|

시장보고서

상품코드

1906941

무수프탈산 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Phthalic Anhydride - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

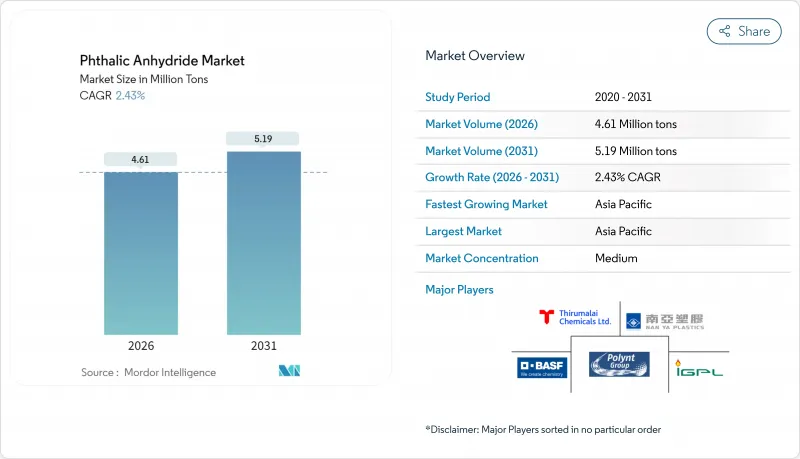

무수프탈산 시장 규모는 2026년 461만 톤으로 추정되고, 2025년 450만 톤에서 성장할 전망입니다. 2031년 예측치는 519만 톤으로, 2026-2031년 연평균 복합 성장률(CAGR) 2.43%로 확대될 전망입니다.

이 추이는 안정적인 하류 소비가 강화되는 규제 모니터링 및 바이오 대체품의 점진적인 상승과의 균형을 이루는 성숙 단계를 보여줍니다. 수요의 회복력은 건설 관련 PVC 용도, 풍력 에너지의 복합재 사용 확대, 전기자동차의 특수 요건에 기인합니다. 반면 생산 경제성은 원료 가격 변동, 특히 오르토 크실렌 가격 변동의 영향을 받고 있으며, 아시아 생산 능력 증가는 세계 마진을 계속 압박하고 있습니다. 따라서 경쟁 전략은 통합 생산 체제, 원료 유연성, 저독성 화학제품의 가속 혁신을 중심으로 전개됩니다.

세계의 무수프탈산 시장 동향 및 인사이트

아시아태평양의 PVC 기반 건설 수요 급증

중국, 인도, 인도네시아, 베트남의 건설 활동은 PVC 소비에 대한 견조한 견인력을 유지하고 있으며, 디옥틸 프탈레이트 및 관련 에스테르계 가소제 수요를 높이고 있습니다. 중국 연안부의 통합 석유화학 콤플렉스는 비용 효율적인 원료 공급 및 하류 가공 클러스터의 집적을 실현하고 있지만, 공급 과잉이 계속되었기 때문에 2024년의 전국 평균 가동률은 57%에 그쳤습니다. 인도 생산자, 특히 IG Petrochemicals와 Thirumalai Chemicals는 국내 공급 부족 및 새로운 수출 기회에 대응하기 위해 생산 능력을 강화하고 있습니다. 중국은 2024년에 약 13만 1천톤의 무수프탈산을 수출했으며, 지역 간 깊은 무역 관계를 뒷받침하고 있습니다. ISO 14001 환경 기준의 점진적인 강화로 생산자는 사회적 허용을 유지하기 위해 폐열 회수 및 저 NOx 버너에 대한 투자를 추진하고 있습니다.

풍력 터빈 블레이드에서 UPE(불포화 폴리 에스테르 수지) 사용 확대

2024-2025년 풍력 발전 설비가 급증하여 유리 섬유 블레이드에 사용되는 불포화 폴리에스테르 수지 수요가 확대되었습니다. 유럽에서의 재활용 시연 시험은 시멘트 킬른으로 사용한 블레이드를 공동 처리함으로써 클링커 생산용 광물 성분을 회수하면서 열에너지를 공급할 수 있음을 보여줍니다. 이러한 노력을 통해 2050년까지 누적 4,300만 톤으로 예측되는 블레이드 폐기물을 줄이고 차세대 터빈에 대한 새로운 수지 수요를 지속시킬 수 있습니다. 해상 프로젝트에서는 입증된 내피로성으로부터 무수프탈산계 수지 시스템이 선호됩니다. 한편, 바이오 제형의 점진적 개발은 주로 시험 단계에 있습니다. 국제에너지기구(IEA)의 넷제로 로드맵에 기반한 정책의 명확화는 복합재료 원료 수요의 장기적인 전망을 지원합니다.

EU 및 미국에서 독성에 기초한 프탈산 규제

미국 환경보호청(EPA)은 2025년 특정 스프레이 용도에서 불합리한 위험을 이유로 DINP 및 DIDP의 TSCA 위험 평가를 최종 결정했습니다. BBP, DEHP, DBP, DIBP에 대한 병행 초안 누적 평가는 종합적인 노출 시점을 도입하여 보다 광범위한 규제로 이어질 수 있습니다. 유럽연합(EU)에서는 유럽화학물질청(ECHA)의 규제 요구 평가에서 무수프탈산이 REACH 규제 하에서 제한 대상 후보로 꼽히고, 특정 업무용 및 소비자용 용도를 대상으로 하고 있습니다. 감시, 대체시험, 노동자 훈련의 컴플라이언스 비용은 상승하고 있으며, 연질 PVC의 제조자는 1,2-사이클로헥산디카르복실산 에스테르 및 시트레이트의 시험을 적극적으로 진행하고 있습니다. 중기 수요 감퇴는 틈새 도료 및 실란트 분야로 제한되지만, 장기적인 불확실성은 북미와 서유럽에서 신규 가소제 라인에 대한 투자를 방해하고 있습니다.

부문 분석

2025년 무수프탈산 시장 수요의 83.08%를 나프탈렌이 지원했습니다. 이것은 중국에서 밀집된 콜타르 증류 네트워크와 확립된 고정층 반응기 기술에 의해 지원되었습니다. 이 부문의 설비 투자(CAPEX) 면에 있어서 우위성 및 공급의 안정성이 중국 본토에서의 o-크실렌 기반 생산에 비해 평균 공장 출하 가격이 8-10% 낮은 동향을 지지하고 있습니다. 그 결과, 나프탈렌계 플랜트는 주기적인 공급 과잉에도 불구하고, 가동률이 80% 가까이를 유지하고 있습니다. 한편 오르토크실렌계는 중동 및 북미의 통합방향족 복합 시설이 정유소의 제품별을 활용함으로써 2031년까지 연평균 복합 성장률(CAGR) 3.28%로 성장해 무수프탈산 시장 전체의 성장을 웃도는 것으로 예측되고 있습니다. 고급 액상 산화 반응 장치는 에너지 소비 및 배수 부하를 줄이고 환경 발자국을 개선합니다.

궁극적으로 지역의 가용성에 따라 원료 선택이 결정됩니다. 걸프 협력 회의(GCC)의 생산자는 방향족 개질물의 잉여분을 활용하고 있는 반면, 인도 기업은 수입 오르토크실렌 및 자사 생산의 나프탈렌을 결합하여 환율 변동의 위험을 헤지하고 있습니다. 환경 규제도 고려해야 할 요소입니다. 오르토크실렌의 제조 공정은 타르 폐기물의 발생량이 적고, 베트남이나 필리핀에서 새롭게 제정된 유해 폐기물에 관한 법령의 준수를 용이하게 합니다.

무수프탈산 보고서는 원료별(오르토크실렌 및 나프탈렌), 용도별(가소제, 알키드 수지, 불포화 폴리에스테르 수지, 기타 용도), 최종 사용자 산업별(자동차, 전기 및 전자, 페인트, 코팅, 플라스틱 및 기타 최종 사용자 산업) 및 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다.

지역별 분석

아시아태평양은 2025년에 세계 전체의 61.10%를 차지했고, 2031년까지 연평균 복합 성장률(CAGR) 3.02%로 확대될 전망입니다. 산서성, 산시성, 내몽골 자치구의 통합 석탄화학 공업단지 및 강소성의 연안방향족 화합물 복합시설이 결합되어 중국은 비교할 수 없는 비용 우위성을 가지고 있습니다. 선진적인 환경 규제에 대한 정부의 우대조치로 촉매식 소각로나 응축액 회수장치로의 개수가 촉진되어 배출원 단위의 억제가 진행되고 있습니다.

유럽에서는 규제 강화 및 비용 상승이라는 역풍이 불고 있습니다. REACH 규제 대응 서류의 작성이나 에너지 가격의 변동이 조업 비용을 밀어 올려 소규모 단독 플랜트의 폐쇄를 촉진하고 있습니다. BASF사가 2025년에 실시한 루트비히스하펜 공장의 합리화는 이 동향을 상징하는 사례입니다. 그러나 유럽은 풍력 블레이드용 복합재 생산의 중심지이며, 고스펙 UPE 수요를 계속 지원하고 있습니다. 북미는 자급 체제를 유지하고 특수 등급에 주력함과 동시에 멕시코에서 급성장하는 자동차용 하네스 분야에 공급하고 있습니다. TSCA 정책의 불투명감에 의해 대규모 재투자는 억제되고 있지만, 고순도 등급 및 MOF 전구체 등 틈새 분야에서는 높은 이익률이 전망됩니다. 중동 및 아프리카에서는 소비량이 세계 총량의 일부에 머물지만 낮은 베이스에서 성장을 계속하고 있습니다. 사우디아라비아 및 아랍에미리트(UAE)은 유리한 나프타 및 방향족 흐름을 활용하고 Jubile의 새로운 통합 프로젝트에는 하류 무수프탈산 유닛의 설치도 포함되어 있습니다. 아프리카 수요는 이집트, 남아프리카, 나이지리아에 집중하고, 인프라 정비에 수반하는 PVC 파이프 및 케이블 절연재의 성장과 연동하고 있습니다. 남미 수요 동향은 완만한 성장을 유지하고 있습니다. 브라질은 PVC 및 알키드 수지 플랜트의 원료로서 아시아로부터 대량 수입을 실시하고 있는 한편 아르헨티나는 풍력 발전용 블레이드 제조에 진입해 UPE 수요 증가가 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아태평양에서의 PVC계 건축 자재 수요 급증

- 풍력 터빈 블레이드에서 UPE 사용 확대

- 전기자동차용 전선 및 케이블용 가소제 수요 증가

- 아시아의 PAN 제조업체에 의한 생산 능력 확대(저비용화)

- CCUS용 PAN계 금속 유기 구조체(MOF)의 채용

- 시장 성장 억제요인

- EU 및 미국에서 독성에 기초한 프탈산 규제

- 도료 분야에서 바이오 베이스 무수물 채용 확대

- 휘발성 오르톡실렌 원료 가격

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 기술 동향 개요

- 가격 분석

- 수출입 동향

제5장 시장 규모 및 성장 예측

- 원재료별

- 오르토크실렌

- 나프탈렌

- 용도별

- 가소제

- 알키드 수지

- 불포화 폴리에스테르 수지

- 기타 용도(염료 및 안료, 살충제 등)

- 최종 사용자 업계별

- 자동차

- 전기 및 전자 기기

- 페인트 및 코팅

- 플라스틱

- 기타 최종 사용자 산업(화학, 농업 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- AEKYUNG

- BASF

- EMCO Dyestuff

- IG Petrochemicals Ltd.

- Koppers Inc.

- LANXESS

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- NAN YA PLASTICS CORPORATION

- Paari Chem Resources

- Perstorp

- Polynt SpA

- Shandong Hongxin Chemical Co., Ltd.

- Stepan Company

- Thirumalai Chemicals

- UPC Technology Corporation

제7장 시장 기회 및 장래 전망

AJY 26.01.26Phthalic Anhydride market size in 2026 is estimated at 4.61 Million tons, growing from 2025 value of 4.5 Million tons with 2031 projections showing 5.19 Million tons, growing at 2.43% CAGR over 2026-2031.

This trajectory indicates a maturing phase in which steady downstream consumption balances intensifying regulatory oversight and a gradual rise of bio-based substitutes. Demand resilience stems from construction-linked PVC applications, expanding composite use in wind energy, and specialized requirements in electric vehicles. At the same time, production economics remain exposed to feedstock swings, particularly for ortho-xylene, while increased Asian capacity keeps global margins under pressure. Competitive strategies therefore revolve around integrated production footprints, feedstock flexibility, and accelerated innovation in lower-toxicity chemistries.

Global Phthalic Anhydride Market Trends and Insights

Surge in PVC-Based Construction Demand in APAC

Construction activity across China, India, Indonesia, and Vietnam maintains a robust pull on PVC consumption, elevating demand for dioctyl phthalate and related ester plasticizers. Integrated petrochemical complexes in coastal China deliver cost-efficient feedstock and consolidate downstream processing clusters, although countrywide utilization averaged only 57% in 2024 owing to persistent oversupply. Indian producers, notably IG Petrochemicals and Thirumalai Chemicals, are boosting capacity to address local deficit and emerging export prospects. China exported around 131,000 tons of phthalic anhydride in 2024, underscoring deep regional trade ties. Incremental tightening of ISO 14001 environmental requirements is prompting producers to invest in waste-heat recovery and low-NOx burners to sustain social license to operate.

Expansion of UPE Use in Wind-Turbine Blades

Wind-energy installations rose sharply in 2024 and 2025, amplifying demand for unsaturated polyester resins used in glass-fiber blades. European recycling pilots demonstrate that co-processing spent blades in cement kilns can reclaim mineral content for clinker production while supplying thermal energy. Such initiatives mitigate the projected 43 million tons of cumulative blade waste by 2050 and sustain virgin resin needs for next-generation turbines. Offshore projects favor phthalic-anhydride-based resin systems because of proven fatigue resistance, while incremental bio-based formulations remain largely in developmental trials. Policy clarity under the International Energy Agency's net-zero road map supports long-range visibility for composite raw-material demand.

Toxicity-Driven Phthalate Regulations in EU and US

The U.S. EPA finalized TSCA risk evaluations for DINP and DIDP in 2025, citing unreasonable risks in specific spray applications. Parallel draft cumulative assessments covering BBP, DEHP, DBP, and DIBP introduce a holistic exposure lens that may yield broader restrictions. In the European Union, ECHA's Assessment of Regulatory Needs has listed phthalic anhydrides for possible restriction under REACH, targeting certain professional or consumer uses. Compliance costs for monitoring, alternative testing, and worker training are climbing, and formulators of flexible PVC are actively trialing 1,2-cyclohexane dicarboxylic esters and citrates. While mid-term demand erosion is limited to niche coatings and sealants, long-term uncertainty hinders investment in new plasticizer lines in North America and Western Europe.

Other drivers and restraints analyzed in the detailed report include:

- Rising EV Wire-and-Cable Plasticizer Needs

- Adoption of PAN-Based MOFs for CCUS

- Shift Toward Bio-Based Anhydrides in Coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Naphthalene supported 83.08% of phthalic anhydride market demand in 2025, buoyed by dense Chinese coal-tar distillation networks and established fixed-bed reactor technology. The segment's CAPEX advantage and supply security underpin average ex-plant costs that trend 8-10% below o-xylene-based production within mainland China. As a result, naphthalene-oriented plants consistently post utilization rates near 80% despite cyclical oversupply. Ortho-xylene, however, is forecast to advance at a 3.28% CAGR through 2031, outpacing overall phthalic anhydride market growth as integrated aromatics complexes in the Middle East and North America capitalize on refinery by-products. Advanced liquid-phase oxidation reactors reduce energy intensity and effluent load, improving environmental footprints.

Regional availability ultimately dictates feedstock choice. Gulf Cooperation Council producers exploit aromatic reformate surplus, whereas Indian players hedge between imported o-xylene and captive naphthalene to cushion forex swings. Environmental regulations are another consideration: o-xylene processes generate lower tar waste streams, easing compliance with emerging hazardous-waste statutes in Vietnam and the Philippines.

The Phthalic Anhydride Report is Segmented by Raw Material (Ortho-Xylene and Naphthalene), Application (Plasticizers, Alkyd Resins, Unsaturated Polyester Resins, and Other Applications), End-User Industry (Automotive, Electrical and Electronics, Paints and Coatings, Plastics, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific controlled 61.10% of global volume in 2025 and will expand at a 3.02% CAGR through 2031. Integrated coal-chemicals parks in Shanxi, Shaanxi, and Inner Mongolia, coupled with coastal aromatics complexes in Jiangsu, give China unmatched cost leadership. Government incentives for advanced environmental controls are spurring retrofits to catalytic incinerators and condensate recovery units, curbing emissions intensity.

Europe confronts regulatory and cost headwinds. REACH dossiers and energy-price volatility lift operating expenses, pushing smaller standalone units toward closure; BASF's Ludwigshafen line rationalization in 2025 is emblematic of this trend. Yet the continent remains central to wind-blade composite production, sustaining demand for high-spec UPE. North America maintains self-sufficiency, focusing on specialty grades and supplying Mexico's burgeoning automotive harness sector. TSCA policy uncertainty tempers large-scale reinvestment, but niche opportunities in high-purity grades and MOF precursors offer higher margins. In the Middle-East and Africa, consumption remains a fraction of global totals but grows off a low base. Saudi Arabia and the UAE leverage advantaged naphtha and aromatics streams, and new integrated projects in Jubail include provision for downstream phthalic anhydride units. African demand centers on Egypt, South Africa, and Nigeria, aligned with PVC pipe and cable-insulation growth for infrastructure initiatives. South America's trajectory stays moderate; Brazil imports bulk volumes from Asia to feed hosting PVC and alkyd resin plants, while Argentina ventures into wind-blade fabrication, creating incremental UPE demand.

- AEKYUNG

- BASF

- EMCO Dyestuff

- IG Petrochemicals Ltd.

- Koppers Inc.

- LANXESS

- MITSUBISHI GAS CHEMICAL COMPANY, INC.

- NAN YA PLASTICS CORPORATION

- Paari Chem Resources

- Perstorp

- Polynt S.p.A.

- Shandong Hongxin Chemical Co., Ltd.

- Stepan Company

- Thirumalai Chemicals

- UPC Technology Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in PVC-Based Construction Demand in APAC

- 4.2.2 Expansion of UPE Use in Wind-Turbine Blades

- 4.2.3 Rising Electric-Vehicle Wire-And-Cable Plasticizer Needs

- 4.2.4 Capacity Expansions by Asian PAN Producers (Lower Costs)

- 4.2.5 Adoption of PAN-Based Metal-Organic Frameworks for CCUS

- 4.3 Market Restraints

- 4.3.1 Toxicity-Driven Phthalate Regulations in EU and US

- 4.3.2 Shift Toward Bio-Based Anhydrides in Coatings

- 4.3.3 Volatile O-Xylene Feedstock Prices

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Technological Snapshot

- 4.7 Pricing Analysis

- 4.8 Import and Export Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 Ortho-xylene

- 5.1.2 Naphthalene

- 5.2 By Application

- 5.2.1 Plasticizers

- 5.2.2 Alkyd Resins

- 5.2.3 Unsaturated Polyester Resins

- 5.2.4 Other Applications (Dyes and Pigments, Insecticides, etc.)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Electrical and Electronics

- 5.3.3 Paints and Coatings

- 5.3.4 Plastics

- 5.3.5 Other End-user Industries (Chemicals, Agriculture, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AEKYUNG

- 6.4.2 BASF

- 6.4.3 EMCO Dyestuff

- 6.4.4 IG Petrochemicals Ltd.

- 6.4.5 Koppers Inc.

- 6.4.6 LANXESS

- 6.4.7 MITSUBISHI GAS CHEMICAL COMPANY, INC.

- 6.4.8 NAN YA PLASTICS CORPORATION

- 6.4.9 Paari Chem Resources

- 6.4.10 Perstorp

- 6.4.11 Polynt S.p.A.

- 6.4.12 Shandong Hongxin Chemical Co., Ltd.

- 6.4.13 Stepan Company

- 6.4.14 Thirumalai Chemicals

- 6.4.15 UPC Technology Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment