|

시장보고서

상품코드

1906996

본질 안전 방폭 장비(IS 장비) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Intrinsically Safe Equipment (IS Equipment) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

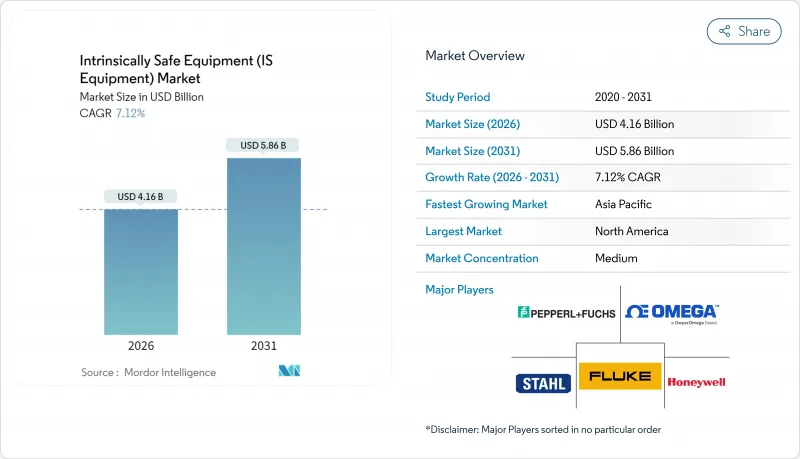

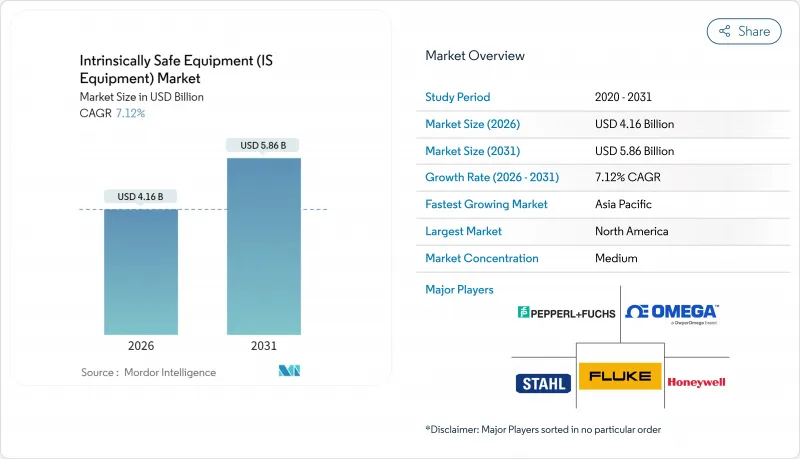

본질 안전 방폭 장비(IS 장비) 시장은 2025년 38억 8,000만 달러로 평가되었고 예측 기간(2026-2031년)에 CAGR 7.12%를 나타내 2026년 41억 6,000만 달러에서 2031년까지 58억 6,000만 달러에 달할 전망입니다.

이 확장은 중후한 방폭 하우징에서 규제 준수와 Industry 4.0의 연결성을 결합한 디지털 대응의 본질 안전 아키텍처로의 전환을 반영합니다. 세계 표준의 엄격화, 광업 및 공정 산업의 확대, 무선 모듈에 의한 종래에는 채산이 불가능하다고 생각되고 있던 개수 프로젝트의 실현에 의해 수요는 가속하고 있습니다. 석유 및 가스 사업자는 여전히 주요 고객이지만, 휘발성 용제가 생산 라인에 도입됨에 따라 개별 부품 제조업체도 인증 취득된 자동화 기술을 채용하게 되었습니다. 시설 소유자가 새로운 시스템의 사양을 결정할 때 라이프사이클 비용, 공급망 확실성, 예지보전 기능을 고려하여 인증과 사이버 보안을 모두 습득한 기업이 최대의 가치를 획득하고 있습니다.

세계의 본질 안전 방폭 장비(IS 장비) 시장 동향과 인사이트

엄격한 세계 방폭 안전 규제

2024년 1월에 발행된 IEC 60079-11 7판에는 173개의 기술적 개정이 도입되었습니다. 여기에는 보다 엄격한 전지 시험과 그룹 IIC 환경에서의 촉매식 센서의 사용 금지가 포함되어 있어 기존 설비 전체에서의 개수 투자를 촉구하는 내용이 되고 있습니다. EN IEC 60079-11 : 2024는 2024년 12월에 유럽 연합관보에 게재되었으며, 2012년 버전은 2027년 12월까지 조화 해제되어 의무적 업그레이드의 명확한 실시 기간이 설정되었습니다. 다국적기업은 ATEX와 IECEx의 서류 대응에 분주하고 있지만, 기술적인 무결성에도 불구하고 제출 스케줄의 동기화는 아직 실현되지 않았습니다. 또한 본 규제는 기기의 범위를 넘어, IEC 60079-14 : 2024에 근거한 현장 배선도 대상으로 확대되어 인증이 끝난 설치 및 재인증 서비스 수요를 환기하고 있습니다. 이러한 움직임이 결합되어 사업자가 비준거 자산을 교환하고 신규규칙에 연동한 장기보수계약을 체결함에 따라 본질 안전 방폭 장비(IS 장비) 시장은 확대되고 있습니다.

인더스트리 4.0이 견인하는 본질 안전 방폭 센서·계장기기 수요

디지털 전환의 진전에 수반해, 위험 구역으로부터의 실시간 데이터 수집 요구가 높아지고 있어, 본질 안전 방폭 센서가 최전선의 실현 수단으로서 자리매김되고 있습니다. 이더넷 APL 기술을 사용하면 전력과 데이터를 단일 트위스트 페어로 최대 1km까지 전송할 수 있으며, 플랜트 소유자는 성능을 저하시키지 않고 Zone 1 및 Zone 2에 스마트 계측을 설치할 수 있습니다. 무선 노드는 배선 비용을 줄이고 가혹한 환경에서도 다년간의 배터리 수명을 실현하는 SmartPower 모듈에서 알 수 있듯이 리노베이션을 단순화합니다. 지하 광산은 이러한 장치를 채택하여 가스 수준과 장비 상태를 지상 운영 센터로 스트리밍하고 안전 조치를 일련의 정기 점검에서 지속적인 모니터링으로 전환합니다. 동일한 아키텍처가 예측 보전의 기반이 되고 에지 분석이 비정상적인 진동을 감지하고 고장이 발생하기 전에 서비스 요구를 알립니다. 이를 통해 시설 소유자는 컴플라이언스 보장과 생산성 향상을 동시에 실현하고 아시아태평양 및 걸프 협력 회의(GCC) 국가에서 구매를 가속화하고 있습니다.

인증 비용의 높이와 설계 복잡성

ATEX 인증을 받는 데는 1만 5,000-5만유로의 비용이 소요되며 IECex 시험에는 추가로 2만-6만달러가 추가로 소요되므로 중소기업은 경쟁에서 벗어날 수밖에 없습니다. 제7판 규칙의 변경은 추가 배터리 스트레스 테스트, 스파크 점화 테스트, 부품 간격 테스트를 필요로 하며, 종종 설계를 여러 번 수정해야 합니다. 또한 기업은 인증을 유지하기 위해 ISO 9001 및 QA 감사를 유지해야 하며 각 제품 라인에 정기적인 간접비가 내장되어 있습니다. 이 비용은 사내 연구소와 전임 컴플라이언스 팀을 보유한 다국적 기업에 경쟁을 치우치고 지적 재산을 집중시키고 신규 참가자를 막고 있습니다. 신흥 시장공급업체는 현지 연구소의 처리 능력이 부족하기 때문에 해외 시험을 강요하고 리드 타임이 길어지고 예산이 부풀어 오르기 때문에 가장 고전하고 있습니다.

부문 분석

2025년 시점에서 Zone 1 용도는 본질 안전 방폭 장비(IS 장비) 시장의 38.15%를 차지했으며, 보수작업 중에 폭발성 분위기가 발생하는 정유소나 화학플랜트에서의 보편성을 뒷받침했습니다. 예측 보전을 효율화하는 IoT 대응 신 디바이스와 종래 배선을 병용하는 운용 형태에 의해 존 1용 지출은 안정을 유지하고 있습니다. 반면 존 0은 8.31%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이는 가연성 가스가 지속적으로 존재하는 환경에서 인쇄형 센서나 무선 허브가 결국 실시간 감시를 가능하게 했기 때문입니다. 이러한 증가 추세는 특히 다운타임 비용이 장비 프리미엄을 초과하는 해저 유정 및 제약 반응기에서 격리에서 적극적인 위험 완화로의 사고 방식의 전환을 보여줍니다. 존 2는 저비용 컴플라이언스 솔루션을 필요로 하는 하역 도크 및 창고에서 여전히 중요성을 유지합니다. 한편, 분진 구역인 존 20-22는 자동화 투자를 진행하는 식품·제약 시설에서 완만한 수요 증가를 보이고 있습니다. 공급업체는 현재 펌웨어 전환 및 퓨즈 변경으로 여러 영역 요구사항을 충족하는 모듈형 보드를 개발하고 있으며, 이로 인해 개발 주기와 재고 압축이 이루어지고 있습니다.

존 1 인증 무선 게이트웨이는 단선 이더넷을 통해 안전 구역의 히스토리컬 시스템과 함께 작동할 수 있습니다. 이에 따라 본질 안전 방폭 장비(IS 장비) 시장 전체가 추가 케이블 트레이를 필요로 하지 않고 대응 가능한 엔드포인트를 확대하고 있습니다. 통합자는 복잡한 장벽 계산에 필요한 엔지니어 작업을 줄일 수 있다는 점에서 이러한 게이트웨이를 높이 평가합니다. 규격 책정 기관이 다가스·다분진 에리어용의 지침을 정밀화하는 가운데, 존 횡단 아키텍쳐는 설계상의 모범 사례로서 정착해, 현재의 개수 수요의 피크가 지나간 후에도 존 0용 출하가 2자리 성장을 유지하는 것이 확실시됩니다.

가스·증기 위험에 초점을 맞춘 클래스 1 시스템은 2025년 수익의 62.10%를 차지했고, 메탄 검지, 수소 누설 감시, LNG 취급에 의한 센서 갱신 수요를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 8.76%를 나타낼 전망입니다. 사업자는 파이프라인에 광학식 가스 이미징 카메라를 개장하여 현장에서 AI 기반의 누설 정량화를 실시하는 본질 안전 엣지 박스와 연동시킴으로써 수리 시간을 대폭 단축하고 있습니다. 클래스 2 분진 대책 기기는 미세 분진에 의한 발화 위험이 종래 간과되었던 바이오매스 발전소나 적층 조형 공장에서 새로운 구입처를 발견하고 있습니다. 더 많은 국가가 NFPA 652 표준을 준수하는 규제를 도입함에 따라 Class 2 본질 안전 방폭 장비(IS 장비) 시장 규모는 완만한 확대가 예상됩니다.

클래스 3의 용도는 섬유·목공 분야 등 틈새 상태가 계속됩니다만, 절단 라인의 자동화 진전에 수반하는 부유 섬유 발생에 의해 수요는 안정되고 있습니다. 공급업체는 개스킷 교환 및 분진 필터 추가를 통한 클래스 1 설계 재사용을 목표로 하여 시험 비용 절감을 도모하고 있습니다. 특히 이더넷 APL은 클래스 1에 유리합니다. 가스그룹은 분진보다 높은 허용전력이 인정되므로 스위치 도입이 단순화되기 때문입니다. 이 호환성에 의해 클래스 1은 새로운 본질 안전 네트워크 개념의 시험장으로서의 지위를 한층 더 굳혀, 나중에 분진·섬유 분야에 파급해 갑니다.

본질 안전 방폭 장비 보고서는 존별(존 0, 존 20, 존 1 등), 클래스별(클래스 1, 클래스 2, 클래스 3), 제품 유형별(센서, 검출기, 스위치 등), 최종 사용자별(석유 및 가스, 광업, 전력 및 유틸리티, 화학 및 석유화학, 가공·제조 등), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러) 기준으로 제공됩니다.

지역별 분석

북미는 2025년 수익의 38.20%를 차지했습니다. 이는 OSHA와 NFPA 규정이 셰일 분지, 멕시코 걸프 정유소, 지하 광산의 지속적인 현대화를 지원했기 때문입니다. 하니웰의 2024년 재편은 센싱 기술과 안전 기술이 단일 자동화 부서에 통합되어 주요 공급업체가 안전성과 생산성 요구를 모두 충족하는 통합 하드웨어 소프트웨어 스택을 제공하고자 함을 보여주었습니다. 미국 사업자는 노동력 부족에 대한 대책으로서 본질안전형 LTE/5G 게이트웨이 도입에도 주도적 입장에 있습니다.

아시아태평양은 2031년까지 8.55%라는 가장 빠른 CAGR를 나타낼 전망입니다. 이는 중국의 신규 정유소 건설, 인도의 석유화학 확장, 호주의 대규모 구리·리튬 채굴이 견인하고 있습니다. 각국 정부는 수출 허가를 IEC 또는 ATEX 준거와 연동시킴으로써 현지 제조업체를 인증 부품으로 유도하고 있습니다. 중국의 자동화 벤더는 유럽의 시험기관과 협력하여 인증 스케줄을 단축함으로써 지역공급업체 에코시스템을 확대하여 본질 안전 방폭 장비(IS 장비) 시장을 활성화하고 있습니다. 유럽에서는 ATEX 지침에 근거한 대규모의 기존 설비가 유지되고 있으며, EN IEC 60079-11 : 2024 규격이 2027년까지 의무화될 전망으로 설비 갱신이 가속될 것입니다. 독일은 첨단 화학 복합체를 주도하고 배출 목표 달성을 위해 존 너머 센서 네트워크를 통합하고 있습니다. 영국과 노르웨이는 북해 이행국이 정한 본질안전방폭과 사이버보안 양쪽의 규칙을 충족하는 해양 작업용 기기에 대한 투자를 계속하고 있습니다. 기타 지역에서는 중동의 국영석유회사(NOC)가 대규모 가스 프로젝트에서 본질안전형 SCADA 시스템의 갱신을 전개하는 한편, 브라질의 설탕·에탄올 증류소에서는 방폭 모터에서 본질안전형 가변 주파수 구동장치로 전환하여 에너지 사용량을 삭감하고 있습니다. 이러한 지역적인 동향이 함께 세계 수요는 견조하게 추이하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 세계의 방폭 안전 규제

- Industry 4.0이 견인하는 IS 센서 및 계측 기기에 대한 수요

- 석유 및 가스 및 광업활동 확대

- 방폭 구조의 비용 절감을 위해 Ex d에서 Ex i 아키텍처로의 전환

- 원격·예지 보전용 무선 IS 모듈의 성장

- 인쇄된 초저소비 전력 센서 어레이가 리노베이션 시장을 개척

- 시장 성장 억제요인

- 인증 비용의 높이와 설계의 복잡성

- 지역마다 다른 승인 스케줄

- IS 규격 인정이 끝난 전자 부품의 부족

- IS 무선 기기에서의 사이버 보안 대응 비용의 상승

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 존별

- 존 0

- 존 20

- 존 1

- 존 21

- 존 2

- 존 22

- 클래스별

- 클래스 1

- 클래스 2

- 클래스 3

- 제품 유형별

- 센서

- 검출기

- 스위치

- 송신기

- 절연기 및 배리어

- LED 표시등

- 기타 유형

- 최종 사용자별

- 석유 및 가스

- 광업

- 전력 및 유틸리티

- 화학 및 석유화학

- 가공 및 제조

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Pepperl Fuchs SE

- Honeywell International Inc.

- ABB Ltd.

- Siemens AG

- Eaton Corporation plc

- Schneider Electric SE

- R. Stahl AG

- BARTEC Top Holding GmbH

- Emerson Electric Co.

- Rockwell Automation Inc.

- MSA Safety Inc.

- Dragerwerk AG and Co. KGaA

- OMEGA Engineering(Spectris plc)

- Fluke Corporation(Fortive)

- Banner Engineering Corp.

- Extronics Ltd.

- CorDEX Instruments Ltd.

- Bayco Products Inc.

- Kyland Technology Co. Ltd.

- Georgin SAS

- ABB Measurement and Analytics(added sub-brand)

- Teledyne FLIR LLC

- PATLITE Corp.

- GM International srl

- RAE Systems by Honeywell

제7장 시장 기회와 향후 전망

KTH 26.01.20The intrinsically safe equipment market was valued at USD 3.88 billion in 2025 and estimated to grow from USD 4.16 billion in 2026 to reach USD 5.86 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031).

This expansion traces a shift from heavy flameproof housings toward digitally enabled, intrinsically safe architectures that blend regulatory compliance with Industry 4.0 connectivity. Demand accelerates as global standards tighten, mining and process industries expand, and wireless modules unlock retrofit projects once deemed uneconomic. Oil and gas operators remain the anchor customers, yet discrete manufacturers now adopt certified automation as volatile solvents enter production lines. Companies that master both certification and cybersecurity capture the most value as facility owners weigh lifecycle costs, supply-chain certainty, and predictive-maintenance capabilities when specifying new systems.

Global Intrinsically Safe Equipment (IS Equipment) Market Trends and Insights

Stringent Global Explosion-Safety Regulations

IEC 60079-11 Edition 7, released in January 2024, introduced 173 technical amendments, including tougher battery tests and a ban on catalytic sensors in Group IIC service, compelling retrofit spending across existing installations. EN IEC 60079-11:2024 entered the Official Journal in December 2024, and the prior 2012 edition will be de-harmonized by December 2027, which fixes a clear window for mandatory upgrades. Multinational plants juggle ATEX and IECEx paperwork that still lacks synchronized submission schedules despite technical alignment. The regulation also broadens scope beyond equipment to cover field wiring under IEC 60079-14:2024, stimulating demand for certified installation and recertification services. Together these actions boost the intrinsically safe equipment market as operators replace non-compliant assets and lock in long-term maintenance contracts tied to the new rules.

Industry 4.0-Driven Demand for IS Sensors and Instrumentation

Digital transformation raises the need for real-time data from hazardous zones, positioning intrinsically safe sensors as frontline enablers. Ethernet-APL now carries power and data on a single twisted pair up to 1 km, letting plant owners place smart instruments in Zone 1 and Zone 2 with no performance trade-off. Wireless nodes reduce cabling costs and simplify retrofits, as shown by SmartPower modules that support multi-year battery life in harsh areas. Underground mines adopt these devices to stream gas levels and equipment health to surface operations centers, shifting safety from periodic checks to continuous oversight. The same architecture underpins predictive maintenance, where edge analytics detect abnormal vibrations and flag service needs before breakdowns occur. Facility owners thus gain both compliance assurance and productivity improvements, accelerating purchases across Asia-Pacific and the Gulf Cooperation Council states.

High Certification Cost and Design Complexity

Gaining ATEX approval can cost EUR 15,000-50,000 per variant, and IECEx tests add USD 20,000-60,000, sums that push smaller firms out of contention. Edition 7 rule changes require additional battery stress, spark ignition, and component spacing tests, often driving multiple design revisions. Firms must also maintain ISO 9001 and QA audits to keep certificates active, embedding recurring overhead into each product line. The expense skews competition toward multinationals with in-house labs and dedicated compliance teams, concentrating intellectual property and deterring fresh entrants. Emerging-market suppliers struggle the most, as local labs lack throughput, forcing overseas testing that lengthens lead times and inflates budgets.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Oil and Gas and Mining Activities

- Cost-Saving Shift from Ex d to Ex i Architectures

- Shortage of Certified IS-Grade Electronic Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zone 1 applications commanded 38.15% of the intrinsically safe equipment market share in 2025, underscoring their ubiquity in refineries and chemical plants where explosive atmospheres arise during maintenance. Zone 1 spending remains steady as operators blend legacy wiring with new IoT-ready devices that streamline predictive maintenance. In contrast, Zone 0 displays a 8.31% CAGR as printed sensors and wireless hubs finally make real-time monitoring feasible where flammable gases persist continuously. This uptick signals a philosophical shift from isolation toward active risk mitigation, especially in subsea wells and pharmaceutical reactors where downtime costs outweigh device premiums. Zone 2 retains relevance for loading docks and warehouses needing inexpensive compliance solutions, while dust Zones 20-22 gain modest traction in food and pharma sites investing in automation. Suppliers now build modular boards that meet multiple zone requirements via firmware toggles and fuse changes, compressing development cycles and inventory.

Wireless gateways certified for Zone 1 now talk to safe-area historians over single-pair Ethernet. The broader intrinsically safe equipment market therefore enjoys expanded addressable endpoints without extra cable trays. Integrators value such gateways because they reduce engineer-hours on complex barrier calculations. As standards bodies refine guidance for multi-gas, multi-dust areas, zone-crossing architectures will cement themselves as design best practices, ensuring continued double-digit shipments into Zone 0 even after the current retrofit surge subsides.

Class 1 systems focused on gas and vapor hazards held 62.10% of 2025 revenue and are forecast to grow at a 8.76% CAGR through 2031 as methane detection, hydrogen leak monitoring, and LNG handling drive sensor upgrades. Operators retrofit pipelines with optical gas-imaging cameras linked to intrinsically safe edge boxes that perform AI-based leak quantification on site, slashing remediation time. Class 2 dust equipment finds new purchasers in biomass power plants and additive-manufacturing shops, where fine powders present ignition risks previously overlooked. The intrinsically safe equipment market size for Class 2 is projected to expand modestly as more countries adopt NFPA 652-style regulations.

Class 3 applications remain niche, serving textiles and woodworking, yet demand holds steady thanks to rising automation of cutting lines that create airborne fibers. Suppliers aim to reuse Class 1 designs by replacing gaskets and adding dust filters, saving test costs. Ethernet-APL especially benefits Class 1 because gas groups allow higher permissible power than dust, simplifying switch deployment. This compatibility further entrenches Class 1 as the proving ground for new intrinsically safe networking concepts that later trickle to dust and fiber sectors.

The Intrinsically Safe Equipment Report is Segmented by Zone (Zone 0, Zone 20, Zone 1, and More), Class (Class 1, Class 2, and Class 3), Product Type (Sensors, Detectors, Switches, and More), End User (Oil and Gas, Mining, Power and Utilities, Chemical and Petrochemical, Processing and Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 38.20% of 2025 revenue as OSHA and NFPA rules anchored continuous modernization across shale basins, Gulf Coast refineries, and underground mines. Honeywell's 2024 reorganization consolidated sensing and safety technologies into a single automation division, signaling that major suppliers aim to deliver unified hardware-software stacks that meet both safety and productivity needs. U.S. operators also lead in adopting intrinsically safe LTE/5G gateways, seeing the technology as a hedge against workforce shortages.

Asia-Pacific posts the fastest 8.55% CAGR through 2031, fueled by new refinery builds in China, petrochemical expansion in India, and large-scale copper and lithium mining in Australia. Governments link export licenses to IEC or ATEX compliance, steering local manufacturers toward certified components. Chinese automation vendors collaborate with European test houses to shorten certification schedules, enlarging the regional supplier ecosystem and boosting the intrinsically safe equipment market. Europe retains a sizable installed base under the ATEX directive, and EN IEC 60079-11:2024 will likely become mandatory by 2027, driving accelerated replacements. Germany leads in advanced chemical complexes, integrating Zone-crossing sensor networks to achieve emissions targets. The United Kingdom and Norway continue to invest in offshore intervention equipment that meets both intrinsic safety and cybersecurity rules dictated by the North Sea Transition Authority. Elsewhere, Middle East NOCs deploy intrinsically safe SCADA upgrades across large gas projects, while Brazilian sugar-ethanol distilleries switch from explosionproof motors to intrinsically safe variable-frequency drives that cut energy use. Collectively these regional narratives sustain robust global demand.

- Pepperl + Fuchs SE

- Honeywell International Inc.

- ABB Ltd.

- Siemens AG

- Eaton Corporation plc

- Schneider Electric SE

- R. Stahl AG

- BARTEC Top Holding GmbH

- Emerson Electric Co.

- Rockwell Automation Inc.

- MSA Safety Inc.

- Dragerwerk AG and Co. KGaA

- OMEGA Engineering (Spectris plc)

- Fluke Corporation (Fortive)

- Banner Engineering Corp.

- Extronics Ltd.

- CorDEX Instruments Ltd.

- Bayco Products Inc.

- Kyland Technology Co. Ltd.

- Georgin SAS

- ABB Measurement and Analytics (added sub-brand)

- Teledyne FLIR LLC

- PATLITE Corp.

- G.M. International srl

- RAE Systems by Honeywell

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent global explosion-safety regulations

- 4.2.2 Industry 4.0-driven demand for IS sensors and instrumentation

- 4.2.3 Expansion of oil and gas and mining activities

- 4.2.4 Cost-saving shift from Ex d to Ex i architectures

- 4.2.5 Growth of wireless IS modules for remote, predictive maintenance

- 4.2.6 Printed, ultra-low-power sensor arrays unlocking retrofit markets

- 4.3 Market Restraints

- 4.3.1 High certification cost and design complexity

- 4.3.2 Fragmented approval timelines across regions

- 4.3.3 Shortage of certified IS-grade electronic components

- 4.3.4 Rising cybersecurity-compliance cost for IS wireless devices

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Zone

- 5.1.1 Zone 0

- 5.1.2 Zone 20

- 5.1.3 Zone 1

- 5.1.4 Zone 21

- 5.1.5 Zone 2

- 5.1.6 Zone 22

- 5.2 By Class

- 5.2.1 Class 1

- 5.2.2 Class 2

- 5.2.3 Class 3

- 5.3 By Product Type

- 5.3.1 Sensors

- 5.3.2 Detectors

- 5.3.3 Switches

- 5.3.4 Transmitters

- 5.3.5 Isolators and Barriers

- 5.3.6 LED Indicators

- 5.3.7 Other Types

- 5.4 By End User

- 5.4.1 Oil and Gas

- 5.4.2 Mining

- 5.4.3 Power and Utilities

- 5.4.4 Chemical and Petrochemical

- 5.4.5 Processing and Manufacturing

- 5.4.6 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pepperl + Fuchs SE

- 6.4.2 Honeywell International Inc.

- 6.4.3 ABB Ltd.

- 6.4.4 Siemens AG

- 6.4.5 Eaton Corporation plc

- 6.4.6 Schneider Electric SE

- 6.4.7 R. Stahl AG

- 6.4.8 BARTEC Top Holding GmbH

- 6.4.9 Emerson Electric Co.

- 6.4.10 Rockwell Automation Inc.

- 6.4.11 MSA Safety Inc.

- 6.4.12 Dragerwerk AG and Co. KGaA

- 6.4.13 OMEGA Engineering (Spectris plc)

- 6.4.14 Fluke Corporation (Fortive)

- 6.4.15 Banner Engineering Corp.

- 6.4.16 Extronics Ltd.

- 6.4.17 CorDEX Instruments Ltd.

- 6.4.18 Bayco Products Inc.

- 6.4.19 Kyland Technology Co. Ltd.

- 6.4.20 Georgin SAS

- 6.4.21 ABB Measurement and Analytics (added sub-brand)

- 6.4.22 Teledyne FLIR LLC

- 6.4.23 PATLITE Corp.

- 6.4.24 G.M. International srl

- 6.4.25 RAE Systems by Honeywell

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment