|

시장보고서

상품코드

1910456

친수성 코팅 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Hydrophilic Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

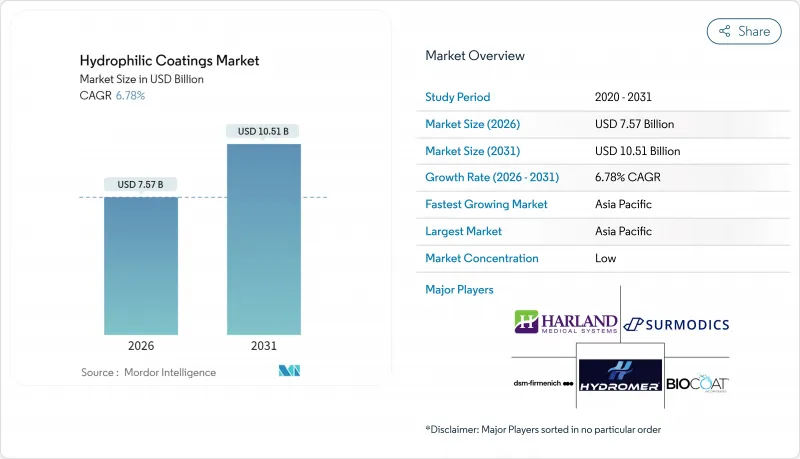

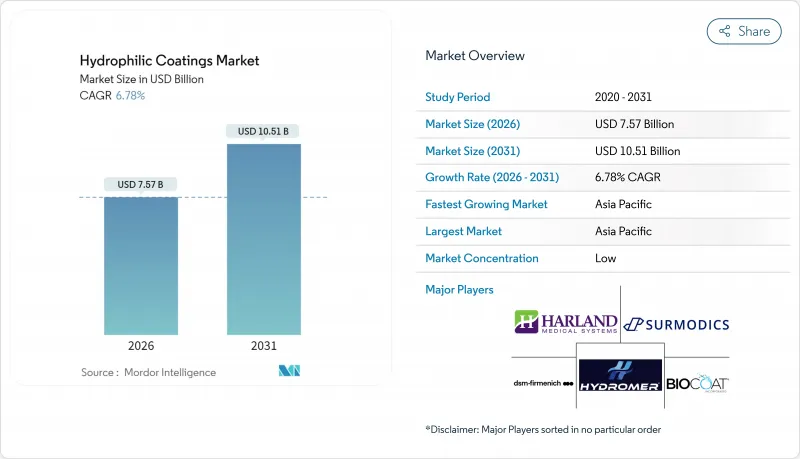

친수성 코팅 시장은 2025년에 70억 9,000만 달러로 평가되었으며, 2026년 75억 7,000만 달러, 2031년까지 105억 1,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026-2031년)의 CAGR은 6.78%를 나타낼 전망입니다.

의료, 광학 및 자동차 응용 분야에서의 채택의 급증과 보다 엄격한 지속가능성 요구 사항이 이러한 성장을 지원합니다. 폴리머 기판이 여전히 주류이지만 나노입자를 응용한 표면처리가 그 우위성을 침식하고 있습니다. 반면 아시아태평양은 지리적 플라이휠 효과를 제공하여 세계 공급망의 재구축을 촉진하고 있습니다. 의료기기에 대한 가격 압력 증가, PFAS 규제 강화, 내구성 우려가 지속적으로 확대를 억제하고 있지만, 재료의 지속적인 혁신, 증착 기술의 효율화, PFAS 프리 솔루션의 생태계 확대가 상업적 기회를 넓히고 있습니다.

세계 친수성 코팅 시장 동향과 인사이트

의료 용도에서 수요 증가

의료기기 설계자는 침습 수술이 낮을 때 삽입 저항을 줄이고 혈전증을 줄이기 위해 친수성 코팅에 의존합니다. 임상적 증거는 카테터 마찰을 최대 70%까지 줄이고 혈관내 조작을 원활화하고 수술 시간을 단축할 수 있음을 보여줍니다. 윤활성과 항균제 또는 항혈전제를 조합한 코팅이 주목을 받고 있으며, 특히 신경혈관 스텐트에서 표면 개질된 혈류 전환 장치가 혈소판 부착을 억제하여 이중 항혈소판 요법의 필요성을 경감할 가능성이 있습니다. 병원에서는 현재 회복 기간의 단축과 감염 위험의 억제로 이어지는 이러한 다기능층을 갖춘 기기를 우선적으로 채택하고 있습니다. 병행하여 학계와 산업계의 연계에 의한 전임상 검증이 가속되고 있어, 채택을 한층 더 촉진하고 있습니다.

코팅 재료의 기술 혁신

나노입자를 응용한 기재는 높은 친수성, 내마모성, 서방형을 겸비함으로써 성능의 한계를 재정의하고 있습니다. 실리카 폴리아크릴산 제제는 경미한 마모 하에서도 초친수성을 유지하여 수년간의 과제였던 내구성의 갭을 해소합니다. 스타 PEG-헤파린 등의 반응성 하이드로겔은 카테터 전개시의 전단력을 견디면서 온디맨드의 항응고 작용을 발휘합니다. 이러한 진보는 코팅이 기계적 무결성을 손상시키지 않으면 서 표면 윤활성과 치료 기능이라는 이중 역할을 수행하는 새로운 제품 구조를 가능하게합니다.

고비용 생산

다단계 합성, 클린룸 내 증착, 철저한 품질 검사로 표준 코팅에 비해 제조 비용이 30-40% 증가하여 가격에 민감한 카테터 및 가이드와이어 제품 라인의 이익률을 압박하고 있습니다. 전문적인 노하우는 여전히 소수공급업체에 집중하고 있으며, 규모의 경제를 제한하고 OEM 제조업체의 전환 비용을 높입니다. 공정 자동화 및 롤 투 롤 UV 경화 시스템으로 사이클 시간이 단축되고 있지만, 자본 요건이 소규모 신규 진입을 막고 있습니다.

부문 분석

나노입자 대응 기판은 CAGR 7.45%로 성장을 지속하고, 폴리머가 차지하는 47.25%의 수익 기반을 침식하고 있습니다. 할로이사이트 나노튜브 강화 에폭시 아크릴레이트 에멀젼은 염수 분무 시험 16일 동안 녹 발생 제로를 달성하였습니다. 내구성에서 명확한 도약을 보여줍니다. 유리상에서 접촉각 162°를 실현하는 초발수성 실리카 코팅은 나노기술의 장점이 기재를 넘어 응용되는 사례입니다.

제조업체는 비용 효율적인 대량 생산을 위해 폴리머를 여전히 선호하고 있지만, 나노 실리카와 층상 규산염을 폴리머 매트릭스에 통합 한 하이브리드 설계가 기판의 계층 구조를 바꾸고 있습니다. 이러한 하이브리드는 유연한 가공 창과 강화된 내마모성을 융합시켜 카테고리 경계를 모호하게 만듭니다. 금속과 유리 기재는 생체 적합성이나 광학 투명성이 중요한 틈새 분야에서 역할을 유지하고 있지만, 이러한 분야에서도 나노 스케일의 중간층이 접착성과 내식 성능을 향상시키고 있습니다.

2025년 시점에서는 딥 코팅이 매출 점유율 41.35%를 유지했습니다. 그러나, 플라즈마 및 UV 이식법은 연간 7.38%로 성장하여, 용매의 잔류 없이 복잡한 형상에 대한 주문 표면 화학 처리를 가능하게 하고 있습니다. 유기 화학 기상 성장 방법(iCVD)은 그라디언트 폴리머 층을 형성하여 빙기피성을 향상시키고 온도 변동 하에서도 친수성을 유지합니다.

스프레이 및 슬롯 다이 라인은 사이클 시간을 단축하고 증가하는 카테터 생산 목표에 대응합니다. 화학 기상 성장 방법은 시너지 효과 성분의 동시 증착을 가능하게 하고, 물 접촉각을 43.2°로 감소시킴으로써 코팅의 균일성 및 수명 주기 안정성을 향상시킵니다.

지역별 분석

아시아태평양은 2025년 세계 수익의 32.35%를 차지했고 연간 7.55%의 성장률로 가속화될 전망입니다. 중국의 정부 의료 지출과 중-고급 카테터 제조의 확대가 견고한 디바이스 수요를 지지하고 있습니다. 일본 기업은 정밀 성막 기술을 세련시키고 한국의 전자 대기업은 이미지 센서에 친수성 코팅을 채택하여 지역의 주도적 지위를 확고하게 하고 있습니다.

북미 시장은 풍부한 의료기기 개발 파이프라인과 고품질 코팅을 평가하는 FDA의 엄격한 성능 기준으로 중요한 지위를 차지하고 있습니다. EPA의 PFAS 규제는 신속한 재배합을 다루고 있으며, 규제 적합하고 높은 윤활성을 확보한 국내 공급업체가 선행자 우위성을 획득하고 있습니다.

유럽 시장은 지속가능성에 대한 요청이 중심입니다. 임박한 REACH 규제에 의한 PFAS 규제 강화는 수성 및 UV 경화 시스템으로의 이행을 가속화하여 저 VOC 폴리우레탄 및 에폭시 분산액의 혁신을 촉진하고 있습니다. 현지 OEM 제조업체는 재료 전문 기업과 제휴해, 규제 기한전에 접촉각 성능이나 세포독성 성능의 검증을 진행하고 있습니다.

라틴아메리카 및 중동 및 아프리카은 여전히 초기 단계이지만 성장하고 있습니다. 브라질의 카테터 제조업체는 수출 확대에 따라 턴키식 코팅 모듈을 도입하고 사우디아라비아는 '비전 2030' 아래 첨단 재료에 투자, 의료 승인된 코팅 기술에 대한 지역 수요를 육성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 의료 분야 수요 증가

- 코팅 재료의 기술 혁신

- 광학 및 전자 산업에 있어서의 기술 진보

- 지속가능한 코팅에 대한 규제지원

- 유럽 지역의 VOC 기준 충족 수계 및 UV 경화형 제형 확대

- 시장 성장 억제요인

- 높은 생산 비용

- 내구성과 성능에 대한 우려

- 원재료 가격의 변동성

- 밸류체인 분석

- 규제 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측(금액)

- 기재별

- 폴리머

- 유리/세라믹

- 금속

- 나노입자 기술을 활용한

- 증착 공정 기술별

- 딥 코팅

- 스프레이 및 슬롯 다이

- 플라즈마 및 UV 그라프트

- 화학 기상 증착

- 기타 기술

- 용도별

- 카테터 및 가이드와이어

- 스텐트 및 임플란트

- 광학 렌즈 및 안경 렌즈

- 자동차용 센서 및 카메라

- 건축용 유리 및 태양전지용 유리

- 기타(선박, 섬유, 항공우주)

- 최종 사용자 업계별

- 의료기기

- 광학 및 광학기술

- 자동차

- 운송 및 해양

- 기타 산업

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- Aculon

- Applied Medical Coatings

- AST Products Inc.

- Biocoat Incorporated

- Coatings2Go

- dsm-firmenich

- Formacoat

- Harland Medical Systems, Inc.

- Hydromer

- Mitsubishi Chemical America, Inc.

- PPG Industries Inc.

- Specialty Coating Systems Inc.

- Surface Solutions Group LLC

- Surmodics Inc.

- Teleflex Incorporated

제7장 시장 기회와 장래의 전망

SHW 26.01.26The Hydrophilic Coatings Market was valued at USD 7.09 billion in 2025 and estimated to grow from USD 7.57 billion in 2026 to reach USD 10.51 billion by 2031, at a CAGR of 6.78% during the forecast period (2026-2031).

Surging adoption across medical, optical and automotive applications, coupled with stricter sustainability mandates, underpins this growth. Polymer substrates still dominate but nanoparticle-enabled surfaces are eroding that lead, while Asia-Pacific delivers a geographic flywheel effect that is redrawing global supply chains. Intensifying price pressure on medical devices, tightening PFAS regulations and durability concerns continue to temper expansion; nevertheless, continuous materials innovation, streamlined deposition techniques and an expanding eco-system of PFAS-free solutions are widening commercial opportunities.

Global Hydrophilic Coatings Market Trends and Insights

Rising Demand in Healthcare Applications

Medical device designers rely on hydrophilic coatings to lower insertion forces and mitigate thrombosis in minimally invasive procedures. Clinical evidence shows up to 70% reduction in catheter friction, enabling smoother vascular navigation and shorter procedure times. Coatings that blend lubricity with antimicrobial or antithrombotic agents are gaining traction, especially for neurovascular stents, where surface-modified flow diverters reduce platelet adhesion and may lessen dual-antiplatelet therapy requirements. Hospitals now prioritize devices with such multifunctional layers because they shorten recovery and curb infection risk. In parallel, academic-industry collaborations are accelerating pre-clinical validation, further lifting adoption.

Technological Innovations in Coating Materials

Nanoparticle-enabled substrates redefine performance ceilings by combining high hydrophilicity, abrasion resistance, and controlled-release capability. Silica-poly(acrylic-acid) formulations retain super-hydrophilicity under mild wear, tackling a long-standing durability gap. Responsive hydrogels such as starPEG-heparin withstand shear forces during catheter deployment while delivering on-demand anticoagulation. These advances open new product architectures where coatings deliver dual roles-surface lubricity plus therapeutic functionality-without compromising mechanical integrity.

High Production Costs

Multi-step synthesis, clean-room deposition and intensive quality testing add 30-40% to manufacturing costs versus standard coatings, squeezing margins in price-sensitive catheter and guidewire lines. Specialized know-how remains concentrated among a handful of suppliers, limiting economies of scale and elevating switching costs for OEMs. Although process automation and roll-to-roll UV-cure systems are trimming cycle times, capital requirements deter smaller entrants.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Optical and Electronics Industries

- Regulatory Support for Sustainable Coatings

- Durability and Performance Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nanoparticle-enabled substrates posted 7.45% CAGR and are eroding polymer's 47.25% revenue stronghold. Halloysite nanotube-reinforced epoxy acrylate emulsions showed zero rusting after 16 days of salt-spray exposure compared with 9 days for conventional polymers, signalling a clear durability leap. Superhydrophobic silica coatings with 162° contact angles on glass illustrate cross-substrate migration of nanotechnology benefits.

Manufacturers continue to favor polymers for cost-effective volume output, but hybrid designs that embed nano-silica or layered silicates within polymer matrices are reshaping the substrate hierarchy. These hybrids merge flexible processing windows with enhanced abrasion resistance, blurring category lines. Metal and glass substrates retain niche roles where biocompatibility or optical clarity are critical, yet even here, nanoscale interlayers are elevating adhesion and corrosion performance.

Dip-coating retained 41.35% revenue share in 2025. However, plasma and UV-graft routes, growing 7.38% annually, increasingly allow tailor-made surface chemistries on complex geometries without solvent carryover. Initiated Chemical Vapor Deposition (iCVD) creates gradient polymer layers that improve ice-phobicity and maintain hydrophilicity across temperature swings.

Spray and slot-die lines shrink cycle times, meeting rising catheter output targets. Chemical vapor deposition methods enable co-deposition of synergistic components, driving water contact angles down to 43.2°, thereby boosting coating uniformity and lifecycle stability.

The Hydrophilic Coatings Market Report Segments the Industry by Substrate (Polymer, Glass/Ceramic, and More), Deposition Technology (Dip-Coating, Spray and Slot-Die, and More), Application (Catheters and Guidewires, Stents and Implantables, and More), End-User Industry (Medical Devices, Optics and Photonics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific generated 32.35% of global revenue in 2025 and will accelerate at 7.55% a year. Government healthcare spending and mid- to high-end catheter manufacturing expansion in China underpin robust device demand. Japanese firms refine precision deposition, and Korean electronics giants deploy hydrophilic coatings in image sensors, cementing regional leadership.

North America has a significant position in the market, buoyed by deep medical-device pipelines and strict FDA performance expectations that reward premium coatings. EPA's PFAS classification forces rapid reformulation; domestic suppliers that secure compliant, high-lubricity chemistries gain early mover status.

Europe's market centres on sustainability mandates. Imminent REACH curbs on PFAS accelerate migration toward water-borne and UV-cure systems, fostering innovation in low-VOC polyurethane and epoxy dispersions. Local OEMs partner with materials specialists to validate contact-angle and cytotoxicity performance ahead of compliance deadlines.

Latin America and the Middle East & Africa remain nascent but rising. Brazil's catheter producers incorporate turnkey coating modules as they scale exports, while Saudi Arabia invests in advanced materials under Vision 2030, nurturing regional demand for medically approved coating technologies.

- Aculon

- Applied Medical Coatings

- AST Products Inc.

- Biocoat Incorporated

- Coatings2Go

- dsm-firmenich

- Formacoat

- Harland Medical Systems, Inc.

- Hydromer

- Mitsubishi Chemical America, Inc.

- PPG Industries Inc.

- Specialty Coating Systems Inc.

- Surface Solutions Group LLC

- Surmodics Inc.

- Teleflex Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand in Healthcare Applications

- 4.2.2 Technological Innovations in Coating Materials

- 4.2.3 Advancements in Optical and Electronics Industries

- 4.2.4 Regulatory Support for Sustainable Coatings

- 4.2.5 VOC-Compliant Water-borne and UV-Cure Formulations in Europe

- 4.3 Market Restraints

- 4.3.1 High Production Costs

- 4.3.2 Durability and Performance Concerns

- 4.3.3 Volatility in Raw Material Prices

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value )

- 5.1 By Substrate

- 5.1.1 Polymer

- 5.1.2 Glass / Ceramic

- 5.1.3 Metal

- 5.1.4 Nanoparticle-Enabled

- 5.2 By Deposition Technology

- 5.2.1 Dip-Coating

- 5.2.2 Spray and Slot-Die

- 5.2.3 Plasma and UV-Graft

- 5.2.4 Chemical Vapor Deposition

- 5.2.5 Other Technologies

- 5.3 By Application

- 5.3.1 Catheters and Guidewires

- 5.3.2 Stents and Implantables

- 5.3.3 Optical and Eyewear Lenses

- 5.3.4 Automotive Sensors and Cameras

- 5.3.5 Architectural and Solar Glass

- 5.3.6 Others (Marine, Textile, Aerospace)

- 5.4 By End-User Industry

- 5.4.1 Medical Devices

- 5.4.2 Optics and Photonics

- 5.4.3 Automotive

- 5.4.4 Transportation and Marine

- 5.4.5 Other Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aculon

- 6.4.2 Applied Medical Coatings

- 6.4.3 AST Products Inc.

- 6.4.4 Biocoat Incorporated

- 6.4.5 Coatings2Go

- 6.4.6 dsm-firmenich

- 6.4.7 Formacoat

- 6.4.8 Harland Medical Systems, Inc.

- 6.4.9 Hydromer

- 6.4.10 Mitsubishi Chemical America, Inc.

- 6.4.11 PPG Industries Inc.

- 6.4.12 Specialty Coating Systems Inc.

- 6.4.13 Surface Solutions Group LLC

- 6.4.14 Surmodics Inc.

- 6.4.15 Teleflex Incorporated

7 Market Opportunities and Future Outlook

- 7.1 Development of Eco-Friendly Coatings

- 7.2 White-space and Unmet-need Assessment