|

시장보고서

상품코드

1906950

말레이시아의 플라스틱 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Malaysia Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

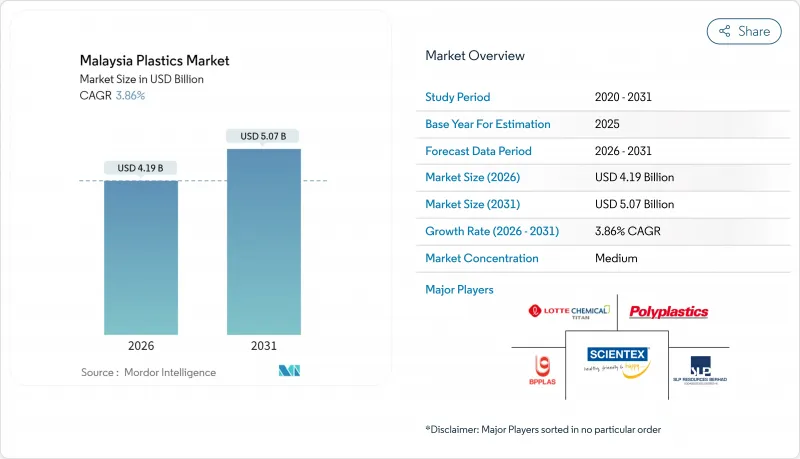

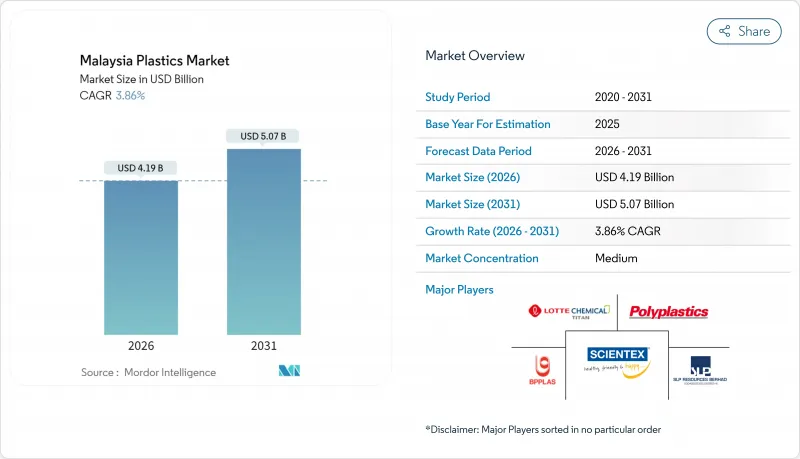

말레이시아의 플라스틱 시장 규모는 2026년에 41억 9,000만 달러로 추정되고, 2025년 40억 4,000만 달러에서 계속 성장하고 있습니다. 2031년 예측은 50억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR) 3.86%로 확대될 것으로 전망됩니다.

이 꾸준한 확대는 말레이시아가 지역적인 석유화학 원료 공급 거점인 동시에 동남아시아 전역의 전자기기, 자동차 및 포장 밸류체인에 공급하는 하류 제조 거점이라는 이중 역할을 담당하고 있는 것에 지지되고 있습니다. 페트로나스의 통합 플랜트로부터의 안정적인 원료 공급, 세랑고르주, 조호르주, 페낭주에서의 수출 지향형 제조 클러스터, 그리고 하류 석유화학 산업을 위한 정책 주도형 인센티브가 함께 공급의 안정성과 비용 경쟁력을 강화하고 있습니다. 게다가 재활용 소재와 바이오 베이스 소재를 요구하는 세계의 브랜드, 말레이시아의 일회용 플라스틱 제로화 로드맵, 기능 부족 대책으로서의 자동화 가공에 대한 투자가 성장의 기세를 뒷받침하고 있습니다. 한편, 환경 규제 및 원료 가격 변동은 이익률을 억제하는 것, 특수 등급 및 정밀 성형 등 고부가가치 용도로의 전환을 촉진하여 프리미엄 가격의 획득을 가능하게 하고 있습니다.

말레이시아의 플라스틱 시장 동향 및 인사이트

식품 및 음료 포장 분야에서 수요 증가

식품 및 음료 제조업체는 수출 시장의 고급 식품 안전 기준을 충족하기 위해 플라스틱 장벽 필름 및 다층 구조에 의존합니다. 펭귄 통합 복합 시설 내에 바이오리파이너리를 통합하는 페트로나스사의 결정은 바이오 포장 수지의 현지 공급이 곧 실현될 것임을 나타냅니다. 말레이시아 수출 식품 거래에 널리 적용되는 할랄 인증 규칙은 장거리 운송 중에도 제품 무결성을 유지하는 특수 포장이 필요합니다. 도시 지역의 소득 수준 상승 및 즉시 먹을 수 있는 형태에 대한 선호도 증가가 편리한 포장 소비를 확대하고 있습니다. 그 결과 스탠드업 파우치, 레토르트 파우치, PET 음료병을 공급하는 컨버터는 성능과 지속가능성 인증에 연동된 프리미엄 마진을 확보하고 있습니다.

전자기기 제조 생태계 성장

말레이시아의 국가 반도체 전략은 인피니언과 같은 세계 기업들로부터 새로운 투자를 불러들여 백엔드 패키징, 테스트, IC 설계 활동의 확대를 촉진하고 있습니다. 5G 인프라 및 전기자동차용 반도체 모듈은 높은 열 안정성 및 난연 성능을 갖춘 엔지니어링 플라스틱의 채택이 증가하고 있습니다. 따라서 페낭의 바얀 레파스와 크림 하이테크 파크에서는 마이크론 단위의 공차를 실현하는 사출 성형 라인이 급속히 보급되고 있습니다. 자동 시각 검사 및 폐쇄 루프 성형 시스템을 통해 제조업체는 엄격한 불량률 요구 사항을 충족하면서 정밀 폴리머 가공의 현지 기술자 부족을 보완할 수 있습니다.

환경 문제 및 일회용 제품 금지

말레이시아의 2025-2030년 일회용 플라스틱 제로화 로드맵에서는 일회용 봉투, 빨대, 발포 스티롤 제식기에 대해 단계적인 규제가 부과되고 있습니다. 2025년 7월에 강화된 플라스틱 스크랩의 수입 규제로 저비용 원료 공급원은 상실되었지만 국내 폐기물 처리에 대한 국민의 인식은 향상되었습니다. 재활용 가능하거나 퇴비화 가능한 제품으로 전환할 수 없는 가공업자는 쿠알라룸푸르 수도권, 조호르 바루, 조지타운에서 더 높은 물품세와 엄격한 집행에 직면합니다. 한편, 퇴비화 가능한 필름 라인과 재사용 가능한 푸드 서비스 모델을 보유한 기업은 규정 준수 대체품으로의 전환을 포착하고 있습니다.

부문 분석

폴리에틸렌 및 폴리프로필렌과 같은 기존 폴리머는 저비용 생산을 지원하는 펜게란의 통합 크래커 폴리머 라인에 힘입어 2025년 시점에서 말레이시아 플라스틱 시장 점유율의 78.84%를 유지했습니다. 한편, 생분해성 플라스틱은 퇴비화 가능 포장재를 요구하는 브랜드 목표와 이 나라에서 일회용 제품 금지의 동향에 뒷받침되어 CAGR4.86%에서 가장 급속한 성장이 전망되고 있습니다. 전기 절연재 및 자동차 보닛 하부 부품용 엔지니어링 수지는 현지 마감을 위해 재조정된 수입 반제품 컴파운드의 지원을 받아 중간 정도의 단일 자릿수 성장을 달성했습니다.

말레이시아의 플라스틱 시장에 관련된 생산자는 기존 크래커에서 필름까지의 물류망을 활용하여 대량 소비재용 용도에 공급하고 있지만, 증가하는 EPR(확대 생산자 책임) 과징금에 의해 이익률이 압박되고 있습니다. 조호르의 복합시설 내에 건설 예정인 바이오리파이너리에 의해 화석 유래의 PET나 PE의 대체품이 실현되고, 현지의 컨버터는 수출 입찰에 있어서 고도의 리사이클 크레딧을 획득할 수 있는 입장이 됩니다. 말레이시아의 플라스틱 산업용 특수 컴파운더는 난연성, 유리 섬유 강화, 무할로겐 등급(특히 스마트 장치용 커넥터용)을 제공함으로써 프리미엄 가격을 획득하고 있습니다. 재료과학 분야에서 스킬 갭의 확대는 식품 접촉 용도 및 전자부품 인증을 위한 새로운 바이오베이스 등급을 인정할 수 있는 기술 서비스 팀의 가치를 돋보이게 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 식품 및 음료 포장 분야에서 수요 증가

- 전자기기 제조 생태계 성장

- 하류 석유화학 산업에 대한 정부의 우대조치

- 세계 브랜드에 의한 순환형 경제에 대한 대처

- 의료기기 클러스터의 확대

- 시장 성장 억제요인

- 환경 문제 및 일회용 제품 금지

- 원료 가격의 변동성

- 고도의 폴리머 가공에서 스킬 부족

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 가격 동향 분석

- 수입 및 수출

제5장 시장 규모 및 성장 예측

- 유형별

- 기존 플라스틱

- 엔지니어링 플라스틱

- 바이오플라스틱

- 기술별

- 블로우 성형

- 압출 성형

- 사출 성형

- 기타 기술

- 용도별

- 포장

- 전기 및 전자 기기

- 건축 및 건설

- 자동차 및 운송

- 가정용품

- 가구 및 침구

- 기타 용도

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%) 및 순위 분석

- 기업 프로파일

- Behn Meyer

- BP Plastics Holding Bhd

- Commercial Plastic Industries Sdn Bhd

- CYL Corporation

- Ee-Lian Enterprise(M) Sdn. Bhd.

- Fu Fong Plastic Industries Sdn Bhd

- Guppy Group

- HICOM-Teck See

- Lam Seng Plastics Industries Sdn Bhd

- LOTTE CHEMICAL TITAN HOLDING BERHAD.

- Malayan Electro-Chemical Industry Co. Sdn Bhd

- Meditop International

- Megafoam Containers Enterprise Sdn Bhd(MEGAFOAM)

- Metro Plastic Manufacturer Sdn. Bhd.

- Polyplastics Co., Ltd.

- Sanko Plastics(M) Sdn Bhd

- Scientex Berhad

- SLP RESOURCES BERHAD

- Teck See Plastic Sdn Bhd(TSP)

- TORAY INDUSTRIES, INC.

제7장 시장 기회 및 장래 전망

AJY 26.01.26The Malaysia Plastics Market size in 2026 is estimated at USD 4.19 billion, growing from 2025 value of USD 4.04 billion with 2031 projections showing USD 5.07 billion, growing at 3.86% CAGR over 2026-2031.

This steady expansion is anchored by Malaysia's dual role as a regional petrochemical feedstock hub and a downstream manufacturing base that supplies the electronics, automotive, and packaging value chains across Southeast Asia. Stable feedstock from PETRONAS's integrated complexes, export-oriented manufacturing clusters in Selangor, Johor, and Penang, and policy-driven incentives for downstream petro-chemicals together reinforce supply security and cost competitiveness. Momentum is further supported by global brands demanding recycled or bio-based content, Malaysia's zero single-use plastics roadmap, and investments in automated processing that counter skills shortages. Meanwhile, environmental regulation and feedstock price volatility continue to temper margins but also catalyze upgrades into higher-value applications where specialty grades and precision molding command premium pricing.

Malaysia Plastics Market Trends and Insights

Rising Demand From Food and Beverage Packaging

Food and beverage manufacturers rely on plastic barrier films and multilayer structures to meet higher food-safety standards in export markets. PETRONAS's decision to embed a biorefinery inside the Pengerang Integrated Complex signals an upcoming local supply of bio-based packaging resins. Halal certification rules, prevalent in Malaysia's export food trade, necessitate specialized packaging that maintains product integrity during long transit times. Rising urban income levels and a preference for ready-to-eat formats amplify the consumption of convenience packaging. As a result, converters supplying stand-up pouches, retort pouches, and PET beverage bottles are securing premium margins tied to performance and sustainability credentials.

Growth of Electronics Manufacturing Ecosystem

Malaysia's National Semiconductor Strategy has attracted fresh investments from global players such as Infineon to expand back-end packaging, testing, and IC design activities. Semiconductor modules for 5G infrastructure and electric vehicles increasingly specify engineering plastics with high thermal stability and flame-retardant performance. Injection molding lines capable of micron-level tolerances are therefore proliferating within Penang's Bayan Lepas and Kulim High-Tech parks. Automated vision inspection and closed-loop molding systems allow manufacturers to meet tight defect-rate requirements while offsetting the local skills gap in precision polymer processing.

Environmental Concerns and Single-Use Bans

Malaysia's 2025-2030 zero single-use plastics roadmap imposes phased restrictions on disposable bags, straws, and EPS foodware. Import controls on plastic scrap, tightened in July 2025, have removed low-cost feedstock streams but improved public perception of domestic waste handling. Converters that cannot pivot to recyclable or compostable formats face higher excise levies and tighter enforcement in Greater Kuala Lumpur, Johor Bahru, and George Town. Conversely, firms with compostable film lines and reusable food-service models are capturing the shift toward regulatory-compliant alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Downstream Petro-Chemicals

- Circular-Economy Commitments by Global Brands

- Feedstock Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional polymers such as polyethylene and polypropylene retained 78.84% Malaysia plastics market share in 2025, buoyed by Pengerang's integrated cracker and polymer lines that anchor low-cost output. Bioplastics, however, are forecast to grow fastest at a 4.86% CAGR, aided by brand targets for compostable packaging and the country's single-use ban trajectory. Engineering resins addressing electrical insulation and under-hood automotive parts achieved mid-single-digit growth, supported by imported semifinished compounds rewired for localized finishing.

Producers associated with the Malaysia plastics market leverage existing cracker-to-film logistics to supply high-volume FMCG applications, yet face mounting EPR levies that narrow margins. The upcoming biorefinery within Johor's complex will enable drop-in replacements for fossil-based PET and PE, positioning local converters to claim advanced recycling credit in export tenders. Specialty compounders catering to the Malaysia plastics industry gain premium prices by offering flame-retardant, glass-fiber, and halogen-free grades, particularly for smart-device connectors. A widening skills gap in materials science underscores the value of technical service teams able to qualify new bio-based grades for food-contact and electronic-component certification.

The Malaysia Plastics Market Report is Segmented by Type (Traditional Plastics, Engineering Plastics, and Bioplastics), Technology (Blow Molding, Extrusion, Injection Molding, and Other Technologies), and Application (Packaging, Electrical and Electronics, Building and Construction, Automotive and Transportation, Houseware, Furniture and Bedding, and Other Applications). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Behn Meyer

- BP Plastics Holding Bhd

- Commercial Plastic Industries Sdn Bhd

- CYL Corporation

- Ee-Lian Enterprise (M) Sdn. Bhd.

- Fu Fong Plastic Industries Sdn Bhd

- Guppy Group

- HICOM-Teck See

- Lam Seng Plastics Industries Sdn Bhd

- LOTTE CHEMICAL TITAN HOLDING BERHAD.

- Malayan Electro-Chemical Industry Co. Sdn Bhd

- Meditop International

- Megafoam Containers Enterprise Sdn Bhd (MEGAFOAM)

- Metro Plastic Manufacturer Sdn. Bhd.

- Polyplastics Co., Ltd.

- Sanko Plastics (M) Sdn Bhd

- Scientex Berhad

- SLP RESOURCES BERHAD

- Teck See Plastic Sdn Bhd (TSP)

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand from food and beverage packaging

- 4.2.2 Growth of electronics manufacturing ecosystem

- 4.2.3 Government incentives for downstream petro-chemicals

- 4.2.4 Circular-economy commitments by global brands

- 4.2.5 Expansion of medical-device clusters

- 4.3 Market Restraints

- 4.3.1 Environmental concerns and single-use bans

- 4.3.2 Feed-stock price volatility

- 4.3.3 Skills gap in advanced polymer processing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Price Trend Analysis

- 4.7 Imports and Exports

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.2 Engineering Plastics

- 5.1.3 Bioplastics

- 5.2 By Technology

- 5.2.1 Blow Molding

- 5.2.2 Extrusion

- 5.2.3 Injection Molding

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Packaging

- 5.3.2 Electrical and Electronics

- 5.3.3 Building and Construction

- 5.3.4 Automotive and Transportation

- 5.3.5 Houseware

- 5.3.6 Furniture and Bedding

- 5.3.7 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Behn Meyer

- 6.4.2 BP Plastics Holding Bhd

- 6.4.3 Commercial Plastic Industries Sdn Bhd

- 6.4.4 CYL Corporation

- 6.4.5 Ee-Lian Enterprise (M) Sdn. Bhd.

- 6.4.6 Fu Fong Plastic Industries Sdn Bhd

- 6.4.7 Guppy Group

- 6.4.8 HICOM-Teck See

- 6.4.9 Lam Seng Plastics Industries Sdn Bhd

- 6.4.10 LOTTE CHEMICAL TITAN HOLDING BERHAD.

- 6.4.11 Malayan Electro-Chemical Industry Co. Sdn Bhd

- 6.4.12 Meditop International

- 6.4.13 Megafoam Containers Enterprise Sdn Bhd (MEGAFOAM)

- 6.4.14 Metro Plastic Manufacturer Sdn. Bhd.

- 6.4.15 Polyplastics Co., Ltd.

- 6.4.16 Sanko Plastics (M) Sdn Bhd

- 6.4.17 Scientex Berhad

- 6.4.18 SLP RESOURCES BERHAD

- 6.4.19 Teck See Plastic Sdn Bhd (TSP)

- 6.4.20 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment