|

시장보고서

상품코드

1907337

폴리메틸메타크릴레이트(PMMA) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Polymethyl Methacrylate (PMMA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

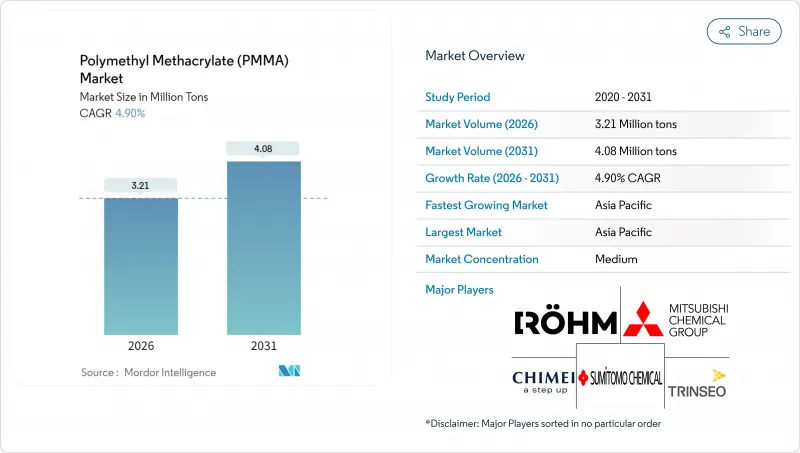

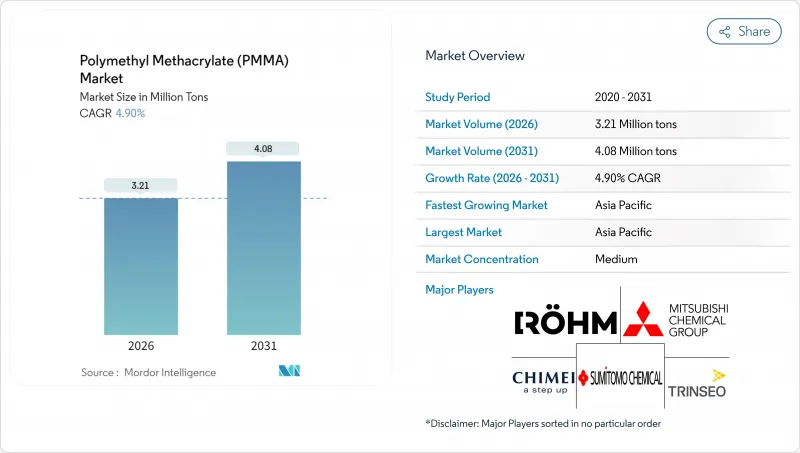

폴리메틸메타크릴레이트(PMMA) 시장 규모는 2026년 321만 톤에 달할 것으로 예측되고 있습니다.

이는 2025년 306만 톤에서 성장한 수치이며 2031년에는 408만 톤에 이를 전망입니다. 2026-2031년에 걸쳐는 CAGR 4.90%로 성장을 계속할 것으로 예측되고 있습니다.

자동차 경량화, 건축용 유리, LED 디스플레이로부터의 견고한 수요가 메틸 메타크릴레이트(MMA) 원료 가격 변동성 속에서도 성장을 지속시키고 있습니다. PMMA의 광학 투명도, 자외선 안정성, 간편한 가공성은 경쟁 폴리머와의 차별점을 제공하여 핵심 용도에서 대체 압력으로부터 판매량을 보호합니다. 지역별 과잉 생산 능력(특히 중국)은 가격 경쟁력을 유지시키는 반면, 획기적인 화학 재활용 파일럿 프로젝트는 순환형 생산 모델로의 길을 열어주고 있습니다. 생산사들은 PMMA 시장에서 방어 전략으로 수직 통합과 특수 등급 개발을 우선시하고 있습니다.

세계의 폴리메틸메타크릴레이트(PMMA) 시장 동향 및 인사이트

자동차 경량화 및 조명 수요

전기차 제조사들은 PMMA를 파노라마 선루프, 테일램프 커버, 센서 하우징에 적용합니다. 이 폴리머는 유리보다 무게가 50% 가벼우면서도 높은 광학 품질을 제공하기 때문입니다. 적응형 LED 시스템으로의 기술 전환은 정밀한 빔 패턴을 형성하는 로옴의 광 관리 등급 수요를 증폭시킵니다. 저이방성 특성이 요구되는 자율주행차용 LiDAR 렌즈에서도 추가 수요가 발생합니다. 새로운 내충격성 폴리카보네이트(PC) 공중합체가 등장했음에도, 비용 및 자외선 내구성이 미미한 강도 향상보다 우세한 PMMA 시장의 회복력은 지속됩니다.

건축 글레이징 외관에 채택

스마트 빌딩 외관에는 이제 센서와 가열 요소가 내장된 PMMA 시트가 통합되어 일광 관리, 결로 방지, 자가 세척 기능을 수행합니다. PMMA는 가시광선 투과율이 92-93%로 PC(86-89%)보다 높아 유럽 건축 규정의 에너지 효율 인증을 지원합니다. PMMA 패널에 디지털 인쇄를 적용하면 복합 재료 조립 없이도 복잡한 외벽 디자인이 가능해 설치 시간이 단축됩니다. 고층 프로젝트의 화재 규정 제한으로 여전히 보급률이 제한되나, 장기 보증과 자외선 저항성으로 투명성과 미관이 중요한 분야에서 PMMA의 경쟁력은 유지됩니다.

MMA 원료 가격 변동성

MMA 가격 변동은 석유화학 원료 추세를 반영하며, 에너지 집약적 공정으로 인해 증폭됩니다. 트린스오는 2025년 3월 프로필렌 비용 급등으로 변환업체 마진이 압박되자 유럽 PMMA 가격을 톤당 250유로 인상했습니다. 유럽과 같은 수입 의존 지역은 바이오 기반 또는 재활용 MMA가 상업적으로 확대되기 전까지 취약한 상태를 유지할 것입니다. 아세톤 생산 라인을 역통합한 아시아 생산자들은 비용 우위를 점하며 글로벌 가격 격차를 심화시키고 있습니다.

부문 분석

시트는 2025년 PMMA 시장 점유율의 38.19%를 차지했으며, 2031년까지 연평균 5.36%의 성장률을 보이며 이 카테고리의 전체 PMMA 시장 규모에 비례하는 달러 기준 매출 성장을 뒷받침할 것입니다. 더 얇은 게이지 압출 라인은 이제 자동차 선루프 하중 요구 사항을 충족하는 견고한 기계적 안정성을 제공하여, 안전 여유를 희생하지 않고도 차량 제조사가 무게를 줄일 수 있게 합니다. 주조 아크릴 시트는 광학 결함을 최소화하는 더 엄격한 두께 공차 덕분에, 특히 LED 엣지 조명 패널에서 프리미엄 위치를 유지합니다.

비드와 펠릿은 사출 성형 렌즈, 가전 제품 노브 및 의료 부품의 주력 원료로 그 뒤를 잇습니다. 복합 단계에서 충격 개질제와 자외선 흡수제를 점점 더 많이 첨가함으로써 실외 간판용 제품의 내구성을 높이기 위해 일부 투명도를 희생하는 사례가 증가하고 있습니다. 레이저 조각용으로 맞춤 제작된 과립은 트로피 및 선물용품 부문에서 틈새 수익원을 창출합니다. 시트 부문보다 성장 속도는 느리지만, 수지 컴파운드는 단기 맞춤형 제품의 폭넓은 범위를 지원함으로써 PMMA 시장의 꾸준한 수요를 뒷받침합니다./p>

PMMA 시장 보고서는 제품 형태(시트, 비드, 펠릿, 수지 컴파운드, 그래뉼), 최종 사용자 산업(자동차, 건축, 건설, 전기, 전자, 항공우주, 산업기계 및 장비 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카)별로 분류됩니다. 시장 예측은 수량(톤) 및 금액(달러)으로 제공됩니다.

지역별 분석

아시아태평양 지역은 중국의 대규모 변환기 기반과 인도의 인프라 확충에 힘입어 2025년 PMMA 시장 점유율의 50.30%를 차지했습니다. 그러나 중국의 과잉 생산 능력은 마진을 압박하여 국내 업체들을 특수 제품 수출로 유도하고 신규 생산 능력 축소를 촉진하고 있습니다. 인도는 2027년까지 수입 의존도를 낮추고 지역 점유율을 확보하기 위해 11억 달러를 투자하여 MMA-PMMA 통합 단지를 건설할 계획입니다. 일본과 한국은 전자 및 광학 분야와 연계된 고부가가치 틈새 시장을 주도하며, 일반 등급 제품에서 나타나는 가격 하락을 완화하고 있습니다.

북미는 성숙했으나 수익성이 높은 시장으로, 지속가능성 특성이 프리미엄을 창출합니다. LG화학의 2025년 바이오 아크릴산 출시로 북미 변환업체들은 화장품 포장용 재생성분 PMMA 제품을 공급할 수 있게 되었다. 항공우주 산업 회복과 전기차 투자가 수입 시트 경쟁에도 불구하고 기본 물량을 견인합니다.

유럽은 순환경제에 주력하며, 독일과 네덜란드의 화학적 재활용 시범사업은 정책 지원을 받아 재활용 성분 할당량을 충족하는 초기 상업용 물량을 생산 중입니다. 그러나 수입 MMA 원료 의존도는 유럽 PMMA 제조사들을 에너지 가격 급등에 취약하게 만든다. 남미 및 중동 시장은 인프라 메가프로젝트가 투명 방음벽과 대형 간판을 요구함에 따라 규모는 작지만 유망하다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자동차 업계의 경량화와 조명 수요

- 건축용 유리 및 외관의 채택 상황

- LED 간판, 디스플레이 산업의 확대

- 의료, 치과 분야의 PMMA 사용량 증가

- PMMA 화학적 재활용 경제성 개선

- 시장 성장 억제요인

- MMA 원료 가격의 변동성

- 폴리카보네이트 및 유리 대체 위협

- 엄격한 일회용 플라스틱 규제

- 밸류체인 분석

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 수출입 동향

- 가격 동향

- 규제 상황

- 최종 용도 부문 동향

- 항공우주(항공우주부품 생산수익)

- 자동차(자동차 생산)

- 건축 및 건설(신축상 지역)

- 전기 및 전자 기기(전기 및 전자 기기 생산 수익)

- 포장(플라스틱 포장 수량)

제5장 시장 규모와 성장 예측

- 제품 형태별

- 시트

- 비드 및 펠릿

- 수지 컴파운드 및 그래뉼

- 최종 사용자 업계별

- 자동차

- 건축 및 건설

- 전기 및 전자 기기

- 항공우주

- 산업용 기계, 설비

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 말레이시아

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 이탈리아

- 영국

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 나이지리아

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- Asahi Kasei Corporation

- CHIMEI

- Kuraray Co., Ltd.

- LOTTE MCC Corp.

- Lucite International Alpha BV

- LX MMA(LX Group)

- Mitsubishi Chemical Corporation

- Rohm GmbH

- Sanors

- Sumitomo Chemical Co., Ltd.

- Suzhou Double Elephant Optical Materials Co., Ltd.

- Trinseo

- Wanhua

제7장 시장 기회와 장래의 전망

제8장 CEO를 위한 주요 전략적 과제

HBR 26.02.04Polymethyl Methacrylate (PMMA) market size in 2026 is estimated at 3.21 Million tons, growing from 2025 value of 3.06 Million tons with 2031 projections showing 4.08 Million tons, growing at 4.90% CAGR over 2026-2031.

Solid demand from automotive lightweighting, architectural glazing, and LED displays sustains growth even as methyl methacrylate (MMA) feedstock costs remain volatile. PMMA's optical clarity, UV stability, and straightforward processing differentiate it from competing polymers, shielding volumes from substitution pressure in many core uses. Regional overcapacity-especially in China-keeps pricing competitive, while breakthrough chemical-recycling pilots open a pathway to circular production models. Producers prioritize vertical integration and specialty-grade development as defensive strategies in the PMMA market.

Global Polymethyl Methacrylate (PMMA) Market Trends and Insights

Automotive lightweight and lighting demand

Electric-vehicle makers specify PMMA for panoramic sunroofs, tail-lamp covers, and sensor housings because the polymer weighs 50% less than glass yet offers high optical quality. The technology shift toward adaptive LED systems amplifies demand for Rohm's light-management grades that shape precise beam patterns. Additional pull comes from autonomous-vehicle LiDAR lenses requiring low birefringence. Despite new impact-resistant polycarbonate (PC) copolymers, PMMA market resilience persists where cost and UV durability outweigh marginal toughness gains.

Architectural Glazing and Facade Adoption

Smart-building envelopes now integrate PMMA sheets embedded with sensors and heating elements that manage daylight, condensation, and self-cleaning functions. PMMA transmits 92-93% visible light versus 86-89% for PC, supporting energy-efficiency credits under European building codes. Digital printing on PMMA panels enables complex facade designs without multi-material assemblies, reducing installation time. Fire-code restrictions in high-rise projects still cap penetration, yet long-term warranties and UV resistance keep PMMA competitive where clarity and aesthetics dominate.

Volatile MMA Feedstock Pricing

MMA price swings mirror petrochemical feedstock trends, magnified by energy-intensive processes. Trinseo raised European PMMA prices by EUR 250 / t in March 2025 after propylene costs surged, compressing converter margins. Import-dependent regions such as Europe remain exposed until bio-based or recycled MMA scales commercially. Asian producers with back-integrated acetone routes gain cost advantage, exacerbating global price disparities.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of LED Signage & Display Industry

- Growth in Medical & Dental PMMA Use

- Substitution Threat from Polycarbonate and Glass

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sheets captured 38.19% of PMMA market share in 2025 and will expand at a 5.36% CAGR through 2031, underpinning USD-denominated sales growth proportionate with the overall PMMA market size for this category. Thinner-gauge extrusion lines now deliver robust mechanical stability that satisfies automotive sunroof load requirements, enabling vehicle makers to shave weight without sacrificing safety margins. Cast-acrylic sheets retain premium positioning-especially in LED edge-lit panels-thanks to tighter thickness tolerances that minimize optical defects.

Beads and pellets follow as the workhorse feedstocks for injection-molded lenses, appliance knobs, and medical parts. Formulators increasingly incorporate impact modifiers and UV absorbers at the compounding stage, trading some transparency for higher durability in outdoor signage. Granules tailored for laser engraving open niche revenue streams in trophy and giftware segments. Although growth lags the sheet category, resin compounds support consistent PMMA market demand by serving a wider span of short-run customized products.

The PMMA Market Report is Segmented by Product Form (Sheets, Beads and Pellets, Resin Compounds and Granules), End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Aerospace, Industrial Machinery and Equipment, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

Geography Analysis

Asia-Pacific accounted for 50.30% of PMMA market share in 2025 on the strength of China's large converter base and India's infrastructure build-out. However, Chinese overcapacity compresses margins, pushing domestic players toward specialty exports and prompting new capacity curtailments. India's commitment of USD 1.1 billion to an integrated MMA-PMMA complex aims to cut import reliance and seize regional share by 2027. Japan and South Korea anchor high-value niches tied to electronics and optics, mitigating price erosion seen in commodity grades.

North America remains a mature but lucrative arena where sustainability attributes command premiums. LG Chem's 2025 bio-acrylic acid launch positions North American converters to offer renewable-content PMMA products in cosmetics packaging. Aerospace recovery and electric-vehicle investments bolster baseline volumes despite imported sheet competition.

Europe focuses on circularity; chemical-recycling pilots in Germany and the Netherlands receive policy support and generate early commercial lots that meet recycled-content quotas. Nevertheless, exposure to imported MMA feedstocks leaves European PMMA producers vulnerable to energy-driven cost spikes. South American and Middle-Eastern markets remain small but promising as infrastructure megaprojects demand transparent noise barriers and large-format signage.

- Asahi Kasei Corporation

- CHIMEI

- Kuraray Co., Ltd.

- LOTTE MCC Corp.

- Lucite International Alpha B.V.

- LX MMA (LX Group)

- Mitsubishi Chemical Corporation

- Rohm GmbH

- Sanors

- Sumitomo Chemical Co., Ltd.

- Suzhou Double Elephant Optical Materials Co., Ltd.

- Trinseo

- Wanhua

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive lightweight and lighting demand

- 4.2.2 Architectural glazing and facade adoption

- 4.2.3 Expansion of LED signage and display industry

- 4.2.4 Growth in medical and dental PMMA use

- 4.2.5 Breakthroughs in PMMA chemical-recycling economics

- 4.3 Market Restraints

- 4.3.1 Volatile MMA feedstock pricing

- 4.3.2 Substitution threat from polycarbonate and glass

- 4.3.3 Stringent single-use plastics regulation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import and Export Trends

- 4.7 Pricing Trends

- 4.8 Regulatory Landscape

- 4.9 End-use Sector Trends

- 4.9.1 Aerospace (Aerospace Component Production Revenue)

- 4.9.2 Automotive (Automobile Production)

- 4.9.3 Building and Construction (New Construction Floor Area)

- 4.9.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.9.5 Packaging(Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Form

- 5.1.1 Sheets

- 5.1.2 Beads and Pellets

- 5.1.3 Resin Compounds and Granules

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.3 Electrical and Electronics

- 5.2.4 Aerospace

- 5.2.5 Industrial Machinery and Equipment

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Malaysia

- 5.3.1.7 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 United Kingdom

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 CHIMEI

- 6.4.3 Kuraray Co., Ltd.

- 6.4.4 LOTTE MCC Corp.

- 6.4.5 Lucite International Alpha B.V.

- 6.4.6 LX MMA (LX Group)

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Rohm GmbH

- 6.4.9 Sanors

- 6.4.10 Sumitomo Chemical Co., Ltd.

- 6.4.11 Suzhou Double Elephant Optical Materials Co., Ltd.

- 6.4.12 Trinseo

- 6.4.13 Wanhua

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment