|

시장보고서

상품코드

1907233

모발 재생 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hair Restoration Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

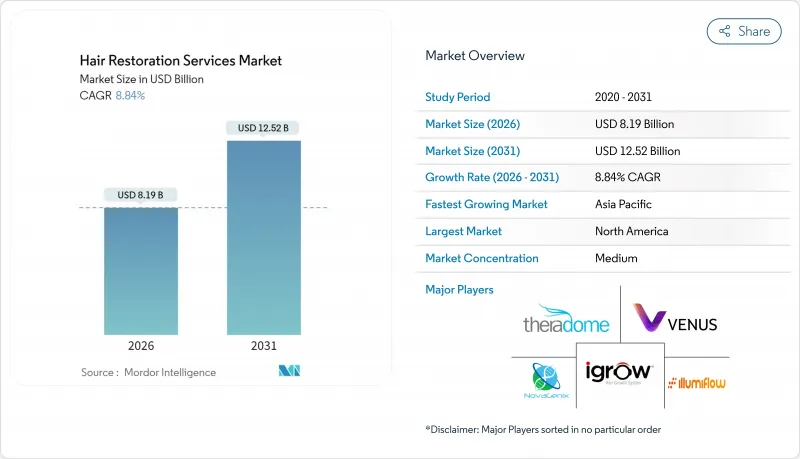

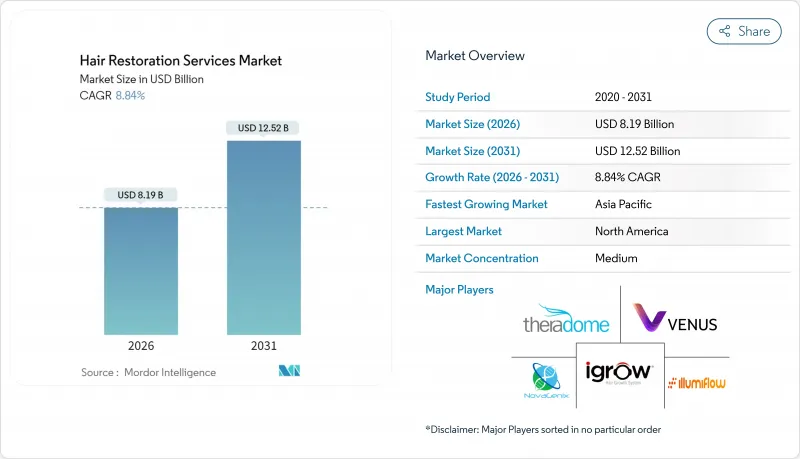

모발 재생 서비스 시장은 2025년 75억 3,000만 달러에서 2026년에는 81억 9,000만 달러로 성장해 2026년부터 2031년에 걸쳐 CAGR 8.84%를 나타낼 전망입니다. 2031년까지 125억 2,000만 달러에 달할 것으로 예측됩니다.

이러한 성장세는 퍼라주 퍼머슈티컬즈의 PP405와 같은 재생 의료 화합물의 임상적 성공, 44마이크론 해상도를 갖춘 ARTAS iXi 로봇과 같은 차세대 디바이스, 그리고 지속적이고 자신감을 높이는 결과를 인식하는 잠재 환자층의 확대에 의해 추진되고 있습니다. 사회적 수용의 확대, 인플루언서에 의한 인지도 향상, 유연한 지불 플랜에 의해 26-35세의 성인에 있어서 첫회 시술이 가속하고 있습니다. 한편, FoLix 분수 레이저 치료와 같은 장치 보조 요법은 수술을 원하지 않거나 적합하지 않은 소비자들에게 치료를 확대하고 있습니다. 의료 관광, 특히 튀르키예와 인도에 대한 수요가 병행하여 증가하여 비용 장벽 저하와 시술 건수 증가를 초래하고 있습니다. 한편, 두피냉각시스템에 대한 FDA의 ⅡⅡ 규제에서 볼 수 있는 지원적인 규제는 탈모증이 삶의 질과 관련된 문제로 제도적으로 인식되고 있음을 보여줍니다.

세계의 모발 재생 서비스 시장 동향과 인사이트

세계적으로 증가하는 탈모증 및 모발 손실 장애의 부담

남성형 탈모증은 현재 세계 성인의 최대 50%에 영향을 미치고 있으며 세대를 넘어 디히드로테스토스테론(DHT) 감수성이 높아짐에 따라 유병률이 증가하고 있습니다. 2024년에는 세계 70만건 이상의 모발 재생 처치가 실시되어 2016년 대비 16% 증가했으며, 미충족 요구를 부각했습니다. 26-35세의 젊은 환자층이 조기에 치료를 개시하는 경향이 있어, 평생에 걸친 시술 수요 증가와 유지 요법의 준수율 향상으로 이어지고 있습니다. 자가면역 관련 탈모증이나 화학요법에 의한 탈모증의 조사 확대에 의해 종래의 남성형 탈모증 이외의 환자층도 대상이 되고 있습니다. 고소득 국가에서 고령화됨에 따라 인지도 향상, 비용 효율성 및 접근성 향상으로 수요는 급격한 상승세를 유지하고 있습니다.

가처분 소득 증가와 미용 성형에 대한 지출 의욕

미국, 독일, 중국 및 걸프 협력 회의(GCC) 국가의 경제권에서는 가처분 소득이 증가함에 따라 건강 관리 비용이 미용 성형 서비스로 되돌아갑니다. 처음으로 식모 수술을 받는 환자의 평균 연령은 현재 26-35세이며, 이 연령에서는 수술이 보다 간단하고, 시간의 경과에 따라 뛰어난 밀도를 얻을 수 있습니다. 소비자 조사에 따르면 77%의 결정은 경력과 인간 관계를 동기로 하고 있으며, 풍부한 머리카락은 사회적 자본과 동등한 것으로 간주되고 있습니다. 할부 플랜, 무이자 클리닉 론, 후불 앱으로 중소득층에도 저렴한 가격대가 펼쳐집니다. 전 축구 선수 웨인 브릿지 씨가 7,000파운드(약 100만엔)의 시술을 받았다고 하는 유명인의 사례는 그 효과를 뒷받침해, 시술 비용을 일반적인 것으로 인식시키는 역할을 하고 있습니다.

고액의 시술비용과 한정적인 보험 적용 범위

선진 지역에서 4,000-1만 5,000달러의 수술 비용은 여전히 고액이며, 민간 보험사는 식모를 임의 수술로 분류하기 때문에 환자는 자기 부담을 강요받게 됩니다. 신흥 시장에서는 1인당 소득이 시술비용을 밑돌기 때문에 인지도가 높아지는 가운데 격차는 더욱 두드러집니다. 할부 플랜과 제3자 신용기관의 대출은 가격에 대한 저항감을 완화하지만 많은 잠재적인 환자는 치료를 늦추고 모낭의 미세화 위험을 높입니다. 의료 투어리즘은 비용 격차를 줄이지만 이동비가 가해지면 지역 내 환자에게 절약 효과가 상쇄될 수 있습니다. 한편, 저출력 레이저 캡과 같은 장비 기반 치료법이 1,000달러 미만으로 시장에 진입하고 가격에 민감한 소비자 입구를 제공하는 동시에 수술 치료 채널에서 일정한 수요를 빼앗고 있습니다.

부문 분석

두피 수술은 2025년 시점에서 모발 재생 서비스 시장의 87.02%를 차지했으며, 남성형 탈모증의 유병률의 높이와 확립된 수술 프로토콜을 반영했습니다. 소셜미디어의 미용 기준에 뒷받침된 눈썹 재생은 10.22%의 연평균 복합 성장률(CAGR)로 확대되어 기존 남성층을 넘어 클리닉 수익의 다양화가 예측됩니다. 수염 시술은 더 풍부한 얼굴 미학을 요구하는 밀레니얼 세대에 틈새 매력을 가지고 있지만, 속눈썹과 체모 시술은 기증자 머리 부족과 수술 복잡성에 의해 여전히 제한적입니다. 아프리카계 모질을 위해 설계된 로봇 직접 모발 이식(DHI) 기술은 기존 서비스가 충분하지 않은 층을 개척하여 조기 도입 클리닉의 경쟁 우위를 높입니다. 여성 환자의 인지도 향상과 고급 마이크로펀치 도구의 보급으로 다운타임과 흉터가 줄어들고 두피 수술의 핵심 지위가 강화됨과 동시에 고이익률의 안면 서비스 포트폴리오가 확대됩니다.

2차적 영향은 조달과 마케팅에 이릅니다. 눈썹과 수염의 잠재 고객을 위해 캠페인을 조정하는 클리닉은 핵심 두피 수요를 손상시키지 않으면서 추가 시술을 확보하고 모발 재생 서비스 시장 전체의 수익을 높여줍니다. 한편, 장비 제조업체는 섬세한 안면 영역에서의 외상을 최소화하기 위해 펀치 직경과 식모 펜의 최적화를 진행하고 있습니다. 규제 당국은 두피 이외의 시술용 인증 프로세스를 적응시켜 해부학적 차이가 있음에도 불구하고 표준화된 안전성을 확보하고 있습니다. 그 결과, 이식 부위의 다양화에 의해 제공업체는 두피 수요의 주기적인 변동의 영향을 완화할 수 있는 동시에, 모발 재생 서비스 시장의 총 잠재 규모를 확대하고 있습니다.

지역별 분석

2025년 시점에서 북미는 모발 재생 서비스 시장의 40.05%를 차지해 선두를 유지했습니다. 고소득층과 AI 지원 로봇 기술의 조기 도입이 견인 요인입니다. 미국에서는 보즐리 등의 클리닉이 프랙셔널 레이저나 엑소좀 추가 치료로 다각화하여 환자 1인당 수익 확대를 도모하고 있습니다. 캐나다에서는 의료기기 승인 과정이 유리하기 때문에 기타 국가에서는 이용할 수 없는 신기술을 요구하는 국경 간 환자의 유입이 촉진되고 있습니다. 보험 적용 범위의 부족은 남아 있는 것, 제3자 금융 및 고용주의 건강 수당이 비용 장벽을 완화하고 있습니다.

유럽은 성숙하면서도 혁신적인 시장입니다. 독일에서는 PRP(다혈소판 혈장)나 의료기기의 시술자에게 전문 자격을 의무화하여 품질 향상과 제공업체 수의 억제를 도모하고 있습니다. 환자 유동은 양방향으로 발생하고 있습니다. 비용 의식이 높은 독일인은 저가 FUE 시술을 위해 이스탄불로 여행하고, 걸프 지역 주민은 이식 + 필러 병용 패키지를 찾아 베를린으로 날아갑니다. 스마일 헤어 클리닉의 2025년 함부르크 진출은 유럽에서 프리미엄 수요에 대한 확신을 보여줍니다. EU의 광고 기준 감시는 투명성 있는 시술 결과의 주장을 보장하고, 모발 재생 서비스 시장에 대한 신뢰를 강화하고 있습니다.

아시아태평양은 CAGR 9.44%를 나타낼 것으로 예측되는 성장 엔진입니다. 중국에는 3,000개 이상의 이식 제공업체가 있지만, 소비자가 개인 관리 시설보다 브랜드 네트워크를 선호하는 경향으로 통합 압력이 높아지고 품질이 향상되었습니다. 인도는 영어로 원격 진료와 미국 가격의 1/4이라는 가격 설정을 살려 저렴한 가격을 요구하는 서양인을 매료하고 있습니다. 튀르키예는 지리적으로 유럽에 위치하고 있지만 아시아태평양, 중동 및 아프리카, 미국 고객에게 똑같이 서비스를 제공하고 있으며 지리적 경계를 넘어 전개를 보여줍니다. 이스탄불과 라고스에 도입된 아프리카계 헤어에 최적화된 로봇 기술은 서비스의 포섭성을 넓혀 의료관광으로서의 입지를 강화하고 있습니다. 태국과 한국의 정부기관은 현재 미용관광비자 발행을 추진하고 있으며, 모발재생을 국가의 의료 수출 전략에 공식적으로 통합하고 있습니다. 이러한 요인들이 함께 모발 재생 서비스 시장은 전통적인 서양 지역의 범위를 넘어 확장하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계적으로 증가하는 탈모증 및 탈모 장애의 부담

- 가처분 소득 증가와 미용 시술에의 지출 의욕의 고조

- 수술 및 비 수술 모발 재생 기술의 지속적인 기술 발전

- 전문적인 식모 클리닉 및 프랜차이즈 체인의 확대

- 비용 효율적인 시술을 요구하는 미용 목적의 해외 여행(코스메틱 투어리즘)의 수용 확대

- 소셜 미디어 마케팅 및 인플루언서 추천 확대

- 시장 성장 억제요인

- 고액의 시술 비용과 한정적인 보험 적용 범위

- 숙련된 식모 외과의의 부족

- 수술 후 위험과 성공률의 편차

- 저침습한 미용 대체 수단의 보급

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 이식 부위별

- 두피

- 수염 및 콧수염

- 눈썹

- 속눈썹

- 기타 신체 부위

- 시술 방법별

- 수술적 기법

- FUE(모낭 단위 추출술)

- FUT(모낭 단위 이식술)

- DHI(직접 모발 이식술)

- 로봇 FUE

- 비수술적 및 보조 치료법

- 저수준 레이저 치료(LLLT)

- 혈소판 풍부 플라즈마(PRP)

- 줄기세포 및 엑소좀 치료

- 국소 및 주사 보조제

- 수술적 기법

- 최종 사용자별

- 전문 헤어 클리닉

- 종합병원

- 외래 수술 센터(ASC)

- 메디컬 스파 및 웰니스 센터

- 기타 최종 사용자

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Aderans Co., Ltd.(HairClub)

- Bosley Inc.

- Venus Concept Inc.

- Bernstein Medical-Center for Hair Restoration

- The Cole Clinic

- Elite Hair Restoration

- Hairline International Hair & Skin Clinic

- Apira Sciences Inc.(iGrow)

- Lexington Intl. LLC(HairMax)

- Illumiflow

- National Hair Centers

- NovaGenix

- Theradome Inc.

- Restoration Robotics Inc.(ARTAS)

- Neograft Solutions

- Follica Inc.

- Advanced Hair Studio

- DHI Global Medical Group

- Eugenix Hair Sciences

- Sisram Medical(Alma Lasers)

- Solta Medical(Bausch Health)

제7장 시장 기회와 향후 전망

KTH 26.01.20The hair restoration services market is expected to grow from USD 7.53 billion in 2025 to USD 8.19 billion in 2026 and is forecast to reach USD 12.52 billion by 2031 at 8.84% CAGR over 2026-2031.

Momentum is driven by the clinical success of regenerative compounds such as Pelage Pharmaceuticals' PP405, next-generation devices like the ARTAS iXi robot with 44-micron resolution, and a widening pool of prospective patients aware of permanent, confidence-enhancing outcomes. Wider social acceptance, influencer visibility, and flexible payment plans are accelerating first-time procedures among adults aged 26-35, while device-based adjuncts such as FoLix fractional laser therapy extend care to consumers unwilling or unfit for surgery. Parallel growth in medical tourism, notably to Turkey and India, lowers cost barriers and adds volume, whereas supportive regulation-evident in the FDA's Class II rules for scalp-cooling systems-signals institutional recognition of hair loss as a quality-of-life issue.

Global Hair Restoration Services Market Trends and Insights

Growing Global Burden of Alopecia and Hair Loss Disorders

Androgenetic alopecia now afflicts up to 50% of adults worldwide, a prevalence climbing as dihydrotestosterone (DHT) sensitivity intensifies across generations. More than 700,000 hair restoration procedures were performed globally in 2024, up 16% from 2016, underscoring unmet clinical need. Younger patients aged 26-35 are acting earlier, generating higher lifetime procedure demand and improving compliance with maintenance regimens. Expanding research into autoimmune-related alopecia and chemotherapy-induced hair loss enlarges the candidate pool beyond traditional male pattern baldness. As populations age in high-income countries, awareness, affordability, and access combine to keep demand on a steep upward curve.

Rising Disposable Income and Willingness to Spend on Aesthetic Procedures

Disposable income growth in the United States, Germany, China, and Gulf Cooperation Council economies is steering healthcare dollars toward appearance-enhancing services. First-time transplant patients now average 26-35 years old, when surgery is simpler and yields superior density over time. Consumer surveys indicate 77% of decisions are career- or relationship-motivated, equating fuller hair with social capital. Financed payment plans, zero-interest clinic loans, and buy-now-pay-later apps expand affordability to middle-income cohorts. Celebrity stories such as former soccer player Wayne Bridge's GBP 7,000 procedure validate outcomes and normalize spending.

High Procedure Costs and Limited Reimbursement Coverage

Surgical outlays at USD 4,000-15,000 in developed regions remain prohibitive, while private insurers classify hair transplantation as elective, leaving patients to self-fund. The disparity is sharper in emerging markets where per-capita income trails procedure fees, even as awareness rises. Financing plans and third-party credit mitigate sticker shock, yet many prospects delay treatment, risking further follicular miniaturization. Medical tourism narrows cost gaps but adds travel costs that can offset savings for intra-regional patients. Meanwhile, device-based therapies such as low-level laser caps enter the market below USD 1,000, offering an entry point for price-sensitive consumers but diverting some volume from surgical channels.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Technological Advancements in Surgical and Non-Surgical Restoration

- Increasing Acceptance of Cosmetic Tourism for Cost-Effective Procedures

- Shortage of Skilled Hair Transplant Surgeons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Scalp procedures accounted for 87.02% of the Hair Restoration Services market in 2025, reflecting the prevalence of androgenetic alopecia and well-established surgical protocols. Eyebrow restoration, propelled by social media beauty standards, is forecast to expand at 10.22% CAGR and diversify clinic revenue beyond traditional male segments. Beard procedures hold niche appeal among millennials seeking a fuller facial aesthetic, while eyelash and body-hair work remains limited by donor-hair scarcity and surgical complexity. Robotic direct-hair-implantation (DHI) designed for Afro-textured follicles unlocks underserved demographic clusters, sharpening competitive positioning for clinics that adopt early. Growing awareness among female patients and advanced micropunch tools decrease downtime and scarring, reinforcing scalp surgery's centrality yet widening the portfolio of high-margin facial services.

Second-order impacts span procurement and marketing. Clinics tailoring campaigns to eyebrow and beard prospects secure incremental sessions without cannibalizing core scalp demand, lifting overall Hair Restoration Services market revenue. Device makers, meanwhile, are optimizing punch diameters and implanter pens to minimize trauma across delicate facial zones. Regulatory bodies are adapting certification pathways for non-scalp work, ensuring standardized safety despite anatomical variation. As a result, recipient-area diversification cushions providers against cyclical scalp demand swings while expanding total addressable Hair Restoration Services market.

The Hair Restoration Services Market Report is Segmented by Recipient Area (Scalp, Beard/Moustache, and More), Treatment (Surgical Techniques and Non-Surgical/Adjunct Therapies), End User (Specialty Hair Clinics, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 40.05% share of the Hair Restoration Services market in 2025, buoyed by high income and early adoption of AI-assisted robotics. U.S. clinics such as Bosley have diversified into fractional laser and exosome add-ons, deepening wallet share per patient. Canada's favorable medical-device approval pathway catalyzes cross-border patient inflow seeking newer technologies unavailable elsewhere. Reimbursement gaps persist, but third-party financing and employer wellness stipends soften cost obstacles.

Europe represents a mature yet innovative arena. Germany mandates specialized certification for PRP and device operators, raising quality while compressing provider counts. Patient flows run both ways: cost-conscious Germans travel to Istanbul for budget FUE, whereas Gulf residents fly to Berlin for combined transplant-plus-filler packages. Smile Hair Clinic's 2025 expansion into Hamburg signals confidence in premium European demand. EU vigilance on advertising standards ensures transparent outcome claims, bolstering trust in the Hair Restoration Services market.

Asia-Pacific is the growth engine with a 9.44% CAGR projection. China counts more than 3,000 transplant providers, yet consolidation pressures elevate quality as consumers favor branded networks over mom-and-pop rooms. India leverages English-language teleconsultations and pricing at one-quarter U.S. levels to draw Westerners chasing affordability. Turkey, though technically in Europe, serves APAC, MEA, and U.S. clients alike, illustrating geographic crossover. Afro-hair optimized robotics debuting in Istanbul and Lagos widen inclusion and fortify medical-tourism positioning. Government agencies in Thailand and South Korea now target cosmetic-tourism visas, formally integrating hair restoration into national health-export strategies. Collectively, these factors align to expand the Hair Restoration Services market beyond historical Western confines.

- Aderans Co., Ltd. (HairClub)

- Bosley Inc.

- Venus Concept Inc.

- Bernstein Medical - Center for Hair Restoration

- The Cole Clinic

- Elite Hair Restoration

- Hairline International Hair & Skin Clinic

- Apira Sciences Inc. (iGrow)

- Lexington Intl. LLC (HairMax)

- Illumiflow

- National Hair Centers

- NovaGenix

- Theradome Inc.

- Restoration Robotics Inc. (ARTAS)

- Neograft Solutions

- Follica Inc.

- Advanced Hair Studio

- DHI Global Medical Group

- Eugenix Hair Sciences

- Sisram Medical

- Solta Medical (Bausch Health)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Global Burden of Alopecia and Hair Loss Disorders

- 4.2.2 Rising Disposable Income and Willingness to Spend on Aesthetic Procedures

- 4.2.3 Continuous Technological Advancements in Surgical And Non-Surgical Hair Restoration

- 4.2.4 Expansion of Specialized Hair Transplant Clinics and Franchise Chains

- 4.2.5 Increasing Acceptance of Cosmetic Tourism for Cost-Effective Procedures

- 4.2.6 Proliferation of Social Media Marketing and Influencer Endorsements

- 4.3 Market Restraints

- 4.3.1 High Procedure Costs and Limited Reimbursement Coverage

- 4.3.2 Shortage of Skilled Hair Transplant Surgeons

- 4.3.3 Post-Operative Risks and Variable Success Rates

- 4.3.4 Availability of Less-Invasive Cosmetic Alternatives

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Recipient Area

- 5.1.1 Scalp

- 5.1.2 Beard / Moustache

- 5.1.3 Eyebrows

- 5.1.4 Eyelashes

- 5.1.5 Other Body Areas

- 5.2 By Treatment

- 5.2.1 Surgical Techniques

- 5.2.1.1 Follicular Unit Extraction (FUE)

- 5.2.1.2 Follicular Unit Transplant (FUT)

- 5.2.1.3 Direct Hair Implantation (DHI)

- 5.2.1.4 Robotic FUE

- 5.2.2 Non-Surgical / Adjunct Therapies

- 5.2.2.1 Low-Level Laser Therapy (LLLT)

- 5.2.2.2 Platelet-Rich Plasma (PRP)

- 5.2.2.3 Stem-Cell & Exosome Therapy

- 5.2.2.4 Topical & Injectable Adjuvants

- 5.2.1 Surgical Techniques

- 5.3 By End User

- 5.3.1 Specialty Hair Clinics

- 5.3.2 Multispecialty Hospitals

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Medical Spas & Wellness Centers

- 5.3.5 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Aderans Co., Ltd. (HairClub)

- 6.3.2 Bosley Inc.

- 6.3.3 Venus Concept Inc.

- 6.3.4 Bernstein Medical - Center for Hair Restoration

- 6.3.5 The Cole Clinic

- 6.3.6 Elite Hair Restoration

- 6.3.7 Hairline International Hair & Skin Clinic

- 6.3.8 Apira Sciences Inc. (iGrow)

- 6.3.9 Lexington Intl. LLC (HairMax)

- 6.3.10 Illumiflow

- 6.3.11 National Hair Centers

- 6.3.12 NovaGenix

- 6.3.13 Theradome Inc.

- 6.3.14 Restoration Robotics Inc. (ARTAS)

- 6.3.15 Neograft Solutions

- 6.3.16 Follica Inc.

- 6.3.17 Advanced Hair Studio

- 6.3.18 DHI Global Medical Group

- 6.3.19 Eugenix Hair Sciences

- 6.3.20 Sisram Medical (Alma Lasers)

- 6.3.21 Solta Medical (Bausch Health)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment