|

시장보고서

상품코드

1907243

유럽의 의료기기 포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Medical Devices Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

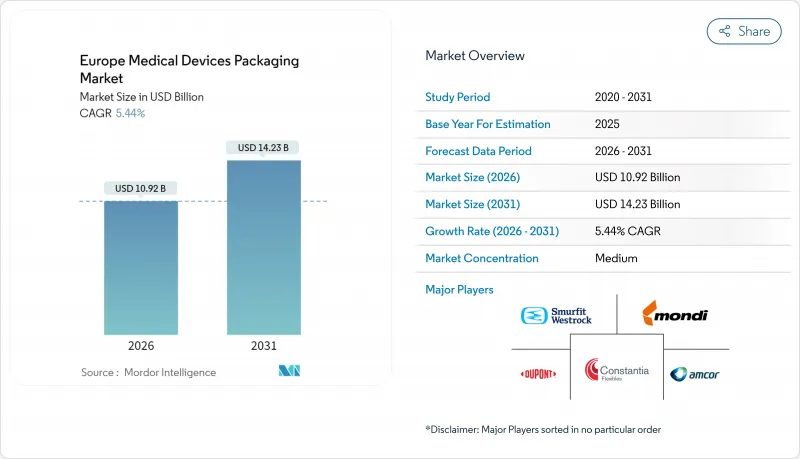

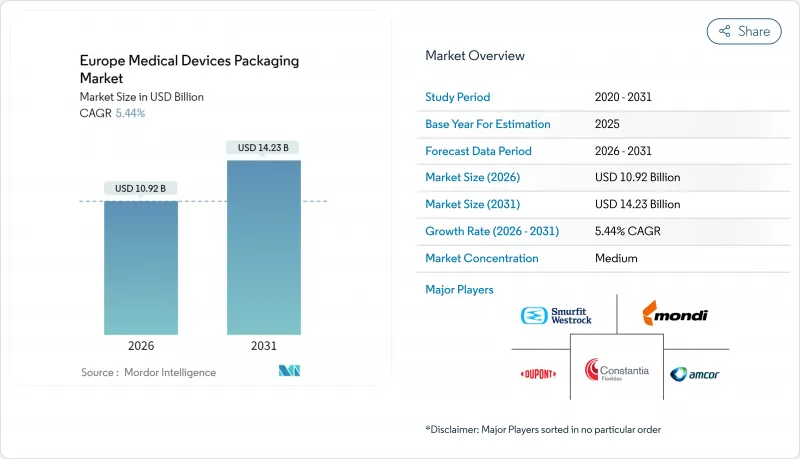

유럽의 의료기기 포장 시장 규모는 2026년에는 109억 2,000만 달러로 평가되었습니다.

이는 2025년 103억 6,000만 달러에서 성장한 수치이며, 2031년에는 142억 3,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 5.44%로 성장이 전망됩니다.

수요는 고유 의료기기 식별, 향상된 추적성, 일련번호 라벨링을 요구하는 엄격한 EU 의료기기 규정(MDR)에 의해 뒷받침됩니다. 제조사들이 EU 포장 및 포장 폐기물 규정에 부합함에 따라 스마트 라벨링, 멸균 장벽 혁신, 생물 기반 소재에 대한 투자는 지속적으로 증가하고 있습니다. 독일은 깊은 제조 역량을 통해 선두를 유지하는 반면, 스페인의 급속한 의료 디지털화는 시장 확장을 촉진합니다. 지속가능성 프로그램, 가정 의료 서비스 채택 증가, 기기 소형화가 유럽 의료기기 포장 시장의 기회를 종합적으로 확대하고 있으나, 폴리머 가격 변동성과 재활용 인프라 격차가 성장세를 제한하고 있습니다.

유럽의 의료기기 포장 시장 동향 및 인사이트

MDR 추적성 및 UDI 라벨링 요건

EU MDR 시행은 완전한 공급망 가시성을 확보하는 일련화, 스마트 라벨, 디지털 식별자 투자를 촉진합니다. 2028년까지 단계적으로 시행되는 유럽위원회의 UDI 도입 계획은 고해상도 포장 코드 및 인간이 판독 가능한 데이터에 대한 꾸준한 지출을 보장합니다. 독일의 변환업체들은 현재 UDI 데이터를 통합하고 약물 안정성을 유지하는 산소 차단 라벨을 적용하여 규제 요구사항과 성능 목표가 어떻게 수렴하는지 보여줍니다. 대형 기기 OEM 업체들은 ISO 13485 기준에 부합하는 품질 시스템을 갖춘 공급업체를 요구하며, 이는 전문 프린터 및 센서 라벨 혁신 기업들을 촉진합니다. 유럽 공장들은 리콜 위험을 줄이기 위해 클라우드 기반 추적 시스템도 활용합니다. 규정 준수 비용이 증가함에 따라, 유럽 의료기기 포장 시장에서 MDR(의료기기 규정) 준비 완료 패키징을 제공하는 벤더들은 경쟁 우위를 점하고 있습니다.

의료기기의 소형화 가속이 혁신적인 포장 형태를 주도

초소형 카테터 어셈블리와 이식형 기기에는 감마선, 증기 또는 아산화질소 멸균을 견디면서도 변형되지 않는 얇은 벽의 열성형 트레이가 필요합니다. 웨어러블 기기용으로 개발된 마이크로시스템 공구는 포장 분야로 효과적으로 이전되어 변환업체에게 형상 제어 유연성을 제공합니다. 바이오MEMS 연구는 무선 원격 측정 기능을 지원하면서 습기 보호 기능을 제공하는 생체 적합성 기판에 대한 수요를 보여줍니다. OEM 업체들은 혼합 키트 SKU를 처리하기 위해 중간 생산 과정에서 포켓 깊이를 교체하는 신속 변경 성형 라인을 활용합니다. 규제 기관은 이제 크기별 진동 및 낙하 테스트 프로토콜을 마련하여 재료 선택을 안내합니다. 이러한 압박 요인들이 복합적으로 작용하여 유럽 의료기기 포장 시장의 트레이 및 클램쉘 부문은 고부가가치 엔지니어링 솔루션으로 전환되고 있습니다.

엄격한 다층 EU 규정 및 규정 준수 비용

소규모 변환업체들은 중복 적용되는 MDR(의료기기 규정), 포장 폐기물 규정, 언어 라벨 지침에 직면하여 자본 집약적 검증과 다국어 아트워크를 요구받습니다. 인증 기관의 업무 적체로 인증서 갱신이 지연되어 리드 타임이 길어지고 운전 자본이 묶입니다. 기업들은 EUDAMED 제출 유지 관리를 위해 엔지니어를 배정하여 R&D 자원을 분산시킵니다. 높은 초기 문서화 부담은 아웃소싱을 촉진하지만, 파트너십 검증은 추가적인 복잡성을 더합니다. 이러한 장애물은 중소기업에 불균형적으로 영향을 미쳐 유럽 의료기기 포장 시장의 공급 확장을 제약합니다.

부문 분석

플라스틱은 확립된 멸균 호환성과 비용 효율성으로 수요가 높게 유지되며 2025년 유럽 의료기기 포장 시장 점유율의 63.68%를 차지했습니다. 예측 기간 동안 바이오 기반 폴리머는 EU의 지속가능성 목표와 MedEco 재생 가능 함유 수지와 같은 기술 발전을 반영하여 8.28%의 연평균 성장률(CAGR)을 기록할 것입니다. 판지는 2차 포장재로 확고한 위치를 유지하는 반면, 금속은 초저투과성이 필요한 이식용 기기에서 틈새 장벽 역할을 수행합니다.

제조업체 각사는 이제 전체 라인을 재인증하지 않고도 생물학적 원료를 공동 가공하는 이축 압출기를 운영하여 전환 위험을 완화하고 있습니다. 화학 재활용에 대한 투자는 의료용으로 사용 가능한 버진 등급 스티렌을 생산할 수 있는 파일럿 규모로 확대되고 있습니다. 이러한 진전은 생물학적 소재가 점진적으로 시장 점유율을 확대하여 유럽 의료기기 포장 시장 내 장기적인 소재 구성을 재편할 수 있는 기반을 마련합니다.

2025년 시점의 유럽의 의료기기 포장 시장 규모에서 파우치 및 백이 35.10%로 선두를 차지할 전망입니다. 이는 카테터 세트와 수술 키트 전반에 걸친 다용도성 덕분입니다. 마이크로 전자기기의 정밀한 캐비티 보호 수요 증가로 트레이 및 클램쉘 형식이 7.29%의 연평균 성장률(CAGR)로 다른 포맷을 앞지를 것입니다. 얇은 벽체 열성형 라인은 이제 적층 강도를 저하시키지 않으면서 수지 사용량을 60% 절감해 물류 비용을 축소합니다.

성형 캡 홈을 통합한 고투명 PETG 트레이는 에틸렌옥사이드 사이클 하에서 무균 무결성을 강화하고 캡 박리 현상을 제거합니다. 트레이 모서리에 내장된 스마트 센서는 온도 편차를 기록하여 MDR(의료기기 규정)의 시판 후 감시 규정에 부합합니다. 이러한 특성으로 심혈관 및 신경 기기 OEM 업체들 사이에서 트레이 채택이 촉진되며, 유럽 의료기기 포장 시장 전반의 성장을 지속시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유통기한 연장 포장 솔루션에 대한 수요 증가

- 가속화되는 기기 소형화로 인한 혁신적인 포장 형태

- EU 의료기기규칙(MDR)에 근거한 추적 가능성 및 UDI 표시 요건

- 가정용 및 원격 환자 모니터링 기기의 성장

- 재활용 가능 및 바이오 기반 포장 촉진하는 지속가능성 의무화

- 품질 향상 및 리콜 감소에 기여하는 AI 기반 인라인 검사

- 시장 성장 억제요인

- 엄격한 다층 EU 규정 및 준수 비용

- 폴리머 원료 가격의 변동성

- 다중 소재 멸균 포장재 재활용 인프라 부족

- 공급망 탄소 감축 목표에 따른 블리스터 사용 감소

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

- 거시경제적 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 소재별

- 플라스틱

- 종이 및 판지

- 금속

- 바이오 기반 폴리머

- 패키징 유형별

- 파우치 및 가방

- 트레이 및 크램쉘 용기

- 상자 및 판지

- 기타 포장 형태

- 용도별

- 멸균 포장

- 비멸균 포장

- 최종 사용자별

- 병원 및 진료소

- 재택치료 시설

- 진단센터 및 연구소

- 계약제조기관(CMO 및 CDMO)

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향(M&A, 생산 능력, 제휴 관계)

- 시장 점유율 분석

- 기업 프로파일

- Amcor plc

- Constantia Flexibles

- Klockner Pentaplast

- Smurfit WestRock

- DuPont de Nemours Inc.

- Tekni-Plex Inc.

- Wipak Group

- Nelipak Healthcare Packaging

- Technipaq Inc.

- Riverside Medical Packaging

- Gerresheimer AG

- Sealed Air Corporation

- Mondi Group

- Aptar Group Inc.

- Alpla Werke

- Nolato AB

- Huhtamaki Oyj

- SCHOTT AG

- Europlastec Group

- 주요 계약 포장업체 분석

- Wasdell Packaging Group

- Westfield Medical

- SteriPack Group

- Sky Medical

- Boomerang Distribution

- DaklaPack Group

- Dr. Muller Pharma

- Labo Phytophar

제7장 시장 기회와 장래의 전망

HBR 26.02.04Europe Medical Devices Packaging market size in 2026 is estimated at USD 10.92 billion, growing from 2025 value of USD 10.36 billion with 2031 projections showing USD 14.23 billion, growing at 5.44% CAGR over 2026-2031.

Demand is underpinned by strict EU Medical Device Regulation (MDR) requirements that push for unique device identification, higher traceability, and serialized labeling. Investments in smart labeling, sterile-barrier innovations, and bio-based materials continue to rise as manufacturers align with the EU Packaging and Packaging Waste Regulation. Germany keeps its lead through deep manufacturing capabilities, while Spain's rapid healthcare digitalization fuels expansion. Sustainability programs, growing home-healthcare adoption, and device miniaturization collectively amplify opportunities for the Europe Medical Devices Packaging market, even as polymer price volatility and recycling infrastructure gaps temper gains.

Europe Medical Devices Packaging Market Trends and Insights

MDR Traceability and UDI Labeling Requirements

EU MDR enforcement drives investment in serialization, smart labels, and digital identifiers that secure full supply-chain visibility. The Commission's phased UDI rollout through 2028 guarantees steady spending on high-resolution on-pack codes and human-readable data. German converters now embed oxygen-barrier labels that integrate UDI data and maintain drug stability, illustrating how regulatory needs and performance targets converge. Large device OEMs demand suppliers with ISO 13485-aligned quality systems, propelling specialized printers and sensor-label innovators. European plants also leverage cloud-based tracking to cut recall risk. As compliance costs climb, vendors offering turnkey MDR-ready packaging gain a competitive edge across the Europe Medical Devices Packaging market.

Accelerating Device Miniaturization Driving Innovative Pack Formats

Ultra-compact catheter assemblies and implantables require thin-wall thermoformed trays able to tolerate gamma, steam, or nitrogen-oxide sterilization without collapse. Microsystems tooling developed for wearables transfers effectively to packaging, giving converters flexibility in geometry control. Research on BioMEMS shows demand for biocompatible substrates that deliver moisture protection while supporting wireless telemetry. OEMs lean on quick-change forming lines that swap pocket depths mid-run to handle mixed kit SKUs. Regulatory bodies now draft size-specific vibration and drop-test protocols, guiding material selection. These pressures collectively push the trays and clamshells segment of the Europe Medical Devices Packaging market toward high-value engineering solutions.

Stringent Multi-layer EU Regulations and Compliance Costs

Small converters face overlapping MDR, Packaging Waste, and language-label directives that demand capital-intensive validation and multilingual artwork. Notified-body backlogs slow certificate renewals, stretching lead times and tying up working capital. Firms allocate engineers to maintain EUDAMED submissions, diverting resources from R&D. High upfront documentation burdens encourage outsourcing, yet partnership vetting adds further complexity. These hurdles disproportionately affect SMEs, restraining supply expansion in the Europe Medical Devices Packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Home-based and Remote Patient Monitoring Devices

- Sustainability Mandates Boosting Recyclable and Bio-based Packs

- Polymer Raw-material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastics retained 63.68% of Europe Medical Devices Packaging market share in 2025, as established sterilization compatibility and cost efficiency kept demand high. Over the forecast horizon, bio-based polymers will deliver 8.28% CAGR, reflecting EU sustainability goals and advancements such as MedEco renewable-content resins. Paperboard remains entrenched for secondary packs, while metals fill niche barrier roles in implantables needing ultra-low permeability.

Manufacturers now run twin-screw extruders that co-process bio-attributed feedstocks without requalifying entire lines, easing transition risks. Investments in chemical recycling scale pilot volumes capable of producing virgin-grade styrene for medical apps. These advances position bio-materials to capture incremental volumes, reshaping long-term material mix inside the Europe Medical Devices Packaging market.

Pouches and bags led with 35.10% Europe Medical Devices Packaging market size in 2025 due to versatility across catheter sets and surgical kits. Tray and clamshell formats will outpace others at 7.29% CAGR as micro-electronics push for precise cavity protection. Thin-wall thermoforming lines now achieve 60% resin savings without compromising stack strength, shrinking logistics costs.

High-clarity PETG trays that integrate molded lid channels enhance sterile integrity under ethylene-oxide cycles and eliminate lidding delamination. Smart sensors embedded in tray corners log temperature excursions, aligning with MDR post-market surveillance rules. These traits propel tray uptake among cardiovascular and neuro device OEMs, sustaining growth across the Europe Medical Devices Packaging market.

The Europe Medical Devices Packaging Market Report is Segmented by Material (Plastics, Paper and Paperboard, Metal, and Bio-Based Polymers), Packaging Type (Pouches and Bags, Trays and Clamshells, and More), Application (Sterile Packaging, Non-Sterile Packaging), End-User (Hospitals and Clinics, Home-Health Settings, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amcor plc

- Constantia Flexibles

- Klockner Pentaplast

- Smurfit WestRock

- DuPont de Nemours Inc.

- Tekni-Plex Inc.

- Wipak Group

- Nelipak Healthcare Packaging

- Technipaq Inc.

- Riverside Medical Packaging

- Gerresheimer AG

- Sealed Air Corporation

- Mondi Group

- Aptar Group Inc.

- Alpla Werke

- Nolato AB

- Huhtamaki Oyj

- SCHOTT AG

- Europlastec Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for longer shelf-life packaging solutions

- 4.2.2 Accelerating device miniaturisation driving innovative pack formats

- 4.2.3 EU MDR-driven traceability and UDI labelling requirements

- 4.2.4 Growth of home-based and remote patient monitoring devices

- 4.2.5 Sustainability mandates boosting recyclable and bio-based packs

- 4.2.6 AI-enabled inline inspection improving quality and reducing recalls

- 4.3 Market Restraints

- 4.3.1 Stringent multi-layer EU regulations and compliance costs

- 4.3.2 Volatility in polymer raw-material prices

- 4.3.3 Limited recycling infrastructure for multi-material sterile packs

- 4.3.4 Supply-chain carbon reduction targets shrinking blister use

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Plastics

- 5.1.2 Paper and Paperboard

- 5.1.3 Metal

- 5.1.4 Bio-based Polymers

- 5.2 By Packaging Type

- 5.2.1 Pouches and Bags

- 5.2.2 Trays and Clamshells

- 5.2.3 Boxes and Cartons

- 5.2.4 Other Packaging Type

- 5.3 By Application

- 5.3.1 Sterile Packaging

- 5.3.2 Non-Sterile Packaging

- 5.4 By End-User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Home-Health Settings

- 5.4.3 Diagnostic Centres and Laboratories

- 5.4.4 Contract Manufacturing Organisations (CMOs and CDMOs)

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Capacity, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor plc

- 6.4.2 Constantia Flexibles

- 6.4.3 Klockner Pentaplast

- 6.4.4 Smurfit WestRock

- 6.4.5 DuPont de Nemours Inc.

- 6.4.6 Tekni-Plex Inc.

- 6.4.7 Wipak Group

- 6.4.8 Nelipak Healthcare Packaging

- 6.4.9 Technipaq Inc.

- 6.4.10 Riverside Medical Packaging

- 6.4.11 Gerresheimer AG

- 6.4.12 Sealed Air Corporation

- 6.4.13 Mondi Group

- 6.4.14 Aptar Group Inc.

- 6.4.15 Alpla Werke

- 6.4.16 Nolato AB

- 6.4.17 Huhtamaki Oyj

- 6.4.18 SCHOTT AG

- 6.4.19 Europlastec Group

- 6.5 Analysis of Major Contract Packagers

- 6.5.1 Wasdell Packaging Group

- 6.5.2 Westfield Medical

- 6.5.3 SteriPack Group

- 6.5.4 Sky Medical

- 6.5.5 Boomerang Distribution

- 6.5.6 DaklaPack Group

- 6.5.7 Dr. Muller Pharma

- 6.5.8 Labo Phytophar

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment