|

시장보고서

상품코드

1910479

프리필드 시린지 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Prefilled Syringes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

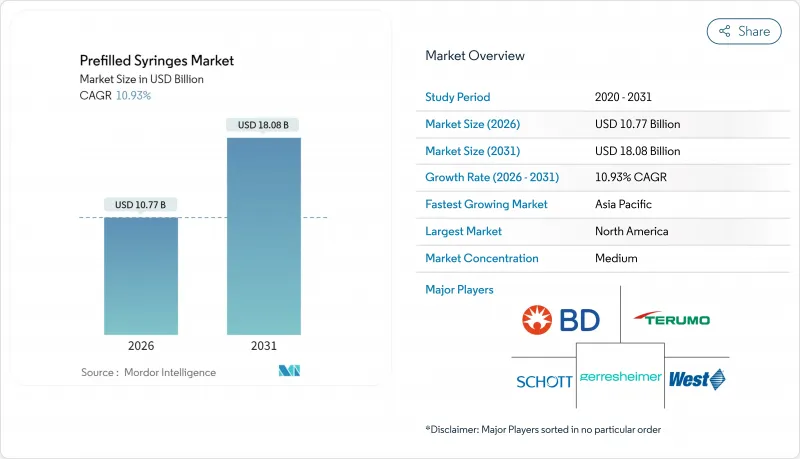

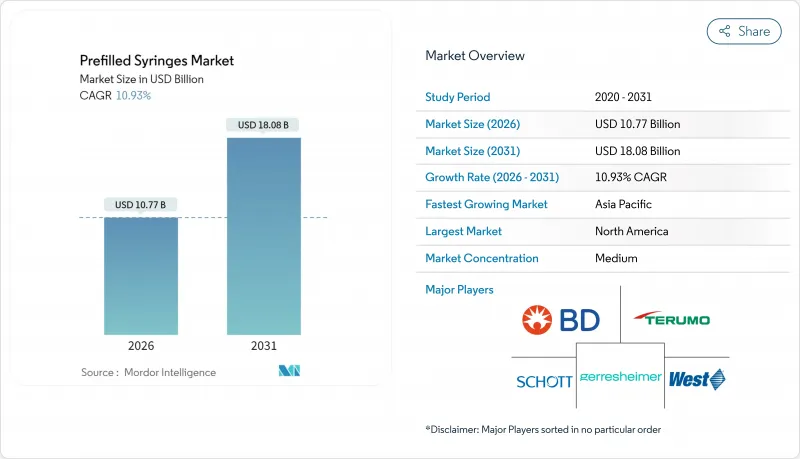

프리필드 시린지 시장은 2025년 97억 1,000만 달러로 평가되었고, 2026년에는 107억 7,000만 달러, 2031년까지 180억 8,000만 달러로 성장할 전망입니다. 2026년부터 2031년에 걸쳐 CAGR은 10.93%를 나타낼 전망입니다.

성장을 견인하고 있는 것은 GLP-1 비만 치료제의 급증, 유행성 후의 충전 및 마무리 능력의 증강, 통합형 안전 장치를 추천하는 규제 동향입니다. 폴리머 주사기 배럴의 혁신은 유리 시스템의 오랜 우위를 위협하고 있습니다. 한편 지역별 동향에서는 북미가 규모면에서 주도권을 유지하고 아시아태평양이 가장 빠른 수량 증가율을 보이고 있습니다. 특히 고점도 바이오의약품에 있어서의 자가주사 수요의 높아짐에 따라 제조업체 각사는 투여형태의 개량, 네스테드라인에 대한 투자, 환상 올레핀 폴리머(COP) 플랫폼에의 이행을 추진하고 있습니다. 경쟁 차별화는 용기와 약물의 적합성, 수동적 안전 기능, 높은 생산성으로 즉시 사용 가능한 구성 공급 능력에 초점을 맞추었습니다.

세계 프리필드 시린지 시장 동향과 인사이트

GLP-1 계 비만 치료제의자가 주사 증가

세계 GLP-1 시장 규모는 2023년 400억 달러에서 2032년까지 1,500억 달러로 확대될 전망이며, 고급 자가주사 형식에 대한 지속적인 수요를 유발하고 있습니다. 노보놀디스크는 미국의 새로운 충전 및 포장 라인에 41억 달러, 프랑스의 주사 펜 확장에 21억 유로를 투입할 계획이며, 이 치료 영역을 향한 인프라 규모의 크기를 나타내고 있습니다. BD사의 Neopak XtraFlow 주사기는 보다 얇은 벽의 캐뉼라를 채택함으로써 고점도 약제의 투여를 용이하게 해, 폭넓은 환자의 자기 투여를 지원하는 동시에, 간호사의 부담 경감에 공헌하고 있습니다. 복약 준수에 관한 연구에서는 프리필드 디바이스에 의한 치료 계속률의 높이가 일관되게 나타나고 있으며, 의료기관에서 재택 케어로의 이행을 원활하게 하고 프리필드 시린지 시장에 지속적인 성장의 기반을 구축하고 있습니다.

생물학적 제형에 적합한 고리형 올레핀 중합체(COP) 주사기로의 전환

제약 회사는 제어된 안정성 시험에서 확인된 우려사항인 민감한 생물학적 제형에서 단백질 응집을 일으키는 실리콘 오일과의 상호작용을 완화하기 위해 COP 배럴을 채택하고 있습니다. COP 주사기는 입자 수가 적고 ISO/EN 10993의 생체적합성 기준을 충족하므로 차세대 의약품에 적합합니다. SCHOTT Pharma의 TOPPAC 냉동 플랫폼은 온도에 민감한 mRNA 요법을 위해 특별히 설계되었습니다. 또한 독일에서 폴리머 생산 능력의 확대는 유리에서의 전환을 강조합니다. 바이오시밀러의 출시가 가속화되고 있는 가운데, COP 주사기를 기반으로 한 차별화된 딜리버리 시스템이 프리필드 시린지 시장에서 경쟁 우위로 대두되고 있습니다.

고 pH 바이오 의약품에서 유리 박리에 의한 회수 사례

박리는 용액의 pH와 이온 함량으로 인해 유리 플레이크가 의약품에 용출됨으로써 발생합니다. 이 고장 메커니즘으로 인해 여러 리콜 및 FDA 경고가 발생합니다. 높은 pH의 생물학적 제제는 특히 취약하기 때문에 규제 당국은 승인 전에 철저한 용기 폐쇄 시스템 적합성 시험을 의무화하고 있습니다. 프리필드 제형은 많은 스트레스 지표에서 바이알을 초과하고 있지만, 잔존 위험이 있기 때문에 제약 기업은 폴리머 대체품의 검토를 진행하고 있습니다. 결과적인 재료 교체는 불확실성을 야기하고, 테스트 비용을 증가시키고, 프리필드 시린지 시장의 단기 성장을 억제합니다.

부문 분석

2025년 시점에서 유리 주사기는 프리필드 시린지 시장 매출의 68.25%를 차지하며, 확립된 규제 지식과 확장 가능한 붕규산 유리 공급의 혜택을 누리고 있습니다. 그러나, 제약 기업이 실리콘과의 상호작용을 회피하고, 서브 가시 입자를 저감하는 COP 배럴로 이행하는 중, 플라스틱은 11.71%의 연평균 복합 성장률(CAGR)로 급속히 추격하고 있습니다. 폴리머제 프리필드 시린지 시장 규모는 2031년까지 2배 이상으로 확대될 전망이며, 용기 선정 기준이 비용에서 의약품과의 적합성으로 이행하고 있음을 나타내고 있습니다. COP는 ISO/EN 10993에서 검증된 고감도 단백질에 중립성으로 mRNA, 유전자 치료, 고점도 GLP-1 제제의 주요 소재로서의 지위를 확립하고 있습니다. SCHOTT Pharma와 같은 조기 채택 기업은 현재 독일과 미국에서 전용 폴리머 라인의 확대를 추진하고 있으며 조달 전략의 돌이킬 수없는 전환을 보여줍니다.

또한, 층간 박리에 의한 리콜이 규제 당국이나 품질 관리 책임자의 경계감을 높이는 가운데, 유리 용기로부터의 이행의 움직임도 가속하고 있습니다. 질소 충전 파우치에 보관된 폴리머 배럴은 기존 주사기에서 볼 수 있는 유리 실리콘 층이 없으며 2-8℃에서 유리와 동등한 안정성을 나타냅니다. 바이오의약품 파이프라인이 확대되고(현재는 세계의 R&D 자산의 절반 이상을 차지함), 조달팀은 폴리머를 위험보험으로 파악하는 경향이 커지고 있습니다. 하지만 유리는 산화 배리어성과 기존의 변경 관리 파일에서 우위성을 유지하고 있으며, 프리필드 시린지 시장에서는 양 소재의 장기적인 공존이 확실시됩니다.

2025년 출하량에서는 1-2.5mL 클래스가 51.68%를 차지하고, 대부분의 단회 투여형 생물학적 제제 요법에 적합한 것을 반영하고 있습니다. 그러나, 1mL 이하의 부문이 성장의 원동력이 되고 있어 고농도 GLP-1 제제나 고효력 항암제 등 미량 투여를 필요로 하는 약제 수요에 의해 CAGR11.73%로 확대하고 있습니다. 밀리리터 미만의 용량은 허용 오차를 엄격하게 하므로 공급업체는 충전기에 인라인 비전 시스템을 개조하여 ±2 마이크로리터 이내의 분주 정밀도를 보장합니다. 이 투자의 물결은 지불자와 임상의가 주사 부담 감소로 일치하는 동안 소형 배럴용 프리필드 시린지 시장 점유율을 확대하고 있습니다.

한편, 2.5mL를 넘는 용량화는 ISO 11040-4의 치수 제한에 저촉하는 경우가 많아 플런저의 막힘이나 라인 정지가 산견됩니다. 5mL를 초과하는 이중 챔버 유형은 더 높은 장애물에 직면하고 검증 비용을 밀어 올립니다. 이러한 경제성에서 컴팩트한 배럴에 들어간 고농도 제제가 우위가 되어 제조 처리량과 가치에 근거한 의료의 요청이 일치하는 형태가 되고 있습니다.

지역별 분석

북미는 2025년 수익의 38.40%를 차지하며 풍부한 생물학적 제제 파이프라인과 견고한 안전 규제가 기반을 두고 있습니다. BD사는 미국 생산능력을 40% 확대하고, SCHOTT Pharma사는 최초의 미국 공장에 3억 7,100만 달러를 투자하고 있으며, 이들은 리쇼어링 정책과 GLP-1 수요 급증에 대한 대응을 목적으로 한 움직임입니다. FDA의 복합 제품 승인 경로에 신속하게 액세스하면 제품 출시를 효율화하고 OSHA의 규제 요구 사항은 수동 안전 형식의 안정적인 수요를 보장합니다. 대통령령 14017에 근거한 연방정부의 우대조치가 국내 생산의 매력을 더욱 높여주고, 이 지역이 프리필드 시린지 시장에서의 주도적 지위를 확고하게 하고 있습니다.

유럽은 견고한 5%대 전반의 성장을 유지하고 있으며, 안전 설계를 우선하는 엄격한 침침 사고 방지 지령이 뒷받침하고 있습니다. 게레스하이머는 동유럽에서 생산량을 두배로 늘리는 동시에 독일과 스위스에서 혁신센터를 운영하고 있습니다. 유럽 의약청(EMA)의 확립된 바이오시밀러 승인 프로세스는 제품 승인을 원활하게 하고 스폰서가 차별화된 주사기 형태를 선택하도록 촉구합니다. 반면 브렉짓의 복잡성으로 인해 일부 기업은 이중 재고 거점을 구축하는 움직임을 볼 수 있지만 전체 공급 회복력은 유지되고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 11.79%로 업계를 견인합니다. 중국 국가약품감독관리국(NMPA)이 2025년 개혁 계획에 통합한 신속 승인 제도는 바이오시밀러 시장 투입을 가속화하고 현지 주사기 수요를 끌어 올리고 있습니다. 일본의 고령화는 자가주사의 보급을 촉진하고 인도의 경쟁 바이오시밀러 클러스터는 수출 능력을 확대하고 있습니다. 니프로가 노스캐롤라이나주에 공장을 개설하기로 한 결정은 아시아와 서양을 연결하는 양방향 공급 흐름을 부각하고 있습니다. 지역정부는 수입적자 억제를 위해 국내 의료기기 제조를 지원하고 있으며 프리필드 시린지 시장의 장기적인 수요 증가를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- GLP-1계 비만치료제의 자가주사 증가

- 생물학적 제제에 적합한 순환 올레핀 폴리머(COP) 시린지로의 전환

- 니들스틱 부상 방지 지침(Needlestick-Injury Directive)으로 안전형 PFS 수요 증가

- 포스트 COVID 백신 충전 및 마무리 공정 확장

- 중국 국가약품감독관리국(NMPA)의 신속 승인 제도에 의한 국내 바이오시밀러의 신속 출시

- 환자의 재택 류마티스 치료 선호

- 시장 성장 억제요인

- 고 pH 생물 제제에서 유리 시린지 층 분리 리콜

- 중첩형 PFS 라인의 고액의 설비 투자가 CMO 진입 억제

- ISO 11040-4 규격에 준거한 5mL 초과의 이중 챔버 설계에 있어서의 규격 불량

- 헤파린 오염 소송에 의한 외부 위탁의 억제

- 가치/공급망 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 소재별

- 유리

- 플라스틱

- 배럴 단위로의 양별

- 1mL 이하

- 1-2.5mL

- 2.5mL 초과

- 제품 유형별

- 바늘 포함

- 바늘 미포함

- 용도별

- 당뇨병

- 아나필락시스

- 백신 접종

- 류마티스 관절

- 종양학

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Becton, Dickinson and Company

- Gerresheimer AG

- SCHOTT AG

- West Pharmaceutical Services Inc.

- Terumo Corporation

- Stevanato Group SpA

- Nipro Corporation

- Catalent Pharma Solutions

- Vetter Pharma

- Haselmeier GmbH

- Baxter International Inc.

- Fresenius Kabi

- Nemera

- Taisei Kako Co. Ltd.

- Oval Medical Technologies

- SHL Medical

- Owen Mumford

- Plas-Tech Engineering Inc.

- Laboratoire Aguettant SA

- Credence MedSystems

- Aptar Pharma

제7장 시장 기회와 장래의 전망

SHW 26.01.26The Prefilled Syringes Market is expected to grow from USD 9.71 billion in 2025 to USD 10.77 billion in 2026 and is forecast to reach USD 18.08 billion by 2031 at 10.93% CAGR over 2026-2031.

Growth is propelled by surging GLP-1 obesity therapeutics, post-pandemic fill-finish capacity additions, and regulatory moves that favor integrated safety devices. Polymer barrel innovation is challenging the long-held dominance of glass systems, while regional dynamics show North America preserving scale leadership and Asia-Pacific delivering the fastest volume gains. Intensifying demand for self-injection, particularly for high-viscosity biologics, pushes manufacturers to upgrade delivery formats, invest in nested lines, and migrate toward cyclic olefin polymer (COP) platforms. Competitive differentiation now pivots on container-drug compatibility, passive safety features, and the ability to supply ready-to-use configurations at high output.

Global Prefilled Syringes Market Trends and Insights

Rising Self-Injection of GLP-1 Obesity Drugs

Global GLP-1 sales are on course to climb from USD 40 billion in 2023 to USD 150 billion by 2032, igniting sustained demand for advanced self-injection formats. Novo Nordisk has earmarked USD 4.1 billion for new US fill-finish lines and EUR 2.1 billion for French injector-pen expansion, demonstrating the scale of infrastructure now directed to this therapeutic area. BD's Neopak XtraFlow syringe with thinner-wall cannulas facilitates high-viscosity dosing, supporting broad patient self-administration while lowering nurse workloads . Adherence studies consistently show higher persistence with prefilled devices, easing the shift from clinic-based to home-based care and embedding a durable growth vector for the prefilled syringes market.

Shift to Biologic-Friendly Cyclic Olefin Polymer (COP) Syringes

Pharmaceutical firms are embracing COP barrels to mitigate silicone-oil interactions that trigger protein aggregation in sensitive biologics, a concern documented in controlled stability trials. COP syringes exhibit lower particulate counts and satisfy ISO/EN 10993 biocompatibility criteria, making them suitable for next-generation drugs. SCHOTT Pharma's TOPPAC freeze platform is purpose-built for temperature-sensitive mRNA therapies, while expanded German polymer capacity underscores the shift away from glass . As biosimilar launches intensify, differentiated delivery systems based on COP barrels are emerging as a competitive lever in the prefilled syringes market.

Glass Delamination Recalls in High-pH Biologics

Delamination erupts when solution pH and ion content leach glass flakes into drug product, a failure mechanism that has forced multiple recalls and FDA warning letters. High-pH biologics are particularly vulnerable, prompting regulators to mandate exhaustive container-closure compatibility studies before approval. Even though prefilled formats outperform vials on many stress metrics, any residual risk spurs pharmaceutical teams to explore polymer alternatives. The resulting material churn injects uncertainty and adds testing costs, tempering near-term growth in the prefilled syringes market.

Other drivers and restraints analyzed in the detailed report include:

- Needlestick-Injury Directive Accelerating Safety-Engineered Demand

- Post-COVID Vaccine Fill-Finish Expansion

- High CAPEX of Nested PFS Lines Deterring CMOs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glass syringes held 68.25% of the prefilled syringes market revenue in 2025, benefiting from entrenched regulatory familiarity and scalable borosilicate supply. Yet plastics are sprinting ahead with an 11.71% CAGR as pharma companies migrate to COP barrels that avoid silicone interactions and reduce subvisible particles. The prefilled syringes market size for polymer formats is set to more than double by 2031, underscoring the shift in container-selection criteria from cost to drug-product compatibility. COP's neutrality toward sensitive proteins, verified under ISO/EN 10993, positions it as the go-to material for mRNA, gene-therapy, and high-viscosity GLP-1 formulations. Early adopters such as SCHOTT Pharma now scale dedicated polymer lines in Germany and the US, signaling an irreversible tilt in procurement strategies.

Momentum away from glass also picks up speed as delamination recalls raise red flags among regulators and quality heads. Polymer barrels stored in nitrogen-filled pouches exhibit stability comparable to glass at 2-8 °C without the free silicone layer found in legacy syringes. As biologic pipelines expand-now representing more than half of global R&D assets-procurement teams increasingly view polymer as risk insurance. Nevertheless, glass retains advantages in oxidative barrier and legacy change-control files, ensuring a prolonged coexistence between the two materials within the prefilled syringes market.

The 1-2.5 mL class dominated 2025 shipments at 51.68%, reflecting its fit with most single-dose biologic regimens. The <=1 mL segment, however, is the dynamo, advancing at an 11.73% CAGR thanks to concentrated GLP-1 formulations and high-potency oncology drugs that favor micro-dosing. Given tighter tolerances at sub-milliliter volumes, suppliers are retrofitting fillers with in-line vision systems to guarantee dispense accuracy within +-2 µL. This investment wave enlarges the prefilled syringes market share for smaller barrels as payers and clinicians unite around a lower injection burden.

Conversely, attempts to push beyond 2.5 mL often collide with ISO 11040-4 dimensional limits, causing sporadic plunger jams and line stoppages. Dual-chamber versions above 5 mL face still steeper hurdles, raising validation costs. The economics thus favor high-concentration formulations housed in compact barrels, aligning manufacturing throughput with value-based care imperatives.

The Prefilled Syringes Market Report is Segmented by Material (Glass, Plastic), Barrel Volume (Less Than or Equal To 1 ML, 1 To 2. 5 ML, More Than 2. 5 ML), Product Type (With Needle, Without Needle), Application (Diabetes, Anaphylaxis, Vaccination, Rheumatoid Arthritis, Oncology, Other Applications), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 38.40% of 2025 revenue, anchored by deep biologic pipelines and robust safety regulations. BD is enlarging US capacity by 40%, and SCHOTT Pharma is spending USD 371 million on its first American plant, moves designed to meet reshoring policies and GLP-1 volume spikes. Ready access to FDA combination-product pathways streamlines launches, while OSHA mandates ensure steady demand for passive-safety formats. Federal incentives under Executive Order 14017 further sweeten the case for domestic production, cementing the region's leadership in the prefilled syringes market.

Europe maintains healthy mid-single-digit progress, drawing support from stringent needlestick directives that prioritize safety-engineered devices. Gerresheimer is doubling Eastern European output while running innovation centers in Germany and Switzerland. EMA's well-trodden biosimilar route smooths product approvals, encouraging sponsors to opt for differentiated syringe presentations. Meanwhile, Brexit complexities have nudged some firms to build dual inventory hubs, but overall supply resilience remains intact.

Asia-Pacific is the pace-setter with an 11.79% CAGR through 2031. China's NMPA fast-track, embedded in the 2025 reform plan, accelerates biosimilar roll-outs and elevates local syringe demand. Japan's aging demographics amplify self-injection uptake, and India's competitive biosimilar clusters expand export capacity. Nipro's decision to open a North Carolina plant highlights the two-way supply flows now linking Asia with the West. Regional governments back local device manufacturing to curb import deficits, bolstering long-run volume upside for the prefilled syringes market.

- Beckton Dickinson

- Gerresheimer

- SCHOTT

- West Pharmaceutical Services

- Terumo

- Stevanato Group

- Nipro

- Catalent Pharma Solutions

- Vetter Pharma

- Haselmeier GmbH

- Baxter

- Fresenius

- Nemera

- Taisei Kako Co. Ltd.

- Oval Medical Technologies

- SHL Medical

- Owen Mumford

- Plas-Tech Engineering Inc.

- Laboratoire Aguettant S.A.

- Credence MedSystems

- Aptar Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Self-Injection of GLP-1 Obesity Drugs

- 4.2.2 Shift to Biologic-Friendly Cyclic Olefin Polymer (COP) Syringes

- 4.2.3 Needlestick-Injury Directive Accelerating Safety-Engineered PFS Demand

- 4.2.4 Post-COVID Vaccine Fill-Finish Expansion

- 4.2.5 Rapid Domestic Biosimilar Launches under China's NMPA Fast-Track

- 4.2.6 Patient Preference for Home-Based Rheumatology Therapies

- 4.3 Market Restraints

- 4.3.1 Glass Delamination Recalls in High-pH Biologics

- 4.3.2 High CAPEX of Nested PFS Lines Deterring CMOs

- 4.3.3 ISO 11040-4 Dimensional Failures in more than 5 mL Dual-Chamber Designs

- 4.3.4 Litigation over Heparin Contamination Curtailing Outsourcing

- 4.4 Value / Supply-Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Glass

- 5.1.2 Plastic

- 5.2 By Barrel Volume

- 5.2.1 Less than or equal to 1 mL

- 5.2.2 1 to 2.5 mL

- 5.2.3 More than 2.5 mL

- 5.3 By Product Type

- 5.3.1 With Needle

- 5.3.2 Without Needle

- 5.4 By Application

- 5.4.1 Diabetes

- 5.4.2 Anaphylaxis

- 5.4.3 Vaccination

- 5.4.4 Rheumatoid Arthritis

- 5.4.5 Oncology

- 5.4.6 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Becton, Dickinson and Company

- 6.3.2 Gerresheimer AG

- 6.3.3 SCHOTT AG

- 6.3.4 West Pharmaceutical Services Inc.

- 6.3.5 Terumo Corporation

- 6.3.6 Stevanato Group S.p.A.

- 6.3.7 Nipro Corporation

- 6.3.8 Catalent Pharma Solutions

- 6.3.9 Vetter Pharma

- 6.3.10 Haselmeier GmbH

- 6.3.11 Baxter International Inc.

- 6.3.12 Fresenius Kabi

- 6.3.13 Nemera

- 6.3.14 Taisei Kako Co. Ltd.

- 6.3.15 Oval Medical Technologies

- 6.3.16 SHL Medical

- 6.3.17 Owen Mumford

- 6.3.18 Plas-Tech Engineering Inc.

- 6.3.19 Laboratoire Aguettant S.A.

- 6.3.20 Credence MedSystems

- 6.3.21 Aptar Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment