|

시장보고서

상품코드

1910491

산업용 안전화 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Industrial Protective Footwear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

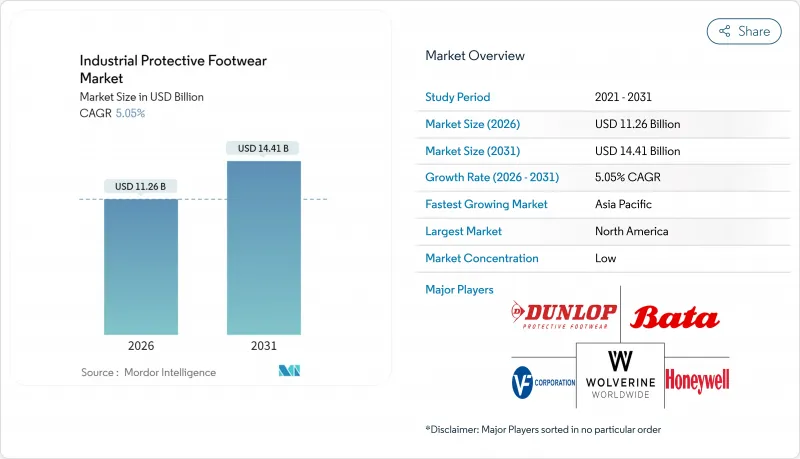

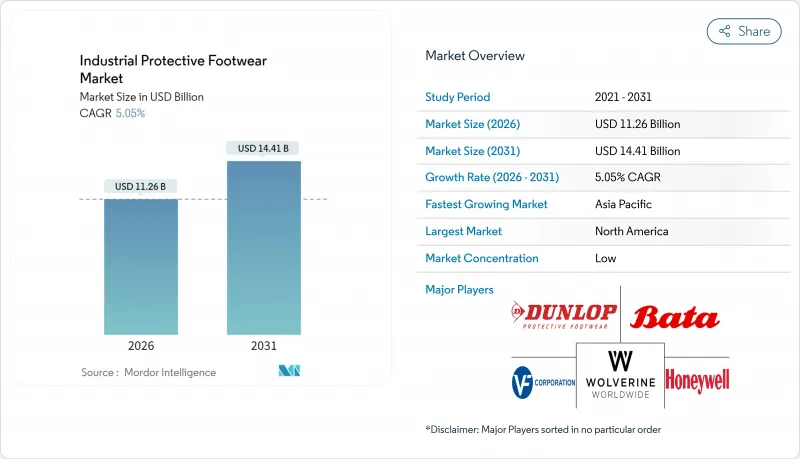

산업용 안전화 시장은 2025년 107억 2,000만 달러로 평가되었으며, 2026년 112억 6,000만 달러에서 2031년까지 144억 1,000만 달러에 이를 것으로 전망됩니다.

예측 기간(2026-2031년)의 CAGR은 5.05%를 나타낼 것으로 예상됩니다.

견고한 건설 프로젝트 파이프라인, 엄격한 안전 규정 및 신속한 소재 혁신이 이러한 성장을 지원합니다. 작업원 사이에서 복합 소재제 발가락 캡이나 통기성막의 채용이 증가하고 있는 점은 특필해야 합니다. 또한, 업데이트된 OSHA 29 CFR 1910.136 규정은 작업 현장 전체에 맞는 테스트와 성능 기준을 강화했습니다. 아시아 및 중동에서 인프라 투자가 증가함에 따라 수요가 이어지고 있습니다. 또한 IoT 센서를 통합한 '스마트' 부츠의 등장으로 데이터 중심의 안전 솔루션에 대한 조달 선택이 진행되고 있습니다. 위조품 거래나 중소 계약자의 가격 감응도 등의 과제는 남아 있는 것, 특히 바이오 베이스 소재나 재생 소재를 중시하는 기업의 ESG 목표가 시장을 뒷받침하고 있습니다.

세계의 산업용 안전화 시장 동향과 인사이트

직장 안전 및 규제 준수에 대한 관심 증가

정부에 의한 직장안전기준의 강화에 따라 규제집행의 강화를 배경으로 보호신발의 채용이 증가하고 있습니다. OSHA(미국노동안전보건국)의 2025년 개정에서는 건설업, 제조업, 일반산업 분야에서 사업주는 적절한 보호신발의 선정과 노동자교육을 의무화할 수 있습니다. 이러한 개정은 29 CFR 1910.136에 따라 의무화되었으며, 노동안전보건국에 의해 제정되었습니다. 노동통계국에 따르면 2023년 비치사적인 직장 부상 건수는 총 260만 건으로 2022년 대비 8.4% 감소했지만, 특정 업종에서는 여전히 발·발목 부상이 과제가 되고 있습니다. 구체적으로는 건설업에서 8.14%, 농업에서 10.23%, 운수업이 11.06%로 가장 높은 발생률을 보이고 있습니다. 유럽에서는 EN ISO 20345 : 2022 표준에 대한 시장 정합이 진행되고 있습니다. 이러한 조화된 요건은 노동자 보호를 강화할 뿐만 아니라 국경을 넘어선 무역을 원활하게 합니다. 이러한 규제의 무결성은 컴플라이언스의 단편화를 완화하고, 제조업체는 주요 시장 전체에서 규모의 경제를 활용할 수 있게 합니다. 의료 분야를 분석하면 미끄러짐, 넘어짐, 넘어짐 사고는 미끄러짐이 현저하게 영향을 미치고, 전 사례의 42.9%를 차지하고 있습니다. 그러나 영국 보건안전청(HSE)이 보고한 국민보건서비스(NHS)에 의한 시험에서는 미끄럼 방지 신발이 이러한 사고율을 37% 삭감할 수 있음이 밝혀졌습니다.

인프라 정비 가속이 PPE 지출을 밀어 올립니다.

건설·에너지 프로젝트가 확대됨에 따라 신흥 시장에서는 인프라 투자가 가속화되어 산업용 안전화의 지속적인 수요로 이어지고 있습니다. 미국 인구조사국은 건설지출 증가와 보호구 조달주기와의 상관관계를 지적하고 있습니다. 특히 특수 안전화에 대한 수요가 현저한 중건축·인프라 분야에서 현저합니다. 한편 아시아태평양에서는 도시화와 산업 성장이 인프라 개발을 견인해 건설 및 광업·에너지 분야에서의 안전화 수요를 자극하고 있습니다. 인도, 동남아시아, 중동에서는 정부 인프라 계획이 국제안전기준의 적용을 추진하고 있으며, 이로써 인증받은 보호신발 제조업체가 시장 진입하는 길이 열리고 있습니다. 공급망의 지역화 동향은 지역 제조업을 강화하고 수입 의존도를 억제함과 동시에 급증하는 인프라 수요에 대응할 수 있도록 하고 있습니다. 또한 인프라 지출의 파급효과는 직접적인 건설뿐만 아니라 보수, 유틸리티, 관련 산업 및 이들 모두에서 안전화의 적합성이 중시되고 있습니다. 이 동향을 현저하게 보여주는 것이 사우디아라비아의 새로운 PPE 기술 규제입니다. 사우디 규격청이 지적했듯이 인프라에 중점을 둔 각국이 안전 의무를 보다 광범위한 개발 전략에 통합하고 있음을 부각하고 있습니다.

저비용 위조 제품의 만연

위조 안전화는 노동자의 안전을 위협할 뿐만 아니라 시장 역학을 왜곡하고 정규 제조업체를 불리한 입장으로 몰아넣습니다. OECD의 분석은 문제의 심각성을 돋보이게 하고 세계의 위조품 거래가 4,670억 달러를 넘다는 것을 밝혔습니다. 우려해야 할 점은 신발류가 압수된 위조품의 62%라는 놀라운 비율을 차지하는 점이며, 이는 OECD 위조품 보고서에 자세히 설명되어 있습니다. 영국안전산업연맹에 의한 시험에서는 영국시장에 비적합 안전화가 대량 유통되고 있다는 우려할 만한 동향이 밝혀졌습니다. 이러한 위조품은 외형은 진짜 같지만 기본적인 안전 기준을 충족하지 않는 경우가 적지 않습니다. 이 문제의 광범위성을 보여주는 현저한 사례로는 필리핀 당국이 1억 5,200만 페소 상당의 위조신발을 몰수한 것을 들 수 있고, 특히 개발도상국에서의 보호구 시장의 과제가 부각되었습니다. 이러한 위조품은 필요한 안전 인증이 부족할 뿐만 아니라 열악한 소재를 사용하고 있어 성능 시험에 합격하지 않는 경우가 적지 않습니다. 이 간과는 고용주에게 중대한 법적 책임 위험을 초래하고 노동자를 위험에 빠뜨립니다. 온라인 마켓플레이스의 대두는 위조품의 유통을 용이하게 해, 규제 당국과 정규 제조업체 양쪽의 검지·단속 활동을 복잡화시킴으로써, 이 문제를 더욱 악화시키고 있습니다.

부문 분석

2025년 가죽 제품은 타의 추종을 불허하는 내구성, 통기성 및 다양한 산업 분야에서의 용이성으로 62.74%의 압도적인 시장 점유율을 차지했습니다. 내마모성과 쾌적성으로 알려진 크롬 태닝 가죽은 종일 착용시의 쾌적성이 최우선되는 건설 및 제조업 분야에서 정평의 선택지입니다. 그러나 환경문제에 대한 관심이 높아지고 기업의 지속가능성이 필 수요건이 되는 가운데 소재 선호는 변화하고 있습니다. 특히 MDPI의 연구에 의하면, 전문용 안전화의 탄소발자국의 39.9%를 가죽 어퍼가 차지하고 있는 것이 밝혀지고 있습니다. 한편, 합성 피혁은 성능 향상과 환경 부하 저감을 강점으로 대두하고 있습니다. 또한 고무부품은 석유 및 가스·화학처리 분야에서의 내약품성에 대한 수요 증가를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 6.49%로 확대되는 성장궤도에 있습니다.

소재 환경의 변화에 따라 제조업체는 ESG 요건을 준수하기 위해 바이오 대체 소재 및 재생 소재의 사용을 확대하고 있습니다. MDPI Rubber Textiles Review가 지적했듯이, 구아유와 러시아 민들레의 천연 고무의 혁신은 산업용 안전화에 필수적인 성능 기준을 손상시키지 않으면 서 석유 의존성 억제에 기여합니다. 선진 복합재나 섬유·고무 복합 소재는 감전 방지나 극한 온도 내성 등 특수 성능을 제공하여 틈새 시장을 개척하고 있습니다. 또한 ASTM F2413 및 EN ISO 20345 : 2022와 같은 규제 프레임워크는 소재 성능을 종합적으로 보장하고 안전 기준을 유지하면서 혁신을 촉진하고 있습니다.

2025년 부츠는 뛰어난 발목 보호 성능과 다양한 산업 환경에의 적응성으로 안전화 시장의 66.92%라는 압도적인 점유율을 차지했습니다. 건설, 광업, 중공업 등의 분야에서는 낙하물로부터 화학물질 노출에 이르는 위험에 직면하는 노동자에게 있어서, 이러한 높은 발목 보호가 필수적입니다. 부츠 분야는 기술 혁신의 혜택도 받고 있으며, 제조업체는 경량 소재, 인체 공학에 기초한 설계, 스마트 센서 기능을 통합하면서 엄격한 보호 기준을 유지하고 있습니다. 반면 신발은 급속한 성장을 보이고 있으며 2031년까지 연평균 복합 성장률(CAGR) 5.46%가 예상됩니다. 이 급성장은 주로 경제조업, 물류, 서비스업에서의 채용 확대에 의한 것으로, 발목 보호보다 작업원의 쾌적성이 중시되는 분야에서 수요 증가가 요인입니다.

제품 설계 혁신은 안전 기준을 유지하면서 기존의 편안함과 관련된 문제를 해결하는 데 점점 더 중점을 두고 있습니다. MDPI 임상 연구의 조사에서 심각한 우려 사항이 부각되었습니다. 기존의 안전 부츠는 보통 550-650그램의 중량이 있어, 작업원의 기동성을 방해해, 사용자의 83.3%에 불쾌감을 가져오고 있습니다. 이 발견은 더 가벼운 대체품에 대한 수요 증가를 뒷받침하고 있습니다. 한편, 창고업, 식품가공업, 의료 분야에서는 로우컷 신발의 디자인이 노동자들 사이에서 지지를 모으고 있습니다. 이 분야에서는 발목의 엄격한 보호보다 기동성과 편안함이 더 중시되는 경향이 있습니다. 제품 유형의 이러한 진화는 직장 환경의 변화를 반영합니다. 서비스업이 급성장하고 전통적인 중공업이 자동화를 진행하는 중 초점은 물리적 위험의 경감뿐만 아니라 발부의 보호가 최우선 사항인 것을 계속할 수 있는 확보에도 놓여 있습니다.

산업용 안전화 보고서는 소재별(피혁, 합성 피혁, 고무 등), 제품 유형별(부츠, 신발), 최종 사용자 산업별(건설, 제조, 석유 및 가스, 광업 등), 유통 채널별(온라인, 오프라인), 지역별(북미, 유럽, 아시아태평양, 남미 등)으로 분류됩니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

지역별 분석

2025년 시점에서 북미는 28.21%라는 압도적인 시장 점유율을 차지했습니다. 이는 엄격한 OSHA 규제, 활기찬 건설 부문 및 노동자 보호를 선호하는 선진적인 제조업에 의해 지원됩니다. 성숙한 규제 프레임워크인 29 CFR 1910.136 하에서 노동안전보건국(OSHA)은 건설업, 제조업, 일반산업에서 안전화 착용을 의무화하고 있으며, 경제 상황이 변동하더라도 안정된 수요가 확보되고 있습니다. 미국의 건설 지출과 인프라 투자 증가는 보호 신발 수요를 뒷받침하고 있습니다. 한편, 캐나다의 광업·에너지 부문에서는 독자적인 전문 제품 요구가 존재합니다. 북미는 기술 혁신의 최전선에 있으며 IoT 센서와 연결 기능을 갖춘 스마트 보호 신발을 세계 최초로 채용했습니다. 또한 멕시코의 급성장하는 자동차·전자기기 조립산업과 NAFTA 무역관계의 장점이 함께 지역 시장을 더욱 확대하고 국경을 넘은 공급망을 효율화하고 있습니다.

유럽 시장은 가맹국간 안전 기준을 통일함과 동시에 무역·제조 효율을 높이는 조화 규격 EN ISO 20345 : 2022의 채용에 의해 크게 영향을 받고 있습니다. 근로자 보호, 환경 지속가능성, 기업의 사회적 책임에 대한 강한 주력이 특히 환경을 배려한 소재와 고급 안전 기능을 갖춘 프리미엄 안전화 수요 급증으로 이어지고 있습니다. 유럽 제조업체는 기업의 ESG 정책에 따라 바이오 대체 소재와 재생 소재를 통합한 지속 가능한 소재 개발의 최전선에 서 있습니다. 독일, 영국, 프랑스 등의 주요 시장은 견조한 제조업, 건설업, 에너지 부문에 의해 계속 성장하고 있습니다. 또한 개인 보호구 규칙 2016/425에 따른 유럽 규제 프레임워크는 엄격한 안전 기준을 유지할 뿐만 아니라 안전화 디자인과 소재의 혁신을 촉진하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 7.18%로 예측되어 가장 빠르게 성장할 것으로 예측됩니다. 이 성장은 급속한 산업화, 인프라 개발, 신흥 경제국의 안전 기준 강화 추진에 의해 견인되고 있습니다. 중국 제조업의 견고한 기반과 적극적인 인프라 투자 계획은 보호 신발 수요 급증을 가져왔습니다. 동시에 인도의 확대하는 공업·건설 섹터가 시장을 더욱 추진하고 있습니다. 이 지역에서는 직장 안전과 규제 준수를 추진하는 정부의 이니셔티브가 이익을 얻고 있지만, 이러한 규제의 시행 상황은 선진국과 개발 도상국에서 크게 다릅니다. 일본과 호주와 같은 성숙시장에서는 엄격한 안전기준이 유지되고 있는 반면 인도네시아, 태국, 베트남을 포함한 동남아시아 국가에서는 제조업 확대와 외국투자 유입을 주요 요인으로 급속한 성장을 볼 수 있습니다. 이 지역 성장 궤적은 다양한 경제 상황에서 산업 활동 증가와 안전 의식 및 규제 시행의 점진적인 향상을 반영합니다.

남미는 중동 및 아프리카와 함께 엄청난 성장 가능성을 지닌 신흥 시장으로 자리매김하고 있습니다. 이 잠재성은 주로 천연 자원 채굴, 인프라 개발, 산업 확대 등의 활동에 기인하고 있습니다. 브라질에서는 광업, 석유 및 가스, 건설업 등의 분야가 안전화 수요를 견인하고 있습니다. 아르헨티나와 칠레에서는 광업과 에너지 산업이 이 수요를 지원하고 있습니다. 중동에서는 석유 및 가스 산업과 대규모 인프라 프로젝트가 보호 신발의 적합성 확보에 대한 필요성을 강조합니다. 직장 안전의 지역 진전으로 사우디아라비아에서는 새로운 PPE 기술 규제가 도입되었습니다(사우디 규격청). 아프리카에서는 남아프리카와 나이지리아의 광업 부문이 특수 보호 신발 수요를 견인하는 반면, 시장의 성장은 경제적 문제와 규제 시행의 장벽에 의해 억제되고 있습니다. 이러한 지역이 경제적으로 발전을 계속하고 안전 의식을 높여 나가면서 유망한 장기적인 성장 기회가 제시될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 직장의 안전과 규제 준수에 대한 주목의 고조

- 급속한 인프라 정비가 개인용 보호구(PPE)의 지출을 촉진

- 혁신적이고 가볍고 인체 공학에 기반한 신발 디자인의 채용

- 바이오 베이스 및 재생 소재를 우선하는 기업의 ESG 방침

- 접속형 「스마트」안전화(IoT센서)의 도입

- 전기적 위험 보호 부츠에 대한 수요 증가

- 시장 성장 억제요인

- 저비용의 위조품의 만연

- 신흥 시장에서 중소기업 계약자들 사이의 높은 가격 탄력성

- 복잡한 규제 준수 및 인증 비용

- 중소기업의 업계 및 노동자에 대한 인식 부족

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 재료별

- 가죽

- 합성 가죽

- 고무

- 기타 재료

- 제품 유형별

- 부츠(높은 발목 보호)

- 신발(낮은 발목 보호)

- 최종 사용자 업계별

- 건설

- 제조

- 석유 및 가스

- 광업

- 화학

- 의약품 및 헬스케어

- 물류 및 운송

- 유틸리티 및 에너지

- 식품 및 음료

- 기타 산업

- 유통 채널별

- 온라인 채널

- 오프라인 채널

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 스페인

- 네덜란드

- 폴란드

- 벨기에

- 스웨덴

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 인도네시아

- 한국

- 태국

- 싱가포르

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 칠레

- 페루

- 기타 남미

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 모로코

- 튀르키예

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Honeywell International Inc.

- VF Corporation

- Wolverine World Wide Inc.

- Bata Corporation

- Dunlop Protective Footwear

- Uvex Group

- Rock Fall Ltd.

- Cofra Srl

- U-Power Group SpA

- Rahman Group

- Oftenrich Holdings(Safety Jogger)

- Red Wing Shoe Company

- Haix Group

- JAL Group

- ELTEN GmbH

- KEEN Utility

- Saina Corporation Co. Ltd

- COFRA Holding AG

- Jallatte

- Hillson Footwear Pvt. Ltd

제7장 시장 기회와 미래 동향

KTH 26.01.22The industrial protective footwear market was valued at USD 10.72 billion in 2025 and estimated to grow from USD 11.26 billion in 2026 to reach USD 14.41 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

Robust construction pipelines, stringent safety mandates, and swift material innovations bolster this growth. The rising acceptance of composite toe caps and breathable membranes among workers is noteworthy. Furthermore, updated OSHA 29 CFR 1910.136 mandates have intensified fit-testing and performance standards across job sites. Increased infrastructure investments in Asia and the Middle East are driving demand. Additionally, the emergence of "smart" boots, integrated with IoT sensors, is steering procurement choices towards data-centric safety solutions. While challenges like counterfeit trade and price sensitivity among smaller contractors persist, the market finds favor in corporate ESG targets, especially those emphasizing bio-based and recycled materials.

Global Industrial Protective Footwear Market Trends and Insights

Increased focus on workplace safety and regulatory compliance

As governments tighten workplace safety standards, the adoption of protective footwear is on the rise, driven by intensified regulatory enforcement. Under OSHA's 2025 updates, employers must ensure proper protective footwear selection and worker training across construction, manufacturing, and general industry applications. These updates, mandated under 29 CFR 1910.136, come from the Occupational Safety and Health Administration. While the Bureau of Labor Statistics noted a total of 2.6 million nonfatal workplace injuries in 2023, marking an 8.4% drop from 2022, certain sectors still grapple with foot and ankle injuries. Specifically, construction sees an incidence rate of 8.14%, agriculture at 10.23%, and transportation leading with 11.06%. In Europe, markets are aligning with the EN ISO 20345:2022 standards. These harmonized requirements not only bolster worker protection but also streamline cross-border trade. Such regulatory alignment reduces compliance fragmentation, allowing manufacturers to capitalize on economies of scale across major markets. Analyzing the healthcare sector, slip, trip, and fall incidents are notably influenced by slipping, accounting for 42.9% of cases. However, trials conducted by the NHS, as reported by the Health and Safety Executive, highlight that slip-resistant footwear can cut these incident rates by 37%.

Rapid infrastructure build boosting PPE spend

As construction and energy projects expand, emerging markets are ramping up infrastructure investments, leading to a sustained demand for industrial protective footwear. The U.S. Census Bureau highlighted a correlation between rising construction spending and the procurement cycles of protective equipment. This is especially evident in heavy construction and infrastructure segments, which have a pronounced need for specialized safety footwear. Meanwhile, in the Asia-Pacific, urbanization and industrial growth are driving infrastructure development, spurring demand for protective footwear in construction, mining, and energy sectors. In India, Southeast Asia, and the Middle East, government infrastructure programs are enforcing international safety standards, paving the way for certified protective footwear manufacturers to enter the market. Trends in supply chain localization are bolstering regional manufacturing, curbing import dependencies, and addressing the surging infrastructure demand. Furthermore, the ripple effect of infrastructure spending touches not just direct construction but also maintenance, utilities, and ancillary industries, all of which emphasize protective footwear compliance. Highlighting this trend, Saudi Arabia's new PPE technical regulation underscores how nations with a focus on infrastructure are weaving safety mandates into their broader development strategies, as noted by the Saudi Standards Authority.

Proliferation of low-cost counterfeit products

Counterfeit protective footwear not only jeopardizes worker safety but also distorts market dynamics, putting legitimate manufacturers at a disadvantage. An OECD analysis highlights the gravity of the issue, revealing a global counterfeit trade exceeding USD 467 billion. Alarmingly, footwear accounts for a staggering 62% of all seized counterfeit goods, as detailed in the OECD Counterfeit Report. Testing by the British Safety Industry Federation uncovered a troubling trend: a significant volume of non-compliant safety footwear in UK markets. These counterfeits, while visually convincing, often fall short of basic safety standards. In a striking example of the widespread nature of this issue, authorities in the Philippines confiscated counterfeit footwear valued at PHP 152 million, underscoring the challenge faced by protective equipment markets, especially in developing nations. Such counterfeit products not only lack essential safety certifications but also utilize inferior materials and often don't pass performance tests. This oversight poses significant liability risks for employers and endangers workers. The rise of online marketplaces has further exacerbated the issue, streamlining the distribution of counterfeit goods and complicating detection and enforcement efforts for both regulatory bodies and genuine manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of innovative, lightweight, and ergonomic footwear designs

- Corporate ESG mandates favoring bio-based and recycled materials

- High price elasticity among SME contractors in emerging markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, leather commands a dominant 62.74% market share, thanks to its unmatched durability, breathability, and acceptance in various industrial applications. Chrome-tanned leather, known for its abrasion resistance and comfort, is the go-to choice in construction and manufacturing, where all-day wear comfort is paramount. Yet, as environmental concerns rise and corporate sustainability becomes a mandate, material preferences shift. Notably, a study by MDPI highlights that leather uppers account for 39.9% of the carbon footprint in professional safety boots. Meanwhile, synthetic leather is gaining ground, boasting enhanced performance and a smaller environmental footprint. Rubber segments, on the other hand, are on a growth trajectory, expanding at a 6.49% CAGR through 2031, driven by heightened demand in the oil, gas, and chemical processing sectors for their chemical resistance.

As the material landscape shifts, manufacturers are turning to bio-based alternatives and recycled content to align with ESG mandates. Innovations in natural rubber, sourced from guayule and Russian dandelion, are curbing petroleum reliance without compromising the performance standards essential for industrial protective footwear, as highlighted in the MDPI Rubber Textiles Review. Advanced composites and textile-rubber blends are carving out niches, offering specialized properties like electrical hazard protection and extreme temperature resistance. Furthermore, regulatory frameworks like ASTM F2413 and EN ISO 20345:2022 guarantee material performance across the board, fostering innovation while upholding safety standards.

In 2025, boots command a dominant 66.92% share of the protective footwear market, thanks to their superior ankle protection and adaptability across various industrial settings. Such high-ankle protection is vital in sectors like construction, mining, and heavy manufacturing, where workers contend with hazards ranging from falling objects to chemical exposure. The boot segment is also reaping the rewards of technological advancements, with manufacturers now integrating lightweight materials, ergonomic designs, and smart sensor features, all while upholding stringent protection standards. In contrast, shoes are witnessing a more rapid growth, projected at a 5.46% CAGR through 2031. This surge is largely attributed to their adoption in light manufacturing, logistics, and service sectors, where the emphasis shifts from ankle protection to worker comfort.

Innovations in product design are increasingly targeting traditional comfort issues, all while upholding safety standards. Research from the MDPI Clinical Study highlights a significant concern: conventional safety boots, typically weighing between 550-650 grams, hinder worker mobility and lead to discomfort for 83.3% of users. This revelation is fueling a growing demand for lighter alternatives. Meanwhile, low-ankle shoe designs are gaining traction among workers in warehousing, food processing, and healthcare. In these sectors, the emphasis is on mobility and comfort, often sidelining the need for stringent ankle protection. This evolution in product types mirrors the shifting dynamics of the workplace. As service sectors burgeon and traditional heavy industries embrace automation, the focus is not just on mitigating physical hazards but also on ensuring foot protection remains paramount.

The Industrial Protective Footwear Report is Segmented by Material (Leather, Synthetic Leather, Rubber, and More), Product Type (Boots, and Shoes), End-User Industry (Construction, Manufacturing, Oil and Gas, Mining, and More), Distribution Channel (Online, and Offline), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, North America holds a commanding 28.21% market share, buoyed by stringent OSHA regulations, a booming construction sector, and advanced manufacturing industries that prioritize worker protection. Under the mature regulatory framework of 29 CFR 1910.136, the Occupational Safety and Health Administration mandates protective footwear across construction, manufacturing, and general industries, ensuring stable demand even in fluctuating economic conditions. Rising construction spending and infrastructure investments in the U.S. bolster the demand for protective footwear. Meanwhile, Canada's mining and energy sectors have their own specialized product needs. North America is at the forefront of technological advancements, being the first to adopt smart protective footwear equipped with IoT sensors and connectivity. Additionally, Mexico's burgeoning automotive and electronics assembly sectors, coupled with the advantages of NAFTA trade relationships, further amplify the regional market and streamline cross-border supply chains.

Europe's market is significantly influenced by the harmonized EN ISO 20345:2022 standards, which not only unify safety requirements across member states but also enhance trade and manufacturing efficiency. The continent's strong focus on worker protection, environmental sustainability, and corporate social responsibility has led to a surge in demand for premium protective footwear, especially those crafted from eco-friendly materials and boasting advanced safety features. European manufacturers are at the forefront of developing sustainable materials, integrating bio-based alternatives and recycled content to align with corporate ESG mandates. Major markets like Germany, the United Kingdom, and France thrive due to their robust manufacturing, construction, and energy sectors. Furthermore, the European regulatory framework, under PPE Regulation 2016/425, not only upholds stringent safety standards but also fosters innovation in the design and materials of protective footwear.

Asia-Pacific is poised to be the fastest-growing region, with a projected CAGR of 7.18% through 2031. This growth is fueled by rapid industrialization, infrastructure development, and a push for enhanced safety standards in emerging economies. China's stronghold in manufacturing and its aggressive infrastructure investment programs lead to a surge in demand for protective footwear. Concurrently, India's expanding industrial and construction sectors further propel the market. While the region benefits from government initiatives advocating workplace safety and regulatory adherence, the enforcement of these regulations varies widely between developed and developing nations. Mature markets like Japan and Australia uphold stringent safety standards, whereas Southeast Asian nations, including Indonesia, Thailand, and Vietnam, are witnessing swift growth, largely driven by manufacturing expansion and an influx of foreign investments. This regional growth trajectory mirrors the rising industrial activities and a gradual uptick in safety awareness and regulatory enforcement across varying economic landscapes.

South America, along with the Middle East and Africa, stands as an emerging market with vast growth potential. This potential is largely attributed to activities in natural resource extraction, infrastructure development, and industrial expansion. In Brazil, sectors like mining, oil and gas, and construction fuel the demand for protective footwear. Argentina and Chile bolster this demand through their mining and energy industries. The Middle East, with its oil and gas industry and expansive infrastructure projects, underscores the necessity for protective footwear compliance. Highlighting regional strides in workplace safety, Saudi Arabia has introduced a new PPE technical regulation [Saudi Standards Authority]. In Africa, while the mining sectors in South Africa and Nigeria drive the demand for specialized protective footwear, the market's growth is tempered by economic challenges and hurdles in regulatory enforcement. As these regions continue to evolve economically and heighten their safety awareness, they present promising long-term growth opportunities.

- Honeywell International Inc.

- VF Corporation

- Wolverine World Wide Inc.

- Bata Corporation

- Dunlop Protective Footwear

- Uvex Group

- Rock Fall Ltd.

- Cofra S.r.l.

- U-Power Group S.p.A

- Rahman Group

- Oftenrich Holdings (Safety Jogger)

- Red Wing Shoe Company

- Haix Group

- JAL Group

- ELTEN GmbH

- KEEN Utility

- Saina Corporation Co. Ltd

- COFRA Holding AG

- Jallatte

- Hillson Footwear Pvt. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased focus on workplace safety and regulatory compliance

- 4.2.2 Rapid infrastructure build boosting PPE spend

- 4.2.3 Adoption of innovative, lightweight, and ergonomic footwear designs

- 4.2.4 Corporate ESG mandates favouring bio-based and recycled materials

- 4.2.5 Deployment of connected "smart" safety boots (IoT sensors)

- 4.2.6 Heightened demand for electrical hazard protection boots

- 4.3 Market Restraints

- 4.3.1 Proliferation of low-cost counterfeit products

- 4.3.2 High price elasticity among SME contractors in emerging markets

- 4.3.3 Complex regulatory compliance and certification costs

- 4.3.4 Lack of industry and worker awareness in small and medium enterprises

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Leather

- 5.1.2 Synthetic Leather

- 5.1.3 Rubber

- 5.1.4 Other Materials

- 5.2 By Product Type

- 5.2.1 Boots (high ankle protection)

- 5.2.2 Shoes (low ankle protection)

- 5.3 By End-User Industry

- 5.3.1 Construction

- 5.3.2 Manufacturing

- 5.3.3 Oil and Gas

- 5.3.4 Mining

- 5.3.5 Chemicals

- 5.3.6 Pharmaceuticals and Healthcare

- 5.3.7 Logistics and Transportation

- 5.3.8 Utilities and Energy

- 5.3.9 Food and Beverage

- 5.3.10 Other Industries

- 5.4 By Distribution Channel

- 5.4.1 Online Channel

- 5.4.2 Offline Channel

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 VF Corporation

- 6.4.3 Wolverine World Wide Inc.

- 6.4.4 Bata Corporation

- 6.4.5 Dunlop Protective Footwear

- 6.4.6 Uvex Group

- 6.4.7 Rock Fall Ltd.

- 6.4.8 Cofra S.r.l.

- 6.4.9 U-Power Group S.p.A

- 6.4.10 Rahman Group

- 6.4.11 Oftenrich Holdings (Safety Jogger)

- 6.4.12 Red Wing Shoe Company

- 6.4.13 Haix Group

- 6.4.14 JAL Group

- 6.4.15 ELTEN GmbH

- 6.4.16 KEEN Utility

- 6.4.17 Saina Corporation Co. Ltd

- 6.4.18 COFRA Holding AG

- 6.4.19 Jallatte

- 6.4.20 Hillson Footwear Pvt. Ltd