|

시장보고서

상품코드

1907312

파라자일렌(PX) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Paraxylene (PX) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

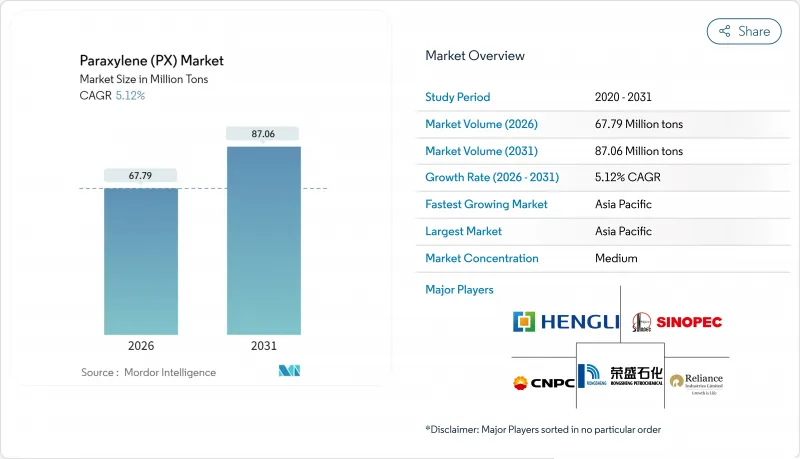

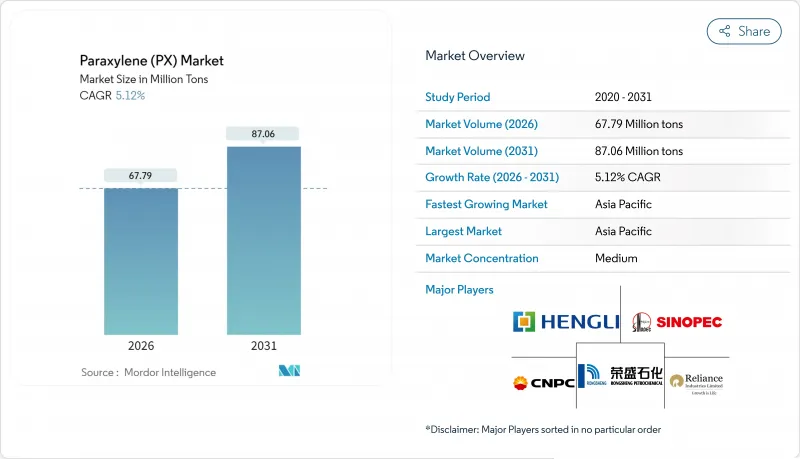

파라자일렌(PX) 시장은 2025년 6,448만 톤에서 2026년에는 6,779만 톤으로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 CAGR 5.12%로 성장할 것으로 예상되며, 2031년까지 8,706만 톤에 달할 것으로 예측되고 있습니다.

파라자일렌의 안정적 공급은 정제 테레프탈산(PTA)이 포장재 및 섬유용 폴리에틸렌 테레프탈레이트(PET)로 직접 전환되기 때문에 글로벌 폴리에스터 생산 라인의 기반이 됩니다. 중국의 석유-화학 복합체는 원유를 직접 방향족 화합물로 가공함으로써 비용 우위를 점하고 있으며, 이러한 접근 방식은 2024-2025년 동안 1천만 톤 이상의 신규 파라자일렌 생산 능력을 추가했습니다. 원료 경제성은 여전히 핵심 요소다. 나프타 가격이 전년 대비 16.5% 하락한 톤당 554.79달러로 조정되면서 2025년 초 마진이 회복되었으나, 공급 과잉으로 현물 가격은 압박을 받았다. 수요 회복력은 음료 및 퍼스널케어 포장, 기술 섬유, 아시아태평양 지역의 증가하는 가처분 소득에서 비롯됩니다. 한편 바이오 기반 공정과 화학 재활용은 기존 생산자들에게 위험과 기회를 동시에 제공합니다. 따라서 경쟁적 입지는 규모, 통합, 에너지 효율성, 그리고 브랜드 조달 전략에 영향을 미치는 지속가능성 의무를 이행할 수 있는 능력에 달려 있습니다.

세계의 파라자일렌(PX) 시장 동향과 전망

PET 포장재 수요 급증

음료, 가정용 세정액, 퍼스널케어를 포장하는 브랜드 소유자들은 여전히 무거운 소재를 PET로 대체하고 있으며, 이는 PTA가 병 수지 중량의 약 70%를 차지하기 때문에 파라자일렌 수요를 촉진하고 있습니다. 릴라이언스 인더스트리즈는 2024 회계연도 글로벌 PET 판매량이 13% 증가했다고 보고했는데, 이는 운송 효율성과 진열 효과를 요구하는 소매업체 기준을 충족하는 경량화 및 완전 재활용 가능 병 형태가 주도했습니다. 온라인 식료품 및 D2C(소비자 직거래) 채널은 긴 유통망에서도 파손이 적은 PET의 장점으로 인해 이러한 판매량을 더욱 확대합니다. 정부 규제는 전면 금지보다 최소 재활용 함량 기준을 점차 명시함으로써, 포장재 성장에 맞춰 신규 파라자일렌 수요를 유지하면서 동시에 수거 인프라를 활성화하고 있습니다. 결과적으로 방향족 화합물 및 PTA 자산을 통합한 정유소는 예측 가능한 기본 수요를 확보하여 운송 연료가 주기적 침체를 겪을 때에도 수익을 안정화합니다.

아시아에서 폴리에스터 섬유 확대

아시아태평양 지역은 여전히 세계의 섬유 생산 거점이며, 파라자일렌 가격 변동성에도 불구하고 폴리에스터의 면 대비 비용 우위가 섬유 수요를 유지합니다. 중국은 2024년 400만 톤 이상의 신규 폴리에스터 스테이플 생산 능력을 가동했으며, 인도는 국내 의류 수출 촉진을 위해 합성섬유를 포함한 성과 연계 인센티브 제도를 승인했습니다. 자동차 에어백, 컨베이어 벨트, 지오텍스타일 등 기술 섬유 수요는 안정적이고 마진이 높은 물량을 추가하며 일관된 PTA 공급에 의존합니다. 잠나가르와 다롄의 통합 단지는 파라자일렌, PTA, 섬유 방적 공정을 한곳에 배치해 운송 비용을 절감함으로써 지역 경쟁력을 강화합니다. 패스트 패션 브랜드의 주문 주기 가속화로 인해 제직 공장들은 PTA의 적시 납품을 보장하는 공급업체를 선호하는데, 이는 중국 동부 연안 지방의 대규모 통합 클러스터 내에서 가장 실현 가능한 역량입니다.

일회용 플라스틱 규제 강화

유럽연합(EU)의 일회용 플라스틱 지침은 특정 테이크아웃 용품을 금지하고 생산자 책임 확대(EPR) 제도를 도입해 신규 PET를 사용하는 가공업체의 준수 비용을 증가시킵니다. 캘리포니아주의 유사한 법안은 2028년까지 음료 병에 재활용 소재 25% 사용을 의무화하여 브랜드 소유자들이 틈새 SKU를 위해 알루미늄 또는 종이 기반 솔루션으로 다각화하도록 촉진합니다. 운영 측면에서 패스트푸드 포장용 파라자일렌 수요는 정체될 수 있으나, 무균 주스나 유제품과 같은 고차단성 PET 용도는 성능 요건으로 보호받는다. 이로 인해 성숙 시장의 성장은 둔화되는 반면, 순수한 생산량 제한보다 실용적인 재활용성 목표를 가진 지역으로 수지 흐름이 재편됩니다.

부문 분석

정제 테레프탈산은 2025년 글로벌 물량의 94.35%를 유지하며 파라자일렌 시장의 핵심 출구로서의 지위를 공고히 했습니다. 장쑤, 저장, 구자라트에서 진행 중인 PTA 확장 규모는 해당 부문이 전체 방향족 공급량을 능가할 것임을 의미하며, 2031년까지 연평균 5.32%의 성장률을 기록할 것으로 예상됩니다. 정유-화학 통합의 지속적 추진은 가동률 유연성을 높여 파라자일렌과 PTA 설비 간 물류 이동을 최소화하고 원료 공급 안정성을 확보합니다. 결과적으로 단일 사이트 메가 프로젝트의 PTA 생산 능력은 연간 300만 톤을 초과하여 현물 파라자일렌 프리미엄 가격 변동을 완화하는 규모의 경제를 실현합니다. 디지털 트윈 모델은 이러한 단지 내 열 통합 네트워크를 최적화하여 에너지 비용을 10-12% 절감하고 배출량을 감소시킵니다. 이는 유럽 수출 고객에게 적용되는 스코프 1 탄소 배출량 제한 준수가 영향을 미치는 상황에서 유리한 점입니다.

디메틸 테레프탈레이트(DMT) 틈새 시장은 라이선스 업체들이 직접 PTA 공정 대비 15-20% 높은 가변 비용을 이유로 에스테르 교환 공정 라인을 폐기함에 따라 축소되고 있습니다. 특수 용제, 가소제, 제초제 중간체 등이 파라자일렌 소비량의 잔여 1-2%를 차지하며 중간 단일자리 수치(5%대 초반)의 성장을 보이지만, 전체 수요를 좌우하기에는 부족하다. 그럼에도 불구하고, 이들은 개질기 방향족 풀 내 이성질체 비율 균형을 맞추는 데 중요하며, 생산 계획이 단일 분자가 아닌 정유소 전체 가치를 극대화하도록 보장합니다. 대체 바이오 방향족이 유망해 보이지만 상업적 생산량은 여전히 미미하여, 전망 기간 동안 기존 PTA가 파라자일렌 시장을 계속 주도할 것임을 시사합니다.

파라자일렌(PX) 시장 보고서는 용도별(정제 테레프탈산, 디메틸 테레프탈레이트(DMT), 기타 용도), 최종 사용자 산업별(플라스틱, 섬유, 기타 최종 사용자 산업), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

지역별 분석

아시아태평양 지역은 2025년 파라자일렌 시장의 82.10% 점유율로 주도했으며, 중국, 인도 및 동남아시아가 다운스트림 폴리에스터 생태계를 강화함에 따라 2031년까지 5.48%의 연평균 복합 성장률(CAGR)을 유지할 것으로 전망됩니다. 중국의 중앙 집중식 석유-화학 전략에 따라 2024-2025년에 각각 파라자일렌, PTA 및 폴리머 통합 설비를 갖춘 5개의 새로운 단지가 가동되었습니다. 다위산(Dayushan) 단지만 해도 연간 1,180만 톤의 방향족 화합물을 생산합니다. 인도는 자므나가르의 140만 톤급 PX 생산라인과 확대되는 기능성 섬유 수출 인센티브를 활용해 지역 자급률을 높이고 의류 제조 클러스터에 외국인 투자를 유치하고 있습니다. 일본과 한국은 프리미엄 사양 PX 등급 공급을 지속하고 있으나, 내수 수요가 정체되면서 생산 능력 조정 가능성이 대두되고 있습니다.

북미는 규모는 작지만 전략적으로 중요한 글로벌 점유율을 유지하고 있습니다. 혼합 자일렌 유분은 가솔린 혼합 시 높은 옥탄값을 제공하여 연료 수요가 높은 시즌에는 독립형 PX 마진이 아시아보다 낮아진다. 그럼에도 첨단 CCR 개조와 풍부한 셰일 콘덴세이트가 원료 다양성을 유지합니다. 북미의 파라-자일렌 시장 규모는 2031년까지 447만 톤에 근접할 수 있으며, 증가분은 물류 체인 단축을 중시하는 소비자 브랜드 인근에 위치한 특수 PET 및 바이오-PX 파일럿 프로젝트와 연계될 전망입니다. 화학 재활용 원료에 대한 정책 지원은 조달원을 더욱 다양화하지만, 예측 기간 동안 신규 PX의 절대적 대체 효과는 미미할 것입니다.

유럽은 더 높은 에너지 및 규제 비용에 직면하여 중동 및 아시아로부터의 수입을 촉진하고 있습니다. 지속적인 천연가스 프리미엄은 스팀 크래커의 유틸리티 비용을 상승시켜 지역 PX 경쟁력을 약화시킵니다. 그럼에도 불구하고 일회용 플라스틱 규제는 수요를 완전 재활용 가능한 PET로 전환시켜 폐쇄형 재활용 방식을 채택한 PTA 공장의 기본 수요를 유지합니다. 중동은 잉여 나프타와 개질유를 방향족 화합물로 전환해 아시아 폴리에스터 주요 기업들과의 수출 계약에 집중함으로써 글로벌 공급 구조를 긴축시키고 있습니다. 남미의 수요는 브라질 음료 부문에 집중되어 구조적 PX 무역 적자를 초래하며, 이는 미국 걸프 연안 및 아라비아만 수출업체들과의 장기 공급 계약을 통해 해결되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- PET 포장재 수요 급증

- 아시아의 폴리에스터 섬유 확대

- 경량화 및 재활용 가능한 음료 병 수요 증가로 인한 PX 수요 촉진

- 고수율 CCR 및 PRT 방향족 유닛 상업화

- 바이오 기반 파라자일렌의 상업 규모 파일럿 플랜트(비화석)

- 시장 성장 억제요인

- 일회용 플라스틱 규제 강화

- 원유 주도의 원료 가격 변동성

- 신흥 화학 재활용이 신규 PX 대체

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 정제 테레프탈산(PTA)

- 디메틸 테레프탈레이트(DMT)

- 기타 용도

- 최종 사용자 산업별

- 플라스틱

- 섬유

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 태국

- 인도네시아

- 말레이시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- China Petrochemical Corporation

- CNPC

- Eneos Corporation

- Exxon Mobil Corporation

- FCFC

- GS Caltex Corporation

- Hengli Petrochemical Co., Ltd.

- Idemitsu Kosan Co.,Ltd.

- Ineos

- LOTTE CHEMICAL CORPORATION

- PTT Global Chemical Public Company Limited

- Reliance Industries Limited

- Rongsheng Petrochemical Co., Ltd.

- S-oil Corporation

- TotalEnergies

제7장 시장 기회와 장래의 전망

HBR 26.02.04The Paraxylene Market is expected to grow from 64.48 Million tons in 2025 to 67.79 Million tons in 2026 and is forecast to reach 87.06 Million tons by 2031 at 5.12% CAGR over 2026-2031.

A secure supply of para-xylene underpins the global polyester chain because purified terephthalic acid (PTA) converts directly into polyethylene terephthalate (PET) for packaging and fiber. Integrated oil-to-chemicals complexes in China hold cost advantages by processing crude directly into aromatics, an approach that added more than 10 million tons of new para-xylene capacity during 2024-2025. Feedstock economics remain pivotal; a 16.5% year-over-year decrease in naphtha pricing to USD 554.79 per ton restored margins in early 2025 even as oversupply pressured spot values. Demand resilience comes from beverage and personal-care packaging, technical textiles and rising disposable incomes across Asia-Pacific, while bio-based routes and chemical recycling offer both risk and opportunity for incumbent producers. Competitive positioning, therefore, rests on scale, integration, energy efficiency, and the ability to navigate sustainability mandates that influence brand procurement strategies.

Global Paraxylene (PX) Market Trends and Insights

Surging Demand for PET Packaging

Brand owners that package beverages, home-care liquids and personal-care products continue to substitute heavier materials with PET, propelling para-xylene demand because PTA constitutes nearly 70% of bottle resin weight. Reliance Industries reported a 13% in global PET off-take during fiscal 2024, driven by lightweight and fully recyclable bottle formats that satisfy retailer requirements for transport efficiency and shelf appeal. Online grocery and direct-to-consumer channels magnify these volumes because PET resists breakage throughout longer distribution chains. Government regulations increasingly specify minimum recycled content rather than outright bans, allowing virgin para-xylene to keep pace with packaging growth while stimulating collection infrastructure. Consequently, refineries with integrated aromatics and PTA assets secure predictable baseload demand, smoothing earnings even when transportation fuels see cyclical downturns.

Polyester-Fiber Expansion in Asia

Asia-Pacific remains the textile workbench of the world, and polyester's cost advantage over cotton sustains fiber demand despite para-xylene price volatility. China commissioned more than 4 million tons of new polyester staple capacity in 2024, while India approved performance-linked incentive schemes covering man-made fibers to stimulate domestic garment exports. Technical textile off-take in automotive airbags, conveyor belts, and geotextiles adds steadier, higher-margin volumes that rely on consistent PTA supply. Integrated complexes in Jamnagar and Dalian reduce transport costs by colocating para-xylene, PTA, and fiber spinning, thereby boosting regional competitiveness. Fast-fashion brands accelerate order cycles, meaning mills favor suppliers that guarantee just-in-time PTA deliveries, a capability most feasible inside large integrated clusters across Eastern China's coastal provinces.

Single-Use-Plastic Legislation Tightening

The European Union's Single-Use Plastics Directive bans selected takeaway items and imposes extended-producer-responsibility fees that raise compliance costs for converters using virgin PET. Similar proposals in California mandate 25% recycled content in beverage bottles by 2028, prompting brand owners to diversify into aluminum or paper-based solutions for niche SKUs. Operationally, para-xylene demand could stall in quick-service packaging, though high-barrier PET applications such as aseptic juice or dairy remain protected by performance requirements. The net effect reduces growth in mature markets while redirecting resin flows toward regions with pragmatic recyclability targets rather than outright volume caps.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight, Recyclable Beverage Bottles Push PX

- High-Yield CCR and PRT Aromatics Units Commercializing

- Crude-Oil-Led Feedstock Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Purified terephthalic acid retained 94.35% of global volume in 2025, cementing its status as the core outlet for the para-xylene market. The scale of PTA expansions underway in Jiangsu, Zhejiang, and Gujarat means the segment will outpace overall aromatics supply, generating a 5.32% CAGR to 2031. Ongoing refinery-to-chemicals integration raises operating-rate flexibility, minimizing logistics transfers between para-xylene and PTA units and locking in feedstock security. As a result, PTA capacity at single-site mega-projects now exceeds 3 million tons per year, enabling economies that blunt price swings in spot PX premiums. Digital-twin models optimize heat-integration networks within these complexes, shaving 10-12 % from energy costs and shrinking emissions-an advantage when compliance with Scope 1 carbon limits affects European export customers.

The dimethyl terephthalate niche shrinks as licensees retire transesterification lines, citing 15-20 % higher variable costs than direct PTA routes. Specialty solvents, plasticizers, and herbicide intermediates account for the residual 1-2 % of para-xylene consumption and exhibit mid-single-digit growth, insufficient to sway aggregate demand. Nevertheless, they remain important for balancing isomer ratios inside reformer aromatics pools, ensuring that production planning maximizes overall refinery value rather than a single molecule. While substitute bio-aromatics appear promising, commercial tonnage remains minimal, indicating that conventional PTA will continue to shape the para-xylene market during the outlook period.

The Paraxylene (PX) Market Report is Segmented by Application (Purified Terephthalic Acid, Dimethyl Terephthalate, and Other Applications), End-User Industry (Plastics, Textile, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific dominated the para-xylene market with an 82.10% share in 2025 and is forecast to maintain a 5.48% CAGR to 2031 as China, India, and Southeast Asia reinforce downstream polyester ecosystems. China's centralized oil-to-chemicals strategy placed five new complexes online in 2024-2025, each with integrated para-xylene, PTA, and polymer units; Dayushan alone yields 11.8 million tons of aromatics annually. India leverages Jamnagar's 1.4 million-ton PX train and the nation's expanding technical-textile export incentives, enhancing regional self-sufficiency and attracting foreign investment in apparel manufacturing clusters. Japan and South Korea continue to supply premium specification PX grades, although capacity rationalizations loom as domestic demand plateaus.

North America retains a smaller but strategically important slice of global volume. Mixed-xylene streams fetch a strong octane value in gasoline blending, pushing stand-alone PX margins below those in Asia during high-fuel-demand seasons. Nevertheless, advanced CCR revamps and abundant shale condensate maintain feedstock diversity. The para-xylene market size in North America could edge toward 4.47 million tons by 2031, with incremental growth tied to specialty PET and bio-PX pilots located close to consumer brands that value shorter logistics chains. Policy support for chemically recycled content further diversifies sourcing, though absolute displacement of virgin PX remains modest through the forecast horizon.

Europe confronts steeper energy and regulatory costs, driving imports from the Middle East and Asia. Persistent natural-gas premiums elevate steam-cracker utility expenses, eroding local PX competitiveness. Nonetheless, single-use-plastic rules tilt demand toward fully recyclable PET, preserving baseload offtake for PTA plants that adopt closed-loop recycling schemes. The Middle East tightens global supply equations by channeling surplus naphtha and reformate into aromatics, focusing on export contracts with Asia's polyester majors. South America's demand centers on Brazil's beverages sector, leading to structural PX trade deficits addressed through long-term supply contracts with U.S. Gulf Coast and Arabian Gulf exporters.

- China Petrochemical Corporation

- CNPC

- Eneos Corporation

- Exxon Mobil Corporation

- FCFC

- GS Caltex Corporation

- Hengli Petrochemical Co., Ltd.

- Idemitsu Kosan Co.,Ltd.

- Ineos

- LOTTE CHEMICAL CORPORATION

- PTT Global Chemical Public Company Limited

- Reliance Industries Limited

- Rongsheng Petrochemical Co., Ltd.

- S-oil Corporation

- TotalEnergies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for PET Packaging

- 4.2.2 Polyester-fiber Expansion in Asia

- 4.2.3 Lightweight, Recyclable Beverage Bottles Push PX

- 4.2.4 High-yield CCR and PRT Aromatics Units Commercialising

- 4.2.5 Bio-based PX Commercial Scale Pilots (non-fossil)

- 4.3 Market Restraints

- 4.3.1 Single-use-plastic Legislation Tightening

- 4.3.2 Crude-oil Led Feedstock Price Volatility

- 4.3.3 Emerging Chemical Recycling Displacing Virgin PX

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Purified Terephthalic Acid (PTA)

- 5.1.2 Dimethyl Terephthalate (DMT)

- 5.1.3 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Plastics

- 5.2.2 Textile

- 5.2.3 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Indonesia

- 5.3.1.7 Malaysia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 China Petrochemical Corporation

- 6.4.2 CNPC

- 6.4.3 Eneos Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FCFC

- 6.4.6 GS Caltex Corporation

- 6.4.7 Hengli Petrochemical Co., Ltd.

- 6.4.8 Idemitsu Kosan Co.,Ltd.

- 6.4.9 Ineos

- 6.4.10 LOTTE CHEMICAL CORPORATION

- 6.4.11 PTT Global Chemical Public Company Limited

- 6.4.12 Reliance Industries Limited

- 6.4.13 Rongsheng Petrochemical Co., Ltd.

- 6.4.14 S-oil Corporation

- 6.4.15 TotalEnergies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment