|

시장보고서

상품코드

1906926

게이미피케이션 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Gamification - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

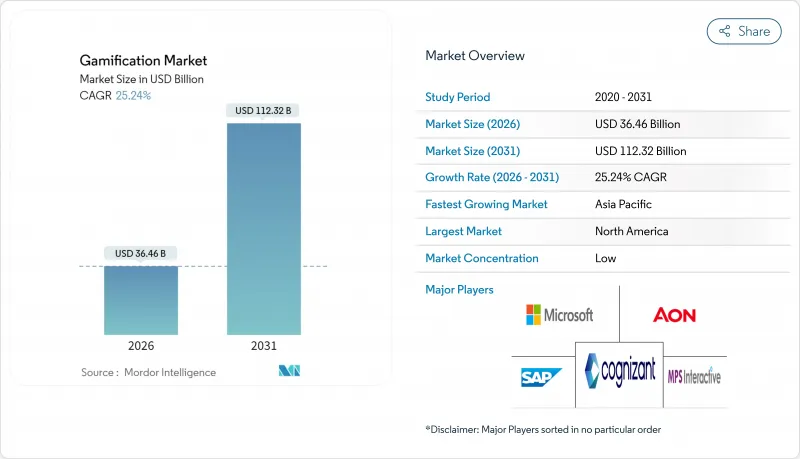

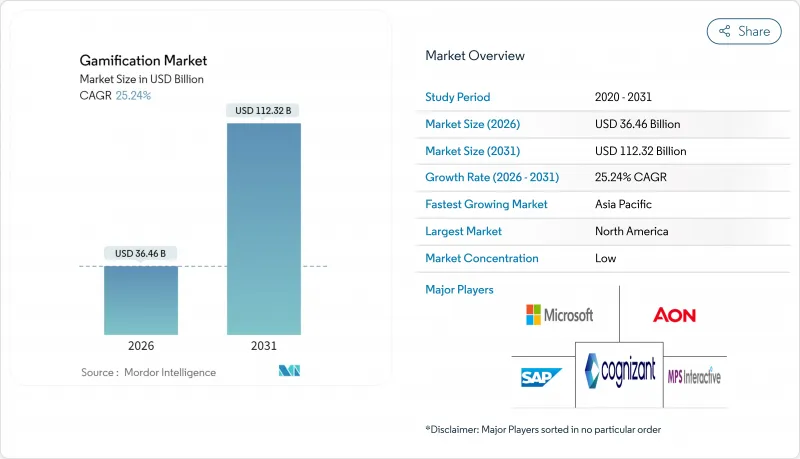

게이미피케이션 시장은 2025년에 291억 1,000만 달러로 평가되었고, 2026년 364억 6,000만 달러에서 2031년까지 1,123억 2,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년) CAGR 25.24%로 성장이 예상됩니다.

클라우드 기반의 도입은 이미 지출의 대부분을 차지하고 있으며, 분산된 팀 전체에 실시간 분석을 제공함으로써 현재의 확대를 많이 지원하고 있습니다. 대기업은 여전히 수익의 대부분을 차지하고 있지만, 로우코드 플랫폼의 도입 비용이 낮아짐에 따라 중소기업(SME)의 성장이 가속화되고 있습니다. 소매 업계의 로열티 프로그램이 가장 큰 애플리케이션 분야인 반면, 직원을 위한 프로그램, 특히 마이크로 학습 시책이 가장 급속히 보급되고 있습니다. 지역별로는 북미가 주도적 입장을 유지하고 있습니다만, 아시아태평양의 모바일 퍼스트 비즈니스 문화가 신흥 디지털 경제권으로 중심을 옮기고 있습니다. 규제 대상 업계에서 미개척 분야의 기회를 기존 소프트웨어 벤더와 전문 스타트업 기업이 경쟁하고 있기 때문에 경쟁은 여전히 치열한 상황입니다.

세계의 게이미피케이션 시장 동향 및 인사이트

클라우드 퍼스트의 디지털 워크플레이스 도입 급증

클라우드 마이그레이션을 가속화하는 기업은 하이브리드 팀 전체에서 기본적으로 작동하는 참여 도구가 필요합니다. Microsoft Power Apps는 게임 메커니즘을 워크플로에 직접 통합하여 전개 기간을 몇 달에서 몇 주로 단축합니다. 클라우드 호스팅 플랫폼은 데이터 스트림을 통합하고 실시간 리더보드를 모든 디바이스에 전달하므로 27.58%의 연평균 복합 성장률(CAGR)이 예측됩니다. 게이미피케이션을 기존 클라우드 인프라와 통합한 조직은 원격 근무 환경에서 최대 90%의 생산성 향상을 보고했습니다. 구독 라이선싱의 비용 우위는 도입을 더욱 가속화하고 있습니다. IT 부서가 온프레미스 자산을 간소화하는 동안 클라우드 네이티브 벤더는 구조적 이점을 얻고 있으며, 이러한 추세는 예측 기간 동안 역전될 가능성이 낮을 것으로 예측됩니다.

로우코드 게이미 피케이션 플랫폼 보급

드래그 앤 드롭 개발은 참여 체험의 디자인을 민주화합니다. SAP Build는 시민 개발자가 코드를 작성하지 않고 핵심 업무 프로세스에 과제, 배지 및 보상을 통합하여 맞춤 프로젝트와 비교하여 개발 비용을 70% 절감합니다. 이 접근성 향상으로 기술 자원 부족의 중견 중소기업까지 대상 시장이 확대되고 있습니다. 플랫폼 공급업체는 영업 콘테스트와 온보딩 임무에 특화된 템플릿의 급증을 보고하고 있으며, 비즈니스의 주류화가 진행되고 있음을 보여줍니다. 로우코드 스택은 SaaS 에코시스템에 직접 연결할 수 있으므로 중소기업에게 중요한 조달 장벽인 가치 실증 사이클도 단축됩니다. 맞춤형 개발의 구조적 감소는 중소기업 부문의 28.67%라는 CAGR과 일치합니다.

설계 불량 프로그램은 부정적인 ROI를 초래합니다.

표면적인 도입 및 공식적인 배지 부여는 직원의 이탈 및 예산 낭비를 초래할 위험이 있습니다. Versus Systems사에서는 2023년 도입 사례가 16건에서 5건으로 감소했습니다. 이것은 유저 관심을 유지할 수 없었던 불충분한 도입 사례가 겉보기만의 도입에 대한 반발을 상징하는 사례입니다. 기업은 새로운 프로젝트를 승인하기 전에 매출 향상 및 오류율 감소와 같은 비즈니스 성과 지표를 찾습니다. 이 엄격한 검토는 판매 주기를 장기화하고 공급업체는 보다 강력한 컨설팅 지원을 제공해야 합니다. 조기 도입 부문의 도입 실수는 후발 기업에 경계심을 안겨 단기적인 지출을 억제합니다. 교육 설계 및 행동 과학을 경시하는 벤더는 게이미피케이션 시장 전체에 파급될 가능성이 있는 평판 리스크를 안깁니다.

부문 분석

2025년 수익에서 클라우드 솔루션은 67.62%를 차지하였고, 2031년까지 연평균 복합 성장률(CAGR) 26.91%를 배경으로 게이미피케이션 시장 규모의 점유율은 더욱 확대될 것으로 전망됩니다. 실시간 텔레메트리, 원활한 업데이트 및 탄력적인 스토리지가 선호를 지원하고 성숙한 보안 인증은 보수적인 산업조차도 영향을 받고 있습니다. 데이터 주권이 최우선으로 되는 분야에서는 온프레미스형 패키지가 여전히 중요하지만, IT 예산의 축소 및 사이버 보험의 보험료 상승으로 인해 비용 편익의 균형이 매니지드 호스팅에 기울어지고 있습니다.

지속적 전개(CD) 파이프라인을 통한 신속한 반복 사이클을 통해 클라우드 공급업체는 클라이언트 측 패치 적용 없이 달성 알고리즘을 미세 조정하고 A/B 테스트를 수행할 수 있습니다. 고급 분석이 실시간으로 개인화된 과제를 제안하는 경우 기업은 37%의 생산성 향상을 보고합니다. 하이브리드 전개는 마이그레이션 단계의 선택 역할을 하며 기밀 데이터를 온프레미스에 유지하면서 참여 논리를 클라우드에 배치할 수 있습니다. 예측 기간 동안 퍼블릭 클라우드 인프라로의 전환은 통합 패턴을 표준화하여 총 소유 비용 절감 및 공급업체 발자국의 집계를 기대합니다.

대기업은 2025년 수익의 57.02%를 차지했으며, 풍부한 예산 및 복잡한 통합 요구를 반영합니다. 한편, 중소기업은 게이미피케이션 시장에서 가장 급성장하는 부문이며, 27.65%의 연평균 복합 성장률(CAGR)로 확대 중입니다. 프리미엄 가격, 템플릿 라이브러리 및 성장에 따른 과금 아키텍처는 중소기업의 진입 장벽을 줄여줍니다.

중소기업은 일반적으로 영업팀의 동기부여 및 계절 직원의 온보딩 등 특정 과제 해결을 목적으로 도입되기 때문에 몇 주간 ROI를 입증할 수 있습니다. 싱가포르와 같은 시장에서 정부의 디지털화 보조금은 구독 비용을 보충함으로써 도입을 더욱 촉진하고 있습니다. 클라우드 플랫폼이 엔터프라이즈급 ID 관리를 대중 시장 가격대에서 제공하기 때문에 기능 측면에서의 격차는 감소하는 경향이 있습니다. 그 결과, 중견 기업을 위한 구매 담당자는 SOC 2 준수 및 싱글 사인온을 점점 더 요구하고 있으며, 공급업체는 가격 탄력성을 유지하면서 보안 강화 로드맵을 추진할 수밖에 없습니다.

지역별 분석

북미는 2025년 수익의 38.74%를 차지했으며, SaaS의 조기 도입 및 깊은 벤더 생태계의 혜택을 누리고 있습니다. 기업은 HRIS 및 CRM 제품군과의 연계를 우선하기 때문에 기능의 신속한 배치가 월렛 점유율 확대를 견인하고 있습니다. 연방 정부의 접근성 소송 위험으로 인해 플랫폼은 WCAG 호환 설계에 대한 투자를 촉진하고 모든 공급업체의 품질 기준을 인상하고 있습니다.

아시아태평양은 28.6%라는 지역 최고 CAGR을 기록하며, 모바일 퍼스트 업무 형태 및 정부 주도의 디지털 스킬 프로그램이 성장을 견인하고 있습니다. 싱가포르의 공공 서비스에서의 게이미피케이션 시책은 유효성을 실증하고, 민간 부문에서의 모방을 촉진하고 있습니다. 태국의 디지털 월렛 계획은 중앙 은행 디지털 통화(CBDC)를 게이미피케이션화한 인센티브 실험을 실시하여 정책 수준에서의 지지를 시사하고 있습니다. 기업은 저지연 5G 네트워크에 최적화된 경량 용도를 제공함으로써 이익을 얻고 있으며 인도와 인도네시아와 같은 인구 밀집 시장에서의 보급을 가속화하고 있습니다.

유럽에서는 엄격한 프라이버시 규정에도 불구하고 안정적인 수요를 볼 수 있습니다. GDPR(EU 개인정보보호규정)의 의무는 보상 데이터를 익명화하는 차등 프라이버시 분석의 혁신을 촉진하고 있습니다. MiFID-II의 대상이 되는 금융기관에 대한 동의 흐름을 커스터마이즈할 때, 사내에 법무팀을 옹호하는 벤더가 우위성을 발휘합니다. 남아메리카 및 중동 및 아프리카는 절대 금액에서 뒤쳐져 있지만 스마트폰 보급률 증가로 혜택을 누리고 있으며 클라우드 호스팅 모바일 네이티브 솔루션이 기본 옵션입니다. 이러한 신흥 지역의 전환율에서 언어 및 문화적 현지화는 여전히 결정적인 요소입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 시장 성장 촉진요인

- 클라우드 퍼스트의 디지털 워크플레이스 도입 급증

- 로우코드 게이미피케이션 플랫폼 보급

- 소매 업계에서의 로열티 전쟁의 격화 및 포인트 배지 제도 도입

- 스마트폰 중심의 마이크로러닝에 의한 현장 종업원용 연수

- 프라이버시 보호형 인게이지먼트 분석

- 중앙은행에 의한 게이미피케이션을 적용한 CBDC 파일럿 사업

- 시장 성장 억제요인

- 설계가 불충분한 프로그램은 부의 투자 이익률 초래

- 플랫폼 간 데이터 소유권에 관한 분쟁

- 업계 고유의 컴플라이언스(HIPAA, MiFID-II)에 있어서의 안티게이밍 조항

- 비종합적인 게임 메커니즘에 대한 접근성 소송

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 업계 생태계 분석

- 주요 이용 사례 및 사례 연구

- 거시 경제 동향 평가

- 투자 분석

제5장 시장 규모 및 성장 예측

- 전개 모드별

- 온프레미스

- 클라우드

- 조직 규모별

- 대기업

- 중소기업(SME)

- 업계별

- 소매

- BFSI

- 정부

- 헬스케어

- 교육 및 조사

- IT 및 통신

- 기타

- 용도별

- 마케팅 및 영업

- 인사 및 연수

- 제품 개발 및 혁신

- 고객 지원 및 고객 경험

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 싱가포르

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Microsoft Corporation

- SAP SE

- Cognizant Technology Solutions Corp.

- Axonify Inc.

- Aon plc(incl. Aon Assessment)

- Bunchball Inc.

- Salesforce Inc.(incl. Trailhead)

- Cisco Systems Inc.

- LevelEleven LLC

- Badgeville Inc.

- Genesys Cloud Services Inc.

- Callidus Software Inc.(SAP Litmos)

- Ambition Solutions Inc.

- MPS Interactive Systems Ltd.

- IACTIONABLE Inc.

- G-Cube Solutions

- Gamifier Inc.

- BI Worldwide

- Kahoot!ASA

- Classcraft Studios Inc.

제7장 시장 기회 및 장래 전망

AJY 26.01.26The gamification market was valued at USD 29.11 billion in 2025 and estimated to grow from USD 36.46 billion in 2026 to reach USD 112.32 billion by 2031, at a CAGR of 25.24% during the forecast period (2026-2031).

Cloud-based deployments already capture the majority of spend and, by delivering real-time analytics across distributed teams, underpin much of the current expansion. Large enterprises still account for the bulk of revenue, yet small and medium enterprises (SMEs) are scaling faster as low-code platforms lower adoption costs. Retail loyalty schemes remain the single-largest application, but employee-centric programs-particularly micro-learning initiatives-are recording the strongest uptake. Regionally, North America holds the lead, although Asia-Pacific's mobile-first business culture is shifting the center of gravity toward emerging digital economies. Competitive intensity stays high because established software vendors and specialist start-ups target the same white-space opportunities in regulated verticals.

Global Gamification Market Trends and Insights

Surge in Cloud-First Digital-Workplace Roll-Outs

Enterprises accelerating cloud migration need engagement tools that function natively across hybrid teams. Microsoft Power Apps embeds game mechanics directly into workflows, cutting rollout times from months to weeks . Cloud-hosted platforms generate the 27.58% CAGR forecast because they consolidate data streams and push real-time leaderboards to any device. Organizations integrating gamification with existing cloud infrastructure report up to 90% productivity improvement in remote work settings. The cost advantages of subscription licensing further accelerate adoption. As IT departments rationalize on-premise assets, cloud-native vendors gain a structural advantage that is unlikely to reverse over the outlook period.

Proliferation of Low-Code Gamification Platforms

Drag-and-drop development is democratizing the design of engagement experiences. SAP Build allows citizen developers to insert challenges, badges, and rewards into core business processes without writing code, trimming development spend by 70% against bespoke projects. The accessibility expands the total addressable base beyond large enterprises to SMEs that lacked technical resources. Platform vendors report a surge in templates focused on sales contests and onboarding missions, indicating mainstream business adoption. Because low-code stacks connect directly to SaaS ecosystems, they also shorten proof-of-value cycles, a key procurement hurdle for smaller firms. The structural decline in custom development aligns with the segment's 28.67% SME CAGR.

Poorly-Designed Programs Deliver Negative ROI

Superficial point-and-badge deployments risk disengagement and budget waste. Versus Systems' client roster fell from 16 to 5 in 2023 after lackluster implementations failed to sustain user interest, exemplifying backlash against gimmicky rollouts. Enterprises now demand business-outcome metrics, such as sales lift or error-rate reduction, before green-lighting new projects. This scrutiny lengthens sales cycles and forces vendors to provide stronger consultative support. Implementation missteps in early-adopter sectors also create caution among laggards, dampening near-term spend. Vendors that neglect instructional design and behavioral science risk reputational damage that can reverberate across the wider gamification market.

Other drivers and restraints analyzed in the detailed report include:

- Retail Loyalty Wars Escalating Points and Badges Adoption

- Smartphone-Centric Micro-Learning for Frontline Workforces

- Antigaming Clauses in Sector-Specific Compliance (HIPAA, MiFID-II)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions accounted for 67.62% of 2025 revenue, and their share of the gamification market size is projected to climb further, given a 26.91% CAGR to 2031. Real-time telemetry, seamless updates, and elastic storage underpin the preference, while maturing security certifications sway even conservative sectors. On-premise packages remain relevant where data sovereignty is paramount, yet shrinking IT budgets and rising cyber-insurance premiums tilt cost-benefit equations toward managed hosting.

Rapid iteration cycles, achieved through continuous delivery pipelines, let cloud vendors fine-tune achievement algorithms and A/B-test narratives without client-side patches. Enterprises report 37% productivity gains when advanced analytics recommend personalized challenges in real time. Hybrid rollouts serve as a transitional choice, allowing sensitive data to stay on site while engagement logic resides in the cloud. Over the forecast, migration to public-cloud stacks is expected to standardize integration patterns, reducing total cost of ownership and consolidating vendor footprints.

Large enterprises contributed 57.02% to 2025 revenue, reflecting deep budgets and complex integration needs. In contrast, SMEs represent the fastest-growing slice of the gamification market, expanding at 27.65% CAGR. Freemium pricing, template libraries, and pay-as-you-grow architectures lower entry barriers for smaller firms.

SMEs typically target narrow pain points-motivating a sales pod or onboarding seasonal staff-allowing them to demonstrate ROI within weeks. Government digitalization grants in markets such as Singapore further stimulate uptake by offsetting subscription fees. Feature parity is narrowing because cloud platforms offer enterprise-grade identity management at mass-market price tiers. As a result, mid-market buyers increasingly insist on SOC 2 compliance and single-sign-on, forcing vendors to harden security roadmaps while keeping price elasticity.

Gamification Market Report is Segmented by Deployment (On-Premise, and Cloud), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (Retail, BFSI, Government, Healthcare, and More), Application (Marketing and Sales, HR and Training, Product Development and Innovation, Customer Support and Experience, and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.74% of 2025 revenue, benefitting from early SaaS adoption and a deep vendor ecosystem. Corporations prioritize integrations with HRIS and CRM suites, leading to rapid feature rollouts that drive wallet share. Federal accessibility litigation risk motivates platforms to invest in WCAG-compliant design, raising quality thresholds for all suppliers.

Asia-Pacific records the highest regional CAGR at 28.6%, powered by mobile-first working patterns and government-sponsored digital-skills programs. Singapore's public-service gamification initiatives validate efficacy and encourage private-sector replication. Thailand's digital-wallet scheme experiments with gamified Central Bank Digital Currency incentives, signaling policy-level endorsement. Companies capitalize by shipping lightweight applications optimized for low-latency 5G networks, accelerating uptake in populous markets such as India and Indonesia.

Europe shows steady demand despite stringent privacy rules. GDPR obligations spur innovation in differential-privacy analytics that anonymize reward data. Vendors with in-house legal teams gain an edge when customizing consent flows for financial institutions subject to MiFID-II. South America and the Middle East and Africa trail in absolute dollars but benefit from growing smartphone penetration, making cloud-hosted, mobile-native solutions the default choice. Localization-both linguistic and cultural-remains a decisive factor in conversion rates across these emerging territories.

- Microsoft Corporation

- SAP SE

- Cognizant Technology Solutions Corp.

- Axonify Inc.

- Aon plc (incl. Aon Assessment)

- Bunchball Inc.

- Salesforce Inc. (incl. Trailhead)

- Cisco Systems Inc.

- LevelEleven LLC

- Badgeville Inc.

- Genesys Cloud Services Inc.

- Callidus Software Inc. (SAP Litmos)

- Ambition Solutions Inc.

- MPS Interactive Systems Ltd.

- IACTIONABLE Inc.

- G-Cube Solutions

- Gamifier Inc.

- BI Worldwide

- Kahoot! ASA

- Classcraft Studios Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in cloud-first digital-workplace roll-outs

- 4.2.2 Proliferation of low-code gamification platforms

- 4.2.3 Retail loyalty wars escalating points and badges adoption

- 4.2.4 Smartphone-centric micro-learning for frontline workforces

- 4.2.5 Privacy-preserving engagement analytics

- 4.2.6 Gamified CBDC pilots by central banks

- 4.3 Market Restraints

- 4.3.1 Poorly-designed programs deliver negative ROI

- 4.3.2 Inter-platform data-ownership disputes

- 4.3.3 Antigaming clauses in sector-specific compliance (HIPAA, MiFID-II)

- 4.3.4 Accessibility lawsuits on non-inclusive game mechanics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By Industry Vertical

- 5.3.1 Retail

- 5.3.2 BFSI

- 5.3.3 Government

- 5.3.4 Healthcare

- 5.3.5 Education and Research

- 5.3.6 IT and Telecom

- 5.3.7 Others

- 5.4 By Application

- 5.4.1 Marketing and Sales

- 5.4.2 HR and Training

- 5.4.3 Product Development and Innovation

- 5.4.4 Customer Support and Experience

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 SAP SE

- 6.4.3 Cognizant Technology Solutions Corp.

- 6.4.4 Axonify Inc.

- 6.4.5 Aon plc (incl. Aon Assessment)

- 6.4.6 Bunchball Inc.

- 6.4.7 Salesforce Inc. (incl. Trailhead)

- 6.4.8 Cisco Systems Inc.

- 6.4.9 LevelEleven LLC

- 6.4.10 Badgeville Inc.

- 6.4.11 Genesys Cloud Services Inc.

- 6.4.12 Callidus Software Inc. (SAP Litmos)

- 6.4.13 Ambition Solutions Inc.

- 6.4.14 MPS Interactive Systems Ltd.

- 6.4.15 IACTIONABLE Inc.

- 6.4.16 G-Cube Solutions

- 6.4.17 Gamifier Inc.

- 6.4.18 BI Worldwide

- 6.4.19 Kahoot! ASA

- 6.4.20 Classcraft Studios Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment