|

시장보고서

상품코드

1907323

의료 시뮬레이션 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Medical Simulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

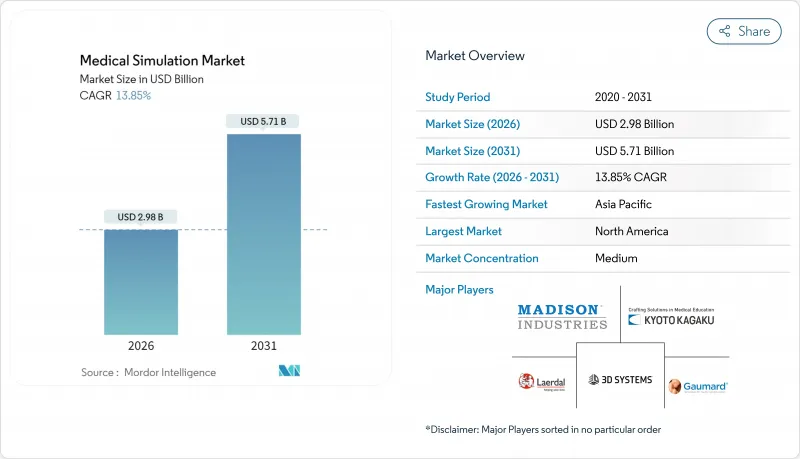

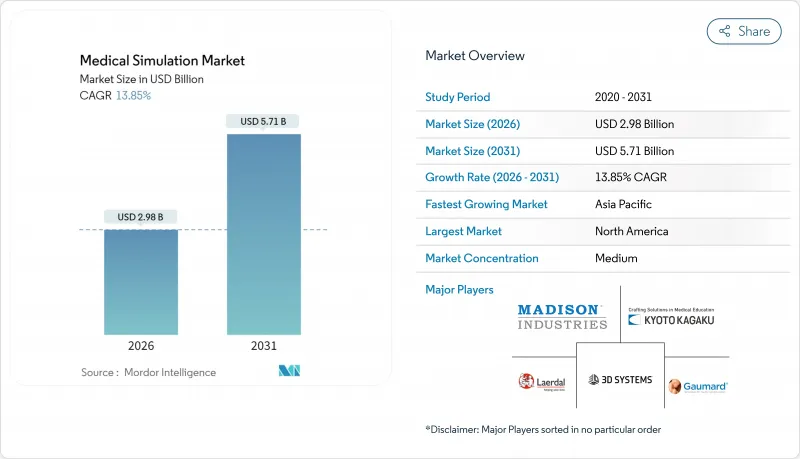

2026년 의료 시뮬레이션 시장 규모는 29억 8,000만 달러로 추정되며, 2025년 26억 2,000만 달러에서 성장을 계속하고 있습니다.

2031년까지의 예측으로는 57억 1,000만 달러에 이르고, 2026년부터 2031년에 걸쳐 CAGR 13.85%를 나타낼 것으로 전망됩니다.

촉각 대응 가상현실 기술, 인공지능을 활용한 능력 분석, 그리고 환자 안전 규제의 강화가 함께 임상 의사가 기술을 습득·유지하는 방법이 재구축되고 있습니다. 의료기관은 하드웨어 중심의 실습실에서 캠퍼스 밖에서도 훈련을 확장할 수 있는 유연한 클라우드 대응 플랫폼으로 이행하고 있습니다. 기술 공급업체 간의 통합이 가속화되고 있으며, 매디슨 인더스트리즈에 의한 2024년 CAE 헬스케어 인수가 선도 역할을 했습니다. 벤더 각사는 촉각 기술, 역각 피드백, 예측 분석에 있어서 R&D 자금을 확보하기 위해 규모 확대를 도모하고 있습니다. 북미는 의료 시뮬레이션 시장에서 여전히 가장 규모가 큰 지역 고객입니다. 그러나 아시아태평양은 병원의 확장과 정부 자금의 의학 교육 능력 향상을 배경으로 보다 빠른 성장을 보이고 있습니다.

세계의 의료 시뮬레이션 시장 동향과 인사이트

촉각 대응 및 VR/AR 시뮬레이터의 기술적 진보

햅틱 피드백과 몰입형 시각화 기술은 연구 기관에서 주류 교육 커리큘럼으로 전환하고 있습니다. 156개의 치과대학을 대상으로 하는 세계의 조사에서는 강한 관심이 있는 한편, 기술적·비용면의 장벽이 밝혀졌습니다. 응답자의 35%가 시스템의 복잡성을, 28%가 예산 부족을 과제로 꼽았습니다. 선행 도입교에서는 뛰어난 연수 성과를 학생·교원 쌍방의 모집 툴로서 활용하고 있습니다. NVIDIA와 GE Healthcare의 공동 개발을 통한 'Isaac for Healthcare' 플랫폼은 진단 영상 분야로의 전개를 보여 주며, 대상 의료 시뮬레이션 시장의 확대를 의미합니다. RetinaVR과 같은 휴대용 장치도 도입 비용을 줄이고 하드웨어 제약이 완화되고 있음을 보여줍니다.

환자 안전 의무화와 제로 햄 구상에 대한 관심 증가

규제 당국이 안전 기준을 강화함에 따라 시뮬레이션은 모든 강화 수단에서 컴플라이언스 요구 사항으로 전환하고 있습니다. 의료 시뮬레이션 학회(INACSL)는 240개가 넘는 센터를 공부하고 전문적인 정직성 기준을 충족합니다. INACSL 인증 프로그램은 높은 수강료를 설정할 수 있는 인증 제공업체의 프리미엄 계층을 형성합니다. 여러 시설에서의 연구에서는 시뮬레이션 개입 후 능력 점수가 30점 만점 중 6.3점에서 25.7점으로 상승한 것으로 기록되어 새로운 실험실 설치의 예산 정당성을 뒷받침하고 있습니다. 의료 시스템에서는 현재 시뮬레이션 예산을 재량 지출이 아닌 핵심 인프라로 취급하고 있습니다.

전체 임무 시뮬레이터의 높은 자본 비용과 수명주기 비용

종합적인 시뮬레이션 센터의 출시 비용은 1 평방 피트 당 165-1만 7,000달러로 광범위하며 자원 제한 지역에서의 액세스를 제한합니다. 이 가격 차이가 VR 스크린과 3D 프린팅 부품을 융합한 하이브리드 모델의 연구 개발을 촉진. 하드웨어 지출을 줄이면서 촉각적 요소를 유지하고 있습니다. 즉석 태스크 트레이너가 일시적인 갭을 메우고 있습니다만, 보수·교정 비용은 여전히 장벽이 되고 있습니다. 예산 압박은 사이버 보안 지출 증가로 더욱 심각해지고 있으며, 병원 IT 예산의 12-15%를 보일 것으로 예측되어 자본의 가용성을 더욱 압박하고 있습니다.

부문 분석

2025년의 수익 구성비는 제품이 55.72%를 차지했지만, 의료기관이 컨텐츠 라이브러리 및 서비스로서의 분석(Analytics-as-a-Service)으로 이행하는 가운데 서비스 소프트웨어 부문은 연율 14.53%로 성장했습니다. 서비스 소프트웨어 분야의 의료 시뮬레이션 시장 규모는 2026년부터 2031년에 걸쳐 CAGR 14.53%를 나타낼 것으로 예측되고 있습니다. 웹 호스팅 플랫폼은 고가의 마네킹 복제를 필요로 하지 않고 여러 사이트에 배포할 수 있어 학습자 1인당 지출을 줄여줍니다. AI 기반 시나리오 빌더는 목표, 대본 및 평가 기준을 자동으로 생성하여 교사 부족을 완화합니다. 하드웨어 분야에서 복강경 수술과 로봇 수술 커리큘럼 수요로 인터벤셔널 시뮬레이터는 높은 가격대를 유지하고 있습니다. 한편, 태스크 트레이너는 특정 기술 습득에 중점을 둔 비용에 중점을 둔 구매층에 호소하고 있습니다. 환자 시뮬레이터는 학부 과정에서 일정한 지위를 유지하지만 갱신주기는 완만합니다. 벤더 각사는 외과용 제품에 역각 피드백 기술을 탑재하는 케이스가 증가하고 있어, 이것에 의해 전환 비용이 상승해, 보수 수익의 안정화를 도모하고 있습니다.

2세대 클라우드 모듈은 학습 관리 시스템과 직접 연계되어 싱글 사인온을 실현함으로써 도입을 용이하게 하고 있습니다. 구독 가격 체계는 자본 지출을 운영 예산으로 이전하고 예측 가능한 현금 흐름을 요구하는 재무 부문의 요구에 부응합니다. 개방형 API 아키텍처를 통해 병원 IT 팀은 퍼포먼스 데이터를 광범위한 인력 분석 대시보드에 연결할 수 있어 부서 횡단적인 가치를 창출합니다. 소프트웨어 생태계가 성숙함에 따라 공급자는 물리 엔진의 충실도와 실시간 데이터 수집의 입도로 차별화를 도모해 단순한 다각형 수로는 차별화할 수 없게 되었습니다. 기존 하드웨어 중심공급업체보다 낮은 가격 설정을 하는 순수한 SaaS 신규 진출기업 간의 경쟁 격화가 진행되고 있습니다.

저충실도 솔루션은 합리적인 가격, 휴대성 및 유지보수의 용이성으로 2025년 시점에서 의료 시뮬레이션 시장의 43.80% 점유율을 유지했습니다. 한편 고충실도 시스템은 뛰어난 인지적 몰입감을 제공해 2031년까지 연평균 복합 성장률(CAGR) 14.39%를 나타낼 전망입니다. 연구에 따르면, 고화질 마네킹을 사용한 실험군은 평균 숙련도 점수 73.3을 달성하고 대조군의 61.4를 웃돌았습니다. 따라서 고화질 플랫폼의 의료 시뮬레이션 시장 규모는 일반 시장의 성장을 능가할 전망입니다. 중세 장치는 리얼리즘과 예산의 균형을 맞추는 기관을 위한 틈새 시장을 채우고 있으며, 완전 몰입형 스위트에의 발판으로 활용되는 경우가 많습니다.

연구 개발의 초점은 마네킹의 기계 구조에서 소프트웨어 정의의 충실도로 이동하고 있습니다. 물리 기반 엔진이 VR 환경에서 현실적인 조직 반응을 생성하는 기술입니다. 하이브리드 구성은 헤드 마운트 디스플레이와 3D 프린팅 장기 블록을 결합하여 학습자가 공간 인식과 촉각 팁을 모두 얻을 수 있도록 합니다. 센서 가격이 감소함에 따라 저충실도 작업 트레이너조차도 모션 추적 모듈을 추가하고 세분화 테두리가 모호해지고 있습니다. 성과 기반 조달이라는 시장 동향으로 구매자는 기술 사양서가 아닌 학습 효과로 충실도를 평가하게 되었습니다. 특히 인증제도가 중시되는 지역에서는 검토가능한 검증연구를 공표하는 벤더가 시장 진출 제안을 강화하고 있습니다.

지역별 분석

2025년 북미는 의료 시뮬레이션 시장의 40.92%를 나타냈습니다. 이 지역은 인정 센터의 풍부한 네트워크와 AI를 활용한 훈련 파일럿 사업을 지원하는 방위 조성금의 혜택을 받고 있습니다. 연방기구는 2025년 디지털 건강 전략의 일환으로 120개의 의료 AI 프로젝트를 명시하고 지속적인 투자를 확보했습니다. 그러나 증가하는 자본 비용과 사이버 보안 지출은 병원 구매자의 영업 이익률을 압박하고 있습니다. 캐나다에서는 CAE사가 의료부문을 매각함에 따라 트레이닝 분야의 재편이 진행되고 있어 더욱 업계 통합이 시사되고 있습니다.

다국적 공급업체는 복잡한 수입 규제를 극복하기 위해 현지 유통업체와 제휴하고 있습니다. 중국과 인도 대학은 예산 제약을 보완하기 위해 저비용 VR 키트를 채택하여 원격 훈련의 도입을 촉진합니다. 우대 조달 규칙은 제조를 현지화하고 지역 기술 지원 센터를 개설하는 공급업체를 우대합니다.

유럽에서는 환경 규제를 기반으로 일관된 확대가 계속되고 있으며, 에너지 효율이 높은 시뮬레이션 실험실로의 이행이 추진되고 있습니다. 이 지역의 호라이즌 자금은 탄소 중립 훈련 인프라 조사를 지원합니다. 병원에서는 클라우드 마이그레이션과 일반 데이터 보호 규칙(GDPR(EU 개인정보보호규정)) 준수를 비교 검토하고 하이브리드 구성을 채택하는 경우가 늘고 있습니다. 중동 및 아프리카 시장에서는 국가기금에 의한 의료도시에 대한 투자가 돌풍이 되는 한편, 인터넷 인프라의 격차가 하이파이 클라우드 스트리밍의 장벽이 되고 있습니다. 남미에서는 대학 연계를 통해 커리큘럼 컨텐츠의 수입과 언어 대응 평가 툴의 공유에 의해 능력 개발이 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 촉각 대응 및 VR/AR 시뮬레이터의 기술적 진보

- 환자 안전 의무와 "제로 햄" 이니셔티브에 대한 주목 증가

- 저침습·로봇 수술에 대한 수요 증가

- 시뮬레이션 인증 프로그램 확대(SSH, ASPIRE)

- AI를 활용한 능력 분석에 의한 개별 스킬 평가

- 탄소 중립적인 원격 시뮬레이션 실험실에 대한 정부의 장려책

- 시장 성장 억제요인

- 풀 미션 시뮬레이터의 높은 자본 비용과 라이프 사이클 비용

- 개발도상국에서의 훈련예산의 자금 부족

- 교원 연수와 커리큘럼 통합의 복잡성

- 클라우드 플랫폼에서의 사이버 보안 및 학습자 데이터의 프라이버시에 관한 우려

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 및 서비스별

- 제품

- 중재적/수술 시뮬레이터

- 복강경 수술

- 로봇 및 내시경

- 정형외과

- 환자 시뮬레이터

- 작업 훈련기

- 기타 제품

- 중재적/수술 시뮬레이터

- 서비스 및 소프트웨어

- 웹 기반 시뮬레이션

- 시뮬레이션 소프트웨어 라이선스

- 교육 및 컨설팅 서비스

- 제품

- 충실도별

- 고충실도

- 중충실도

- 저충실도

- 최종 사용자별

- 학술 및 연구 기관

- 병원 및 수술 센터

- 군 및 방위 기관

- 의료기기 및 제약기업

- 배포 모드별

- On-Premise형 시뮬레이션 실험실

- 클라우드 기반 및 원격 플랫폼

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Laerdal Medical

- 3D Systems

- Gaumard Scientific

- Limbs & Things

- Simulab Corporation

- VirtaMed AG

- Surgical Science Sweden AB

- Inovus Medical

- SimX

- Medical-X

- IngMar Medical

- Operative Experience

- 3B Scientific(Cardionics)

- Nasco Healthcare

- Mentice AB

- Kyoto Kagaku

- Simulaids Inc.

- Avkin

- EchoPixel

- Madison Industries

제7장 시장 기회와 향후 전망

KTH 26.01.20Medical simulation market size in 2026 is estimated at USD 2.98 billion, growing from 2025 value of USD 2.62 billion with 2031 projections showing USD 5.71 billion, growing at 13.85% CAGR over 2026-2031.

A convergence of haptic-enabled virtual reality, artificial-intelligence competency analytics, and tightening patient-safety mandates is reshaping how clinicians acquire and maintain skills. Institutions are migrating from hardware-centric labs toward flexible, cloud-supported platforms that extend training beyond campus walls. Consolidation among technology suppliers is accelerating, led by Madison Industries' 2024 purchase of CAE Healthcare, as vendors seek scale to fund R&D in haptics, force feedback, and predictive analytics. North America remains the largest regional customer for the medical simulation market. Yet, Asia-Pacific is growing faster on the back of hospital expansion and government-funded medical-education capacity upgrades.

Global Medical Simulation Market Trends and Insights

Technological Advances in Haptic-Enabled & VR/AR Simulators

Haptic feedback and immersive visualisation have moved from research labs into mainstream curricula. A global survey of 156 dental schools confirmed strong interest but highlighted technical and cost barriers, with 35% citing system complexity and 28% flagging budget shortfalls. Successful early adopters now use superior training outcomes as a recruitment tool for both students and faculty. NVIDIA's joint work with GE HealthCare on the Isaac for Healthcare platform illustrates crossover into diagnostic imaging, broadening the addressable medical simulation market. Portable units such as RetinaVR are also lowering entry costs, signalling that hardware constraints are diminishing.

Growing Focus on Patient-Safety Mandates & Zero-Harm Initiatives

Simulation has shifted from optional enhancement to compliance requirement as regulators tighten safety metrics. The Society for Simulation in Healthcare has accredited more than 240 centres that must satisfy debriefing and professional-integrity standards. Endorsement programs from INACSL are creating a premium tier of certified providers that command higher tuition fees. A multi-centre study recorded competency scores rising from 6.3 to 25.7 out of 30 after simulation intervention, reinforcing budget justification for new labs. Health systems now treat simulation budgets as core infrastructure rather than discretionary expenditure.

High Capital & Lifecycle Costs of Full-Mission Simulators

Start-up costs for a comprehensive simulation centre range from USD 165 to 17,000 per square foot, restricting access in resource-constrained regions. This price wedge has fuelled R&D into hybrid models that blend VR screens with 3D-printed components, reducing hardware outlays while preserving tactile cues. Improvised task trainers are bridging gaps temporarily, although maintenance and calibration expenses remain a hurdle. Budget pressure is compounded by the rise in cybersecurity spending, forecast to reach 12-15% of hospital IT allocations, further squeezing capital availability.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Minimally-Invasive & Robotic Procedures

- AI-Driven Competency Analytics for Personalised Skill-Scoring

- Cyber-Security & Learner-Data Privacy Concerns in Cloud Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Products accounted for 55.72% of revenue in 2025, yet Services & Software are growing 14.53% annually as institutions pivot toward content libraries and analytics-as-a-service. The medical simulation market size for Services & Software is projected to expand at 14.53% CAGR between 2026 and 2031. Web-hosted platforms enable multi-site deployments without replicating costly manikins, reducing per-learner spend. AI-based scenario builders mitigate faculty shortages by auto-generating objectives, scripts and assessment rubrics. Within hardware, interventional simulators remain premium-priced due to laparoscopic and robotic curriculum demand. Task trainers, meanwhile, appeal to cost-sensitive buyers focusing on discrete competencies. Patient simulators retain a foothold in undergraduate programs but face slower replacement cycles. Vendors increasingly bundle force-feedback patents into surgical offerings, raising switching costs and locking in maintenance revenue streams.

Second-generation cloud modules now integrate directly with learning-management systems for single-sign-on, easing adoption. Subscription pricing shifts capital expenditure to operating budgets, pleasing finance departments that seek predictable cash flows. Open-API architectures enable hospital IT teams to feed performance data into broader workforce analytics dashboards, creating cross-departmental value. As software ecosystems mature, providers differentiate through fidelity of physics engines and real-time data capture granularity rather than raw polygon count. Competitive intensity is rising among pure-play SaaS entrants that undercut legacy hardware-centric suppliers.

Low-fidelity solutions kept 43.80% share of the medical simulation market in 2025 because they are affordable, portable and easy to maintain. High-fidelity systems, however, deliver superior cognitive immersion and are growing at 14.39% CAGR through 2031. Studies show experimental groups using high-fidelity manikins achieved mean competency scores of 73.3, outperforming control cohorts at 61.4. The medical simulation market size for high-fidelity platforms will therefore outpace general market growth. Medium-fidelity devices fill a niche for institutions balancing realism and budget, often serving as a stepping stone toward full immersive suites.

R&D focus has shifted from mannequin mechanics to software-defined fidelity where physics-based engines generate realistic tissue response in VR settings. Hybrid configurations marry head-mounted displays with 3D-printed organ blocks so learners gain both spatial orientation and tactile cues. As sensor prices fall, even low-fidelity task trainers are adding motion-tracking modules, blurring segmentation lines. The market trend toward outcome-based procurement prompts buyers to evaluate fidelity on learning gains rather than technical specification sheets. Vendors that publish peer-reviewed validation studies are strengthening their go-to-market propositions, especially in accreditation-driven regions.

The Medical Simulation Market Report is Segmented by Products & Services (Products [Surgical Simulators, Patient Simulators, and More]; Services & Software [Web-Based Simulation, and More]), Fidelity (High-Fidelity, Medium-Fidelity, and More), End User (Academic and More), Delivery Mode, and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commands 40.92% of the medical simulation market in 2025. The region benefits from a deep roster of accredited centers and defense grants that underwrite AI-powered training pilots. Federal agencies itemized 120 medical AI projects as part of the 2025 Digital Health Strategy, ensuring sustained investment. Yet rising capital costs and cybersecurity spending dilute operating margins for hospital buyers. Canada's training sector is realigning after CAE divested its healthcare unit, signalling further consolidation.

Multinational suppliers partner with local distributors to navigate fragmented import regulations. Colleges in China and India adopt low-footprint VR kits to offset budget constraints, boosting remote training adoption. Preferential procurement rules favour vendors that localize manufacturing or open regional tech-support centres.

Europe maintains consistent expansion anchored in environmental regulations that push toward energy-efficient simulation labs-the region's Horizon funding streams back research into carbon-neutral training infrastructures. Hospitals weigh cloud migration against compliance with the General Data Protection Regulation and often adopt hybrid topologies. Middle East and Africa markets benefit from sovereign-wealth investment in flagship medical cities but face uneven internet infrastructure that limits high-fidelity cloud streaming. South America develops capabilities through university partnerships that import curriculum content and share language-localised assessment tools.

- Laerdal Medical

- 3D Systems

- Gaumard Scientific

- Limbs & Things

- Simulab

- VirtaMed

- Surgical Science Sweden

- Inovus Medical

- SimX

- Medical-X

- Ingmar Medical

- Operative Experience

- 3B Scientific (Cardionics)

- Nasco Healthcare

- Mentice

- Kyoto Kagaku

- Simulaids

- Avkin

- EchoPixel

- Madison Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Advancements in Haptic-enabled & VR/AR Simulators

- 4.2.2 Growing Focus on Patient-safety Mandates & "Zero-harm" Initiatives

- 4.2.3 Rising Demand for Minimally-invasive & Robotic Procedures

- 4.2.4 Expansion of Simulation Accreditation Programs (SSH, ASPIRE)

- 4.2.5 AI-driven Competency Analytics for Personalized Skill-scoring

- 4.2.6 Government Incentives for Carbon-neutral Remote Simulation Labs

- 4.3 Market Restraints

- 4.3.1 High Capital & Lifecycle Costs of Full-mission Simulators

- 4.3.2 Funding Gaps in Developing Economies' Training Budgets

- 4.3.3 Faculty-training & Curriculum-integration Complexity

- 4.3.4 Cyber-security & Learner-data Privacy Concerns in Cloud Platforms

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value-USD)

- 5.1 By Products & Services

- 5.1.1 Products

- 5.1.1.1 Interventional/Surgical Simulators

- 5.1.1.1.1 Laparoscopic

- 5.1.1.1.2 Robotic & Endoscopic

- 5.1.1.1.3 Orthopaedic

- 5.1.1.2 Patient Simulators

- 5.1.1.3 Task Trainers

- 5.1.1.4 Other Products

- 5.1.1.1 Interventional/Surgical Simulators

- 5.1.2 Services & Software

- 5.1.2.1 Web-based Simulation

- 5.1.2.2 Simulation Software Licences

- 5.1.2.3 Training & Consulting Services

- 5.1.1 Products

- 5.2 By Fidelity

- 5.2.1 High-fidelity

- 5.2.2 Medium-fidelity

- 5.2.3 Low-fidelity

- 5.3 By End User

- 5.3.1 Academic & Research Institutes

- 5.3.2 Hospitals & Surgical Centres

- 5.3.3 Military & Defense Organizations

- 5.3.4 Medical-device & Pharma Companies

- 5.4 By Delivery Mode

- 5.4.1 On-premise Simulation Labs

- 5.4.2 Cloud-based / Remote Platforms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Laerdal Medical

- 6.3.2 3D Systems

- 6.3.3 Gaumard Scientific

- 6.3.4 Limbs & Things

- 6.3.5 Simulab Corporation

- 6.3.6 VirtaMed AG

- 6.3.7 Surgical Science Sweden AB

- 6.3.8 Inovus Medical

- 6.3.9 SimX

- 6.3.10 Medical-X

- 6.3.11 IngMar Medical

- 6.3.12 Operative Experience

- 6.3.13 3B Scientific (Cardionics)

- 6.3.14 Nasco Healthcare

- 6.3.15 Mentice AB

- 6.3.16 Kyoto Kagaku

- 6.3.17 Simulaids Inc.

- 6.3.18 Avkin

- 6.3.19 EchoPixel

- 6.3.20 Madison Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment