|

시장보고서

상품코드

1907282

폴리프로필렌 섬유 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Polypropylene Fibers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

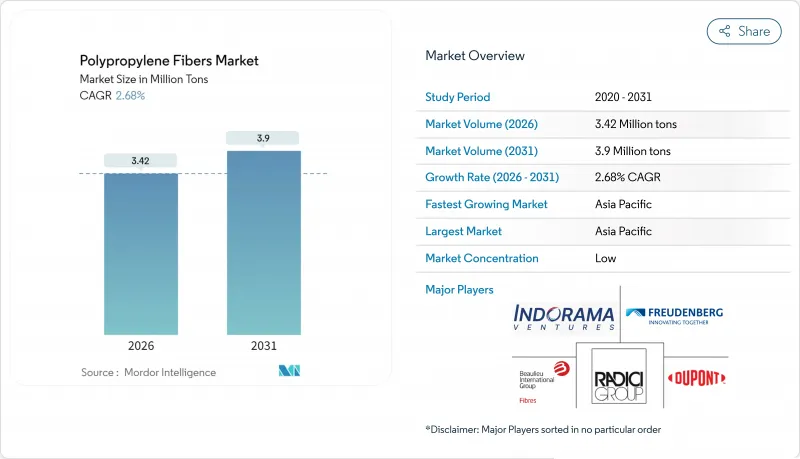

폴리프로필렌 섬유 시장은 2025년 333만 톤으로 평가되었고, 2026년에는 342만 톤, 2026년에서 2031년에 걸쳐 CAGR 2.68%로 성장하고 2031년까지 390만 톤에 달할 것으로 예측되고 있습니다.

이 성장은 위생 용품, 건설 및 자동차 용도의 안정적인 수요를 충족시키면서 미세 플라스틱 규제 강화 및 재생 폴리 에스테르와의 가격 경쟁을 극복하는 폴리프로필렌 섬유 시장의 능력을 반영합니다. 중국이 2024년부터 2026년까지 연간 1,870만 톤의 폴리프로필렌 수지 생산 능력을 추가함으로써 원재료 비용은 낮은 수준으로 유지되고 폴리프로필렌 섬유 시장의 비용 우위성이 지속되고 있습니다. 아시아태평양의 최종 용도 확대, 특히 일회용 위생 용품 및 인프라 분야에서 수요 증가는 재활용 의무화에 의해 버진 섬유 수요가 억제되고 있는 북미 및 유럽에서의 성장의 둔화를 상쇄하고 있습니다.

세계의 폴리프로필렌 섬유 시장 동향과 전망

위생용품 및 의료용 일회용 제품에 있어서의 사용량 증가

2024년 스펀본드법 폴리프로필렌 부직포는 기저귀, 여성용 위생 용품, 수술용 드레이프 수요에 견인되어 세계 위생용 부직포 시장을 독점했습니다. 병원에서는 현재, 일회용 프로토콜이 채택되고 있어 COVID-19 팬데믹 시에 급증한 멜트블로운 생산 능력을 계속 활용하고 있어 의료용 일회용 제품에 있어서의 폴리프로필렌 섬유의 존재감을 확고한 것으로 하고 있습니다. 인도의 위생 분야는 생리대의 보급 확대와 여성 노동력 증가에 힘입어 크게 성장할 것으로 예상되어 폴리프로필렌 섬유의 지역 소비가 촉진됩니다. 인도네시아, 베트남, 태국에서도 유사한 동향이 관찰되어 도시 지역의 소득 증가가 기저귀의 보급을 촉진하고 있습니다. 폴리프로필렌은 소수성, 통기성, 멸균과의 궁합이 우수하기 때문에 EU 의료기기 규정(MDR 2017/745) 하에서는 우선적으로 채택되고 있지만, 고급 성인용 실금 제품에서는 현저한 변화가 보입니다. 이러한 제품은 부드러움을 중시하고 폴리에틸렌과 폴리 프로파일렌의 이중 성분 블렌드가 점점 선호되는 경향이 있으며 섬유 제조 업체는 제품 라인의 다양 화를 진행하고 있습니다.

건설 분야에서 거시 합성 섬유 콘크리트 보강재로의 전환

매크로 합성 폴리프로필렌 섬유(3-5kg/m3 첨가)는 플라스틱 수축 균열을 억제하고, 강재에 비해 설치 비용을 삭감하고, 녹 관련 유지보수를 저감하기 위해 대규모 바닥재 및 터널 프로젝트에 대한 지속적인 채택을 지원하고 있습니다. 바라트말라 고속도로와 사갈마라 항만 계획에서는 섬유 강화 콘크리트 조항이 인도 입찰서에 통합되어 있습니다. 시공업체는 철근망의 설치가 불필요하다는 점을 평가하고 있으며, 폴리프로필렌 섬유 시장은 ASTM C1399 및 EN 14889-2에 있어서의 잔류 강도 사양의 인상으로부터 혜택을 받고 있습니다. 주택 분야에서의 채택은 규제의 공백에 의해 여전히 한정적이지만, 인도 콘크리트 협회에 의한 새로운 가이드라인이 열대 기후 지역에서의 보급 촉진을 목표로 하고 있습니다.

저비용 PET 및 재생 PET 섬유 공급 상태

병 회수 네트워크와 화학적 재활용 기술의 진전으로 재생 PET의 생산 능력이 급속히 확대되고 있는 가운데, rPET의 프리미엄 가격은 저하되고, 카펫 안감, 의류 안감, 가구장지 등의 분야에서 대체 리스크가 높아지고 있습니다. 신발과 의류 분야의 주요 세계 브랜드는 재생 폴리 에스테르 함량 향상을 공약하고 기존에 우선 해 온 폴리 프로파일렌에서 조달 예산을 재분배하고 있습니다. 이러한 변화는 특히 패션 분야에서 폴리프로필렌 섬유 시장에 압력을 가하고 있습니다. 폴리프로필렌의 재활용 수율은 낮은 용융 강도와 안료 오염 등의 과제로 인해 PET보다 낮지만, 이러한 제약이 순환성에 대한 주장을 방해하고 rPET에 유리한 비용 비교를 뒷받침하고 있습니다. 위생 분야에서는 범용 스펀본드가 PET에 비해 속도면에서 우위성을 자랑합니다. 그러나 폴리프로필렌이 상당한 가격 할인을 제공하지 않는 한, 섬유 산업은 점점 rPET에 기울어지고 있습니다.

부문 분석

2025년 생산량의 84.46%를 차지한 실부문은 2031년까지 연평균 복합 성장률(CAGR)2.72%로 증가할 것으로 전망되고 있습니다. 이것은 폴리프로필렌 섬유 시장 전체의 성장률을 4베이시스 포인트 웃돌고, 직조 지오텍스타일이나 카펫 안감에 있어서의 기초적인 역할을 강화하는 것입니다. 직조 지오텍스타일용 직기는 연속 장섬유를 필요로 하고, 피팅에 의한 생산 정지가 발생하지 않기 때문에 수요의 연속성이 보증되고 있습니다. 벌크성을 목표로 하는 텍스처 가공을 실시한 벌크 연속 긴 섬유 등급은 카펫용 실 수요의 절반을 공급하고, 고강도의 평사는 터프팅 및 봉제사를 지지합니다. 카펫 안감은 실의 내오염성과 나일론에 대한 비용 우위성을 살려 연간 상당량을 흡수하고 있습니다.

나머지 점유율을 차지하는 단섬유는 바늘 펀치가공된 자동차용 라이너, 수축 가공된 위생 흡수층, 복합 여과 웹의 기반이 됩니다. 단섬유 제품은 필라멘트를 38-102mm의 길이로 절단하고 이를 카딩하여 열 또는 기계적으로 결합하는 웹으로 가공하여 부피와 부드러움을 실현합니다. 자동차용 트렁크 라이너는 재생 소재를 포함한 15-25 데니어의 단섬유 블렌드를 사용하여 0.6 이상의 소음 감소 계수를 달성했으며 실 소비량이 지배적이면서도 가치가 유지되고 있음을 보여줍니다. 그러나 스테이플 섬유의 점유율 확대에는 스펀본드와의 처리 속도 차이가 장벽이 됩니다. 스펀본드는 필라멘트 형성과 웹 결합을 800m/분으로 통합하기 때문입니다. 카딩 속도의 향상이나 재활용 규제가 불연속 섬유를 우대하지 않는 한, 2031년까지 실이 주도권을 유지할 전망입니다.

폴리프로필렌 섬유 시장 보고서는 유형별(단섬유와 방적사), 최종 사용자 산업별(섬유, 건설, 의료 위생, 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카)으로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 수량의 51.05%를 차지하며 2031년까지 연평균 복합 성장률 3.33%로 성장할 것으로 예측됩니다. 이 지역은 2031년까지 꾸준한 성장이 예상되어 주도적 지위를 유지할 전망입니다. 중국의 견고한 프로파일렌 기반은 폴리프로필렌에 상당량을 할당하고 있어 수지 공급이 과잉이 되어 국내 섬유 생산자를 지지하고 있습니다. 특필해야할 것은 이러한 생산자가 최근 방적 능력을 확대하고 있다는 점입니다. 공급 과잉을 배경으로 주로 동남아시아 시장을 목표로 한 PP 섬유의 수출이 급증했습니다. 인도의 부직포 산업은 위생 수요와 바라 토말라 계획에서 도로 지오텍 스타일 사양에 견인되어 상당한 성장이 예상됩니다. 한편, 역내 수요의 상당 부분을 차지하는 ASEAN 국가에서는 도시의 소득 수준이 상승하고 있습니다. 이 추세로 종이 기저귀와 생리대의 소비가 증가하고 있습니다. 동시에 인도네시아와 베트남에서는 현지 컨버터가 스펀본드 생산 라인의 확장을 진행하고 있습니다.

세계 시장에서 큰 점유율을 차지하는 북미에서는 성장률이 둔화되고 있습니다. 이 성장 문제는 성숙한 자동차 생산과 지오텍 스타일의 재활용 의무가 EV 관련 복합재의 성장을 상쇄하고 있기 때문입니다. 텍사스의 신규 폴리프로필렌 플랜트가 수지 공급을 강화한 반면, 2024년에 가동한 신규 섬유 방사 설비는 한정적이었습니다. 이 제한적인 확장은 사출 성형 등급 및 필름 등급에 대한 시장 선호도를 돋보이게합니다. 시장 규모에서 큰 비율을 차지하는 유럽은 꾸준한 성장 궤도를 추적하고 있습니다. 이 지역은 순환형 경제의 선구적 노력에서도 최전선에 위치하고 있습니다. 주목할만한 프로젝트에는 지오텍 스타일의 재활용 및 재생 사용 노력이 포함됩니다. 이러한 이니셔티브는 경제적 실현 가능성을 검증 중이지만 과제에 직면하고 있습니다. 보조금이 없으면 비용은 Virgin PP보다 높게 유지됩니다. 또한, 2023년부터 시행된 EU의 마이크로플라스틱 규제는 여과장치의 개조를 의무화하고 있습니다. 이러한 움직임은 컴플라이언스 비용을 증가시킬 뿐만 아니라 시장에서 대규모 수직 통합 기업을 유리하게 만드는 경향이 있습니다.

세계 수요의 상당 부분을 차지하는 남미 지역과 중동 및 아프리카에서는 꾸준한 성장을 볼 수 있습니다. 이 성장은 주로 인프라 메가 프로젝트의 진전과 위생 기준의 보급 확대에 의해 견인되고 있습니다. 브라질에서는 특정 지역에서 종이 기저귀의 보급률 상승을 배경으로 부직포 수요량이 견고하게 증가하고 있습니다. 한편, 사우디아라비아에서는 「비전 2030」구상에 기초한 시설에 있어서, 폴리프로필렌제 지오텍스타일 및 매크로 합성 섬유의 사용이 의무화되고 있습니다. 이 사양에 따라 2028년까지 연간 수요 견인이 예상되지만 실시 일정은 여전히 유동적입니다. 다만 양 지역 모두 수입 의존도가 높고 운임 변동의 영향을 받기 쉬운 상황에 있습니다. 예를 들어, 아시아로부터의 운송비는 착륙비용을 높일 수 있습니다. 이 상황은 특히 통화가 낮을 때 국내 PET 생산자에게 경쟁 우위를 가져옵니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 위생용품 및 의료용 일회용 제품에 있어서의 사용량 증가

- 건설 업계에서의 매크로 합성 콘크리트 보강재로의 전환

- 도로 및 해안 공학에 있어서의 지오텍스타일의 보급 상황

- 저밀도 경량 자동차 내장재에 대한 수요

- PP 섬유 강화 복합재의 3D 프린팅

- 시장 성장 억제요인

- 저비용 PET 및 재생 PET 섬유의 이용 가능성

- 낮은 녹는점으로 인한 고온 환경 적용의 한계

- 미세 플라스틱 유출에 대한 ESG 규제 및 감시 강화

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 원재료 분석

제5장 시장 규모와 성장 예측

- 유형별

- 스테이플

- 원사

- 최종 사용자 업계별

- 섬유

- 건설

- 의료 및 위생

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- ABC Polymer Industries LLC

- Beaulieu Fibres International(BFI)

- Belgian Fibers

- Chemosvit Fibrochem SRO

- China National Petroleum Corporation

- DuPont

- Fiberpartner Aps

- Freudenberg Group

- Huimin Taili Chemical Fiber Products Co. Ltd

- Indorama Ventures

- International Fibres Group

- Kolon Fiber Inc.

- Mitsubishi Chemical Corporation

- Radici Partecipazioni SpA

- Sika AG

- Tri Ocean Textile Co. Ltd

- W. Barnet GmbH & Co. KG

- Zenith Fibres Ltd

제7장 시장 기회와 장래의 전망

SHW 26.01.26The Polypropylene Fibers market is expected to grow from 3.33 million tons in 2025 to 3.42 million tons in 2026 and is forecast to reach 3.9 million tons by 2031 at 2.68% CAGR over 2026-2031.

Growth reflects the polypropylene fiber market's ability to meet steady demand from hygiene, construction, and automotive applications while navigating tighter microplastics regulations and price competition from recycled polyester. China's addition of 18.7 million tons per year of polypropylene resin capacity between 2024 and 2026 keeps raw-material costs low and sustains the polypropylene fiber market's cost advantage. End-use expansion within the Asia-Pacific, particularly in disposable hygiene and infrastructure, offsets slower gains in North America and Europe, where recycling mandates temper demand for virgin fiber.

Global Polypropylene Fibers Market Trends and Insights

Rising Usage in Hygiene and Medical Disposables

In 2024, spunbond polypropylene nonwovens dominated the global hygiene nonwoven market, driven by demand for diapers, feminine care products, and surgical drapes. Hospitals, now adopting single-use protocols, continue to utilize the meltblown capacity that surged during the COVID-19 pandemic, solidifying polypropylene fiber's presence in medical disposables. India's hygiene sector, buoyed by the broader distribution of sanitary napkins and a growing female workforce, is poised for significant growth, thereby bolstering regional consumption of polypropylene fibers. A similar trend is observed in Indonesia, Vietnam, and Thailand, where increasing urban incomes are driving the adoption of diapers. While polypropylene's hydrophobicity, breathability, and compatibility with sterilization make it the preferred choice under EU MDR 2017/745, there's a notable shift in premium adult incontinence products. These are increasingly favoring bicomponent polyethylene-polypropylene blends for their softness, leading fiber producers to diversify their offerings.

Construction-Sector Shift to Macro-Synthetic Concrete Reinforcement

Macro-synthetic polypropylene fibers, dosed at 3-5 kg/m3, curtail plastic-shrinkage cracking, reduce installed costs relative to steel, and cut rust-related maintenance, supporting sustained inclusion in large flooring and tunnel projects. The Bharatmala highway and Sagarmala port programs have incorporated fiber-reinforced concrete clauses into Indian tenders. Contractors value the elimination of steel-mesh placement, while the polypropylene fiber market benefits from higher residual-strength specifications in ASTM C1399 and EN 14889-2. Residential uptake remains limited by code gaps; however, new guidelines from the Indian Concrete Institute aim to accelerate adoption in tropical climates.

Availability of Lower-Cost PET and Recycled-PET Fibers

As recycled PET capacity rapidly expands-bolstered by bottle collection networks and advancements in chemical recycling-the premium for rPET has decreased, heightening the risk of substitution in areas such as carpet backing, apparel linings, and upholstery. Major global brands in footwear and apparel, now committing to higher recycled-polyester content, are reallocating procurement budgets away from their traditional preference for polypropylene. This shift puts pressure on the polypropylene fiber market, particularly in the fashion segment. While recycling yields for polypropylene trail those of PET due to challenges such as lower melt strength and pigment contamination, these limitations hinder circularity claims and bolster cost comparisons in favor of rPET. In the hygiene sector, commodity spunbond boasts a speed edge compared to PET. However, the textile industry is increasingly leaning towards rPET, unless polypropylene offers a substantial price discount.

Other drivers and restraints analyzed in the detailed report include:

- Geotextile Penetration in Road and Coastal Engineering

- Demand for Low-Density Lightweight Automotive Interiors

- Low Melting Point Restricts High-Temperature Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Yarn generated 84.46% of 2025 volume and is forecast to increase at a 2.72% CAGR to 2031, outpacing the broader polypropylene fiber market by 4 basis points and reinforcing its foundational role in woven geotextiles and carpet backing. Woven-geotextile looms require continuous filament, and any splice halts production, ensuring demand continuity. Bulk continuous filament grades, texturized for loft, supply half of the carpet yarn demand, while high-tenacity flat yarn supports tufting and sewing thread. Carpet backing, capitalizing on yarn's stain resistance and a cost advantage over nylon, absorbs a significant amount annually.

Staple fiber captures the remaining share and underpins needle-punched automotive liners, crimped hygiene acquisition layers, and composite filtration webs. Staple products deliver loft and softness by cutting filament into lengths of 38-102 mm, then carding it into webs that bond thermally or mechanically. Automotive trunk liners achieve noise-reduction coefficients greater than 0.6 using 15-25 denier staple blends with recycled content, illustrating value retention even as yarn volume dominates. However, staple's share is capped by the throughput gap with spunbond, which integrates filament formation and web bonding at 800 m/min. Unless carding speeds rise or recyclability rules favor discontinuous fibers, yarn will retain leadership through 2031.

The Polypropylene Fiber Market Report is Segmented by Type (Staple and Yarn), End-User Industry (Textile, Construction, Healthcare and Hygiene, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region accounted for 51.05% of the 2025 volume and is projected to grow at a rate of 3.33% annually through 2031. The region is set to maintain its lead, with steady growth projected through 2031. China's robust propylene base dedicates a significant portion to polypropylene, resulting in a surplus resin supply that bolsters domestic fiber producers. Notably, these producers have expanded their spinning capacity in recent years. With an oversupply in hand, PP fiber exports surged, primarily targeting Southeast Asian markets. India's nonwoven industry, driven by hygiene demands and highway geotextile specifications under the Bharatmala program, is poised for significant growth. Meanwhile, ASEAN economies, accounting for a notable portion of the region's demand, are witnessing a rise in urban incomes. This uptick has led to increased consumption of diapers and sanitary napkins. Concurrently, local converters are expanding their spunbond lines in both Indonesia and Vietnam.

North America, holding a considerable share in the global market, is experiencing a tempered growth rate. This muted pace can be attributed to a balance between mature automotive outputs and geotextile recycling mandates, which counterbalance the growth seen in EV-related composites. While new polypropylene plants in Texas have bolstered resin supplies, the market saw limited new fiber spinning capacity come online in 2024. This limited expansion highlights a market preference for injection-molding and film grades. Europe, commanding a significant portion of the market volume, is charting a steady growth trajectory. The region is also at the forefront of pioneering circular initiatives. Notable projects include geotextile recycling and reclamation efforts. While these initiatives are testing economic viability, they face a challenge: costs remain higher than virgin PP unless subsidized. Additionally, the EU's microplastics regulation, effective from 2023, mandates filtration retrofits. This move not only increases compliance costs but also appears to favor larger, vertically integrated players in the market.

The South America and Middle East-Africa regions, each accounting for a notable portion of the global demand, are witnessing steady growth. This growth is largely driven by advancements in infrastructure megaprojects and a rising adoption of hygiene standards. In Brazil, nonwoven volumes are climbing at a strong rate, spurred by increased diaper penetration in certain regions. Meanwhile, in Saudi Arabia, venues under the Vision 2030 initiative are mandating the use of polypropylene geotextiles and macro-synthetic fibers. This specification translates to an anticipated annual demand pull through 2028, although the execution timelines remain somewhat fluid. However, both regions face import dependencies, making them vulnerable to fluctuations in freight costs. For instance, shipping costs from Asia can inflate landed costs. This dynamic offers a competitive edge to domestic PET producers, especially when currencies decline, as highlighted by recent devaluations.

- ABC Polymer Industries LLC

- Beaulieu Fibres International (BFI)

- Belgian Fibers

- Chemosvit Fibrochem SRO

- China National Petroleum Corporation

- DuPont

- Fiberpartner Aps

- Freudenberg Group

- Huimin Taili Chemical Fiber Products Co. Ltd

- Indorama Ventures

- International Fibres Group

- Kolon Fiber Inc.

- Mitsubishi Chemical Corporation

- Radici Partecipazioni SpA

- Sika AG

- Tri Ocean Textile Co. Ltd

- W. Barnet GmbH & Co. KG

- Zenith Fibres Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising usage in hygiene and medical disposables

- 4.2.2 Construction-sector shift to macro-synthetic concrete reinforcement

- 4.2.3 Geotextile penetration in road and coastal engineering

- 4.2.4 Demand for low-density lightweight automotive interiors

- 4.2.5 3-D printing of PP fibre-reinforced composites

- 4.3 Market Restraints

- 4.3.1 Availability of lower-cost PET and recycled-PET fibres

- 4.3.2 Low melting point restricts high-temperature applications

- 4.3.3 ESG scrutiny on micro-plastics leakage

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

- 4.6 Raw-Material Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Staple

- 5.1.2 Yarn

- 5.2 By End-User Industry

- 5.2.1 Textile

- 5.2.2 Construction

- 5.2.3 Healthcare and Hygiene

- 5.2.4 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABC Polymer Industries LLC

- 6.4.2 Beaulieu Fibres International (BFI)

- 6.4.3 Belgian Fibers

- 6.4.4 Chemosvit Fibrochem SRO

- 6.4.5 China National Petroleum Corporation

- 6.4.6 DuPont

- 6.4.7 Fiberpartner Aps

- 6.4.8 Freudenberg Group

- 6.4.9 Huimin Taili Chemical Fiber Products Co. Ltd

- 6.4.10 Indorama Ventures

- 6.4.11 International Fibres Group

- 6.4.12 Kolon Fiber Inc.

- 6.4.13 Mitsubishi Chemical Corporation

- 6.4.14 Radici Partecipazioni SpA

- 6.4.15 Sika AG

- 6.4.16 Tri Ocean Textile Co. Ltd

- 6.4.17 W. Barnet GmbH & Co. KG

- 6.4.18 Zenith Fibres Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment