|

시장보고서

상품코드

1910438

전원 관리 집적 회로(PMIC) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Power Management Integrated Circuit (PMIC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

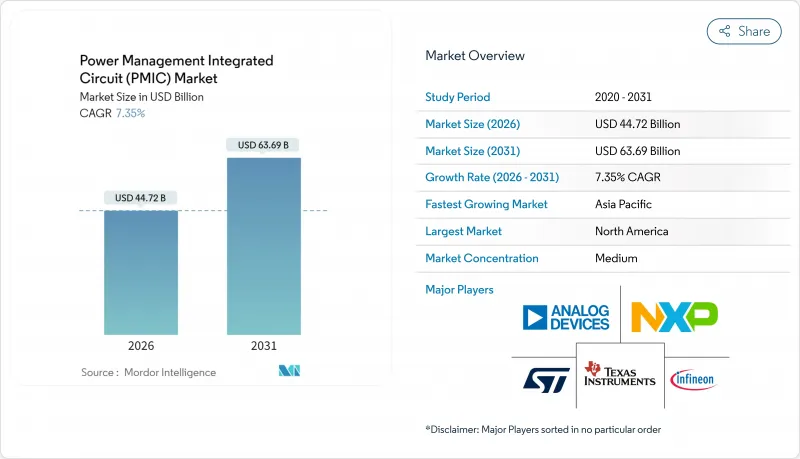

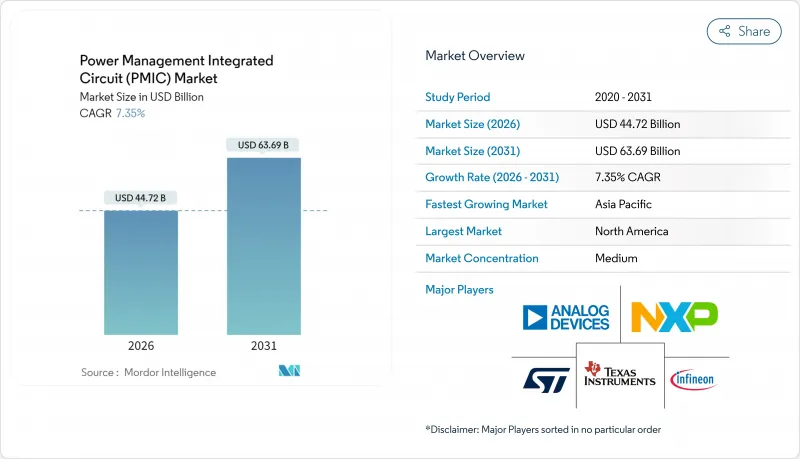

2026년 전원 관리 집적 회로(PMIC) 시장 규모는 447억 2,000만 달러로 추정되며, 2025년 416억 6,000만 달러에서 성장해 왔으며, 2031년에는 636억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지는 CAGR 7.35%를 나타낼 것으로 예상됩니다.

전기자동차, 플래그쉽 스마트폰, 초저전력 IoT 디바이스의 확대로 고효율 변환 토폴로지, 엄격한 전압 공차, 고급 프로세스 노드에 대한 수요가 증가하고 있습니다. 배터리 관리 IC는 계속 전원 관리 집적 회로(PMIC) 시장의 기반으로 무선 충전용 PMIC, 와이드 밴드갭 전원 스테이지, 20nm 이하의 설계가 성장의 중요한 촉매로서 대두하고 있습니다. 경쟁 구도는 독자적인 지적 재산(IP)으로 점유율을 지키는 아날로그 분야의 기존 기업과 수직 통합을 위한 자사 전용 솔루션을 개발하는 프로세서 벤더에 의해 형성되고 있습니다. 파운더리 용량, 초박형 디바이스의 열적 제약, 위조 부품의 유입은 시장 전체의 기세에 대한 구체적인 위험으로 계속 존재하고 있습니다.

세계의 전원 관리 집적 회로(PMIC) 시장 동향과 인사이트

EV 및 xEV의 급속한 보급이 고전류, 고효율 PMIC 수요를 끌어 올리고 있습니다.

전기자동차 아키텍처는 전원 관리 집적 회로(PMIC) 시장 사양을 재구성합니다. 테슬라의 4680 배터리 셀은 125°C 이하의 접합 온도를 유지하면서 최대 500A의 연속 전류를 처리할 수 있는 PMIC를 요구하며, 이로써 실리콘 카바이드(SiC) 파워 스테이지와 첨단 열 패키징이 촉진됩니다. BYD의 분산형 배터리 관리 설계는 10C의 급속 충전 능력을 실현하여 셀 단위 PMIC 제어의 필요성을 보여줍니다. 인피니언의 CoolSiC 모듈은 800V 차량 충전기로 98.5%의 효율을 달성하고, 플릿 오퍼레이터는 예지 보전을 가능하게 하는 PMIC 진단 기능을 우선하고 있습니다. 이러한 요구는 센서 인터페이스와 무선 링크의 통합을 촉진하고 PMIC를 단일 레귤레이터에서 스마트 서브시스템으로 전환하고 있습니다.

미세화 프로세스 노드를 통한 온칩 전력 밀도 향상

20nm 이하의 프로세스 마이그레이션으로 단일 다이에 여러 개의 전원 레일과 제어 로직을 배치할 수 있어 기판 면적의 축소와 기생 요소의 억제를 실현합니다. TSMC의 16nm FinFET 플랫폼은 설계 기판에 의한 열 프로파일 보호를 유지하면서 65nm 시 0.3W/mm2에 대해 1W/mm2 이상의 전력 밀도를 달성하고 있습니다. MediaTek의 Dimensity 9400은 AI 워크로드에 대해 서브마이크로초 단위의 전압 스케일링을 수행하는 온다이 PMIC에서 관리하는 12개의 독립적인 전원 도메인을 통합합니다. 그러나 양자효과에 의한 누설전류의 편차 증가로 보상 알고리즘의 채용이 강요되고 있으며, 현행의 3nm 프로세스에 비해 30%의 소비 전력 삭감을 목표로 하는 2nm 프로세스 노드에서는 게이트 올 어라운드 구조의 도입이 시사되고 있습니다.

아날로그 및 혼합 신호 노드를 위한 파운드리 용량 공급 체인 순환성

아날로그 생산은 디지털 용량 확대에 뒤쳐져 2024년 말에는 TSMC의 전문 라인에서 95%의 가동률에 이르렀으며, PMIC의 리드 타임은 기존의 8주에서 16주로 연장되었습니다. 세계 파운드리즈의 성숙 노드로의 전략 전환으로 자동차용 인증 로트공급자가 감소하고 지정학적 리스크에 대한 노출이 높아지고 있습니다. 자동차 프로그램이 5년간의 계약을 체결하는 가운데, 민생 전자 기기는 축소하는 슬롯을 겨루고, 할당 리스크가 격화하고 있습니다.

부문 분석

2025년에 있어서 전원 관리 집적 회로(PMIC) 시장 규모의 33.15%를 배터리 관리 IC가 차지해, 전기자동차용 팩이나 고정형 축전 시스템에 있어서 그 불가결성이 부각되었습니다. 그러나 무선 충전용 PMIC은 Qi2의 자기 정렬 기술로 15W 전송 효율이 85%로 향상되고 MagSafe와 유사한 에코시스템이 확대됨에 따라 2031년까지 연평균 복합 성장률(CAGR) 8.32%를 나타낼 것으로 예측됩니다.

전원 관리 집적 회로(PMIC) 시장 수요는 배터리 관리 IC에서 안전 진단, 셀 밸런스 정밀도, 열 제어를 중심으로 전개하고 있습니다. 한편, 이물 검지와 적응 공진 제어가 무선 충전용 PMIC의 차별화 요인이 됩니다. DC-DC 컨버터 PMIC는 데이터센터 및 노트북 PC의 전원 레일에 계속해서 수요가 있으며 선형 레귤레이터는 10μV 미만의 노이즈 플로어가 필요한 틈새 시장을 유지하고 있습니다. 또한 모터 드라이버 PMIC는 공장 자동화의 성장에 힘입어 있습니다. 전압 레퍼런스 및 수퍼바이저 IC는 자동차의 기능 안전 기준에 따라 필수적인 안정적인 수익 기반입니다.

2025년 전원 관리 집적 회로(PMIC) 시장 점유율에서 소비자용 전자 기기는 42.25%의 수익을 창출했습니다. 이는 스마트폰, 노트북, 태블릿이 1대당 15개 이상의 안정화 레일을 통합하고 있음을 반영합니다. 800V 구동 시스템과 ADAS 컴퓨팅 클러스터에 지원되는 자동차·e모빌리티 분야는 8.55%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측되며, 다른 모든 분야를 뛰어넘는 성장이 예상됩니다.

산업용 및 로봇 공학의 이용 사례에서는 토크 정밀도가 우수한 모터 구동이 요구되고 5G 인프라에서는 48V 직결 전원을 취급하는 고전압 PMIC가 필수적입니다. 의료기기, 특히 임플란트는 1 마이크로암페어 미만의 대기 전류를 선호하며, IoT 엔드포인트는 380mV에서 부팅 가능한 에너지 수확 가능 PMIC를 채택합니다. 각 업계는 신뢰성, 안정화 전압 및 원격 측정의 정밀도를 기준으로 PMIC 사양을 조정하므로 전원 관리 집적 회로(PMIC) 시장 전반에 걸쳐 공급업체의 로드맵이 세분화됩니다.

지역별 분석

북미는 2025년 세계 수익의 36.85%를 차지했으며, 테슬라의 배터리 관리 시스템 수주와 애플의 커스텀 PMIC 실리콘에 대한 주력이 견인했습니다. 이 지역은 설계 서비스 에코시스템의 심화와 견조한 EV 인프라 정비의 혜택을 받고 있습니다.

주요 파운드리와 민생전자기기 조립 거점인 아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 10.21%를 나타낼 것으로 예측됩니다. 중국의 EV 확대와 한국의 메모리 생산 라인이 PMIC의 수량을 견인해, 팹에의 근접성이 개발 사이클을 단축하고 있습니다.

유럽에서는 독일 자동차 제조업체가 800V 시스템을 채용하는 전동화와 엄격한 에코 디자인 규제가 함께 안정적인 수요가 지속되고 있습니다. 북유럽의 재생에너지 분야에서는 최대 전력점 추종(MPPT)을 최적화하는 계통 연계 인버터용 PMIC가 도입되고 있습니다. 중동 및 아프리카에서는 태양광 미니 그리드가 성장의 견인역이 되고, 남미에서는 브라질의 EV 우대 정책과 아르헨티나의 리튬 자원을 활용한 지역 밀착형 배터리 공급망이 성장의 요인이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전기자동차(EV) 및 하이브리드차(xEV)의 급속한 보급에 의해 고전류·고효율 PMIC 수요 증가

- 미세화 프로세스 노드(20nm 미만)에 의한 고밀도 칩내 전력 집적의 실현

- 플래그십 스마트폰에 있어서 선진적인 배터리 헬스 관리 PMIC의 채용

- 소비자용·산업용 전자 기기에 대한 정부의 에너지 절약 규제

- 엣지 AI/IoT의 보급에 의해 초저대기 전류 PMIC 필요

- 급속 충전기에 있어서 와이드 밴드갭(GaN/SiC) 파워 스테이지의 채용

- 시장 성장 억제요인

- 아날로그 및 혼합 신호 노드용 파운드리 용량공급망 순환성

- 설계의 복잡화가 진행되어 NRE 코스트가 중소 OEM 제조업체의 손이 닿지 않는 수준으로 상승

- 초박형 민생 기기에 있어서 열 관리의 한계

- 증가하는 위조 PMIC의 유입이 신뢰성에 대한 인식에 영향

- 업계 공급망 분석

- 규제 상황

- 기술 전망

- 거시경제 요인의 영향

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자·소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- IC 유형별

- 선형 레귤레이터 PMIC

- DC-DC 컨버터 PMIC

- 배터리 관리 IC

- 전압 레퍼런스 및 수퍼바이저 IC

- 모터 제어 및 드라이버 PMIC

- 무선 충전 PMIC

- 용도별

- 소비자용 전자 기기

- 자동차 및 e모빌리티

- 산업 및 로봇

- 통신 및 네트워크

- 의료 및 의료기기

- IoT 및 엣지 디바이스

- 웨이퍼 노드별

- 65nm 이상

- 40-65nm

- 20-40nm

- 20nm 미만

- 전력 범위별

- 저전력 PMIC

- 중전력 PMIC

- 고전력 PMIC

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Texas Instruments Inc.

- Analog Devices, Inc.

- Infineon Technologies AG

- NXP Semiconductors NV

- STMicroelectronics NV

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- Qualcomm Incorporated

- Broadcom Inc.

- Skyworks Solutions, Inc.

- Dialog Semiconductor(Renesas)

- Rohm Co., Ltd.

- Maxim Integrated(ADI)

- Toshiba Electronic Devices and Storage Corp.

- MediaTek Inc.

- Power Integrations, Inc.

- Silicon Laboratories Inc.

- Monolithic Power Systems, Inc.

- Vishay Intertechnology, Inc.

- Littelfuse, Inc.

제7장 시장 기회와 향후 전망

KTH 26.01.22The power management integrated circuit market size in 2026 is estimated at USD 44.72 billion, growing from 2025 value of USD 41.66 billion with 2031 projections showing USD 63.69 billion, growing at 7.35% CAGR over 2026-2031.

An expanding pool of electric vehicles, flagship smartphones, and ultra-low-power IoT devices is boosting demand for highly efficient conversion topologies, tighter voltage tolerances, and advanced process nodes. Battery management ICs remain the cornerstone of the power management integrated circuit market, while wireless-charging PMICs, wide-bandgap power stages, and sub-20 nm designs are emerging as pivotal growth catalysts. The competitive landscape is shaped by analog stalwarts defending share through proprietary IP and by processor vendors developing captive solutions for vertical integration. Foundry capacity, thermal constraints in ultra-thin devices, and counterfeit-component infiltration continue to pose tangible risks to overall market momentum.

Global Power Management Integrated Circuit (PMIC) Market Trends and Insights

Rapid EV and xEV Penetration Elevating Demand for High-Current, High-Efficiency PMICs

Electric-vehicle architecture is reshaping specifications for the power management integrated circuit market. Tesla's 4680 battery cell demands PMICs that handle up to 500 A continuous current while remaining below 125°C junction temperature, prompting silicon-carbide power stages and advanced thermal packaging. BYD's distributed battery-management design delivers 10C fast-charge capability, illustrating the need for granular cell-level PMIC control. Infineon's CoolSiC modules reach 98.5% efficiency in 800 V on-board chargers, and fleet operators now prioritize PMIC diagnostics to enable predictive maintenance. These requirements spur integration of sensor interfaces and wireless links, transforming PMICs into smart subsystems rather than isolated regulators.

Shrinking Process Nodes Enabling Higher On-Chip Power Density

Sub-20 nm migration allows multiple power rails and control logics on a single die, shrinking board footprints and limiting parasitics. TSMC's 16 nm FinFET platform achieves power densities above 1 W/mm2 versus 0.3 W/mm2 at 65 nm while safeguarding thermal profiles through engineered substrates. MediaTek's Dimensity 9400 integrates 12 independent power domains managed by an on-die PMIC that performs sub-microsecond voltage scaling for AI workloads. Yet quantum effects boost leakage variance, forcing adoption of compensation algorithms and heralding gate-all-around structures in 2 nm nodes targeting 30% power drop relative to current 3 nm.

Supply-Chain Cyclicality of Foundry Capacity for Analog and Mixed-Signal Nodes

Analog production lags digital capacity expansion, reaching 95% utilization at TSMC's specialty lines in late 2024 and elongating PMIC lead times to 16 weeks from a historical 8 weeks. GlobalFoundries' strategy shift toward mature nodes leaves fewer suppliers for automotive-qualified lots, raising exposure to geopolitical events. With automotive programs locking five-year commitments, consumer electronics vie for shrinking slots, intensifying allocation risk.

Other drivers and restraints analyzed in the detailed report include:

- Flagship Smartphone Adoption of Advanced Battery-Health PMICs

- Government Energy-Efficiency Mandates for Consumer and Industrial Electronics

- Rising Design Complexity Driving NRE Costs Beyond Reach of Smaller OEMs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery management ICs accounted for 33.15% of the power management integrated circuit market size in 2025, underscoring their indispensability in electric-vehicle packs and stationary storage. Wireless-charging PMICs, however, are expected to log an 8.32% CAGR through 2031 as Qi2 magnetic alignment boosts 15 W transmit efficiency to 85% and as MagSafe-like ecosystems proliferate.

Demand within the power management integrated circuit market pivots around safety diagnostics, cell-balancing accuracy, and thermal orchestration for battery management ICs, whereas foreign-object detection and adaptive resonance control differentiate wireless-charging PMICs. DC-DC converter PMICs still serve data-center and notebook rails, linear regulators reserve niches that need <10 µV noise floors, and motor-driver PMICs ride factory-automation growth. Voltage-reference and supervisor ICs remain a stable revenue bedrock, mandated by automotive functional-safety norms.

Consumer electronics generated 42.25% of 2025 revenue for the power management integrated circuit market share, reflecting smartphones, notebooks, and tablets that integrate upwards of 15 regulated rails per device. Automotive and e-mobility, supported by 800 V drivetrains and ADAS compute clusters, is forecast to post an 8.55% CAGR, outpacing all other verticals.

Industrial and robotics use cases require torque-accurate motor drives, whereas 5 G infrastructure calls for high-voltage PMICs handling 48 V direct feeds. Healthcare devices, especially implants, prioritize <1 µA standby current, and IoT endpoints adopt energy-harvesting PMICs capable of starting at 380 mV. Each vertical calibrates its PMIC specs around reliability, regulation voltage, and telemetry sophistication, fragmenting supplier roadmaps across the power management integrated circuit market.

The Power Management Integrated Circuit (PMIC) Market Report is Segmented by Type (Linear Regulator PMIC, DC-DC Converter PMIC, and More), Application (Consumer Electronics, Automotive and E-Mobility, and More), Wafer Node (Greater Than or Equal To 65 Nm, 40-65 Nm, and More), Power Range (Low Power PMICs, Medium Power PMICs, High Power PMICs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 36.85% of global revenue in 2025, propelled by Tesla battery-management orders and Apple's emphasis on custom PMIC silicon. The region benefits from deep design-service ecosystems and a robust EV infrastructure build-out.

Asia-Pacific, home to leading foundries and consumer-electronics assembly, is projected to post a 10.21% CAGR through 2031. China's EV scale-up and South Korea's memory lines fuel PMIC volume, while proximity to fabs shortens iteration cycles.

Europe combines automotive electrification, where German OEMs adopt 800 V systems, with strict eco-design rules, sustaining steady demand. Nordic renewables deploy grid-tie inverter PMICs optimizing maximum-power-point tracking. Growth pockets in the Middle East and Africa arise from solar mini-grids, whereas South America leverages Brazilian EV incentives and Argentine lithium resources for localized battery supply chains.

- Texas Instruments Inc.

- Analog Devices, Inc.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- Qualcomm Incorporated

- Broadcom Inc.

- Skyworks Solutions, Inc.

- Dialog Semiconductor (Renesas)

- Rohm Co., Ltd.

- Maxim Integrated (ADI)

- Toshiba Electronic Devices and Storage Corp.

- MediaTek Inc.

- Power Integrations, Inc.

- Silicon Laboratories Inc.

- Monolithic Power Systems, Inc.

- Vishay Intertechnology, Inc.

- Littelfuse, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid EV and xEV penetration elevating demand for high-current, high-efficiency PMICs

- 4.2.2 Shrinking process nodes (Less than 20 nm) enabling higher on-chip power density

- 4.2.3 Flagship smartphone adoption of advanced battery-health PMICs

- 4.2.4 Government energy-efficiency mandates for consumer and industrial electronics

- 4.2.5 Edge-AI/IoT proliferation requiring ultra-low-quiescent-current PMICs

- 4.2.6 Adoption of wide-bandgap (GaN/SiC) power stages in fast chargers

- 4.3 Market Restraints

- 4.3.1 Supply-chain cyclicality of foundry capacity for analog and mixed-signal nodes

- 4.3.2 Rising design complexity driving NRE costs beyond reach of smaller OEMs

- 4.3.3 Thermal-management limits in ultra-thin consumer devices

- 4.3.4 Increasing counterfeit PMIC influx affecting reliability perceptions

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers/Consumers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (USD BILLION)

- 5.1 By IC Type

- 5.1.1 Linear Regulator PMIC

- 5.1.2 DC-DC Converter PMIC

- 5.1.3 Battery Management IC

- 5.1.4 Voltage Reference and Supervisor IC

- 5.1.5 Motor-Control and Driver PMIC

- 5.1.6 Wireless-Charging PMIC

- 5.2 By Application

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive and e-Mobility

- 5.2.3 Industrial and Robotics

- 5.2.4 Telecommunications and Networking

- 5.2.5 Healthcare and Medical Devices

- 5.2.6 IoT and Edge Devices

- 5.3 By Wafer Node

- 5.3.1 Greater than and Equal to 65 nm

- 5.3.2 40 - 65 nm

- 5.3.3 20 - 40 nm

- 5.3.4 Less than 20 nm

- 5.4 By Power Range

- 5.4.1 Low Power PMICs

- 5.4.2 Medium Power PMICs

- 5.4.3 High Power PMICs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 South-East Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Texas Instruments Inc.

- 6.4.2 Analog Devices, Inc.

- 6.4.3 Infineon Technologies AG

- 6.4.4 NXP Semiconductors N.V.

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 ON Semiconductor Corporation

- 6.4.7 Renesas Electronics Corporation

- 6.4.8 Qualcomm Incorporated

- 6.4.9 Broadcom Inc.

- 6.4.10 Skyworks Solutions, Inc.

- 6.4.11 Dialog Semiconductor (Renesas)

- 6.4.12 Rohm Co., Ltd.

- 6.4.13 Maxim Integrated (ADI)

- 6.4.14 Toshiba Electronic Devices and Storage Corp.

- 6.4.15 MediaTek Inc.

- 6.4.16 Power Integrations, Inc.

- 6.4.17 Silicon Laboratories Inc.

- 6.4.18 Monolithic Power Systems, Inc.

- 6.4.19 Vishay Intertechnology, Inc.

- 6.4.20 Littelfuse, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment