|

시장보고서

상품코드

1910543

곤충 기피제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Insect Repellent - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

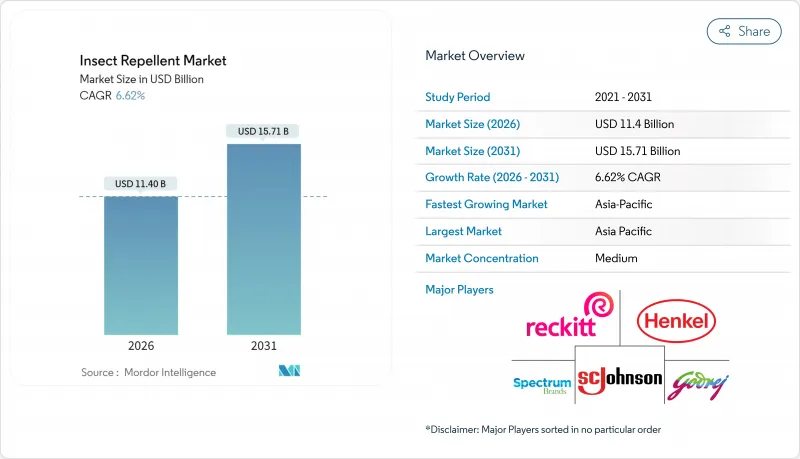

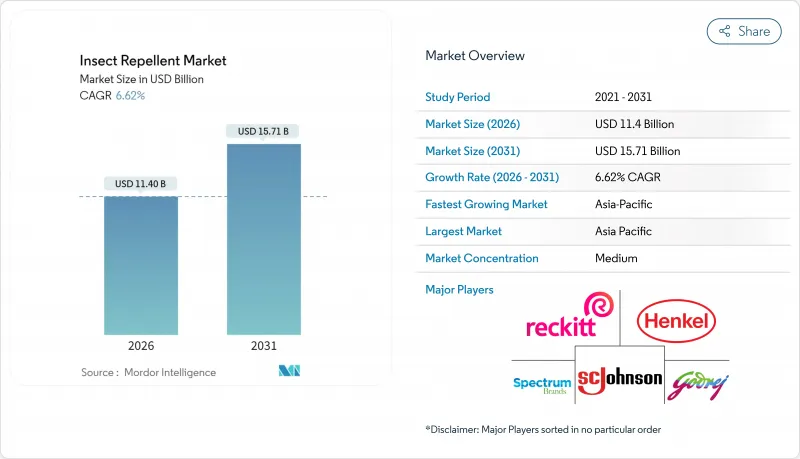

2026년 곤충 기피제 시장 규모는 114억 달러로 추정되며, 2025년 106억 9,000만 달러에서 성장했으며, 2031년에는 157억 1,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 6.62%를 나타낼 전망입니다.

이 성장 궤도는 주로 다음 요인에 의해 견인됩니다. 중재 질환에 대한 세계 우려 증가, 야외 생활의 확대, 보호 효과와 사용자 편의성을 모두 향상시키는 공급 시스템의 지속적인 혁신입니다. 유럽위원회는 라틴아메리카 카리브해 지역에서 아이티와 브라질이 중재 질환의 위험이 가장 높은 국가라고 지적합니다. 2025년, 이들 국가들은 지카바이러스와 뎅기열과 같은 질병에 대한 지표 점수를 각각 8.9와 8.8로 기록했습니다. 아시아태평양이 주요 지역 거점으로서의 지위를 유지하는 한편, 북미와 유럽에서는 기후 변화에 의한 모기의 서식지 확대를 배경으로 수요가 급증하고 있습니다. 천연 유래의 유효 성분이나 공간 처리제가 주목을 받는 한편, N,N-디에틸-m-톨루아미드(DEET)나 피레스로이드계 살충제 등 기존 제품은 확립된 유효성과 규제 당국의 승인에 의해 우위성을 유지하고 있습니다. 시장 진출기업은 R&D 투자, 계절 한정 프로모션, 전자상거래 강화에 주력하여 가격 감응도와 프리미엄화 동향의 미묘한 균형을 모색하고 있습니다.

세계의 곤충 기피제 시장 동향과 인사이트

매개 질환 증가

중재 질환은 세계적으로 증가하는 경향이 있습니다. 세계보건기구(WHO)는 2024년 9월 팩트시트에서 모기나 진드기 등 절지동물에 의해 매개되는 질환에 의한 연간 사망자 수가 70만명을 넘는다고 지적했습니다. 기후 변화에 의해 매개생물의 서식지역이 북상해, 과거 안전으로 여겨지고 있던 온대지역에도 말라리아나 뎅기열의 위협이 미치고 있습니다. 미국 질병 예방 관리 센터(CDC)에 따르면 2024년에는 북미, 중남미, 남미 및 카리브해 지역에서 1,300만 건 이상의 뎅기열 증례가 보고되었습니다. 이 지역의 뎅기열 감염률은 2025년에도 높은 수준을 유지했습니다. 이러한 급증으로 인해 새롭게 위험에 노출된 지역에서는 기피제에 대한 수요가 증가하고 있습니다. 또한 말라리아 매개 모기의 피레스 로이드 내성은 현재 감시 대상 지역의 80% 이상에 영향을 미치는 세계 우려 사항입니다. 이러한 내성으로 소비자는 대체 유효성분을 찾아 새로운 제제 개발을 촉진하고 있습니다. 이러한 과제에 대응하여 정부보건기구는 개인방호책의 권장을 강화하고 있습니다. 특히 CDC는 DEET, 피카리딘, IR3535를 병매 생물에 대한 효과적인 보호책으로 최우선 선택으로 꼽고 있습니다.

증가하는 야외 레크리에이션 활동

유행에 의한 생활양식의 변화에 따라 야외 레크리에이션 참여가 현저하게 증가했습니다. 예를 들어 아웃도어재단의 보고에 따르면 2024년에는 미국에서 6,340만명 이상이 하이킹 활동을 적어도 1회 실시했습니다. 이는 2010년 이후 최고의 참가율을 보여주며 지난 15년간 약 31% 포인트의 성장을 이루고 있습니다. 소비자가 레크리에이션 용품에 해충 대책 기능을 도입하는 동향이 강해지고 있는 가운데, 어드벤처 투어리즘이나 아웃도어 스포츠 용품의 매출은 기피제 시장의 성장과 직접적인 상관관계를 나타내고 있습니다. 이 동향은 캠프나 하이킹 등 전통적인 활동에 머무르지 않고, 야외에서의 식사, 페스티벌, 도시의 녹지 이용 등에도 퍼져, 시장의 옷자락을 자연 애호가 이외에도 확대하고 있습니다. 게다가 건설업, 농업, 조경업 등의 분야에서 일하는 전문의 야외 작업자는 지금까지 간과되기 쉬웠지만, 업무용 곤충 기피제 수요를 크게 밀어 올리고 있습니다.

대체 보호 수단과의 경쟁

대체 보호 기술이 기존의 기피제 시장에 점점 진출하고 있습니다. 퍼메트린 처리 의류, 모기장, 전자기기 등의 제품은 그 효능에 대한 증거가 여전히 찬반양론임에도 불구하고 소비자의 관심을 모으고 있습니다. 체계적인 검토에 따르면, 전자 모기 장치는 모기 착륙에 대해 측정 가능한 보호 효과를 제공하지 못합니다. 그러나 소비자들은 편의성과 화학물질을 사용하지 않는 매력에 매료되어 계속 채택하고 있습니다. 퍼메트린 처리 의류는 도포형 기피제보다 방호 지속시간이 길다는 이점이 있지만, 이 우위성은 시장에 있어서 대체 리스크를 가져오고 있어, 특히 아웃도어 전문가나 군사 유저에 있어서 현저합니다. 주택환경에 있어서는 환경조정, 생물적 방제, 물리적 장벽을 통합한 종합적 해충 관리 전략이 개인용 기피제품에 대한 의존도를 저하시키고 있습니다. 게다가 초음파 기피 기능을 구사하는 스마트폰 앱의 등장은 그 효과를 부정하는 과학적 증거가 있음에도 불구하고 소비자의 동향을 부각하고 있습니다. 즉, 대체 기술을 탐구하려는 의지가 기존 제품의 전환을 지연시킬 수 있다는 것입니다.

부문 분석

2025년 시점에서 스프레이 및 에어로졸 제품은 편의성, 휴대성, 즉각적인 사용 측면에서 광범위한 소비자들에게 지지되어 45.72% 시장 점유율을 차지했습니다. 한편, 액체식 가습기는 2031년까지 연평균 복합 성장률(CAGR) 7.32%로 가장 급성장하고 있는 부문입니다. 이러한 급성장은 공간보호기술의 진보와 핸즈프리로 지속적인 효과를 추구하는 소비자의 지향변화에 지지되고 있습니다. 코일식은 연소 부산물에 대한 우려가 있는 것, 가격에 민감한 시장에서는 여전히 지위를 유지하고 있습니다. 한편, 매트식은 기존의 코일식과 현대적인 액체 시스템의 균형을 맞추고 있습니다. 병충해 종합 관리를 위해 설계된 미끼 제품은 규제 장벽과 복잡한 적용 방법으로 성장 과제에 직면 해 있습니다.

액체 증발기는 특히 서방 메커니즘 및 휘발성 피레스 로이드 제형에서 특허 기술 혁신의 혜택을 누리고 있습니다. 특필해야할 것은 2024년 7월에 고드레이 컨슈머 프로덕츠사가 발표한 「레노푸르트린」입니다. 이것은 액체 증발기 용으로 개발된 인도 최초의 국산 모기 기피 분자입니다. 이 첨단 제형은 카트리지 당 12시간의 보호 효과를 약속하며 활성 성분의 지속적인 방출을 보장합니다. 이 혁신은 소비자가 요구하는 지속적인 효과를 충족하고 빈번한 재 도포의 필요성을 줄입니다. 웨어러블 디바이스와 전자식 디스펜서와 같은 신흥 카테고리는 기피제공급을 일상 제품에 통합하고 있지만, 그 시장에서의 존재감은 아직 겸손하고, 효과의 검증과 비용 저하가 기다리고 있습니다.

2025년 시점에서 기존 곤충 기피제는 82.10% 시장 점유율을 차지했습니다. 이는 수십년에 걸쳐 입증된 효과, 규제 당국의 승인, DEET, 피카리딘, 피레스로이드 제제의 확립된 제조거점에 의해 지원되고 있습니다. 한편 천연유래의 곤충 기피제는 성장궤도에 있으며 2031년까지 연평균 복합 성장률(CAGR) 8.05%를 나타낼 것으로 전망됩니다. 이 급성장은 소비자의 건강 의식이 높아지고 레몬 유칼립투스 오일과 각종 정유 블렌드 등 식물성 유효 성분에 대한 규제면의 지원에 뒷받침되고 있습니다. 성장률의 격차는 소비자의 우선순위 변화를 나타내며, 안전성과 환경 지속성의 향상을 기대할 수 있다면 보호기간이 짧아도 선호하는 소비자가 늘고 있습니다.

조사에 의해 천연 성분의 유효성이 뒷받침되고 있습니다. 예를 들어, PMD(파라멘탄-3,8-디올)는 적절한 농도로 사용하면 주요 매개종에 대한 DEET와 동등한 성능을 발휘합니다. 또한 나노에멀젼 기술 등의 발전으로 식물성 성분의 안정성과 생체이용률이 향상되고 있습니다. 이 혁신은 식물 유래 기피제가 기존에 가지고 있던 과제, 예를 들어 급속한 분해나 효과의 편차에 대처하는 것입니다. 천연제품에 대한 프리미엄 가격의 수용이 진행되고 이익률 확대의 가능성을 시사하고 있는 한편, 식물성 원료의 조달난이 시장 점유율의 급속한 확대를 억제할 가능성이 있습니다.

지역별 분석

2025년 시점에서 아시아태평양은 세계 수익의 49.10%를 차지했으며, 2031년까지의 기간에 지역별로 가장 높은 CAGR 9.15%로 성장을 지속하고 있습니다. 이것은 주로 뎅기열과 말라리아에 대한 공중 보건에 대한 지속적인 관심이 견인하고 있습니다. 정부 주도의 계발활동과 매스미디어 캠페인의 시너지 효과에 의해 기피제의 채용이 대폭 증가했습니다. 현지 연구개발 능력의 증거로 인도의 'Goodknight Flash'(레노플루트린 배합)는 수입 비용 절감에 기여할 뿐만 아니라 공급의 탄력 강화에도 기여하고 있습니다. 가처분 소득이 증가함에 따라 도시의 가정에서는 기존의 모기 향에서 액체 증발기로의 전환이 진행되어 지역 곤충 기피제 시장을 더욱 확대하고 있습니다.

북미는 후진을 숭배하고 있지만, 야외 레크리에이션 활동의 활발함과 곤충 매개 질환의 만연으로 인해 여전히 큰 시장 규모를 자랑하고 있습니다. 2024년에는 미국의 소매 매출이 3억 7,690만 달러에 달했습니다. 이 지역에서는 식물 유래 성분에 대한 강한 기호성으로부터 프리미엄 가격 설정이 가능해 혁신적인 제품에는 높은 이익률을 기대할 수 있습니다. 게다가 기후 변화의 영향으로 북부 제주의 모기의 활동기가 장기화 되어, 종래와 같은 여름철의 급격한 수요 피크가 아니라, 월간 베이스에서의 안정된 곤충 기피제 수요가 태어나고 있습니다.

유럽의 성장은 엄격한 화학물질 규제에 의해 억제되고 있으며, 업계는 생태독성학 기준에 따라 천연 유래 처방으로 전환하고 있습니다. 독일과 프랑스는 최전선에 서서 지속가능성 인증을 추진하고 재활용 가능한 포장 채용을 촉진하고 있습니다.

중동 및 아프리카에서는 말라리아 발생 지역에서의 기증자 자금에 의한 대처가 보급을 촉진하여 저소득층 커뮤니티에 대한 기피제 액세스 향상에 기여하고 있습니다.

한편, 라틴아메리카에서는 열대 지역으로의 도시 확대에 따라 병매 생물과의 접촉 기회가 증가하고 있으며, 다양한 제품 라인업의 확충과 현지 생산에 대한 투자가 급증하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 매개 생물에 의한 감염증 증가

- 증가하는 아웃도어레크리에이션 활동

- 반려동물 사육 증가

- 천연 제품에 대한 소비자 기호의 변화

- 급속한 기술 진보가 혁신을 추진

- 정부 및 공중위생 캠페인

- 시장 성장 억제요인

- 대체 보호 방법과의 경쟁

- 화학물질에 대한 소비자의 건강에 대한 우려

- 살충제 내성

- 위조품의 유통

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 미끼

- 코일

- 스프레이 및 에어로졸

- 매트

- 액체 증발기

- 기타 제품 유형

- 성분 유형별

- 천연 곤충 기피제

- 기존 곤충 기피제

- 최종 사용자별

- 성인용

- 어린이 및 유아

- 유통 채널별

- 슈퍼마켓 및 하이퍼마켓

- 편의점

- 온라인 소매점

- 기타 유통 채널

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 칠레

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 스웨덴

- 벨기에

- 폴란드

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 태국

- 싱가포르

- 인도네시아

- 한국

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

- 나이지리아

- 이집트

- 모로코

- 튀르키예

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SC Johnson & Son Inc.

- Reckitt Benckiser Group PLC

- Spectrum Brands Holdings Inc.

- Godrej Consumer Products Ltd.

- Dabur India Ltd.

- Henkel AG & Co. KGaA

- Newell Brands Inc.

- Enesis Group

- Quantum Health

- Jyothy Labs Limited

- Sawyer Products Inc.

- Avon Products Inc.

- Tender Corporation(Natrapel)

- Kao Corporation

- The Coleman Company, Inc.

- Merck KGaA(IR3535)

- 3M

- Coleman(Repel brand)

- Wondercide Inc.

- Sawyer Products, Inc.

- Enesis Group

제7장 시장 기회와 향후 전망

KTH 26.01.22Insect repellent market size in 2026 is estimated at USD 11.4 billion, growing from 2025 value of USD 10.69 billion with 2031 projections showing USD 15.71 billion, growing at 6.62% CAGR over 2026-2031.

This growth trajectory is largely driven by escalating global apprehensions regarding vector-borne diseases, a burgeoning outdoor lifestyle, and ongoing innovations in delivery systems that enhance both protection and user convenience. The European Commission highlights Haiti and Brazil as the foremost nations at risk of vector-borne diseases in Latin America and the Caribbean. In 2025, these countries registered index scores of 8.9 and 8.8, respectively, for diseases like the Zika virus and Dengue fever. While Asia-Pacific continues to dominate as the primary regional hub, North America and Europe are witnessing a surge in demand, spurred by climate change's expansion of mosquito habitats. Although natural active ingredients and spatial formats are gaining popularity, traditional offerings like N, N-diethyl-meta-toluamide (DEET) and pyrethroids maintain their edge due to established efficacy and regulatory acceptance. Players in the market are focusing on research and development investments, seasonal promotions, and bolstering e-commerce presence, navigating the delicate balance between price sensitivity and the trend towards premiumization.

Global Insect Repellent Market Trends and Insights

Rise in Vector-borne Diseases

Vector-borne diseases are on the rise worldwide. The World Health Organization (WHO) highlighted in its September 2024 factsheet that over 700,000 deaths occur annually due to diseases spread by mosquitoes, ticks, and other arthropods. Climate change is pushing vector habitats further north, bringing malaria and dengue threats to temperate regions that were once safe. According to the Centers for Disease Control and Prevention, in 2024, more than 13 million cases of dengue were reported in North, Central, and South America and the Caribbean. Dengue transmission in these areas remains high in 2025. This surge has led to a heightened demand for repellents in these newly at-risk areas. Furthermore, pyrethroid resistance in malaria vectors is now a global concern, affecting over 80% of monitored sites. This resistance is steering consumers towards alternative active ingredients and spurring innovation in new formulations. In response to these challenges, government health agencies are amplifying their recommendations for personal protective measures. Notably, the CDC has highlighted DEET, picaridin, and IR3535 as top choices for effective protection against disease vectors.

Increasing Outdoor Recreational Activities

In the wake of pandemic-induced lifestyle changes, outdoor recreation saw a notable uptick in participation. For example, the Outdoor Foundation reported that in 2024, over 63.4 million individuals in the U.S. engaged in hiking activities at least once. This marks the highest participation rate since 2010, showcasing a growth of approximately 31 percentage points over the past 15 years. As consumers increasingly incorporate pest protection into their recreational gear, sales in adventure tourism and outdoor sports equipment have seen a direct correlation with the growth of the repellent market. This trend isn't limited to traditional activities like camping and hiking; it now encompasses outdoor dining, festivals, and the use of urban green spaces, expanding the market's reach beyond just wilderness enthusiasts. Moreover, professional outdoor workers from sectors like construction, agriculture, and landscaping, often overlooked, are significantly boosting the demand for commercial-grade repellents.

Competition from Alternative Protection Methods

Alternative protection technologies are increasingly encroaching on the traditional repellent market. Products like permethrin-treated clothing, bed nets, and electronic devices are drawing consumer interest, even as evidence of their efficacy remains mixed. Systematic reviews indicate that electronic mosquito repellents fail to offer measurable protection against mosquito landings. Yet, consumers continue to adopt them, swayed by their perceived convenience and the allure of being chemical-free. While permethrin-treated clothing boasts a longer protection duration than topical repellents, this advantage poses a substitution risk in the market, especially for outdoor professionals and military users. In residential settings, integrated pest management strategies, merging environmental tweaks, biological controls, and physical barriers, are diminishing the dependence on personal repellent products. Furthermore, the rise of smartphone apps touting ultrasonic repellent features, despite scientific evidence debunking their effectiveness, underscores a consumer trend: a willingness to explore alternative technologies, potentially postponing the shift away from traditional products.

Other drivers and restraints analyzed in the detailed report include:

- Growing Pet Ownership

- Shifting Consumer Preferences Towards Natural Products

- Consumer Health Concerns Over Chemicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, sprays and aerosols command the market with a 45.72% share, capitalizing on their convenience, portability, and instant application appeal to a wide range of consumers. Meanwhile, liquid vaporizers are the fastest-growing segment, boasting a 7.32% CAGR through 2031. This surge is fueled by tech advancements in spatial protection and a consumer shift towards hands-free, continuous coverage. While coils hold their ground in price-sensitive markets, despite concerns over combustion byproducts, mats strike a balance between traditional coils and modern liquid systems. Bait products, tailored for integrated pest management, face growth challenges due to regulatory hurdles and complex applications.

Liquid vaporizers are reaping the rewards of patent innovations, especially in controlled-release mechanisms and volatile pyrethroid formulations. Notably, in July 2024, Godrej Consumer Products unveiled 'Renofluthrin', India's inaugural indigenous mosquito repellent molecule, tailored for liquid vaporizers. These advanced formulations promise 12-hour protection per cartridge, ensuring a steady release of active ingredients. This innovation meets consumer demands for prolonged efficacy, reducing the need for frequent reapplications. Emerging categories like wearable devices and electronic dispensers are weaving repellent delivery into everyday products, but their market presence is still modest, awaiting validation of efficacy and a drop in costs.

In 2025, conventional insect repellents command an 82.10% market share, bolstered by decades of proven efficacy, regulatory endorsements, and a well-established manufacturing base for DEET, picaridin, and pyrethroid formulations. Meanwhile, natural insect repellents are on a growth trajectory, boasting an 8.05% CAGR through 2031. This surge is fueled by a rising consumer health consciousness and regulatory backing for botanical active ingredients, such as oil of lemon eucalyptus and various essential oil blends. The disparity in growth rates underscores a shift in consumer priorities: many now prefer shorter protection durations if it means enhanced safety and environmental sustainability.

Research underscores the efficacy of natural ingredients. For instance, PMD (para-menthane-3,8-diol) matches DEET's performance against major vector species, provided it's used in the right concentrations. Furthermore, advancements like nano-emulsion technologies bolster the stability and bioavailability of botanical ingredients. This innovation addresses the traditional challenges of plant-based repellents, such as swift degradation and variable efficacy. While there's a growing acceptance of premium pricing for natural products, hinting at potential margin expansions, challenges in sourcing botanical ingredients could temper swift market share growth.

The Insect Repellent Market is Segmented by Product Type (Bait, Coils, Sprays/Aerosols, Mats, Liquid Vaporizer, and More), by Ingredient Type (Natural Insect Repellent and Conventional Insect Repellent), by End User (Adults and Kids/Children), by Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region accounted for 49.10% of global revenue, and the region also registers the strongest regional CAGR at 9.15% during the period to 2031, primarily driven by the ongoing public health focus on dengue and malaria. Government-led awareness initiatives, bolstered by mass media campaigns, have significantly increased the adoption of repellents. A testament to local research and development capabilities, India's Goodknight Flash, featuring Renofluthrin, not only cuts down on import costs but also fortifies supply resilience. With rising disposable incomes, urban households are upgrading from traditional coils to liquid vaporizers, further expanding the regional insect repellent market.

North America, while trailing, boasts substantial figures, largely due to outdoor recreational activities and the spread of insect-borne diseases. In 2024, retail sales in the U.S. reached an impressive USD 376.9 million. The region's strong preference for botanical ingredients allows for premium pricing and higher margins for innovators. Additionally, climate change has lengthened the mosquito season in northern states, leading to a more consistent monthly demand for insect repellents, rather than the previously sharp summer peak.

Europe's growth is tempered by stringent chemical regulations, pushing the industry towards natural formulations that align with eco-toxicology standards. Germany and France are at the forefront, championing sustainability certifications and driving the adoption of recyclable packaging.

In the Middle East and Africa, donor-funded initiatives are bolstering distribution in malaria-prone areas, making repellents more accessible to lower-income communities.

Meanwhile, Latin America's urban sprawl into tropical regions is increasing contact with disease vectors, prompting a surge in diverse product offerings and investments in localized manufacturing.

- S.C. Johnson & Son Inc.

- Reckitt Benckiser Group PLC

- Spectrum Brands Holdings Inc.

- Godrej Consumer Products Ltd.

- Dabur India Ltd.

- Henkel AG & Co. KGaA

- Newell Brands Inc.

- Enesis Group

- Quantum Health

- Jyothy Labs Limited

- Sawyer Products Inc.

- Avon Products Inc.

- Tender Corporation (Natrapel)

- Kao Corporation

- The Coleman Company, Inc.

- Merck KGaA (IR3535)

- 3M

- Coleman (Repel brand)

- Wondercide Inc.

- Sawyer Products, Inc.

- Enesis Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Vector-borne Diseases

- 4.2.2 Increasing Outdoor Recreational Activities

- 4.2.3 Growing Pet Ownership

- 4.2.4 Shifting Consumer Preferences Towards Natural Products

- 4.2.5 Rapid Technological Advancements Driving Innovation

- 4.2.6 Government and Public Health Campaigns

- 4.3 Market Restraints

- 4.3.1 Competition from Alternative Protection Methods

- 4.3.2 Consumer Health Concerns Over Chemicals

- 4.3.3 Insecticide Resistance

- 4.3.4 Availability of Counterfeit Products

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Product Type

- 5.1.1 Bait

- 5.1.2 Coils

- 5.1.3 Sprays/Aerosols

- 5.1.4 Mats

- 5.1.5 Liquid Vaporizer

- 5.1.6 Other Product Types

- 5.2 By Ingredient Type

- 5.2.1 Natural Insect Repellent

- 5.2.2 Conventional Insect Repellent

- 5.3 By End User

- 5.3.1 Adults

- 5.3.2 Kids/Children

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Chile

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Sweden

- 5.5.3.8 Belgium

- 5.5.3.9 Poland

- 5.5.3.10 Netherlands

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Thailand

- 5.5.4.5 Singapore

- 5.5.4.6 Indonesia

- 5.5.4.7 South Korea

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 S.C. Johnson & Son Inc.

- 6.4.2 Reckitt Benckiser Group PLC

- 6.4.3 Spectrum Brands Holdings Inc.

- 6.4.4 Godrej Consumer Products Ltd.

- 6.4.5 Dabur India Ltd.

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Newell Brands Inc.

- 6.4.8 Enesis Group

- 6.4.9 Quantum Health

- 6.4.10 Jyothy Labs Limited

- 6.4.11 Sawyer Products Inc.

- 6.4.12 Avon Products Inc.

- 6.4.13 Tender Corporation (Natrapel)

- 6.4.14 Kao Corporation

- 6.4.15 The Coleman Company, Inc.

- 6.4.16 Merck KGaA (IR3535)

- 6.4.17 3M

- 6.4.18 Coleman (Repel brand)

- 6.4.19 Wondercide Inc.

- 6.4.20 Sawyer Products, Inc.

- 6.4.21 Enesis Group