|

시장보고서

상품코드

1907274

북미의 스마트 제조 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)North America Smart Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

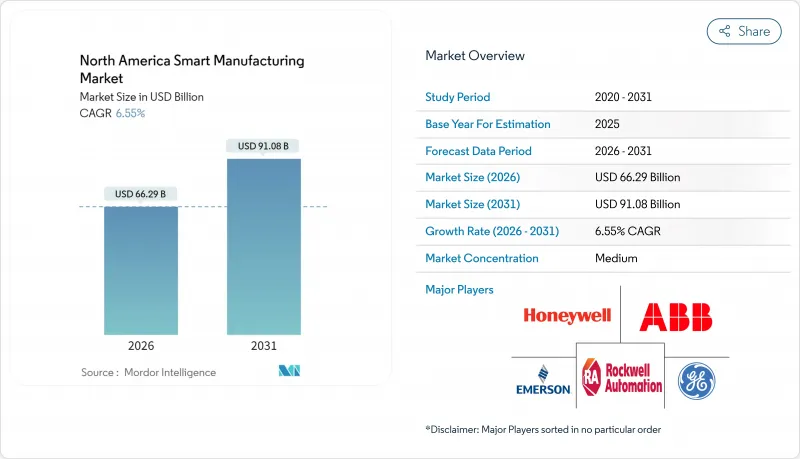

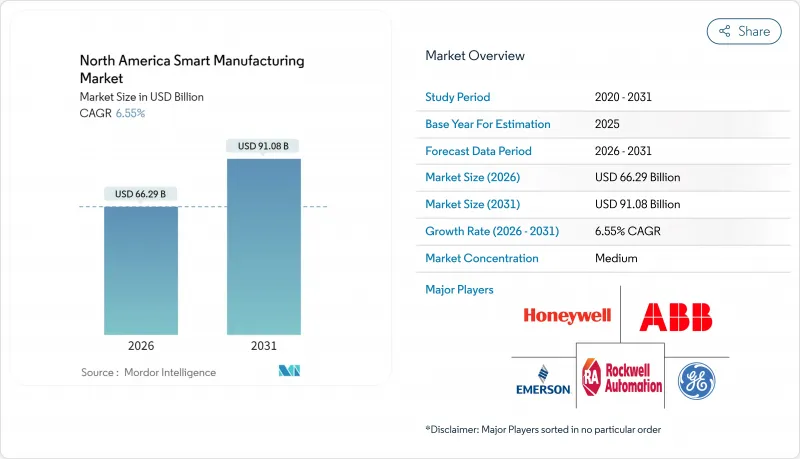

북미의 스마트 제조 시장은 2025년 622억 1,000만 달러로 평가되었으며, 2026년 662억 9,000만 달러, 2031년까지 910억 8,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026년-2031년)에 있어서의 CAGR은 6.55%를 나타낼 전망됩니다.

이 성장세는 연방 정부의 기록적 인센티브, 민간 부문의 강력한 자본 형성, 이산 산업과 공정 산업 전반의 인공지능(AI), 5G, 사이버 물리학 시스템(CPS)의 긴밀한 협력에 기인합니다. 제조업체의 93% 이상이 2024년에 새로운 AI 이니셔티브를 시작했으며 예측 가능하고 자체 최적화하는 생산 환경이 파일럿 단계에서 대규모 배포로 전환하고 있음을 보여줍니다. 반도체 산업의 회귀, 자동차 전동화의 의무화, 배터리 공급망의 확충이 수요를 지지하는 한편, 제약 및 생명과학 시설에서는 엄격한 컴플라이언스 요건 대응을 위해 설비 갱신이 가속하고 있습니다. 북미의 스마트 제조 시장은 노동력 동태 변화에도 영향을 받고 있으며, 숙련된 기술자의 이직과 사이버 보험 비용의 급등이 중소기업 도입 페이스를 억제하고 있습니다.

북미의 스마트 제조 시장 동향과 통찰

미국의 이산 제조업에서 AI 탑재 엣지 분석 도입의 급증

AI 알고리즘이 기계 레벨에 내장되어 예지 보전을 실현합니다. 이를 통해 예기치 않은 다운타임을 최대 60%까지 줄이고 자산 수명을 20%까지 연장할 수 있습니다. 클린 에너지 및 스마트 제조 혁신 연구소는 인재 육성 프로그램을 통해 이러한 툴에 대한 액세스를 확대하고 데이터 사이언스의 스킬 갭 해소를 지원하고 있습니다. 제조업체는 밀리초 단위의 응답이 품질을 좌우하는 자동차 및 항공우주 분야의 지연에 민감한 용도에 있어서 현장에서의 데이터 처리가 필수적이라고 생각하고 있습니다.

캐나다 국내 공장에서 5G 대응 산업용 IoT 네트워크의 급속한 보급

사설 5G 네트워크는 기존의 연결 병목 현상을 해결합니다. 한 미국 철강 시설에서는 5G LAN 솔루션 도입 후 운영 장애가 70분의 1로 감소하여 연간 200만 달러의 절약을 달성했습니다. 제조업은 이미 세계에서 발표된 프라이빗 5G 도입의 46%를 차지하고 있습니다. 캐나다 무선통신협회는 5G를 통해 2025년까지 국내 배출량을 12.2MtCO2e 삭감할 수 있을 것으로 예측했습니다.

OT 사이버 보험 보험료 지속적인 인상이 디지털 전환을 방해

2024년에는 제조업체의 65%가 랜섬웨어 피해를 입었고 연결 자산을 도입하는 기업의 보험료는 30% 이상 상승했습니다. 많은 공장에서는 여전히 지속적인 OT 모니터링이 부족하고 인식되는 리스크와 실제 리스크 프로파일의 편차가 확산되고 있습니다.

부문 분석

프로그래머블 로직 컨트롤러(PLC)는 2025년에 21.60%의 수익 점유율을 차지하며 수천 개의 공장에서 제어층의 기반을 담당하고 있습니다. 한편 북미의 협동 로봇 시장 규모는 제조자가 안전한 사람과 로봇의 협동을 우선하는 가운데 CAGR 8.46%로 확대될 것으로 전망됩니다. OTTO Motors사의 자율이동 로봇 등의 도입 사례에서는 11개월에 투자 회수가 가능하며, 안전사고 없이 작업셀의 설치면적을 15% 삭감하고 있습니다.

하이브리드 에지-투-클라우드 아키텍처는 PLC와 AI 추론 엔진의 통합을 추진하고 있습니다. 로크웰 오토메이션과 NVIDIA는 공동으로 레퍼런스 디자인을 개발 중이며, 운영자는 품질 검사 흐름에 생성형 AI를 적용할 수 있습니다. 머신 비전에는 결함 0을 보장하는 신경망이 내장되어 있으며 제품 수명 주기 관리 도구의 디지털 트윈은 물리적 실행 전에 프로세스 조정을 가상으로 테스트하는 데 도움이 됩니다.

제어 하드웨어는 2025년 지출의 54.30%를 차지했지만, 소프트웨어 및 서비스는 2031년까지 연평균 복합 성장률(CAGR)9.86%로 넘을 전망입니다. 제조업체는 분석, 사이버 보안 및 지속적인 최적화를 번들로 제공하는 구독 모델을 적극적으로 채택하여 가치 실현 시간을 단축하고 있습니다. 통신 인프라(특히 사설 5G 및 타임센시티 네트워킹 이더넷)는 이러한 전환을 지원하여 산업용 IoT의 확장성을 촉진합니다.

고급 비전 센서가 이러한 전환을 상징합니다. Cognex의 In-Sight L38 3D 시스템은 AI와 듀얼 모드 이미징을 결합하여 교육 데이터 요구 사항을 최소화하여 도입을 가속화합니다. 스칼라 로봇부터 자율 이동 로봇까지 다루는 로보틱스 컴포넌트 키트는 유연성을 더욱 높였으며, MES 4.0 프레임워크는 IT와 OT 데이터 레이크를 통합하여 자동차 업계의 시험 운영에서 재고를 30% 줄이고 직원 1인당 수익을 75% 향상시켰습니다.

북미의 스마트 제조 시장 점유율 보고서는 기술(PLC, SCADA 등), 구성 요소(제어 장치, 통신 인프라 등), 최종 사용자 산업(자동차, 석유 및 가스 등), 도입 모드(On-Premise, 클라우드 등), 국가(미국, 캐나다)별로 분류됩니다. 시장 규모와 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 가치/공급망 분석

- 규제 및 기술 동향(북미)

- 투자 분석(자본 흐름, M&A, 벤처 자금 조달)

- 거시경제사건(COVID-19, 무역정책, 노동력 부족)의 영향

- 시장 성장 촉진요인

- 미국에서의 이산 제조업에서의 AI 탑재 엣지 분석의 채택 급증

- 캐나다 국내 공장에서 5G 대응 산업용 IoT 네트워크의 급속한 보급

- 리쇼어링 장려책(CHIPS and Science Act, IRA)이 디지털 퍼스트 공장을 촉진

- 지속가능성의 요청이 기존 시설에서 스마트 에너지 관리 개보수를 추진

- 자동차 클러스터에서 제로 결함 생산을 위한 사이버 피지컬 시스템 도입

- 중소규모의 수주 생산 제조업체에 있어서의 모듈 및 로우 코드 MES 수요 증가

- 시장 성장 억제요인

- 지속적인 OT 사이버 보험의 보험료 인상이 디지털 전환 제한

- 기존 PLC 설치 기반에 있어서의 복수 벤더간의 상호 운용성의 갭

- Tier 2 자동차 부품 제조업체에 있어서의 인플레이션 요인에 의한 설비 투자의 연기

- 숙련 기술 인력의 은퇴 속도를 따라가지 못하는 업스킬링(Upskilling) 교육 체계

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁의 격렬함

제5장 시장 규모와 성장 예측

- 기술별

- 모니터링 제어 및 데이터 수집(SCADA)

- 분산제어시스템(DCS)

- 휴먼 머신 인터페이스(HMI)

- 제조 실행 시스템(MES)

- 제품 수명주기 관리(PLM)

- 전사적 자원 계획(ERP)

- 로보틱스 및 협동 로봇

- 머신 비전 및 품질 검사

- 엣지 및 클라우드 분석 플랫폼

- 컴포넌트별

- 제어기기(PLC, DCS, PAC)

- 통신 인프라(5G, 산업용 이더넷)

- 센서 및 액추에이터

- 머신 비전 시스템

- 로봇(다관절, 스카라, 자율 이동 로봇)

- 소프트웨어 및 서비스(MES, 디지털 트윈, SaaS)

- 최종 사용자 업계별

- 자동차

- 항공우주 및 방위

- 석유 및 가스(상류, 중류, 하류)

- 화학제품 및 석유화학제품

- 의약품 및 생명과학

- 식음료

- 금속 및 광업

- 전자 및 반도체

- 펄프 및 제지

- 기타(섬유, 플라스틱)

- 전개 모드별

- On-Premise

- 클라우드(SaaS)

- 하이브리드

- 국가별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 전략적 움직임(제휴, 리쇼어링, ESG 연계 금융)

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- Emerson Electric Co.

- FANUC Corp.

- General Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corp.

- Robert Bosch GmbH(Bosch Rexroth)

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corp.

- Omron Corp.

- PTC Inc.

- IBM Corp.

- Cisco Systems Inc.

- SAP SE

- Dassault Systemes SE

- Cognex Corp.

- Keyence Corp.

- Stratasys Ltd.

제7장 시장 기회와 장래의 전망

SHW 26.01.26The North America smart manufacturing market was valued at USD 62.21 billion in 2025 and estimated to grow from USD 66.29 billion in 2026 to reach USD 91.08 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031).

Momentum stems from record federal incentives, strong private-sector capital formation and the tight coupling of artificial intelligence, 5G and cyber-physical systems across discrete and process industries. More than 93% of manufacturers launched new AI initiatives in 2024, a signal that predictive, self-optimizing production environments are moving from pilots to scaled rollouts. Semiconductor reshoring, automotive electrification mandates and battery supply-chain buildouts anchor demand, while pharmaceutical and life-sciences facilities accelerate upgrades to meet stringent compliance requirements. The North America smart manufacturing market is also shaped by shifting workforce dynamics, with skilled-trades attrition and cyber-insurance cost spikes tempering adoption velocity among small and mid-sized enterprises.

North America Smart Manufacturing Market Trends and Insights

Surging Adoption of AI-Enabled Edge Analytics in U.S. Discrete Manufacturing

AI algorithms are now embedded at the machine layer, enabling predictive maintenance that cuts unplanned downtime by up to 60% and extends asset lifespans by 20%. The Clean Energy Smart Manufacturing Innovation Institute broadens access to these tools through workforce programs, helping close data-science skill gaps. Manufacturers view on-site data processing as essential for latency-sensitive applications in automotive and aerospace where millisecond-level responses govern quality.

Rapid Proliferation of 5G-Powered Industrial IoT Networks across Canadian Plants

Private 5G networks eliminate historical connectivity bottlenecks; one U.S. steel facility recorded a 70-fold reduction in operational disruptions and annual savings of USD 2 million after adopting a 5G LAN solution. Manufacturing already accounts for 46% of announced private 5G deployments worldwide. The Canadian Wireless Telecommunications Association forecasts that 5G could cut national emissions by 12.2 MtCO2e by 2025.

Persistent OT Cyber-Insurance Premium Hikes Limiting Digital Conversions

Ransomware incidents affected 65% of manufacturers in 2024, pushing premiums up more than 30% for firms introducing connected assets. Many plants still lack continuous OT monitoring, widening the gap between perceived and actual risk profiles.

Other drivers and restraints analyzed in the detailed report include:

- Reshoring Incentives Fueling Digital-First Factories

- Sustainability Mandates Driving Smart Energy-Management Retrofits

- North American Skilled-Trades Attrition Outpacing Upskilling Pipelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Programmable Logic Controllers held 21.60% revenue in 2025, anchoring the control layer across thousands of plants. The North America smart manufacturing market size for collaborative robotics, however, is projected to rise at an 8.46% CAGR as manufacturers prioritize safe human-robot collaboration. Deployments such as OTTO Motors' Autonomous Mobile Robots deliver 11-month paybacks and shrink work-cell footprints 15% without safety incidents.

Hybrid edge-to-cloud architectures increasingly unite PLCs with AI inference engines. Rockwell Automation and NVIDIA are co-developing reference designs that let operators apply generative AI for quality inspection flows. Machine vision now embeds neural networks for zero-defect assurance, while digital twins inside Product Lifecycle Management tools help test process tweaks virtually before physical execution.

Control hardware accounted for 54.30% of 2025 spending, yet software and services are forecast to outpace at a 9.86% CAGR through 2031. Manufacturers increasingly embrace subscription models that bundle analytics, cybersecurity and continuous optimization, reducing time-to-value. Communication infrastructure-especially private 5G and Time-Sensitive Networking Ethernet-underpins this pivot and supports Industrial IoT scalability.

Advanced vision sensors spotlight the transition. Cognex's In-Sight L38 3D system combines AI with dual-mode imaging to accelerate deployment by minimizing training data requirements. Robotics component kits, spanning SCARA to Autonomous Mobile Robots, further elevate flexibility, while MES 4.0 frameworks integrate IT and OT data lakes to slash inventory 30% and lift revenue per employee 75% in automotive trials.

North America Smart Manufacturing Market Share Report is Segmented by Technology (PLC, SCADA and More), Component (Control Devices, Communication Infrastructure, and More), End-User Industry (Automotive, Oil and Gas and More), Deployment Mode (On-Premise, Cloud and More), and Country (United States, Canada). The Market Size and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ABB Ltd.

- Emerson Electric Co.

- FANUC Corp.

- General Electric Co.

- Honeywell International Inc.

- Mitsubishi Electric Corp.

- Robert Bosch GmbH (Bosch Rexroth)

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Texas Instruments Inc.

- Yokogawa Electric Corp.

- Omron Corp.

- PTC Inc.

- IBM Corp.

- Cisco Systems Inc.

- SAP SE

- Dassault Systemes SE

- Cognex Corp.

- Keyence Corp.

- Stratasys Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Value / Supply-Chain Analysis

- 4.2 Regulatory and Technological Outlook (North America)

- 4.3 Investment Analysis (capital flows, MandA, venture funding)

- 4.4 Impact of Macroeconomic Events (COVID-19, Trade-Policy, Labor Shortage)

- 4.5 Market Drivers

- 4.5.1 Surging Adoption of AI-enabled Edge Analytics in U.S. Discrete Manufacturing

- 4.5.2 Rapid Proliferation of 5G-powered Industrial IoT Networks across Canadian Plants

- 4.5.3 Reshoring Incentives (CHIPS and Science Act, IRA) Fueling Digital-First Factories

- 4.5.4 Sustainability Mandates Driving Smart Energy-Management Retrofits in Brown-field Sites

- 4.5.5 Adoption of Cyber-Physical Systems for Zero-Defect Production in Automotive Clusters

- 4.5.6 Growing Demand for Modular, Low-Code MES among SME Job-Shops

- 4.6 Market Restraints

- 4.6.1 Persistent OT Cyber-Insurance Premium Hikes Limiting Digital Conversions

- 4.6.2 Multi-vendor Interoperability Gaps in Legacy PLC Install-base

- 4.6.3 Inflation-driven CAPEX Deferrals in Tier-2 Automotive Suppliers

- 4.6.4 North American Skilled-Trades Attrition Outpacing Upskilling Pipelines

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Techonology

- 5.1.1 Supervisory Control and Data Acquisition (SCADA)

- 5.1.2 Distributed Control System (DCS)

- 5.1.3 Human-Machine Interface (HMI)

- 5.1.4 Manufacturing Execution System (MES)

- 5.1.5 Product Lifecycle Management (PLM)

- 5.1.6 Enterprise Resource Planning (ERP)

- 5.1.7 Robotics and Collaborative Robots

- 5.1.8 Machine Vision and Quality Inspection

- 5.1.9 Edge and Cloud Analytics Platforms

- 5.2 By Component

- 5.2.1 Control Devices (PLC, DCS, PAC)

- 5.2.2 Communication Infrastructure (5G, Industrial Ethernet)

- 5.2.3 Sensors and Actuators

- 5.2.4 Machine Vision Systems

- 5.2.5 Robotics (Articulated, SCARA, AMR)

- 5.2.6 Software and Services (MES, Digital Twin, SaaS)

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace and Defense

- 5.3.3 Oil and Gas (Upstream, Midstream, Downstream)

- 5.3.4 Chemicals and Petrochemicals

- 5.3.5 Pharmaceuticals and Life-Sciences

- 5.3.6 Food and Beverage

- 5.3.7 Metals and Mining

- 5.3.8 Electronics and Semiconductors

- 5.3.9 Pulp and Paper

- 5.3.10 Others (Textiles, Plastics)

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Cloud (SaaS)

- 5.4.3 Hybrid

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves (Partnerships, Reshoring, ESG-linked Financing)

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.3.1 ABB Ltd.

- 6.3.2 Emerson Electric Co.

- 6.3.3 FANUC Corp.

- 6.3.4 General Electric Co.

- 6.3.5 Honeywell International Inc.

- 6.3.6 Mitsubishi Electric Corp.

- 6.3.7 Robert Bosch GmbH (Bosch Rexroth)

- 6.3.8 Rockwell Automation Inc.

- 6.3.9 Schneider Electric SE

- 6.3.10 Siemens AG

- 6.3.11 Texas Instruments Inc.

- 6.3.12 Yokogawa Electric Corp.

- 6.3.13 Omron Corp.

- 6.3.14 PTC Inc.

- 6.3.15 IBM Corp.

- 6.3.16 Cisco Systems Inc.

- 6.3.17 SAP SE

- 6.3.18 Dassault Systemes SE

- 6.3.19 Cognex Corp.

- 6.3.20 Keyence Corp.

- 6.3.21 Stratasys Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment