|

시장보고서

상품코드

1907268

유럽의 판유리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

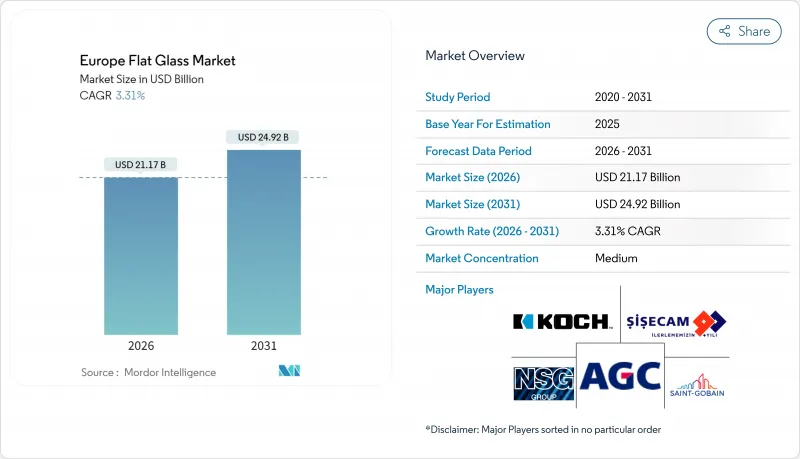

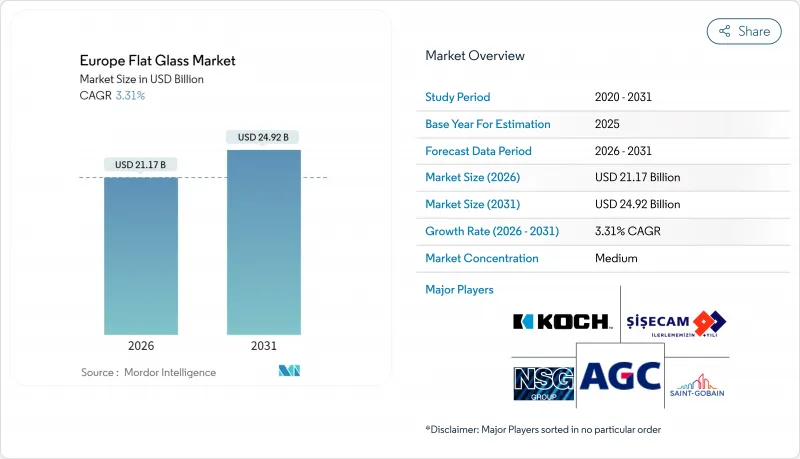

유럽의 판유리 시장은 2025년에 204억 9,000만 달러로 평가되었고, 2026년 211억 7,000만 달러에서 2031년까지 249억 2,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 3.31%를 나타낼 전망입니다.

에너지 효율적인 건축 규정, 차량 경량화 추세, 태양광 발전 용량 증설 간의 강한 상관관계가 유럽의 판유리 시장의 확장을 뒷받침하고 있습니다. 지역 내 건설사들은 저방사(low-E) 및 진공 단열 유닛 설치를 가속화하고 있으며, 자동차 제조사들은 탄소 배출량 감축과 실내 미적 개선을 위해 파노라마 글레이징을 적용하고 있습니다. 동시에 유럽의 가속화된 태양광 보급은 패턴 유리 및 커버 글래스 수요를 촉진하여 기존 건설 주기와는 별개의 구조적 성장 동력을 창출하고 있습니다. EU 배출권 거래제(EU-ETS) 4단계 탄소 가격이 비용 곡선을 재편하는 가운데, 제조사들은 전기 및 수소 용광로 투자로 변동성 큰 소다회와 천연가스 비용을 완화하고 있습니다. 모든 최종 사용 분야에서 유럽의 판유리 시장은 고성능 유리가 선택적 업그레이드가 아닌 규정 준수 필수 요건이 되도록 하는 규제적 호재의 혜택을 받고 있습니다.

유럽의 판유리 시장 동향 및 인사이트

유럽 전역의 건설 및 외관 리모델링 증가

인프라 프로그램과 상업용 리모델링이 2024년 경기 침체 이후 수요를 되살리고 있습니다. 지멘스는 2024년 240억 유로의 스마트 인프라 수주를 기록했으며, 이 중 상당 부분은 삼중 단열 유리를 요구하는 에너지 효율적 건물 외피와 연계됐다. 덴마크 주요 오피스 투자자들은 ESG 기준에 부합하는 리모델링을 우선시하여 저방사(Low-E) 유닛 수요 증가로 이어지고 있습니다. 프랑스와 이탈리아의 노후 주택 재고 역시 U-값 1.0 W/m²K 미만을 규정하는 의무적 업그레이드 주기에 진입 중입니다. 이러한 동향은 건설 비용 상승으로 신축 활동이 위축되는 상황에서도 유럽의 판유리 시장의 기본 물량을 끌어올리고 있습니다. 코팅 및 진공 단열 제품 포트폴리오를 보유한 제조사들이 이러한 규정 준수 수요를 가장 효과적으로 포착할 수 있는 위치에 있습니다.

EU 27개국의 자동차 경량화와 파노라마 유리 채택

OEM들은 강철 지붕 패널을 다중 패널 파노라마 유리 모듈로 교체하여 무게를 줄이고 배터리 전기차 주행 거리를 향상시키고 있습니다. 웨바스토(Webasto)와 고지(Gauzy)는 파노라마 루프에서 두 자릿수 성장을 보고하는 한편, AGC는 헤드업 디스플레이용 증강 현실 윈드실드를 상용화했습니다. 가열 기능, 안테나 내장, 음향 라미네이트는 프리미엄 마진을 확보하며 가공 유리 수요를 높입니다. 상용차 제조사들도 공기역학 규제가 강화되면서 동일한 추세를 따릅니다. 이러한 트렌드들은 종합적으로 차량당 평균 평방미터 소비량을 확대하여, 전반적인 자동차 생산량이 감소할 때 수요 탄력성을 강화합니다.

EU 배출권 거래제(EU-ETS) 4단계 하의 높은 전력 집약도와 탄소 가격

4단계에서는 무료 할당량이 축소되어 2025년 탄소 비용이 톤당 85유로 이상으로 상승할 전망입니다. 판유리 용융 공정은 부가가치 달러당 상위 3대 산업 배출원으로 꼽히므로, 제조사들은 전력 요금을 통해 직접적·간접적 탄소 부담을 동시에 지게 됩니다. 저탄소 가격 지역 수입품과의 경쟁 격차가 확대되면서 탄소 국경 조정(CBDA) 도입 요구가 높아지고 있습니다. 산소연료 버너, 태양광 발전 프리트 가마, 수소 시험에 대한 투자는 자산의 미래 대비를 목표로 하지만, 모든 사업자가 감당할 수 없는 다년간의 투자 회수 기간이 필요합니다.

부문 분석

유럽의 판유리 시장 규모에서 어닐링 처리된 기판이 차지하는 비중은 전체 가치의 51.88%에 달했습니다. 규제 강화로 인해 가공 제품 카테고리로의 성장이 촉진되고 있습니다. 강화 및 접합 유리는 안전 규정을 충족하며, 단열 유리는 저방사(Low-E) 의무 기준을 충족합니다. 소프트 코팅 은층을 적용한 코팅 솔루션은 태양광 제어 기능을 추가하여 HVAC 부하를 20%까지 절감할 수 있습니다. 거울은 가구 분야에서 틈새 시장을 유지하지만, 여전히 광범위한 소비자 지출 주기에 연동됩니다.

가공 유리 생산량은 생산자들이 지속적으로 기술 경계를 확장함에 따라 일반 플로트 유리를 앞지릅니다. 세닥(Sedak)의 곡면 강화 라인으로 6.5m 패널을 생산해 공항 및 박물관 설계 자유도를 높입니다. 리섹(LiSEC)의 로봇 분류 시스템은 폐기물을 줄이고 삼중 유닛 조립에 중요한 두께 편차를 ±0.1mm 이내로 제어합니다. 자동화는 추적성을 향상시켜 다수 금융기관이 요구하는 ESG 감사에 기여합니다. 이러한 혁신은 저가 수입품 대비 유럽의 경쟁 우위를 강화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 유럽 전역의 건설 및 외관 리모델링 증가

- EU 27 가맹국의 자동차 경량화와 파노라믹 유리 채택 동향

- 태양광 PV 설비 증설 급증으로 인한 태양광 및 패턴 유리 수요 증가

- EU의 저방사(Low-E) 및 진공 단열 유리 지원 ‘리노베이션 웨이브(Renovation Wave)’ 보조금

- 건물 일체형 태양광(BIPV) 커튼월의 부상

- 시장 성장 억제요인

- 소다재, 규사, 천연가스의 가격 변동성

- EU 배출권 거래제(EU-ETS) 4단계 하의 높은 전력 집약도 및 탄소 가격 책정

- 초대형 단열 유리의 현장 설치에 대한 새로운 기술 격차

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 제품 유형별

- 어닐링 처리(착색 포함)

- 코팅 처리(저에너지, 태양열 제어)

- 반사 처리

- 가공 처리(강화 유리, 접합 유리, 복층 유리)

- 거울

- 최종 사용자 업계별

- 건축 및 건설

- 자동차

- 태양광, 태양광 발전

- 가구 및 인테리어 장식

- 기타(가전, 철도, 선박)

- 지역별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 폴란드

- 베네룩스

- 북유럽 국가(스웨덴, 노르웨이, 덴마크, 핀란드)

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율**/순위 분석

- 기업 프로파일

- AGC Inc.

- AGP Group

- Ardagh Group SA,

- Bohle AG

- Euroglas

- Interpane Glas Industrie AG

- Koch Industries

- Nippon Sheet Glass Co., Ltd.

- OGIS GmbH

- Press Glass SA

- Saint-Gobain

- SCHOTT

- Sisecam

- Vitro

제7장 시장 기회와 장래의 전망

HBR 26.02.04The Europe Flat Glass Market was valued at USD 20.49 billion in 2025 and estimated to grow from USD 21.17 billion in 2026 to reach USD 24.92 billion by 2031, at a CAGR of 3.31% during the forecast period (2026-2031).

The strong correlation between energy-efficient construction regulations, vehicle lightweighting trends, and solar-photovoltaic capacity additions underpins this expansion of the Europe flat glass market. Builders across the region are accelerating the installation of low-emissivity (low-E) and vacuum-insulated units, while automakers are embedding panoramic glazing to cut carbon emissions and improve cabin aesthetics. Simultaneously, Europe's accelerating solar roll-out fuels demand for patterned and cover glass, creating a structural growth pillar distinct from conventional construction cycles. Producers are mitigating volatile soda-ash and natural-gas costs by investing in electric and hydrogen furnaces, even as EU-ETS Phase IV carbon prices reshape cost curves. Across every end-use, the Europe flat glass market benefits from regulatory tailwinds that make high-performance glazing a compliance necessity rather than a discretionary upgrade.

Europe Flat Glass Market Trends and Insights

Increasing Construction and Facade Renovation Across Europe

Infrastructure programs and commercial retrofits are reviving demand after the 2024 downturn. Siemens booked EUR 24 billion of smart-infrastructure orders in 2024, much of it tied to energy-efficient building envelopes that specify triple-insulated glazing. Danish prime office investors prioritize ESG-aligned refurbishments, translating to higher volumes of low-E units. Older housing stock in France and Italy is also entering a mandated upgrade cycle that prescribes U-values below 1.0 W/m2K. This dynamic lifts baseline volumes for the Europe flat glass market, even as high construction costs temper new-build activity. Producers with coated and vacuum-insulated portfolios are best positioned to capture this compliance-driven wave.

Automotive Lightweighting and Panoramic Glazing Adoption in EU-27 Vehicle Platforms

OEMs are replacing steel roof panels with multi-panel panoramic glass modules that cut weight and improve battery-electric range. Webasto and Gauzy report double-digit growth in panoramic roofs, while AGC has commercialized augmented-reality windshields for heads-up displays. Heated, antenna-embedded, and acoustic laminates command premium margins and push processed-glass demand higher. Commercial-vehicle makers follow the same trajectory as aerodynamic regulations tighten. These trends collectively widen average square-meter consumption per vehicle, reinforcing demand resilience when broader auto output softens.

High Electricity Intensity and Carbon Pricing Under EU-ETS Phase IV

Phase IV allocates fewer free allowances, lifting carbon costs above EUR 85/tCO2 in 2025. Flat-glass melting ranks among the top three industrial emitters per USD of value added, so producers pay both direct and indirect carbon charges via power tariffs. The competitive gap versus imports from low-carbon-price regions widens, raising calls for carbon-border adjustments. Investments in oxy-fuel burners, photovoltaic-powered frit kilns, and hydrogen trials aim to future-proof assets but require multi-year paybacks that not all operators can absorb.

Other drivers and restraints analyzed in the detailed report include:

- Surging Solar-PV Capacity Additions Driving Demand for Solar and Pattern Glass

- EU "Renovation Wave" Subsidies for Low-E and Vacuum-Insulated Glazing

- New Skill Gap for On-Site Installation of Oversized Insulated Glazing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Europe flat glass market size attributable to annealed substrates reached 51.88% of the total value in 2025. Regulatory upgrades steer growth into processed categories. Tempered and laminated panes meet safety codes, while insulated units satisfy low-E mandates. Coated solutions incorporating soft-coat silver layers add solar-control functionality that can cut HVAC loads by 20%. Mirrors maintain niche uptake in furniture, yet remain tied to broader consumer spending cycles.

Processed glass volumes outpace commodity float because producers continually push the technology frontier. Sedak's curved-tempering line fabricates 6.5 m panels, unlocking design latitude for airports and museums. LiSEC's robotic sorting shrinks waste and delivers pane thickness variance within +-0.1 mm, a metric critical for triple-unit assemblies. Automation also improves traceability, aiding ESG audits now required by many lenders. These innovations fortify European competitive advantage against lower-cost imports.

The Europe Flat Glass Market Report is Segmented by Product Type (Annealed, Coated, Reflective, Processed, Mirrors), End-User Industry (Building and Construction, Automotive, Solar and Photovoltaic, Furniture and Interior Decor, Others), and Geography (Germany, United Kingdom, France, Italy, Spain, Poland, Benelux, Nordics, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AGC Inc.

- AGP Group

- Ardagh Group S.A,

- Bohle AG

- Euroglas

- Interpane Glas Industrie AG

- Koch Industries

- Nippon Sheet Glass Co., Ltd.

- OGIS GmbH

- Press Glass SA

- Saint-Gobain

- SCHOTT

- Sisecam

- Vitro

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing construction and facade renovation across Europe

- 4.2.2 Automotive lightweighting and panoramic glazing adoption in EU-27 vehicle platforms

- 4.2.3 Surging solar-PV capacity additions driving demand for solar and pattern glass

- 4.2.4 EU "Renovation Wave" subsidies for low-E and vacuum-insulated glazing

- 4.2.5 Rise of building-integrated-photovoltaic (BIPV) curtain-walls

- 4.3 Market Restraints

- 4.3.1 Volatile soda-ash, silica-sand and natural-gas prices

- 4.3.2 High electricity intensity and carbon-pricing under EU-ETS Phase IV

- 4.3.3 New skill-gap for on-site installation of oversized insulated glazing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Annealed (incl. Tinted)

- 5.1.2 Coated (low-E, solar-control)

- 5.1.3 Reflective

- 5.1.4 Processed (tempered, laminated, IGU)

- 5.1.5 Mirrors

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Solar and Photovoltaic

- 5.2.4 Furniture and Interior Decor

- 5.2.5 Others (appliances, rail, marine)

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Poland

- 5.3.7 Benelux

- 5.3.8 Nordics (Sweden, Norway, Denmark, Finland)

- 5.3.9 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 AGP Group

- 6.4.3 Ardagh Group S.A,

- 6.4.4 Bohle AG

- 6.4.5 Euroglas

- 6.4.6 Interpane Glas Industrie AG

- 6.4.7 Koch Industries

- 6.4.8 Nippon Sheet Glass Co., Ltd.

- 6.4.9 OGIS GmbH

- 6.4.10 Press Glass SA

- 6.4.11 Saint-Gobain

- 6.4.12 SCHOTT

- 6.4.13 Sisecam

- 6.4.14 Vitro

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment