|

시장보고서

상품코드

1906968

에폭시 코팅 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Epoxy Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

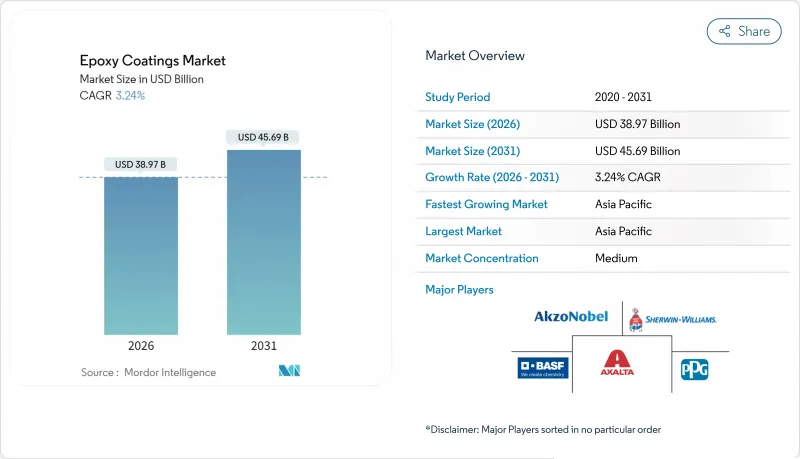

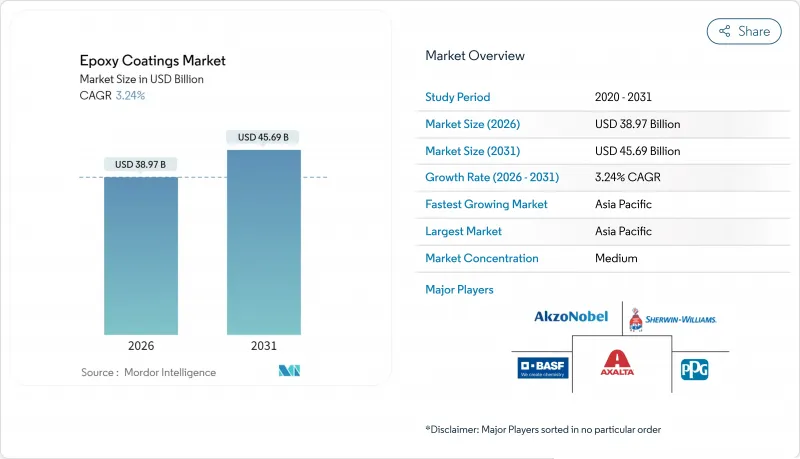

에폭시 코팅 시장은 2025년 377억 5,000만 달러로 평가되었고, 2026년 389억 7,000만 달러에서 2031년까지 456억 9,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 3.24%를 나타낼 전망입니다.

측정된 속도는 강화된 배출 규제를 확대되는 최종 사용 수요와 균형 잡는 성숙한 부문을 반영합니다. 제조업체들은 지속 가능한 화학 기술, 특히 휘발성 유기 화합물(VOC)을 억제하는 수성 기술에 투자를 집중하고 있습니다. 건설, 자동차 및 산업 고객들은 강화되는 대기질 규제를 준수하고 작업장 안전을 개선하기 위해 이러한 저VOC 제품으로 전환하고 있습니다. 공급업체들이 특수 응용 분야와 지역별 성장 중심지로 재편되면서, 일반 제품 라인 매각 및 고성능 자산 인수와 같은 포트폴리오 최적화가 주요 경쟁 전략으로 부상했습니다.

세계의 에폭시 코팅 시장 동향 및 인사이트

산업용 보호 페인트에서 수성 에폭시의 침투율 상승

산업 시설들은 미국 환경보호청(EPA)의 갤런당 4.8파운드 제한과 같은 엄격한 휘발성 유기화합물 배출 기준을 충족하기 위해 수성 시스템으로의 전환을 가속화하고 있습니다. 수지 화학 기술의 발전으로 이제 수성 에폭시도 과거 용제 기반 제품만의 장점이었던 신장률과 내화학성을 따라잡을 수 있게 되었습니다. 2024년 연구에 따르면 에폭시화 천연 고무 라텍스를 사용한 경우 내구성을 저하시키지 않으면서 신장률이 370% 향상되었습니다. 고고형분 버전은 도포 시 사실상 VOC를 배출하지 않아 공장이 대기질 허가 기준을 충족하고 작업자 안전성을 개선하는 데 기여합니다. 규제 준수 기한이 다가옴에 따라 공장 유지보수 프로그램의 수성 제품 전환은 단기적 트렌드가 아닌 구조적 시장 변화로 자리 잡고 있습니다.

식품 및 음료 공장에서 산업용 바닥재 업그레이드

식품 가산업체들은 강력한 살균제에 견디고 미국 농무부(USDA) 검사를 통과하는 에폭시 바닥재로 생산 구역을 재포장하고 있습니다. 노볼락 화학 제품은 낮은 pH 음료를 취급하는 시설에 탁월한 내산성을 제공하며, 100% 고형분 제형은 용제 증발 없이 경화되어 작업 시간을 단축합니다. 운영자들은 수명 주기 모델을 통해 유지보수 비용 감소와 가동 중단 횟수 감소를 확인하면 초기 비용이 높아도 기꺼이 지불합니다. 글로벌 식품 안전 감사가 빈도와 엄격함을 더해감에 따라 이 추세는 더욱 가속화되고 있습니다.

용제 기반 시스템에 대한 글로벌 VOC/HAP 배출 제한 강화

뉴욕주는 산업용 유지보수 코팅제의 VOC 함량을 250g/L로 제한하는 반면, 캘리포니아주는 용도에 따라 100g/L까지 허용합니다. 중국의 GB 30981-2020 표준도 유해 성분에 대해 유사한 상한선을 설정합니다. 규정 미준수 시 벌금 및 시장 접근 장벽이 발생하여 제형 개발사들은 재설계에 투자하거나 해당 지역에서 철수해야 하는 상황에 직면합니다. 많은 경우 수성 또는 분체 대체재가 기존 제품의 성능을 아직 따라잡지 못해 특수 니치 시장에서 단기적 공급 공백이 발생하고 있습니다.

부문 분석

수성 화학 물질은 2025년 매출의 41.80%를 차지했으며 4.32%의 연평균 성장률(CAGR)로 최고 성장률을 기록했습니다. 원자재 공급업체들이 상온 경화형 아민 첨가제 및 자가 가교 수지를 개발함에 따라 비용 경쟁력이 향상되었습니다. 용제형 제품은 극한의 내식성이 VOC(휘발성 유기화합물) 문제보다 우선시되는 해양, 석유·가스, 중장비 분야에서 계속 사용됩니다. 분체 페인트는 점유율이 증가 중이지만 여전히 소수이며, 자동차 휠, 가전제품, 금속 가구 분야에서 도입이 진행 중입니다. 그래핀 강화 분체는 염수 분무 시험에서 부식 방지 주기 시간을 두 배로 늘리는 것으로 입증되었습니다.

수성 코팅 공급업체들은 전 생애 주기 지속가능성 지표를 강조합니다. 핫스팟 없는 생애주기 평가, 공장 환기 요구 감소, 보험료 절감 등이 대표적입니다. 최소 플라스틱 사용 재사용 용기에 2액형 팩을 생산함으로써 범위 3 배출량을 추가로 절감하여 고객사의 탄소중립 로드맵과 부합합니다. 분체 코팅 업체들은 가열로 에너지 절감과 열에 민감한 기판 코팅을 가능케 하는 저온 경화 화학 기술을 통해 탈탄소화를 추진합니다.

에폭시 코팅 보고서는 기술별(수성, 용제계, 분체), 최종 사용자 산업별(건축 및 건설, 자동차, 운송, 산업, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

지역별 분석

아시아태평양 지역은 광범위한 제조 기반과 지속적인 인프라 확장으로 2025년 글로벌 매출의 46.43%를 차지했습니다. 중국은 지역 수요의 절반 이상을 차지하며, 지방자치단체의 용제 사용 금지 조치에 따라 수성 외벽 코팅으로의 전환을 가속화하고 있습니다. 인도의 스마트 시티 미션과 인도네시아의 유료도로 확장은 교량, 공항, 대중교통 터미널로 에폭시 주문이 집중되도록 합니다. 해당 지역 에폭시 코팅 시장은 연평균 3.63% 성장할 것으로 전망됩니다. 현지 허브를 보유한 국내 공급업체는 관세 혜택과 빠른 납품 기간을 누리며, 특히 페인트 수입에 추가 관세가 부과되는 인도네시아에서 이점이 크다.

북미는 항공우주 및 전기차 공장을 위한 신속 경화 및 복합재 호환 시스템으로 기술 선도권을 유지하고 있습니다. 공장 바닥, 송유관 보수, 해양 플랫폼 등 리모델링 수요는 경기 침체기에도 안정적인 기본 소비량을 유지합니다. 유럽 수요는 노후 인프라 재건축과 용제에서 수성으로의 전환을 가속화하는 진보적인 VOC(휘발성 유기화합물) 법규에 의해 주도됩니다. 고객들은 낮은 생애주기 배출량을 검증하는 에코라벨 인증 페인트에 프리미엄을 지불할 의사가 있습니다. 남미, 중동, 아프리카는 점진적이지만 고르지 않은 성장을 보입니다. 브라질은 현지 유통망을 확장하는 11억 5천만 달러 규모의 인수 사례에서 드러나듯 외국인 투자가 재개되고 있습니다. 환율 변동과 정치적 리스크가 프로젝트 파이프라인을 위축시키지만, 계약사들은 가혹한 환경 조건에서 자산 수명을 연장하기 위해 내구성 있는 라이닝을 계속해서 지정하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 산업용 보호 페인트의 수성 에폭시의 침투율 상승

- 아시아태평양 및 아프리카의 건설 부문 확대

- 식품 및 음료 플랜트의 산업용 바닥재의 업그레이드

- 높은 처리량을 실현하는 급속 경화형 UV/LED 경화 에폭시 기술

- 전기차 배터리 케이싱 및 모터 하우징의 내화학성 코팅 수요 증가

- 시장 성장 억제요인

- 용제계 시스템에 대한 세계의 VOC/HAP 배출 규제의 엄격화

- BPA 및 에피클로로히드린 가격 변동성으로 인한 원가 구조 교란

- 인증된 바이오 기반 에폭시 전구체 공급 제한

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- 수성

- 용제계

- 분체

- 최종 사용자 업계별

- 건축 및 건설

- 자동차

- 운송

- 산업

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 북유럽 국가

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- AkzoNobel NV

- Asian Paints

- Axalta Coating Systems LLC

- BASF

- Berger Paints India

- Diamond Vogel

- DuluxGroup Ltd

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Koster Bauchemie AG

- Nippon Paint Holdings Co., Ltd.

- Pidilite Industries Limited

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- The Euclid Chemical Company

- The Sherwin-Williams Company

- Tikkurila

제7장 시장 기회와 장래의 전망

HBR 26.02.04The Epoxy Coatings Market was valued at USD 37.75 billion in 2025 and estimated to grow from USD 38.97 billion in 2026 to reach USD 45.69 billion by 2031, at a CAGR of 3.24% during the forecast period (2026-2031).

The measured pace mirrors a mature sector that is balancing tougher emission rules with widening end-use demands. Manufacturers are channeling investment toward sustainable chemistries, particularly waterborne technologies that curb volatile organic compounds. Construction, automotive, and industrial customers are pivoting toward these low-VOC offerings to comply with tightening air-quality mandates and to improve workplace safety. Portfolio optimization, such as divestitures of commodity lines and acquisitions of high-performance assets, has become the dominant competitive tactic as suppliers reposition around specialty applications and regional growth hotspots.

Global Epoxy Coatings Market Trends and Insights

Waterborne Epoxy Penetration Rising in Industrial Protective Coatings

Industrial facilities are accelerating the shift toward waterborne systems to meet strict volatile organic compound caps, such as the U.S. Environmental Protection Agency limit of 4.8 pounds per gallon. Advances in resin chemistry now allow waterborne epoxies to match the elongation and chemical resistance once exclusive to solvent-based products. A 2024 study using epoxidized natural-rubber latex recorded a 370% gain in elongation without sacrificing durability. High-solids versions emit virtually no VOCs during application, helping plants satisfy air-quality permits and improve worker safety profiles. As compliance deadlines tighten, the conversion of factory maintenance programs to waterborne offerings is becoming a structural market shift rather than a short-term trend.

Industrial Flooring Upgrades in Food and Beverage Plants

Food processors are resurfacing production areas with epoxy floors that withstand aggressive sanitizers and meet USDA inspections. Novolac chemistries offer exceptional acid resistance for facilities that handle beverages with low pH, while 100% solids formulations shorten turnaround times because they cure without solvent evaporation. Operators are willing to pay higher upfront costs once lifecycle models reveal lower maintenance spending and fewer shutdowns. The trend gains momentum as global food-safety audits grow in frequency and rigor.

Stringent Global VOC/HAP Emission Limits on Solvent-Based Systems

New York limits industrial maintenance coatings to 250 g/L VOC, while California allows as little as 100 g/L depending on use. China's GB 30981-2020 standard sets parallel caps on harmful constituents. Non-compliance triggers fines and market access barriers, forcing formulators to invest in re-engineering or face regional exit. In many cases, waterborne or powder alternatives cannot yet duplicate the performance of legacy products, leaving short-term supply gaps in specialty niches.

Other drivers and restraints analyzed in the detailed report include:

- Rapid-Cure UV/LED-Curable Epoxy Technologies Enabling Higher Throughput

- EV Battery Casings and Motor Housings Need Chemically-Resistant Coats

- BPA and Epichlorohydrin Price Volatility Disrupting Cost Structures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-based chemistries contributed 41.80% of 2025 revenue and hold the top growth slot at 4.32% CAGR. Cost competitiveness has improved as raw-material suppliers develop amine adducts and self-crosslinking resins that cure under ambient conditions. Solvent-borne grades continue in marine, oil-and-gas, and heavy-equipment segments where extreme corrosion resistance overrides VOC concerns. Powder coatings account for a rising but still minority share; adoption is pacing automotive wheels, home appliances, and metal furniture. Graphene-reinforced powders have proven to double corrosion-protection cycle time in salt-spray testing.

Waterborne suppliers emphasize cradle-to-grave sustainability metrics: zero-hot-spot life-cycle assessments, reduced plant ventilation needs, and lower insurance premiums. Production of two-component packs in minimal-plastic, returnable containers further cuts scope-3 emissions, aligning with customer net-zero roadmaps. Powder-coating vendors target decarbonization by promoting low-temperature cure chemistries that save furnace energy and enable coating of heat-sensitive substrates.

The Epoxy Coatings Report is Segmented by Technology (Water-Based, Solvent-Based, and Powder-Based), End-User Industry (Building and Construction, Automotive, Transportation, Industrial, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 46.43% of global sales in 2025, reflecting its broad manufacturing base and relentless infrastructure build-out. China represents more than half of regional demand and is intensifying its transition to waterborne exterior wall coatings under municipal solvent bans. India's Smart Cities Mission and Indonesia's toll-road expansions funnel epoxy orders into bridges, airports, and mass-transit depots. The epoxy coatings market is forecast to grow by a 3.63% CAGR in the region. Local suppliers with in-country hubs enjoy tariff advantages and faster delivery times, especially in Indonesia, where paint imports face incremental duties.

North America remains a technology leader through rapid-cure and composite-compatible systems designed for aerospace and electric-vehicle plants. Retrofit demand, such as factory floors, oil-pipeline refurbishment, and offshore platforms, maintains a steady baseline consumption even in flat macro cycles. European demand is driven by the renovation of aged infrastructure and progressive VOC legislation that accelerates solvent-to-water conversions. Customers are willing to pay premiums for coatings certified under Ecolabel frameworks that validate low life-cycle emissions. South America, the Middle East, and Africa offer incremental but uneven growth. Brazil is experiencing renewed foreign investment, exemplified by a USD 1.15 billion acquisition that broadens local distribution reach. Currency swings and political risk temper project pipelines, yet contractors continue to specify durable linings to extend asset life under harsh environmental conditions.

- AkzoNobel N.V.

- Asian Paints

- Axalta Coating Systems LLC

- BASF

- Berger Paints India

- Diamond Vogel

- DuluxGroup Ltd

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Koster Bauchemie AG

- Nippon Paint Holdings Co., Ltd.

- Pidilite Industries Limited

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- The Euclid Chemical Company

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Waterborne Epoxy Penetration Rising in Industrial Protective Coatings

- 4.2.2 Construction Sector Expansion in APAC and Africa

- 4.2.3 Industrial Flooring Upgrades in Food and Beverage Plants

- 4.2.4 Rapid-Cure UV/LED-Curable Epoxy Technologies Enabling Higher Throughput

- 4.2.5 EV Battery Casings and Motor Housings Need Chemically Resistant Coats

- 4.3 Market Restraints

- 4.3.1 Stringent Global VOC/HAP Emission Limits on Solvent-Based Systems

- 4.3.2 BPA and Epichlorohydrin Price Volatility Disrupting Cost Structures

- 4.3.3 Limited Supply of Certified Bio-Based Epoxy Precursors

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Powder-based

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Transportation

- 5.2.4 Industrial

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 NORDIC

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems LLC

- 6.4.4 BASF

- 6.4.5 Berger Paints India

- 6.4.6 Diamond Vogel

- 6.4.7 DuluxGroup Ltd

- 6.4.8 Hempel A/S

- 6.4.9 Jotun

- 6.4.10 Kansai Paint Co., Ltd.

- 6.4.11 Koster Bauchemie AG

- 6.4.12 Nippon Paint Holdings Co., Ltd.

- 6.4.13 Pidilite Industries Limited

- 6.4.14 PPG Industries, Inc.

- 6.4.15 RPM International Inc.

- 6.4.16 Sika AG

- 6.4.17 The Euclid Chemical Company

- 6.4.18 The Sherwin-Williams Company

- 6.4.19 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment