|

시장보고서

상품코드

1907252

초분광 이미징 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hyperspectral Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

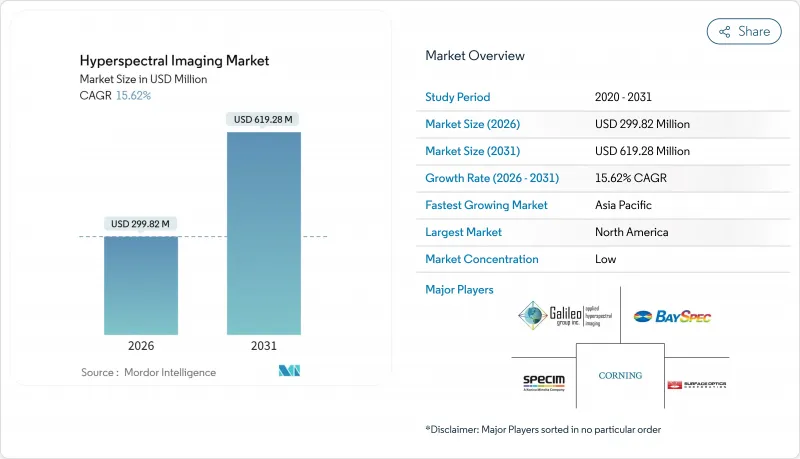

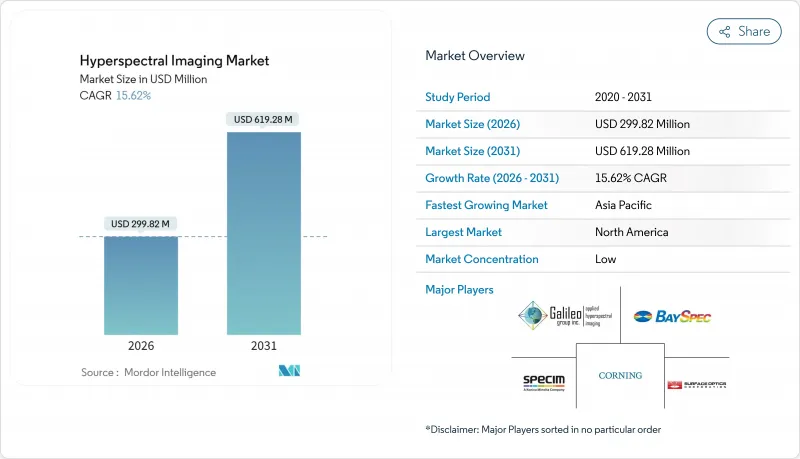

2026년 초분광 이미징 시장 규모는 2억 9,982만 달러로 추정되며, 2025년 2억 5,930만 달러에서 성장했으며, 2031년에는 6억 1,928만 달러에 이를 것으로 예상됩니다.

2026년부터 2031년까지는 CAGR 15.62%를 나타낼 것으로 전망됩니다.

이 확대는 VNIR/SWIR 센서 가격의 저하, 우주 탑재형 별자리에 관한 국방부의 계약 및 아시아태평양에서의 정책 지원을 받은 정밀 농업의 도입에 지지되고 있습니다. 공급업체는 현재 감지기 내에 머신러닝 가속기를 통합하여 현장 분석을 가능하게 하여 부피가 큰 워크스테이션을 필요로 하지 않으며 의사 결정 주기를 몇 밀리초로 단축하고 있습니다. 동시에 소형화된 스냅샷 카메라는 크기, 중량, 소비전력을 2자리 규모로 삭감하여 스마트폰 진단 등 민생 분야로의 전개를 가능하게 하고 있습니다. 미국 정부의 초분광 이미징(HSI) 미션을 위한 13억 달러를 넘는 프로그램 자금은 지속적인 수요를 보장함과 동시에 방어 등급 기술의 민생 분야에의 파급을 가속화하고 있습니다.

세계의 초분광 이미징 시장 동향과 인사이트

AI 기반 온칩 분석 통합

에지 신경망은 검출기 어레이에 직접 구현되어 실시간 처리량을 1.2Tb/s 이상으로 밀어 올리고 있습니다. 미국 육군의 HyperThreAD 프로그램은 무인 항공기 탑재 카메라로부터의 화학 위협 인식을 몇 초 안에 실현하고 있습니다. 이러한 진보는 지연을 줄이고 대역폭 부하를 줄이고 농업 선별기, 재활용 로봇 및 산업 공정 라인에서 자율적인 품질 판정을 가능하게 합니다. Imec사의 박막 필터 스택에 의해 CMOS 레벨의 제조가 가능해져, 단가를 낮추면서 프레임 레이트를 향상시킴으로써, 보다 폭넓은 상용 이용이 가속하고 있습니다. 그 결과, AI 대응 검출기는 물류, 광업, 식품안전 분야에서 차세대 자율 플랫폼의 핵심을 형성하는 태세가 갖추어지고 있습니다.

VNIR/SWIR 센서의 급속한 비용 절감

2024년 이후 InGaAs 웨이퍼 수율은 두 배가 되었고, 공유 백엔드 패키징 라인은 스마트폰 카메라의 경제성을 모방하여 평균 판매 가격을 연간 40% 가까이 밀어내렸습니다. 2027년까지 중급 CMOS 이미저와의 비용 패리티가 달성될 전망이며, 하이퍼스펙트럼 카메라는 많은 생산 라인에서 자본 지출에서 소모품으로 이행할 것입니다. 캘리포니아 대학 데이비스의 압축 센싱 프로토타입은 분광 충실도를 손상시키지 않고 광학계의 질량을 100분의 1로 삭감하고, 이 디플레이션 동향을 더욱 강화하고 있습니다. 가격이 하락함에 따라 초분광 이미징 시장은 자동차 페인트 검사, 전자기기 고장 분석 및 산업 계측 분야에서 기세를 늘리고 있습니다.

지속적인 캘리브레이션 드리프트

온도 변화, 진동 및 공기 중 오염 물질로 인해 에어컨이 없는 공장에서는 스펙트럼 정렬이 매달 2% 이상 저하됩니다. LED 기반 자체 교정 장치는 하이엔드 공중 페이로드의 불확실성을 5% 이내로 억제하지만 5만 달러의 가격으로 인해 그 사용은 고급 시스템으로 제한됩니다. 식품 선별 및 재활용 플랜트용 저가형 유닛은 여전히 주간 검증이 필요하며 작업 흐름을 방해하여 운영자의 신뢰성을 저하시키고 있습니다. 유저가 유지관리 프리의 가동 시간을 요구하는 가운데, 밀폐형 광학계, 온보드 기준 광원, 적응 알고리즘을 통합한 벤더가 점유율 획득의 호기를 맞이하고 있습니다.

부문 분석

2025년 카메라 부문은 초분광 이미징 시장의 50.40%를 차지했으며, 서비스 제공업체는 16.05%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장했습니다. 턴키 모델은 센서 렌탈, 비행 운영, 스펙트럼 분석을 패키징하여 최종 사용자가 가파른 학습 곡선을 피할 수 있도록 합니다. Headwall Photonics와 GRYFN의 제휴는 UAV 탑재 기기와 클라우드 네이티브 대시보드를 결합한 이 매니지드 서비스로의 전환을 구현하고 있습니다. 방위 및 광업 분야의 규제 감사는 인증 공급자의 지정이 강화되어 같은 부문의 성장을 뒷받침하고 있습니다. 시스템 통합자는 머신 비전 리노베이션을 위해 광학 시스템과 조명을 사용자 정의하여 수요를 유지합니다. 예를 들어 QinetiQ 미국사는 감시·환경 미션을 위한 스펙트럼 라이브러리를 구축하고, 다년간 계약에 의한 소프트웨어 갱신이나 데이터 서비스로 수익화를 도모하고 있습니다.

2025년 푸시블룸 스캐너는 장시간 노광 시간에 높은 SNR(신호 대 잡음비)으로 초분광 이미징 시장 점유율의 61.20%를 차지했습니다. 광업 조사와 위성 페이로드는 라인 스캔 방식의 균일한 조명과 스펙트럼 충실도에 의존합니다. 한편, 스냅샷 이미저는 16.35%의 연평균 복합 성장률(CAGR)을 기록해, 단일 프레임으로 완전한 데이터 큐브를 취득. 이것에 의해 농학 분야의 야외 조사나 의료 내시경 검사에 있어서, 핸드헬드 조작과 흔들림 없는 동작을 실현하고 있습니다.

하이브리드 기술 혁신의 일례로 Specim사의 FX 시리즈 열화상 푸시블룸 카메라는 중파장 범위의 커버 범위와 기계식 스캐닝을 조합하여 산업로와 플레어 감시에 활용되고 있습니다. 튜너블 필터 장치는 선택적인 파장대에서 충분한 화학물질 감지를 지원하는 반면, 위스크블룸 구조는 핀포인트 타겟팅이 요구되는 고도의 플랫폼에서 여전히 유용성을 유지하고 있습니다.

지역별 분석

2025년에 있어서 초분광 이미징 시장 규모에서는 북미가 37.50%로 선두를 차지했습니다. 이는 국방예산의 견조한 배분, 미국 국립위생연구소(NIH)의 의료 영상 보조금, 우주 분야의 듀얼 유스 기업에 대한 활발한 벤처 캐피탈 투자가 견인하고 있습니다. 연방정부의 5년간 영상계약은 안정적인 수익원을 보장하고, 실리콘밸리의 신흥기업은 2,400만 달러를 초과하는 시리즈 A 자금조달을 활용하여 저궤도 위성 별자리 구축을 진행하고 있습니다. 캐나다와의 북극권 감시에 있어서 국경 간 협력에 의해 센서 주문과 데이터 처리 서비스가 증가하고 있습니다.

아시아태평양은 16.6%의 연평균 복합 성장률(CAGR)로 가장 빠른 확대를 기록할 전망입니다. 중국의 디지털 빌리지 구상과 인도의 농업 기술 보조금 제도가 견인역이 되어, 모두 실시간의 작물 건강 상태 보고를 의무화하고 있습니다. 쑤저우, 신주쿠, 오사카를 중심으로 한 지역 반도체 클러스터는 리드 타임 단축과 비용 절감을 실현하여 현지 드론 통합 사업자가 1만 달러 미만으로 분광 페이로드를 번들 가능하게 하고 있습니다. 정부기관도 하천오염추적 및 희토류자원탐사용 HSI를 실지시험하고 있어 여러 해에 걸친 파이프라인의 가시성을 높이고 있습니다.

유럽에서는 순환형 경제 규제를 기반으로 한 균형 성장을 유지합니다. EU가 2030년까지 도시 쓰레기 재활용률 65% 달성을 목표로 하기 때문에 광학 선별기에 대한 안정된 수요가 발생할 것으로 예상됩니다. 한편, ESA 지원의 코페르니쿠스 계획 확대에 의해 하이퍼스펙트럼 위성 서비스가 자금 조달되고 있습니다. 독일은 산업 자동화를 추진, 프랑스는 포도밭의 병해 예측에 주력, 북유럽 국가는 목재 품질 등급에 HSI를 활용하고 있습니다. 지역 데이터 주권 규칙은 현지 클라우드 제공업체가 규정 준수 분석 스택을 제공하여 국내 가치 유지를 강화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- AI 기반 온칩 분석의 통합

- VNIR/SWIR 센서의 급속한 비용 저하

- 아시아태평양의 정밀 농업 프로그램 확대

- 우주 탑재형 HSI 콘스텔레이션에 대한 미국 방총성(DoD)/국방 고등 연구 계획국(DARPA)의 자금 제공

- 스마트폰 진단용 소형 스냅샷 HSI

- 필수 ESG 공개가 광물 등급 검증을 추진

- 시장 성장 억제요인

- 현장 배치 유닛의 지속적인 교정 드리프트

- 고액의 설비 투자 비용 및 데이터 보존 비용

- 미국과 중국의 센서 코어에 관한 수출 관리 체제

- 특정 분야용 스펙트럼 라이브러리의 부족

- 특허 분석

- 기술 개요 - 응용 분야

- 감시

- 원격 감지

- 머신 비전 및 광학

- 의료 진단 및 연구

- 업계 밸류체인 분석

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 거시 경제 동향 평가

제5장 시장 규모와 성장 예측

- 제공별

- 카메라

- 시스템 통합업체

- 서비스 제공업체

- 기술별

- 푸시블룸

- 스냅샷

- 튜너블 필터

- 이미징 FTIR

- 위스크 브룸

- 파장별

- 가시광선 및 근적외선(NIR)

- 단파장 적외선(SWIR)

- 중파장 적외선(MWIR)

- 장파장 적외선(LWIR)

- 최종 사용자 업계별

- 식품 및 농업

- 헬스케어

- 국방

- 광업 및 계측

- 재활용

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Galileo Group, Inc.

- BaySpec Inc.

- Specim Spectral Imaging Ltd

- Corning Incorporated

- Surface Optics Corporation

- Headwall Photonics Inc.

- Resonon Inc.

- HyperMed Imaging Inc.

- Norsk Elektro Optikk AS

- Cubert GmbH

- XIMEA GmbH

- HinaLea Imaging(TruTag Technologies Inc.)

- ITRES Research Limited

- Telops Inc.

- Brimrose Corporation of America

- Teledyne DALSA Inc.

- ClydeHSI Ltd.

- ChemImage Corporation

- Diaspective Vision GmbH

- Applied Spectral Imaging Inc.

제7장 시장 기회와 향후 전망

KTH 26.01.20The hyperspectral imaging market size in 2026 is estimated at USD 299.82 million, growing from 2025 value of USD 259.30 million with 2031 projections showing USD 619.28 million, growing at 15.62% CAGR over 2026-2031.

This expansion rests on falling VNIR/SWIR sensor prices, Defense Department contracts for space-borne constellations, and policy-backed precision-agriculture roll-outs across Asia Pacific. Vendors now embed machine-learning accelerators inside detectors, enabling in-field analytics that eliminate bulky workstations and shorten decision cycles to milliseconds. At the same time, miniaturized snapshot cameras shrink size, weight, and power by two orders of magnitude, opening consumer channels such as smartphone diagnostics. Program funding that exceeds USD 1.3 billion for U.S. government HSI missions guarantees recurring demand and accelerates spillover of defense-grade technology into civilian applications.

Global Hyperspectral Imaging Market Trends and Insights

Integration of AI-based on-chip analytics

Edge neural networks now reside directly on detector arrays, pushing real-time throughput beyond 1.2 Tb/s. The U.S. Army's HyperThreAD program demonstrates chemical threat recognition in seconds from UAV-borne cameras. These advances cut latency, reduce bandwidth loads, and enable autonomous quality decisions in agricultural sorters, recycling robots, and industrial process lines. Broader commercial use is accelerating as thin-film filter stacks from Imec allow CMOS-level manufacturing, dropping unit costs while raising frame rates. As a result, AI-enabled detectors are poised to form the core of next-generation autonomous platforms in logistics, mining, and food safety.

Rapid cost erosion of VNIR/SWIR sensors

InGaAs wafer yields have doubled since 2024, and shared back-end packaging lines now mimic smartphone camera economics, pushing average selling prices down nearly 40% per year. Cost parity with mid-range CMOS imagers is expected by 2027, moving hyperspectral cameras from capital expense to consumable tool in many production lines. UC Davis compressive-sensing prototypes cut optics mass by 100X without spectral fidelity loss, reinforcing this deflationary trend. As prices retreat, the hyperspectral imaging market gains traction in automotive paint inspection, electronics failure analysis, and industrial metrology.

Persistent calibration drift

Temperature swings, vibration, and airborne contaminants degrade spectral alignment by more than 2% per month in unconditioned factories. While LED-based self-calibrators keep high-end airborne payloads within 5% uncertainty, their USD 50,000 price tag restricts use to premium systems. Budget units in food sorting and recycling plants still require weekly validation, disrupting workflows and lowering confidence among operators. Vendors that integrate sealed optics, on-board references, and adaptive algorithms are positioned to capture share as users seek maintenance-free uptime.

Other drivers and restraints analyzed in the detailed report include:

- Expanding precision-agriculture programs in APAC

- DoD/DARPA funding for space-borne hyperspectral constellations

- High CAPEX and data-storage costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cameras segment captured 50.40% of the hyperspectral imaging market share in 2025, while service providers grew the fastest at a 16.05% CAGR. Turnkey models bundle sensor rental, flight operations, and spectral analytics, sparing end-users from steep learning curves. Headwall Photonics' alliance with GRYFN exemplifies this managed-service pivot, pairing UAV payloads with cloud-native dashboards. Regulatory audits in defense and mining increasingly stipulate certified providers, reinforcing the segment's momentum. System integrators sustain demand by customizing optics and illumination for machine-vision retrofits. QinetiQ US, for instance, curates spectral libraries for surveillance and environmental missions, monetizing software updates and data services over multiyear contracts

Pushbroom scanners captured 61.20% of hyperspectral imaging market share in 2025 thanks to high SNR across long dwell times. Mining surveys and satellite payloads rely on the line-scan method's uniform illumination and spectral fidelity. Snapshot imagers, however, posted a 16.35% CAGR, capturing full data cubes in a single frame and enabling handheld, jitter-free operation for field agronomy and medical endoscopy.

Hybrid innovations such as Specim's FX-series thermal pushbroom camera marry mid-wave coverage with mechanical scanning to serve industrial furnaces and flare monitoring. Tunable-filter rigs address chemical sensing where selective bands suffice, while whiskbroom architectures retain relevance on high-altitude platforms demanding pinpoint targeting.

The Hyperspectral Imaging Market Report is Segmented by Offering (Cameras, System Integrator, and Service Provider), Technology (Pushbroom, Snapshot, Tunable Filter, and More), Wavelength (Visible and NIR, SWIR, MWIR, and More), End-User Industry (Food and Agriculture, Healthcare, Defense, Mining and Metrology and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 37.50% hyperspectral imaging market size in 2025, driven by strong defense allocations, NIH-funded medical imaging grants, and robust venture capital for dual-use space companies. Federal five-year imagery contracts guarantee steady revenue streams, while Silicon Valley startups tap USD 24 million-plus Series A rounds to build low-Earth-orbit constellations. Cross-border collaboration with Canada on Arctic monitoring generates incremental sensor orders and data-processing services.

Asia Pacific posts the fastest expansion at 16.6% CAGR, propelled by China's Digital Village Initiative and India's agri-tech subsidies, both mandating real-time crop-health reporting. Regional semiconductor clusters around Suzhou, Hsinchu, and Osaka shorten lead times and compress costs, letting local drone integrators bundle spectral payloads below USD 10,000. Governments also field-test HSI for river-pollution tracking and rare-earth exploration, adding multi-year pipeline visibility.

Europe maintains balanced growth anchored in circular-economy regulations. The EU target of 65% municipal-waste recycling by 2030 creates a stable pull for optical sorters, while ESA-backed Copernicus expansion funds hyperspectral satellite services. Germany champions industrial automation, France focuses on vineyard disease prediction, and Nordic countries leverage HSI for timber-quality grading. Regional data-sovereignty rules stimulate local cloud providers to offer compliant analytics stacks, reinforcing domestic value retention.

- Galileo Group, Inc.

- BaySpec Inc.

- Specim Spectral Imaging Ltd

- Corning Incorporated

- Surface Optics Corporation

- Headwall Photonics Inc.

- Resonon Inc.

- HyperMed Imaging Inc.

- Norsk Elektro Optikk AS

- Cubert GmbH

- XIMEA GmbH

- HinaLea Imaging (TruTag Technologies Inc.)

- ITRES Research Limited

- Telops Inc.

- Brimrose Corporation of America

- Teledyne DALSA Inc.

- ClydeHSI Ltd.

- ChemImage Corporation

- Diaspective Vision GmbH

- Applied Spectral Imaging Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of AI-based on-chip analytics

- 4.2.2 Rapid cost erosion of VNIR/SWIR sensors

- 4.2.3 Expanding precision-agriculture programs in APAC

- 4.2.4 DoD/DARPA funding for space-borne HSI constellations

- 4.2.5 Miniaturized snapshot HSI for smartphone diagnostics

- 4.2.6 Mandatory ESG disclosure driving mineral-grade verification

- 4.3 Market Restraints

- 4.3.1 Persistent calibration drift in field-deployable units

- 4.3.2 High CAPEX and data-storage costs

- 4.3.3 US-China export-control regimes on sensor cores

- 4.3.4 Scarcity of domain-specific spectral libraries

- 4.4 Patent Analysis

- 4.5 Technology Snapshot - Applications

- 4.5.1 Surveillance

- 4.5.2 Remote Sensing

- 4.5.3 Machine Vision/Optical

- 4.5.4 Medical Diagnostics/Research

- 4.6 Industry Value Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Assessment of Macro-economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Cameras

- 5.1.2 System Integrator

- 5.1.3 Service Provider

- 5.2 By Technology

- 5.2.1 Pushbroom

- 5.2.2 Snapshot

- 5.2.3 Tunable Filter

- 5.2.4 Imaging FTIR

- 5.2.5 Whiskbroom

- 5.3 By Wavelength

- 5.3.1 Visible and NIR (Near-Infrared)

- 5.3.2 SWIR (Short-Wave Infrared)

- 5.3.3 MWIR (Mid-Wave Infrared)

- 5.3.4 LWIR (Long-Wave Infrared)

- 5.4 By End-user Industry

- 5.4.1 Food and Agriculture

- 5.4.2 Healthcare

- 5.4.3 Defense

- 5.4.4 Mining and Metrology

- 5.4.5 Recycling

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Galileo Group, Inc.

- 6.4.2 BaySpec Inc.

- 6.4.3 Specim Spectral Imaging Ltd

- 6.4.4 Corning Incorporated

- 6.4.5 Surface Optics Corporation

- 6.4.6 Headwall Photonics Inc.

- 6.4.7 Resonon Inc.

- 6.4.8 HyperMed Imaging Inc.

- 6.4.9 Norsk Elektro Optikk AS

- 6.4.10 Cubert GmbH

- 6.4.11 XIMEA GmbH

- 6.4.12 HinaLea Imaging (TruTag Technologies Inc.)

- 6.4.13 ITRES Research Limited

- 6.4.14 Telops Inc.

- 6.4.15 Brimrose Corporation of America

- 6.4.16 Teledyne DALSA Inc.

- 6.4.17 ClydeHSI Ltd.

- 6.4.18 ChemImage Corporation

- 6.4.19 Diaspective Vision GmbH

- 6.4.20 Applied Spectral Imaging Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment