|

시장보고서

상품코드

1907258

이소시아네이트 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Isocyanates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

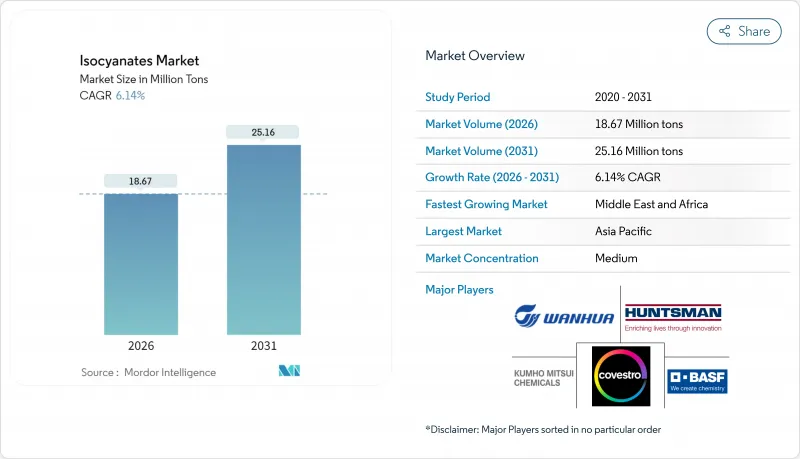

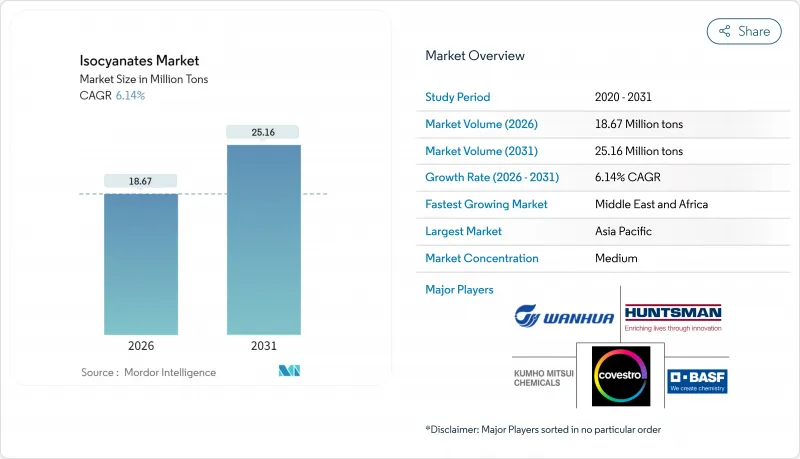

이소시아네이트 시장 규모는 2026년 1,867만 톤으로 추정되며, 2025년 1,759만 톤에서 성장할 전망입니다. 2031년에는 2,516만 톤에 달할 것으로 예측되며, 2026-2031년 CAGR 6.14%로 확대될 전망입니다.

이 성장 궤적은 고성능 폴리우레탄 시스템의 채택 확대, 공급측 통합 및 수직 통합 생산자에게 유리한 환경 규제 강화를 반영합니다. 단열 기준의 인상에 따라 경질 폼 수요는 견조하게 추이해 자동차의 경량화에 의해 건설 용도 이외의 전문적인 수요도 확대되고 있습니다. 통합된 원료 전략, 무역 정책 전환, 고급 지방족 화학으로의 전환은 이소시아네이트 시장에서 경쟁적 위치를 더욱 형성하고 있습니다.

세계의 이소시아네이트 시장 동향 및 인사이트

건축 단열재에서 경질 PU 폼 수요 급증

2024년 국제건축기준의 개정에 의해 가연성 단열재를 포함한 외벽조립구조물에는 NFPA 285 화재 시험이 의무화되어 입증된 이소시아네이트계 시스템이 설계자에게 있어서 저위험적인 선택지가 되고 있습니다. 폴리이소시아누레이트 보드는 열전도율이 0.018 W/m*K로 매우 낮고, 공간이 제한된 개수 현장에 있어서, 광물 울에 비해 보다 얇은 벽 조립 구조를 실현합니다. 주 에너지 기준에서는 ASHRAE 90.1의 인용이 증가하고 있으며, 건설업자에게 기존의 건축 외피 내에서 경질 폴리우레탄이 달성 가능한 고단열 성능(R값)이 요구되고 있습니다. 이 때문에 기존 건축물의 넷 제로 목표 달성을 위한 개수 수요가 이소시아네이트 시장을 뒷받침하고 있습니다. 또한, 세계의 녹색 빌딩 인증 제도에서는 확립된 라이프사이클 데이터를 가지는 재료가 우월하기 때문에 MDI계 폼은 추가적인 적합성면에서 우위성을 가지고 있습니다.

아시아태평양의 급속한 산업화 및 도시화

동남아시아 국가들은 중국 이외의 제조 거점을 확대하고 있으며, MDI와 TDI에 대한 새로운 역내 수요를 창출하고 있습니다. 베트남, 태국, 인도네시아에 생산 기지가 있는 제조업체는 증가하는 현지 소비에 대응하면서 지정학적 요인으로 인한 공급망 위험을 줄일 수 있습니다. 동소 베트남의 연간 130,000톤의 MDI 플랜트는 이 다양화 전략의 좋은 예입니다. ASEAN 전역의 대규모 도시 주택 및 교통 프로젝트는 단열재, 실란트, 복합 패널 수요를 견인하고 있으며, 모두 이소시아네이트 화학에 의존하고 있습니다. 소득 수준이 증가함에 따라 내구 소비재(특히 매트리스 및 가전제품)의 소비가 유연성 폼의 안정적인 수요를 촉진하고 있습니다. 이러한 구조적 변화로 인해 이소시아네이트 시장은 다른 지역의 수출 감속에도 불구하고 다년간의 성장 궤도를 유지하고 있습니다.

벤젠 및 니트로 벤젠의 원료 가격 변동

벤젠은 MDI와 TDI 모두에 대한 주요 방향족 전구체이기 때문에 원유 연동형 나프타 가격의 급등은 이소시아네이트 제조 비용에 직접 파급됩니다. 아시아의 스팟 벤젠 가격은 난고 하락하여 생산자는 월간 가격 조정 조항을 발동하지 않을 수 없어 구매자의 가시성을 해치는 결과가 되었습니다. 방향족 원료와의 소급적 연계가 없는 비통합형 컨버터 기업에서는 마진 압축이 가장 빨리 진행되고 수직 통합 및 장기 오프 테이크 계약의 체결이 촉진되고 있습니다. 재고 전략은 변동을 완화하기 위해 최소 3개월 수요를 다루는 헤지 포지션으로 진화하고 있지만, 이로 인해 운전 자금이 구속되어 보유 비용이 증가합니다. 그 결과, 원료 가격의 동향이 불투명한 경우, 배합 제조업체가 주문을 지연시키기 때문에 단기적인 소비 성장에 억제 효과가 발생하고 있습니다.

부문 분석

MDI는 2025년 시점에서 이소시아네이트 시장에서 58.75%의 점유율을 차지했으며, 이는 고 수요의 건설 및 산업 용도용 경질 발포체 및 복합재료 배합에 있어서의 범용성이 배경에 있습니다. 한편, 지방족 이소시아네이트는 6.72%의 연평균 복합 성장률(CAGR)로 성장하고 있으며, 이는 이소시아네이트 시장 전체를 능가하는 속도입니다. 자외선 안정성의 HDI 및 IPDI는 장기 내구성이 프리미엄 가격을 요구하는 자동차 클리어 코트 및 풍력 터빈 블레이드 수지 시스템에 침투하고 있습니다. TDI 수요는 침구 및 가구 분야에서 견조를 유지하고 있지만, 부문이 성숙기에 이르고, 점탄성 MDI 시스템으로부터의 경쟁 압력이 강해지는 가운데, 성장은 둔화하고 있습니다. 특수 블록화 및 프리폴리머 변종은 생산량이 적은 반면, 전자기기 봉지, 선박용 도료, 항공우주용 복합재를 타겟으로 함으로써 높은 이익률을 제공합니다.

지방족 등급의 이소시아네이트 시장 규모는 자동차 및 신재생 에너지 분야의 OEM 사양이 방향족 화학제품에서는 달성하기 어려운 내구성 지표로 이행함에 따라 꾸준히 확대될 전망입니다. 생산자들은 북미와 유럽의 지역 조달 규제를 추구하고 하류의 폴리이소시아네이트 생산을 위한 공급망 단축을 위해 HDI 단량체 제조 라인의 추가 투자를 추진하고 있습니다. 한편, MDI 공급업체는 비용 우위성을 유지하기 위해 병목 현상 해소를 위한 증산을 진행하고 있으며, 범용품의 규모와 특수품에 의한 부가가치 창출의 밸런스를 취하는 2개립 투자 전략이 부각되고 있습니다.

이소시아네이트 시장 보고서는 유형별(MDI, TDI, 지방족계, 기타), 용도별(경질 폼, 연질 폼, 페인트 및 코팅, 접착제 및 실란트 등), 최종 사용자 산업별(건축 및 건설, 자동차, 의료, 가구, 기타 최종 사용자), 지역별(아시아태평양, 북미, 유럽 등)으로 분석되고 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

2025년 아시아태평양은 이소시아네이트 시장 점유율의 46.85%를 차지했습니다. 이 우위는 중국의 벤젠 우위를 가진 MDI 복합 시설 및 동남아시아의 신흥 제조 거점(지역 컨버터에의 납기 단축을 실현)에 의해 확보되고 있습니다. 보다 엄격한 배출 규제 하에서 중국 중소공장의 통합은 환경 목표를 달성하면서 규모의 경제를 활용할 수 있는 대규모 사업자에게 생산량을 집중시키고 있습니다. 베트남과 인도네시아의 하류 클러스터도 경질 발포체와 신발 생산을 확대하여 수출 변동에 민감한 자율적인 수요 순환을 강화하고 있습니다.

북미는 셰일가스 우위성의 원료 공급과 폴리우레탄 소비를 지지하는 자동차 및 건설 분야에 대한 근접성으로부터 중요한 지위를 차지하고 있습니다. BASF가 루이지애나주 가이스마에서 진행하는 확장에 의해 2026년에는 지역의 MDI 명목 생산 능력이 연간 약 60만 톤에 달하고, 전기차 생산 확대에 수반하는 공급 만족이 확보됩니다. 2025년 미국 국제무역위원회(USITC)가 중국의 MDI를 대상으로 실시한 덤핑조사로 대표되는 무역정책의 불확실성은 이중조달을 촉진하고 국내 플랜트의 가동률을 뒷받침하고 있습니다. 유럽은 기술적으로 선진적인 반면, REACH 규제 대응 비용이 중소 컨버터를 해외 조달로 향하고 있으며, 단열 개수 수요가 계속됨에도 불구하고 지역의 성장 전망을 약간 둔화시키고 있습니다.

중동 및 아프리카는 2031년까지 연평균 6.25%의 연평균 복합 성장률(CAGR)로 이 지역에서 가장 급속한 확대가 예상됩니다. 국영 기업은 저비용 프로판 탈수소 및 벤젠 추출 기술을 활용하여 MDI 및 TDI 통합 유닛에 원료를 공급하고 있습니다. 특히 걸프협력회의(GCC) 국가에서 스마트시티 및 의료복합 시설 건설은 고성능 단열재 및 실란트 수요를 견인하고 이 지역의 이소시아네이트 시장 규모의 성장 궤도를 더욱 확대하고 있습니다. 오만과 사우디아라비아에 자산을 가진 생산자는 기초 방향족 화합물로의 역통합도 가능하며, 변동이 심한 세계의 벤젠 가격 중에서 이익률의 향상을 도모할 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 건축 단열재용 경질 폴리우레탄 폼 수요 급증

- 아시아태평양의 급속한 산업화 및 도시화

- 경량 차량화의 동향이 폴리우레탄 복합재 채용 촉진

- 콜드체인 및 전자상거래용 포장의 성장

- 이소시아네이트 복합재를 이용한 풍력 터빈 블레이드의 제조

- 시장 성장 억제요인

- 벤젠 및 니트로벤젠의 원료 가격의 변동성

- EU REACH 규정에 관한 교육 및 분류 장벽

- 중국에 있어서의 환경 규제에 수반하는 조업 정지에 의한 공급 박박

- 밸류체인 분석

- 규제 상황

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 가격 동향

제5장 시장 규모 및 성장 예측

- 유형별

- MDI

- TDI

- 지방족계(예 : HDI, IPDI)

- 기타 유형

- 용도별

- 경질 발포 플라스틱

- 연질 폼

- 도료 및 코팅

- 접착제 및 실란트

- 엘라스토머

- 바인더

- 기타 용도

- 최종 사용자 업계별

- 건축 및 건설

- 자동차

- 헬스케어

- 가구

- 기타 최종 사용자(항공우주, 전자기기 및 선박)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 러시아

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 튀르키예

- 이집트

- 나이지리아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 및 순위 분석

- 기업 프로파일

- Anderson Development Company

- Asahi Kasei Chemicals

- BASF SE

- BorsodChem

- Chemtura Corp.

- China National Bluestar(Group) Co. Ltd.

- Covestro AG

- Dow Inc.

- Evonik Industries

- Huntsman Corporation LLC

- Kemipex

- 한국 Fine Chemical Co. Ltd.

- Kumho

- MITSUI CHEMICALS AMERICA INC.

- Perstorp

- Tosoh Corporation

- Vencorex

- Wanhua Chemical Group Co. Ltd.

제7장 시장 기회 및 장래 전망

AJY 26.01.26Isocyanates market size in 2026 is estimated at 18.67 million tons, growing from 2025 value of 17.59 million tons with 2031 projections showing 25.16 million tons, growing at 6.14% CAGR over 2026-2031.

This trajectory reflects escalating adoption of high-performance polyurethane systems, supply-side consolidation, and tightening environmental regulations that reward vertically integrated producers. Rigid foam maintains momentum as efficiency standards raise thermal-insulation baselines, while automotive lightweighting broadens specialized demand beyond strictly construction uses. Integrated feedstock strategies, trade-policy shifts, and a pivot toward premium aliphatic chemistries further shape competitive positioning within the isocyanates market.

Global Isocyanates Market Trends and Insights

Surging Demand for Rigid PU Foam in Building Insulation

Revisions to the 2024 International Building Code mandate NFPA 285 fire testing for exterior wall assemblies that contain combustible insulation, making proven isocyanate-based systems the low-risk route for specifiers. Polyisocyanurate boards offer thermal conductivity as low as 0.018 W/m*K, allowing for thinner wall assemblies compared to mineral wool in retrofit settings where space is limited. State energy codes now cite ASHRAE 90.1 more frequently, pushing builders to higher R-values that rigid polyurethane can achieve within existing envelopes. The isocyanates market, therefore, benefits from retro-demand as older structures upgrade to meet net-zero targets. Global green-building certifications also favor materials with established life-cycle data, giving MDI-based foams a further compliance edge.

Rapid Industrialization and Urbanization in APAC

Southeast Asian economies are scaling manufacturing bases beyond China, creating new intra-regional demand pools for MDI and TDI. Producers with units in Vietnam, Thailand, and Indonesia can meet the rising local consumption while mitigating geopolitical-driven supply-chain risks. Tosoh's 130,000-tpy MDI plant in Vietnam exemplifies this diversification strategy. Large-scale urban housing and transportation projects across ASEAN are driving demand for insulation, sealants, and composite panels, all of which rely on isocyanate chemistries. As income levels rise, consumption of durable goods-especially mattresses and appliances-drives steady demand for flexible foam. These structural shifts keep the isocyanates market on a multi-year growth path, irrespective of export softness elsewhere.

Volatile Benzene and Nitro-Benzene Feedstock Pricing

Benzene is the primary aromatic precursor for both MDI and TDI, so any spike in crude-linked naphtha values cascades directly into isocyanate manufacturing costs. Spot benzene in Asia swung, forcing producers to issue monthly price-adjustment clauses that eroded buyer visibility. Margins compress fastest for non-integrated converters that lack backward links to aromatics, encouraging vertical integration or long-term offtake contracts. Inventory strategies are evolving toward hedged positions that cover at least three months of demand to cushion volatility; however, this ties up working capital and raises carrying costs. The net result is a dampening effect on short-term consumption growth as formulators delay orders when the feedstock price direction is unclear.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Vehicle Trend Driving PU Composites Adoption

- Cold-Chain and E-Commerce Packaging Growth

- EU REACH Training and Classification Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MDI held a 58.75% market share of the isocyanates market in 2025, backed by its versatility in rigid foam and composite formulations that serve high-volume construction and industrial applications. At the same time, aliphatic isocyanates are tracking a 6.72% CAGR that outpaces the overall isocyanates market, with UV-stable HDI and IPDI penetrating automotive clearcoat and wind-blade resin systems where long-term durability commands premium prices. TDI demand remains resilient in bedding and furniture, but growth is slower as the segment reaches maturity and competitive pressure from viscoelastic MDI systems intensifies. Specialty blocked and pre-polymer variants, while low volume, offer elevated margins by targeting electronics encapsulation, marine coatings, and aerospace composites.

The isocyanates market size for aliphatic grades is set to climb steadily as OEM specifications in both automotive and renewable-energy sectors pivot to durability metrics that aromatic chemistries struggle to meet. Producers are investing in additional HDI monomer loops to shorten supply chains for downstream polyisocyanate production, anticipating regional content rules in North America and Europe. Meanwhile, MDI suppliers are adding capacity to address bottlenecks to retain cost leadership, highlighting a dual-track investment landscape that balances commodity scale with specialty value capture.

The Isocyanates Market Report is Segmented by Type (MDI, TDI, Aliphatic, and Other Types), Application (Rigid Foam, Flexible Foam, Paints and Coatings, Adhesives and Sealants, and More), End-User Industry (Building and Construction, Automotive, Healthcare, Furniture, and Other End-Users), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific accounted for 46.85% of the isocyanates market share in 2025, a lead secured by China's benzene-advantaged MDI complexes and Southeast Asia's emerging manufacturing corridors that shorten delivery times to regional converters. The consolidation of smaller Chinese plants under stricter emissions regulations is driving volume toward large operators that can leverage economies of scale while meeting environmental targets. Vietnamese and Indonesian downstream clusters are also scaling rigid-foam and footwear production, reinforcing a self-sustaining demand loop that cushions the region from export swings.

North America holds a significant position, benefiting from shale-advantaged feedstock and proximity to the automotive and construction sectors, which anchor polyurethane consumption. BASF's ongoing expansion at Geismar, Louisiana, will lift regional MDI nameplate capacity to roughly 600,000 t/y in 2026, ensuring supply sufficiency as electric-vehicle output scales. Trade-policy uncertainty, exemplified by the 2025 USITC antidumping probe into Chinese MDI, encourages dual sourcing and supports domestic plant utilization. Europe, while technologically advanced, contends with REACH training costs that nudge smaller converters toward offshore sourcing, modestly softening local growth prospects despite continued retro-insulation activity.

The Middle-East and Africa are projected to experience the fastest regional expansion at a 6.25% CAGR to 2031, as governments fund mega-infrastructure projects and petrochemical self-sufficiency programs. State-backed players leverage low-cost propane dehydrogenation and benzene extraction to feed integrated MDI and TDI units. The construction of smart cities and healthcare complexes-particularly in the Gulf Cooperation Council-drives demand for high-performance insulation and sealants, further amplifying the regional isocyanates market size trajectory. Producers with assets in Oman and Saudi Arabia can also back-integrate into basic aromatics, enhancing margin capture under volatile global benzene pricing.

- Anderson Development Company

- Asahi Kasei Chemicals

- BASF SE

- BorsodChem

- Chemtura Corp.

- China National Bluestar (Group) Co. Ltd.

- Covestro AG

- Dow Inc.

- Evonik Industries

- Huntsman Corporation LLC

- Kemipex

- Korea Fine Chemical Co. Ltd.

- Kumho

- MITSUI CHEMICALS AMERICA INC.

- Perstorp

- Tosoh Corporation

- Vencorex

- Wanhua Chemical Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for rigid PU foam in building insulation

- 4.2.2 Rapid industrialization and urbanization in APAC

- 4.2.3 Lightweight vehicle trend driving PU composites adoption

- 4.2.4 Cold-chain and e-commerce packaging growth

- 4.2.5 Wind-turbine blade production using isocyanate composites

- 4.3 Market Restraints

- 4.3.1 Volatile benzene and nitro-benzene feedstock pricing

- 4.3.2 EU REACH training and classification hurdles

- 4.3.3 Supply tightness from China environmental shutdowns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Price Trend

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 MDI

- 5.1.2 TDI

- 5.1.3 Aliphatic (e.g., HDI, IPDI)

- 5.1.4 Other Types

- 5.2 By Application

- 5.2.1 Rigid Foam

- 5.2.2 Flexible Foam

- 5.2.3 Paints and Coatings

- 5.2.4 Adhesives and Sealants

- 5.2.5 Elastomers

- 5.2.6 Binders

- 5.2.7 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Automotive

- 5.3.3 Healthcare

- 5.3.4 Furniture

- 5.3.5 Other End-users (Aerospace, Electronics, Marine)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Turkey

- 5.4.5.5 Egypt

- 5.4.5.6 Nigeria

- 5.4.5.7 South Africa

- 5.4.5.8 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Anderson Development Company

- 6.4.2 Asahi Kasei Chemicals

- 6.4.3 BASF SE

- 6.4.4 BorsodChem

- 6.4.5 Chemtura Corp.

- 6.4.6 China National Bluestar (Group) Co. Ltd.

- 6.4.7 Covestro AG

- 6.4.8 Dow Inc.

- 6.4.9 Evonik Industries

- 6.4.10 Huntsman Corporation LLC

- 6.4.11 Kemipex

- 6.4.12 Korea Fine Chemical Co. Ltd.

- 6.4.13 Kumho

- 6.4.14 MITSUI CHEMICALS AMERICA INC.

- 6.4.15 Perstorp

- 6.4.16 Tosoh Corporation

- 6.4.17 Vencorex

- 6.4.18 Wanhua Chemical Group Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment