|

시장보고서

상품코드

1907327

선박용 코팅 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Marine Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

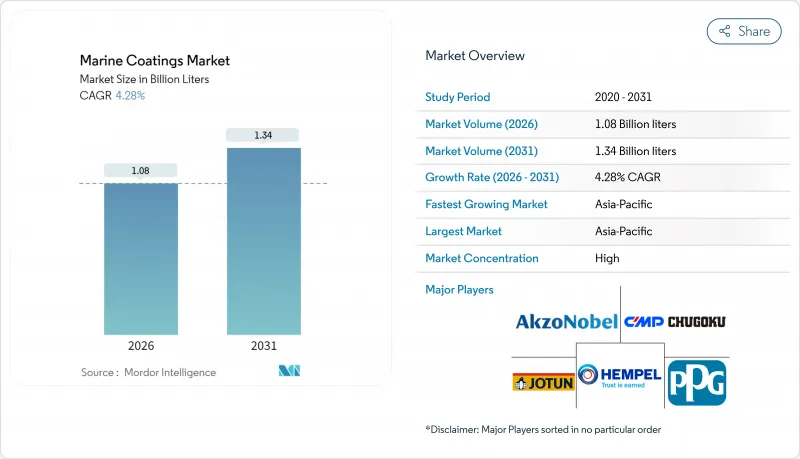

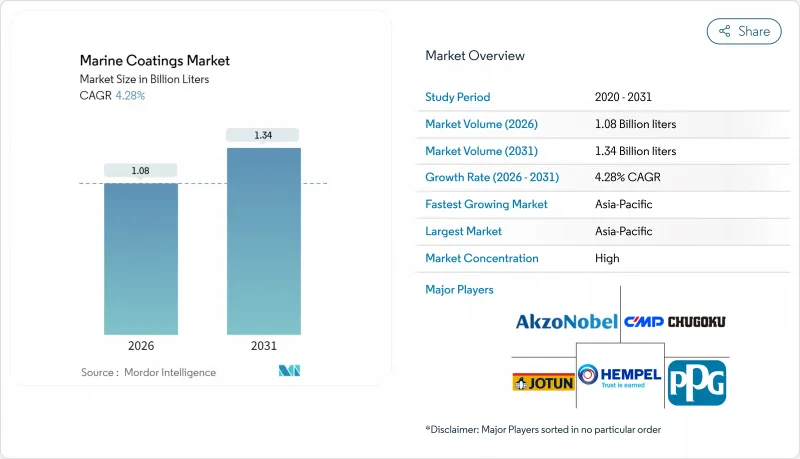

2026년 선박용 코팅 시장 규모는 10억 8,000만 리터로 추정되며, 2025년 10억 4,000만 리터에서 성장했으며, 2031년에는 13억 4,000만 리터에 이를 것으로 예상됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 4.28%를 나타낼 전망입니다.

국제해사기관(IMO)에 의한 성능요구가 엄격한 규제, 특히 에너지효율 기존 선박지수(EEXI) 및 탄소강도지표(CII)에 의해 도료는 유지관리비용에서 연료비와 탄소 배출량을 삭감하는 최전선의 해결책으로 격상되었습니다. 아시아태평양은 세계 시장의 압도적 점유율을 차지하며, 2024년에는 전 선박용 코팅의 72.11%를 공급했습니다. 이는 중국이 신조선 수주의 69%라는 압도적인 점유율을 쥐고 있는 것 외에 한국이 20% 미만의 점유율을 유지하고 있기 때문입니다. 카니발 코퍼레이션이 2024년에 기록한 250억 달러의 수익과 2025년에 예정된 16척의 신조원양 크루즈선의 납품 스케줄은 구조적인 회복을 나타내며, 이는 프리미엄 페인트 수요 증가로 이어졌습니다. 모든 의사결정 포인트, 수지, 기술, 응용 분야에서 시장은 측정가능한 연료 절약, 저탄소 강도 점수 및 더 긴 서비스 간격을 약속하는 솔루션으로 전환하고 있으며, 가치는 더 이상 티켓 가격이 아니라 수명 주기 경제성에 있다는 핵심 주제를 뒷받침합니다.

세계의 선박용 코팅 시장 동향과 인사이트

레저보트 및 크루즈선 생산 증가

레저 크루즈는 확실히 성장 궤도로 돌아왔으며, 크루즈라인 국제협회(CLIA)는 2027년까지 승객 수가 4,000만명에 달할 것으로 예측하고 있습니다(2024년 3,170만명에서 증가). 대규모 항로와 장기 항해로 인해 운항사는 뛰어난 광택 유지와 긴 도크 간격을 제공하는 프리미엄 실리콘 또는 하이브리드 탑 코트를 지정하는 경향이 있습니다. 중국이 크루즈선 건조국으로서 대두(국내 2척째의 선체 현재 조립중)한 것으로, 새로운 생산 능력이 더해지는 한편, 고급 외장 도료의 잠재 수요도 확대하고 있습니다. 2025년 취항 예정인 16척의 크루즈선 중 8척이 LNG 추진을 채용하기 위해, 벙커 작업시의 -163℃에 견디는 극저온 대응 탱크 코팅 및 연료 라인 배리어가 요구되었습니다. 레크리에이션 보트 분야에서 지속적인 가구 소득과 유연한 원격 근무 모델은 프리미엄 해양 마감의 장기 수요를 지원합니다. 이러한 동향이 결합되어 상업화물 부문에 비해 평균 판매 가격과 이익률이 상승하여 선박용 코팅 시장에서 CAGR을 1.2포인트 밀어 올리는 호영향을 강화하고 있습니다.

선박수리·독입량 증가

홍해 위기에 의한 유지 보수의 연기가 아시아의 조선소를 혼잡하게 하고, 정기용선 사업자는 최대 1년 앞까지 예약을 메우는 상황입니다. 이 백로그는 현재 선체 세정·재도장 수요의 상승 사이클로 전환하고 있어 특히 CII 스코어링의 엄격화에 직면하는 파나맥스·스에즈맥스급 선박에서 현저합니다. 다멘십 리페어 로테르담사의 대표 프로젝트는 이러한 변화를 여실히 보여주고 있으며, 선주는 기존의 박리형 방오 도료와 비교하여 5-6%의 연료 절약 효과를 약속하는 실리콘계 저마찰 코팅으로의 개수를 진행하고 있습니다. 학술적 모델링에 따르면 최적의 세척 사이클로 선박 1척당 연간 연료비를 1만 402-2만 6,685달러 줄일 수 있어 투자 회수의 합리성을 뒷받침하고 있습니다. 수요가 가장 강한 것은 세계에서 가장 오래된 상용선대가 집중하는 아시아태평양입니다만, EU 배출량 거래 제도(EU-ETS)의 과금 개시를 앞두고, 유럽·북미에서도 같은 수요 급증을 볼 수 있습니다. 그 결과 수리 수요에 견인된 소비가 전체 성장률을 0.9포인트 밀어 올리고 있습니다.

엄격한 VOC 및 살생물제 규제

2023년 1월 발효한 국제해사기관(IMO)에 의한 시부트린 금지조치는 주요 방오방오제를 하룻밤으로 배제하고, 조제업체에 설계변경사이클의 가속을 강요했습니다. 유럽이 2024년부터 중국산 이산화티타늄에 부과하는 반덤핑 관세는 안료비용을 두자릿수 상승시켜, 지역도료연맹이나 헤지 규모가 부족한 중소도료 제조업체의 반발을 초래했습니다. 워싱턴주의 구리 사용 금지 연기는 환경 목표와 기술적 실현 가능성 사이에서 진행되는 규제의 줄을 가리키고 있지만, 2029년까지의 지속적인 조사는 더 엄격한 규제 상한이 연기된 것만으로 철회된 것은 아님을 시사합니다. 업계 동향은 수성 페인트와 실리콘계 시스템으로의 전환을 향하고 있지만, 이들은 원재료비와 검증비용이 높습니다. 세계 연구개발센터가 없는 중소기업은 필요한 독성학 기준의 자금 조달을 고민하고 있으며, 선박용 코팅 시장 예측 성장률을 0.8포인트 낮추고 있습니다.

부문 분석

방오 시스템은 2025년 수요의 46.75%를 차지하고 선박용 코팅 시장 규모를 견인했습니다. 이것은 선체의 평활성, 연료 소비, CII 점수에 대한 직접적인 영향을 입증합니다. 방오 릴리스계 화학제품은 구리 불사용의 의무화와 환경 인증을 우선하는 전세 계약 조항 증가를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 4.52%를 나타낼 것으로 전망됩니다.

규모의 크기에도 불구하고, 자기 연마형 방오 도료는 살생물제 유출에 대한 규제 모니터링으로 성장 한계에 직면하고 있습니다. 한편, 실리콘 및 불소수지계 방오 릴리스 도료는 초기 비용이 높고 라이프타임 배출량이 적고 유지보수 간격이 길기 때문에 선박용 코팅 시장 내에서의 꾸준한 이행 경로를 강화하고 있습니다. 자기 복구 첨가제에 대한 산학 공동 연구의 지속은 다음 혁신의 파도를 시사합니다. 마이크로캡슐이 부식방지제를 방출하거나 흠집을 채우기 위해 중합함으로써 도킹 간격을 더욱 연장할 수 있습니다.

2025년 출하량에서 알키드계 도료는 54.10%를 차지하며, 비용, 분무성, 세계의 이용 가능성에 관한 수십년에 걸친 최적화를 반영했습니다. 그러나, 이 우위성은 현재 폴리우레탄에 의해 과제를 받고 있으며, 규제가 LNG나 수소 탱크에 적합한 고강도·저막 두께 라이닝을 지지하는 가운데, 2031년까지 연평균 복합 성장률(CAGR) 4.33%를 나타낼 것으로 예측되고 있습니다.

폴리우레탄의 대두는 광택이나 내마모성을 손상시키지 않고 VOC 규제 상한치를 준수하는 수성 2액형 시스템의 진보에 의해 뒷받침되고 있어, 크루즈선의 상부 구조물이나 상부 구조 구역에서의 사양 채용에 공헌하고 있습니다. 병렬로 진행되는 동적 디설파이드 교환 반응의 조사에 의해 상온에서 미세한 균열을 수리하는 자기 수복층이 실현되고 있습니다. 이 특성은 해군 함정의 유지 보수 시간을 줄일 수 있습니다. 이러한 진전에 의해 알키드 수지는 선박용 코팅 시장에 있어서 코스트 중시의 작업선용 틈새 시장을 유지하면서도, 점유율을 서서히 양도하게 됩니다.

본 선박용 코팅 시장 보고서는 유형별(방식 도료, 방오 도료, 오손 방지 도료, 습기 경화형), 수지별(에폭시, 폴리우레탄, 아크릴, 알키드, 기타), 기술별( 수성, 용제계, UV경화형, 분체), 용도별(선박 OEM, 선박 애프터마켓), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)으로 분류되어 있습니다. 시장 예측은 수량(리터) 단위로 제공됩니다.

지역별 분석

아시아태평양의 71.60%라는 점유율은 이 지역이 세계 조선업의 중심지 역할을 하고 있음을 보여줍니다. 중국 단독으로 미납 선박 수주의 69%를 차지하고 있어 이 규모는 운임 사이클이 어떻게 변화해도 최저한의 도료 사용량을 보증하는 것입니다. 2031년까지 지역 CAGR 4.58%는 크루즈선 건조 확대, 연안 무역 증가, 일본·한국·대만 앞바다에서의 초기 단계의 해상풍력발전 프로젝트에 의해 견인됩니다. 일본의 국내 조선소를 위한 69억 달러의 지원책(미국 해군 함정용 서비스에 충당된다)은 고급 프라이머 및 선체 시스템용의 새로운 고부가가치 시장을 창출합니다.

유럽은 규제 엄격화의 지표이며, 고급 요트, 페리, 해양 인프라 분야의 점유율이 도료 수요의 다양성과 기술 집약성을 유지하고 있습니다. EU가 2025년 1월보다 5,000톤 이상의 선박을 배출량거래제도에 통합한 결정은 선주에게 탄소배출 비용 절감이 가능한 저저항·저용제 대체품의 선택을 촉구했습니다. 부유식 풍력 발전의 264GW 글로벌 목표는 상당 부분이 스코틀랜드, 노르웨이 및 이베리아 해안에 설치될 것으로 예상되며, 이는 최상위 공급업체만이 제공할 수 있는 25년 보증이 적용되는 스플래시 존 패키지를 필요로 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 레저보트 및 크루즈선의 생산 증가

- 선박 수리 및 독입량 증가

- 보다 엄격한 국제 해사기구(IMO)의 EEXI 및 CII 연료 효율 규제

- 중부하 도료를 필요로 하는 해상 재생에너지 설비의 급증

- 구리 프리 방오제 배합으로의 이행

- 시장 성장 억제요인

- 엄격한 VOC 및 살생물제 규제

- 에폭시 수지 및 산화티탄의 가격 변동성

- 높은 도포·유지 관리 비용

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 진입업자의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 방청

- 방오

- 오염 이탈

- 습기 경화

- 수지별

- 에폭시

- 폴리우레탄

- 아크릴

- 알키드

- 기타(불소수지, 폴리에스테르 등)

- 기술별

- 수성

- 용제계

- UV 경화

- 분체

- 용도별

- 선박 OEM

- 선박 애프터마켓

- 지역별

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 말레이시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AkzoNobel NV

- Arkema SA(Bostik Yacht Coatings)

- Axalta Coating Systems

- BASF SE

- BOERO BARTOLOMEO SpA

- Carboline Company

- Chugoku Marine Paints Ltd.

- Engineered Marine Coatings LLC

- Hempel A/S

- Jotun

- Kansai Paint Marine Co., Ltd.

- KCC Corporation

- MCU Coating International

- Nippon Paint Marine Coatings Co. Ltd.

- Pettit Marine Paints

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

제7장 시장 기회와 향후 전망

KTH 26.01.20Marine Coatings Market size in 2026 is estimated at 1.08 billion liters, growing from 2025 value of 1.04 billion liters with 2031 projections showing 1.34 billion liters, growing at 4.28% CAGR over 2026-2031.

Performance-demanding regulations from the International Maritime Organization (IMO), notably the Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII), have elevated coatings from a maintenance cost to a frontline solution for cutting fuel bills and carbon emissions. Asia Pacific commands the lion's share of global activity, supplying 72.11% of all marine-grade coatings in 2024, thanks to China's unrivalled 69% grip on new-build orders, while South Korea's share lingers below 20%. Carnival Corporation's record USD 25 billion revenue in 2024 and the delivery schedule of 16 new oceangoing cruise vessels in 2025 signal a structural rebound that is translating into premium coating demand. Across every decision point-type, resin, technology, and application-the market is pivoting toward solutions that promise measurable fuel savings, lower carbon intensity scores, and longer service intervals, underlying the central theme that value now lies in life-cycle economics instead of ticket price.

Global Marine Coatings Market Trends and Insights

Increase in Production of Leisure Boats & Cruise Ships

Leisure cruising is firmly back in growth mode, with the Cruise Lines International Association projecting 40 million passengers by 2027, up from the 31.7 million carried in 2024. Larger itineraries and longer voyages are leading operators to specify premium silicone or hybrid topcoats that deliver superior gloss retention and longer dry-dock intervals. China's emergence as a cruise-ship builder-its second domestic hull is now in assembly-adds fresh capacity yet also widens the addressable demand for high-end exterior paints. LNG propulsion on eight of the 16 cruise vessels scheduled for 2025 requires cryogenic-ready tank coatings and fuel-line barriers that can handle -163 °C during bunker operations. In the recreational boating domain, sustained household income and flexible remote-work models underpin long-run demand for premium marine finishes. Together, these trends lift average selling prices and margins versus commercial cargo segments, reinforcing the sector's positive 1.2 percentage-point lift on the marine coatings market CAGR.

Growing Ship-Repair & Dry-Docking Volumes

Deferred maintenance from the Red Sea crisis has crowded Asian yards, pushing time-charter operators to book slots up to a year in advance. The backlog is now translating into an up-cycle in hull cleaning and repainting, especially on Panamax and Suezmax tonnage that face stricter CII scoring. Damen Shiprepair Rotterdam's showcase projects illustrate the shift: owners are retrofitting silicon-based low-friction coatings that promise 5-6% fuel savings over conventional ablative antifoulings. Academic modelling shows that optimal cleaning cycles can shave USD 10,402-26,685 off annual bunker bills per vessel, reinforcing payback logic. Demand is strongest in Asia Pacific, home to the world's oldest commercial fleet mix, but Europe and North America are seeing similar spikes as EU-ETS charges loom. As a result, repair-driven consumption is supplying a +0.9 percentage-point lift to overall growth.

Stringent VOC & Biocide Regulations

The IMO cybutryne prohibition, effective January 2023, removed a mainstay antifouling biocide overnight, forcing formulators into accelerated redesign cycles. Europe's anti-dumping duties on Chinese titanium dioxide from 2024 have hiked pigment costs by double digits, sparking opposition from the regional paint federation and smaller coating makers that lack hedging scale. Washington State's postponement of its copper ban illustrates the regulatory tightrope between environmental ambition and technical feasibility, yet continued studies through 2029 signal that stricter caps are only deferred, not cancelled. Industry response is trending toward waterborne and silicone systems, but these carry higher raw-material and validation costs. Smaller manufacturers without global R&D centers struggle to fund the necessary toxicology benchmarks, trimming 0.8 percentage points off forecast growth for the marine coatings market.

Other drivers and restraints analyzed in the detailed report include:

- Stricter IMO EEXI & CII Fuel-Efficiency Mandates

- Surge in Offshore Renewable Installations Requiring Heavy-Duty Coatings

- Volatile Epoxy & Titanium-Oxide Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anti-fouling systems led the marine coatings market size by generating 46.75% of 2025 demand, a testament to their direct impact on hull smoothness, bunker consumption, and CII scoring. Foul-release chemistries are projected to climb at a 4.52% CAGR to 2031, propelled by copper-free mandates and rising charter-party clauses that prioritise green credentials.

Despite their scale, self-polishing anti-foulings face a growth ceiling due to regulatory scrutiny on biocide run-off. In contrast, silicone and fluoropolymer foul-release options offer owners higher-upfront costs but lower lifetime emissions and longer maintenance windows, reinforcing a steady migration path within the marine coatings market. Continued university-industry consortia on self-healing additives point to the next wave of innovation, where micro-capsules release corrosion inhibitors or polymerise to fill scratches, extending docking cycles even further.

Alkyds accounted for 54.10% of litres shipped in 2025, reflecting decades-long optimisation around cost, sprayability, and global availability. That dominance, however, is now being tested by polyurethane, which is forecast to expand at 4.33% CAGR through 2031 as regulations favour tougher, low-film-thickness linings suited to LNG and hydrogen tanks.

Polyurethane's rise is aided by advances in waterborne two-component systems that comply with VOC caps without sacrificing gloss or abrasion resistance, helping them win specifications on cruise superstructure and topside areas. Parallel research on dynamic disulfide exchange reactions is delivering self-healing layers capable of restoring micro-cracks at ambient temperature, an attribute that could reduce maintenance hours aboard navy vessels. These developments ensure that alkyds will cede share incrementally even as they retain cost-sensitive workboat niches within the marine coatings market.

The Marine Coatings Market Report is Segmented by Type (Anti-Corrosion, Antifouling, Foul Release, Moisture Cure), Resin (Epoxy, Polyurethane, Acrylic, Alkyd, Other), Technology (Water-Borne, Solvent-Borne, UV-Cured, Powder), Application (Marine OEM, Marine Aftermarket), and Geography (Asia Pacific, North America, Europe, South America, Middle East & Africa). The Market Forecasts are Provided in Terms of Volume (Liters).

Geography Analysis

Asia Pacific's 71.60% share underscores the region's role as the heartbeat of global shipbuilding. China alone holds a 69% slice of pending vessel orders, a scale that guarantees baseline coating volumes whatever the freight cycle does. The regional CAGR of 4.58% to 2031 is propelled by expanding cruise ship fabrication, rising coastal trade, and early-stage floating wind projects off the coasts of Japan, Korea, and Taiwan. Japan's USD 6.9 billion shot-in-the-arm for domestic yards, earmarked to service US naval tonnage, adds another high-specification outlet for advanced primers and hull systems.

Europe remains the bellwether for regulatory stringency, and its share of premium yacht, ferry, and offshore infrastructure keeps coatings demand both diverse and technology intensive. The EU's decision to fold vessels over 5,000 GT into its Emissions Trading System from January 2025 incentivises owners to pick low-drag, low-solvent alternatives that can shave carbon exposure costs. Floating wind's 264 GW global target envisions a substantial portion anchored off Scottish, Norwegian and Iberian coasts, requiring splash-zone packages with 25-year warranties that only top-tier suppliers can deliver.

- AkzoNobel N.V.

- Arkema S.A. (Bostik Yacht Coatings)

- Axalta Coating Systems

- BASF SE

- BOERO BARTOLOMEO S.p.A.

- Carboline Company

- Chugoku Marine Paints Ltd.

- Engineered Marine Coatings LLC

- Hempel A/S

- Jotun

- Kansai Paint Marine Co., Ltd.

- KCC Corporation

- MCU Coating International

- Nippon Paint Marine Coatings Co. Ltd.

- Pettit Marine Paints

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in production of leisure boats and cruise ships

- 4.2.2 Growing ship-repair and dry-docking volumes

- 4.2.3 Stricter IMO EEXI and CII fuel-efficiency mandates

- 4.2.4 Surge in offshore renewable installations requiring heavy-duty coatings

- 4.2.5 Shift toward copper-free antifouling formulations

- 4.3 Market Restraints

- 4.3.1 Stringent VOC and biocide regulations

- 4.3.2 Volatile epoxy and titanium-oxide prices

- 4.3.3 High Application and Maintenance Costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Anti-corrosion

- 5.1.2 Antifouling

- 5.1.3 Foul Release

- 5.1.4 Mositure Cure

- 5.2 By Resin

- 5.2.1 Epoxy

- 5.2.2 Polyurethane

- 5.2.3 Acrylic

- 5.2.4 Alkyd

- 5.2.5 Other (Fluoropolymer, Polyester etc)

- 5.3 By Technology

- 5.3.1 Water-borne

- 5.3.2 Solvent-borne

- 5.3.3 UV-cured

- 5.3.4 Powder

- 5.4 By Application

- 5.4.1 Marine OEM

- 5.4.2 Marine Aftermarket

- 5.5 By Geography

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 South Korea

- 5.5.1.4 India

- 5.5.1.5 Malaysia

- 5.5.1.6 Vietnam

- 5.5.1.7 Rest of Asia Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Nigeria

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Arkema S.A. (Bostik Yacht Coatings)

- 6.4.3 Axalta Coating Systems

- 6.4.4 BASF SE

- 6.4.5 BOERO BARTOLOMEO S.p.A.

- 6.4.6 Carboline Company

- 6.4.7 Chugoku Marine Paints Ltd.

- 6.4.8 Engineered Marine Coatings LLC

- 6.4.9 Hempel A/S

- 6.4.10 Jotun

- 6.4.11 Kansai Paint Marine Co., Ltd.

- 6.4.12 KCC Corporation

- 6.4.13 MCU Coating International

- 6.4.14 Nippon Paint Marine Coatings Co. Ltd.

- 6.4.15 Pettit Marine Paints

- 6.4.16 PPG Industries Inc.

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment