 도요타의 22억 2,000만 달러 규모의 라인 근대화와 스텔란티스의 27억 4,000만 달러 규모의 생산 능력 증강 등 과거 최고의 대내 자본을 유치하고 있습니다. 페인트 공급업체는 조립 공장에 인접한 컬러 매칭 랩을 제공하여 다년간 공급 계약을 체결했습니다.

석유화학 원료 비용의 변동성

나프타 연계 원자재 가격 변동은 수지 및 용제 구매업체들의 총마진을 압박하고 있습니다. 아르헨티나와 칠레의 통화 가치 하락으로 수입 모노머 비용이 가중되면서, 제형 개발사들은 선물 계약 및 현물 화물 스왑을 통한 헤지 전략을 추진 중입니다. 일부 지역 업체들은 원료 비용 안정화를 위해 수지 합성 분야로의 역통합을 모색하고 있습니다. 다른 업체들은 변동성 완화를 위해 재생 용제를 혼합하지만, 일관성 문제로 인한 배치 불량 발생 위험에 직면합니다. 마진 압박은 소규모 생산자들이 대규모 재무 구조를 추구하며 업계 통합을 촉진합니다.

부문 분석

아크릴 시스템은 2025년 매출의 43.78%를 차지하며, 실내·외장 및 보호 코팅 분야의 광범위한 적용을 통해 라틴아메리카 페인트 및 코팅 시장을 주도했습니다. 제형의 다용성 덕분에 광택, 내마모성, 착색 정확도를 신속하게 조정할 수 있어 환경 규제가 강화되는 상황에서도 해당 등급의 입지를 공고히 유지하고 있습니다. 폴리우레탄 화학 물질은 기반 규모는 작지만 OEM 클리어 코트 성능과 산업 자산 내구성 요구가 증가함에 따라 가장 가파른 5.91% CAGR을 기록하고 있습니다. 하이브리드 아크릴-폴리우레탄 블렌드는 경도와 유연성을 결합하여 프리미엄 부문를 지원합니다.

공급업체들은 폴리우레탄 라인을 지속가능성 목표에 부합시키기 위해 바이오 기반 폴리올을 모색하고 있으나 가격 경쟁력은 여전히 달성하기 어렵습니다. 에폭시는 내화학성이 색상 유지 문제보다 우선시되는 바닥 및 해양 시스템에서 우위를 유지합니다. 알키드는 가격에 민감한 소비자 부문에 국한되어 서서히 축소되고 있으나 기존 스프레이 장비와의 호환성으로 보호받고 있습니다. 폴리에스터 수지는 가전제품 및 금속 가구용 분체 페인트에 활용되며, 비닐 및 VAE 에멀젼은 저취성을 중시하는 특수 장식 틈새 시장을 채운다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 주거 및 상업용 건설 활동의 회복

- 자동차 산업의 수요 증가

- 인프라 근대화 프로젝트 증가

- 산업 확장에 따른 수요 창출

- 열대 도시의 쿨루프 코팅 의무화

- 시장 성장 억제요인

- 석유화학 원료 가격 변동성

- 강화된 VOC 및 HAP 배출 규범

- 물류 병목과 컨테이너 부족

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 수지 유형별

- 아크릴 수지

- 에폭시 수지

- 알키드 수지

- 폴리에스터

- 폴리우레탄

- 기타 수지 유형(비닐 수지 및 VAE 등)

- 기술별

- 수성

- 용제계

- 분체 도장

- UV 경화형

- 최종 사용자 업계별

- 건축

- 산업

- 자동차

- 목재

- 포장

- 운송

- 지역별

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 칠레

- 페루

- 기타 라틴아메리카

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Akzo Nobel NV

- Allnex Gmbh

- Axalta Coating Systems LLC

- BASF SE

- Benjamin Moore & Co.

- Iquine

- Jotun

- Lanco Paints

- Pintuco SA

- PPG Industries Inc.

- Renner Herrmann SA

- The Sherwin-Williams Company

- WEG

제7장 시장 기회와 장래의 전망

HBR 26.02.04Latin America Paints And Coatings Market size in 2026 is estimated at USD 9.17 billion, growing from 2025 value of USD 8.74 billion with 2031 projections showing USD 11.66 billion, growing at 4.93% CAGR over 2026-2031.

The expansion aligns with resurgent construction activity, accelerating automotive output, and multi-country infrastructure renewal. Brazil anchors demand through its diversified industrial base, while Mexico gains momentum from near-shoring investments and the build-out of export-oriented manufacturing corridors. Portfolio upgrades toward low-VOC and UV-cured technologies help suppliers defend margins in the face of petrochemical price swings. Competitive intensity rises as multinationals deepen local manufacturing and distribution footprints, whereas regional specialists leverage cost agility and intimate customer ties to hold share.

Latin America Paints And Coatings Market Trends and Insights

Resurgent Residential and Commercial Construction Activity

Construction spending recovers to pre-pandemic levels, lifting architectural sales volumes across the Latin America paints and coatings market. New housing projects in Brazil's Northeast and the restart of delayed commercial towers in Mexico City widen the customer base. Developers specify low-VOC interior paints to meet stricter building codes, prompting formulators to accelerate water-borne innovation. Retail repaint cycles shorten as consumer confidence rebounds, boosting demand for premium interior finishes with stain-blocking features. Producers optimize supply chains by staging tinting facilities closer to fast-growing secondary cities.

Growing Demand from Automotive Industry

Vehicle assembly in Mexico approaches historical peaks as global OEMs relocate platforms to capitalize on USMCA tariff advantages. The surge lifts OEM basecoat volumes and refinish demand for collision repair, enlarging the Latin America paints and coatings market. Electric-vehicle battery housings require thermal-management coatings, creating new high-margin niches. Brazil's automotive cluster attracts record inbound capital, including Toyota's USD 2.22 billion line modernization and Stellantis' USD 2.74 billion capacity upgrade. Coating suppliers lock in multi-year supply contracts by offering color-matching labs adjacent to assembly plants.

Petrochemical Feedstock Cost Volatility

Naphtha-linked raw-material swings compress gross margins for resin and solvent purchasers. Currency depreciation in Argentina and Chile exacerbates imported monomer bills, pushing formulators to hedge through forward contracts and spot cargo swaps. Some regional players pursue backward integration into resin synthesis to stabilize input cost. Others blend recycled solvents to temper volatility but face consistency challenges that can trigger batch rejects. Margin pressure feeds consolidation as smaller producers seek larger balance sheets.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Infrastructure Modernization Projects

- Industrial Expansion Creating Demand

- Stricter VOC and HAP Emission Norms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic systems generated 43.78% of revenue in 2025, anchoring the Latin America paints and coatings market through broad specification in interior, exterior, and protective segments. The formulation versatility allows quick tweaking of sheen, scrub resistance, and tint accuracy, keeping the class entrenched despite rising environmental scrutiny. Polyurethane chemistries, though smaller in base, chart the steepest 5.91% CAGR as OEM clear-coat performance and industrial asset durability needs intensify. Hybrid acrylic-polyurethane blends blend hardness with flexibility, supporting the premium segment.

Suppliers seek bio-based polyols to align polyurethane lines with sustainability targets, but price parity remains elusive. Epoxies retain stronghold in floor and marine systems where chemical resistance overrides color retention concerns. Alkyds shrink slowly, confined to price-sensitive consumer segments yet shielded by compatibility with existing spray equipment. Polyester resins serve powder coatings for appliances and metal furniture, while vinyl and VAE emulsions fill specialized decor niches that prize low odor.

The Latin America Paints and Coatings Market Report is Segmented by Resin Type (Acrylics, Epoxy, Alkyd, Polyester, Polyurethane, and More), Technology (Water-Borne, Solvent-Borne, Powder Coating, UV Cured), End-User Industry (Architectural, Industrial, Automotive, Wood, and More), and Geography (Brazil, Mexico, Argentina, Colombia, Chile, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Akzo Nobel N.V.

- Allnex Gmbh

- Axalta Coating Systems LLC

- BASF SE

- Benjamin Moore & Co.

- Iquine

- Jotun

- Lanco Paints

- Pintuco S.A.

- PPG Industries Inc.

- Renner Herrmann S.A.

- The Sherwin-Williams Company

- WEG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Resurgent residential and commercial construction activity

- 4.2.2 Growing demand from automotive industry

- 4.2.3 Increasing infrastructure modernisation projects

- 4.2.4 Industrial expansion creating demand

- 4.2.5 Cool-roof coating mandates in tropical cities

- 4.3 Market Restraints

- 4.3.1 Petrochemical feedstock cost volatility

- 4.3.2 Stricter VOC and HAP emission norms

- 4.3.3 Logistics bottlenecks and container shortages

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylics

- 5.1.2 Epoxy

- 5.1.3 Alkyd

- 5.1.4 Polyester

- 5.1.5 Polyurethane

- 5.1.6 Other Resin Types (Vinyl and VAE, etc.)

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder Coating

- 5.2.4 UV Cured

- 5.3 By End-user Industry

- 5.3.1 Architectural

- 5.3.2 Industrial

- 5.3.3 Automotive

- 5.3.4 Wood

- 5.3.5 Packaging

- 5.3.6 Transportation

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Mexico

- 5.4.3 Argentina

- 5.4.4 Colombia

- 5.4.5 Chile

- 5.4.6 Peru

- 5.4.7 Rest of Latin America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Allnex Gmbh

- 6.4.3 Axalta Coating Systems LLC

- 6.4.4 BASF SE

- 6.4.5 Benjamin Moore & Co.

- 6.4.6 Iquine

- 6.4.7 Jotun

- 6.4.8 Lanco Paints

- 6.4.9 Pintuco S.A.

- 6.4.10 PPG Industries Inc.

- 6.4.11 Renner Herrmann S.A.

- 6.4.12 The Sherwin-Williams Company

- 6.4.13 WEG

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment