|

시장보고서

상품코드

1910545

RV(레저용 차량) 렌탈 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Recreational Vehicle Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

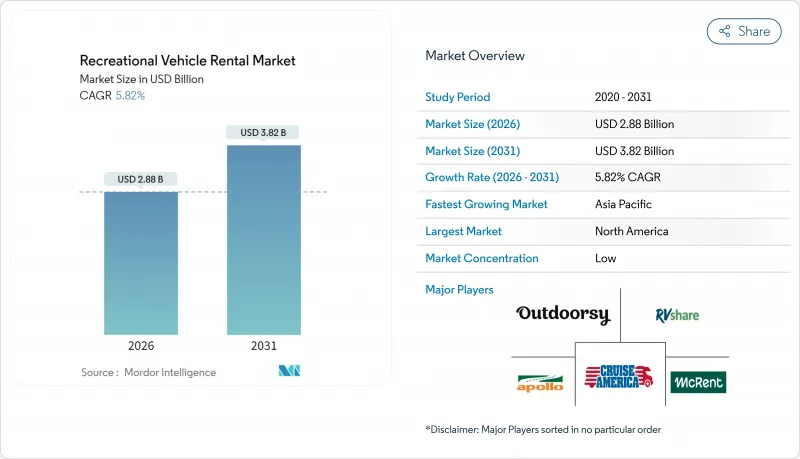

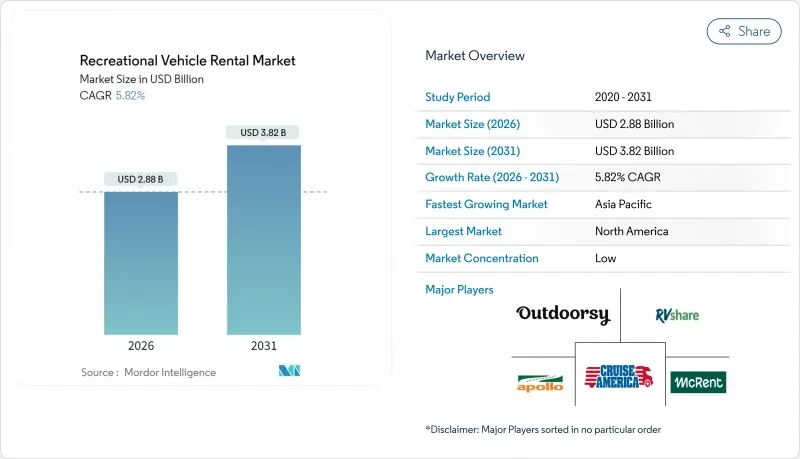

RV(레저용 차량) 렌탈 시장은 2025년에 27억 2,000만 달러로 평가되었으며, 2026년 28억 8,000만 달러에서 2031년까지 38억 2,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 5.82%로 예상됩니다.

연료가격의 상승이나 조닝규제에 의한 운영비용 증가가 발생하는 가운데 꾸준한 성장이 발생하고 있습니다. 도로 여행 휴가로의 구조적인 전환이 수요를 끌어올려, 피어 투 피어 예약 플랫폼의 보급, 운전 및 유지관리가 용이한 현대 차량을 목표로 한 설계 개량이 진행되고 있습니다. 사업자 측은 차량 가동률 향상을 위해 텔레매틱스 도입을 가속화하고 있으며, 여러 주나 EU 국가의 정책 수립자는 제로 에미션 인센티브를 차량 업그레이드 사이클과 연동시키는 움직임을 보이고 있습니다. 경쟁 환경은 유동적이며 통합 시도는 독점 금지법의 심사에 직면하고 있지만, 조달과 보험의 규모의 경제는 여전히 대규모 플릿 소유자에게 유리하게 작동하고 있습니다.

세계의 RV(레저용 차량) 렌탈 시장의 동향 및 인사이트

국내 도로 여행 관광 급증

국내 도로 여행은 팬데믹의 대안에서 주류 레저 옵션으로 이동했습니다. 설문 조사에 따르면 미국 여행자의 70%가 2025년 최소 1회의 도로 여행을 계획했으며 이는 2023년 57%에서 증가하였습니다. 부유층도 이 동향에 참여하여 이용량이 유지되고 평균 1차 렌탈 요금을 밀어 올리고 있습니다. 도로 여행자는 자급 자족형 이동 수단을 요구하기 때문에 차량 탑재 샤워나 Wi-Fi를 갖춘 모터 홈을 선택하는 가족이 증가하고 있습니다. 여행사에 따르면, 2025년 중반에 예약된 패키지 여행의 거의 절반이 운전 여정이 중심이며 이는 전년의 두 배에 이르렀습니다. 이 지속적인 도입은 RV(레저용 차량) 렌탈 시장에 직접 이익을 가져오는 독립 여행으로의 지속적인 전환을 뒷받침합니다.

피어 투 피어(P2P) 렌탈 플랫폼 확대

P2P 네트워크는 미사용 재고의 활용을 가능하게 했습니다. Outdoorsy 플랫폼은 2024년에 누적 예약 금액 30억 달러를 돌파했으며, 2029년까지 80억 달러를 목표로 하고 있습니다. 소유주의 증가는 전문적인 플릿 확장을 능가하고, RV(레저용 차량) 렌탈 시장은 대규모의 대차대조표 투자 없이 차량 선택권 및 지리적 도달범위를 확장할 수 있습니다. 도시 이용자의 이용 거리 문제를 해결하는 배송 서비스를 제공하여 평균 P2P 여행일수는 7일로 증가했습니다. 플랫폼 보험 프로그램과 24시간 365일 긴급출동 지원은 처음 사용하는 사람들의 위험 인식을 완화합니다. 매력적인 단위 경제성으로 인해 가격 상승률은 호텔 업계의 인플레이션률보다 낮아 반복 예약을 촉진하는 가치 격차가 확대되고 있습니다.

높은 유지보수 비용과 보험 비용

현대의 RV는 복잡한 배터리, 슬라이드 아웃 기구, 인포테인먼트 시스템을 탑재하여 수리비가 증가하고 있습니다. 숙련 엔지니어는 여전히 부족하고 주요 시장에서는 정비 공장의 노동 단가가 시간당 160 달러를 초과합니다. 대규모 플릿은 여러 차량에 대해 보험 계약을 협상할 수 있지만 소규모 소유자는 이를 따라갈 수 없으며 이는 RV(레저용 차량) 렌탈 시장 내 비용 격차를 확대하고 있습니다. 예방 프로그램 및 연장 보증은 효과적이지만 현금 흐름에 제약이 있는 사업자에게 부담이 되는 자본 지출이 필요합니다.

부문 분석

2025년 매출의 69.60%를 플릿 사업자가 차지했지만, 개인 소유자가 가장 높은 성장률을 나타냈습니다. 규모의 경제에 의해 기업 플릿은 일괄 구매 할인, 집중 관리된 유지보수, 포괄적인 보험 확보가 가능합니다. 통합기업은 지역 도달범위 확대를 위해 볼트온 인수를 추진하고 있지만 호주에서의 아폴로 모터홈과 투어리즘 홀딩스의 제안 등 경쟁 감시기관은 반경쟁적 움직임을 저지하고 있습니다. 제로 에미션 규제와 관련된 컴플라이언스 비용은 저장소 충전기 및 기술자 재훈련을 위한 자금 조달이 가능한 자본력 있는 플릿에 유리하게 작용합니다.

개인 소유자는 P2P 플랫폼이 예약, 인증 및 보험을 일괄적으로 제공하는 환경에서 확대되고 있습니다. 많은 소유주는 지역 이벤트와 반려동물 동반이 가능한 캠핑카와 같은 틈새 형태에 주력함으로써 연간 운영률을 높이고 있습니다. 플랫폼이 제공하는 정비 네트워크에 의해 소규모 소유주는 인프라를 구축하지 않고도 안전 검사에 대응 가능합니다. 이러한 추세로 인해 개인 소유주는 직접적인 대안이 아닌 민첩한 보완 역할로 자리매김하고, 결과적으로 RV(레저용 차량) 렌탈 시장 전체의 선택을 풍부하게 하고 있습니다.

온라인 채널은 2025년 렌탈 시장의 61.10%를 차지하였고, 7.89%의 복합 성장률을 나타내며 이는 결정적인 디지털 전환을 반영하고 있습니다. 실시간 재고 관리, 동적 가격 설정 및 통합 결제로 예약 기간이 수주에서 수일로 단축되었습니다. 청년층 렌탈 이용자는 여행 계획을 모바일 앱에 의존하고 있으며, 사업자는 360도 차량 투어 및 AI 채팅 지원을 제공해야 합니다.

복잡한 여정에서는 처음으로 이용하는 고객이 차량 클래스, 캠프장 선정 및 경로 안전성에 대해 조언을 요구하기 때문에 오프라인 예약은 여전히 중요합니다. 사업자는 "채팅에서 매장으로"모델의 통합이 진행되고 고객은 온라인으로 계약을 시작한 후 쇼룸 방문 및 화상 통화로 최종 조건을 확정합니다. 이 하이브리드 방식은 대면 서비스의 신뢰성이라는 강점을 유지하면서 RV(레저용 차량) 렌탈 시장의 규모 확대를 실현합니다.

지역별 분석

북미는 2025년에도 46.30%의 수익 점유율을 유지했습니다. 미국은 광범위한 캠프장 네트워크, 성숙한 보험 상품, 높은 가처분 소득을 보유하고 있으며, 이는 RV(레저용 차량) 렌탈 시장의 활황을 뒷받침하고 있습니다. 캘리포니아의 '선진적 청정트럭 규제'는 이미 9개 주에서 채택되었으며 2025년 이후 제로 에미션 차량 판매의 단계적 확대를 의무화하고 있습니다. 이로 인해 초기 비용이 발생하지만 장기적으로 운영 비용 절감이 기대됩니다(rvia.org). 캐나다는 광대한 자연경관과 국내 관광을 위한 세제우대조치의 혜택을 받고 있으며, 멕시코에서는 고속도로 정비와 중산층의 확대로 잠재 수요가 확대되면서 조기 성장이 예상됩니다.

아시아태평양은 2031년까지 11.18%라는 가장 높은 CAGR을 기록할 전망입니다. 일본에서는 2024년 기준으로 등록 캠핑카가 16만 5천대였으며, 인증 RV파크 500곳 이상이 가동 중입니다. 중국에서는 국내 EV 공급망과 신규 고속도로망을 배경으로 렌터카 에코시스템이 급속히 확대되고 있습니다. 호주는 백패커의 주요 여행지로 존재감을 유지하고 있지만 경쟁 당국은 가격 상승을 초래할 수 있는 차량 통합에 반대하고 있습니다. 인도에서는 신규 여행자의 공급이 대폭 증가하고 있으며, 주 관광국의 지원에 의한 도로 시설 정비가 RV(레저용 차량) 렌탈 시장의 진입 장벽을 저하시키고 있습니다.

유럽에서는 국경을 넘은 여행 규제의 조화와 저배출 존의 확대에 의해 꾸준한 성장을 이루고 있습니다. 어윈 하이머 그룹은 2024년에 33억 6,000만 달러의 매출로 유럽 시장에서 점유율 23.6%를 획득했습니다(erwinhymergroup.com). 독일의 아우토반과 밀집한 판매점 네트워크가 교환 수요를 촉진하는 한편, 프랑스와 스페인은 해안부의 매력과 확립된 캠프장 문화에 의존하고 있습니다. 동유럽 회원국에서는 결속기금에 의한 도로 정비가 진행되어 RV 보급률이 서서히 높아지고 있습니다. 노르웨이에서 이탈리아에 이르는 전기자동차 충전 회랑은 배터리 구동 모터 홈에 대한 신뢰를 높이고 유럽을 제로 에미션 차량의 시험장으로 자리매김하고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 국내 도로 여행 관광의 급증

- 피어 투 피어(P2P) 렌탈 플랫폼 확대

- 밀레니얼 세대 및 Z세대의 가처분 소득 증가

- 텔레매틱스를 활용한 플릿 가동률 최적화

- RV를 이동식 팝업 스페이스로 활용하는 기업

- 제로 에미션 RV의 인센티브가 전동화 차량의 도입을 가속화

- 억제요인

- 높은 유지비와 보험 비용

- 계절성에 의한 자산 가동률 저하

- 지자체에 의한 RV 차량의 야간 주차 규제

- 부품 공급의 병목으로 인한 가동률 저하

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 공급자의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측(금액)

- 렌탈 공급자 유형별

- 개인 소유자

- 플릿 운영자

- 예약 유형별

- 오프라인 예약

- 온라인 예약

- 제품 유형별

- 모터 홈

- 클래스 A 모터 홈

- 클래스 B 모터 홈

- 클래스 C 모터 홈

- 견인식 RV

- 피프스 휠 트레일러

- 여행 트레일러

- 트럭 캠퍼

- 스포츠 유틸리티 트레일러

- 모터 홈

- 렌탈 기간별

- 단기(1-7일)

- 중기(8-30일)

- 장기(30일 이상)

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Cruise America

- Apollo Tourism & Leisure Ltd

- Outdoorsy, Inc.

- RVshare

- McRent

- Indie Campers

- RoadSurfer GmbH

- Camplify

- Yescapa

- El Monte RV

- Just Go Motorhome Hire

- Escape Campervans

- JUCY Rentals

- Spaceships Rentals

- Bunk Campers

제7장 시장 기회 및 미래 전망

CSM 26.02.04The RV Rental Market was valued at USD 2.72 billion in 2025 and estimated to grow from USD 2.88 billion in 2026 to reach USD 3.82 billion by 2031, at a CAGR of 5.82% during the forecast period (2026-2031).

Consistent growth is visible even as fuel inflation and zoning constraints raise operating costs. A structural pivot toward road-trip vacations lifts demand, the spread of peer-to-peer booking platforms, and design upgrades that make modern vehicles easier to drive and maintain. Operators are accelerating telematics roll-outs to improve vehicle uptime, while policymakers in several states and EU countries are linking zero-emission incentives to fleet turnover. Competitive dynamics remain fluid as consolidation attempts meet antitrust scrutiny, yet scale advantages in procurement and insurance continue to favor large fleet owners.

Global Recreational Vehicle Rental Market Trends and Insights

Surge in Domestic Road-Trip Tourism

Domestic road-trip travel has moved from pandemic workaround to mainstream leisure choice. Surveys show 70% of U.S. travelers plan at least one road trip during 2025, up from 57% in 2023. Affluent households are joining the trend, lifting average daily rental rates without dampening volume. Road travelers seek self-contained mobility, which pushes more families toward motorized units equipped with onboard showers and Wi-Fi. Travel agencies report that nearly half of packaged vacations booked in mid-2025 revolve around drive-in itineraries, double the prior year. This continued adoption confirms a lasting shift toward independent travel that directly benefits the RV rental market.

Expansion of Peer-to-Peer (P2P) Rental Platforms

P2P networks have unlocked underused inventory. Outdoorsy alone surpassed USD 3 billion in lifetime bookings in 2024 and targets USD 8 billion by 2029. Host growth outpaces professional fleet additions, helping the RV rental market widen vehicle choice and geographic reach without heavy balance-sheet investment. Average P2P trip length rose to seven days, aided by delivery services that solve last-mile issues for urban renters. Platform insurance programs and 24/7 roadside support lower perceived risk for first-time users. Attractive unit economics keep price increases below hotel inflation, extending the value gap that fuels repeat bookings.

High Maintenance & Insurance Costs

Modern RVs carry complex batteries, slide-outs, and infotainment systems that drive repair bills higher. Skilled technicians remain scarce, pushing workshop labor rates past USD 160 per hour in top markets. Large fleets can negotiate multi-vehicle policies that small owners cannot match, widening cost disparities inside the RV rental market. Preventive programs and extended warranties help, yet they demand capital outlays that weigh on cash-flow-constrained operators.

Other drivers and restraints analyzed in the detailed report include:

- Rising Disposable Income Among Millennials & Gen-Z

- Telematics-Enabled Fleet Uptime Optimization

- Municipal Restrictions on Overnight RV Parking

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fleet operators controlled 69.60% of 2025 revenue while individual owners delivered the fastest growth. Scale lets corporate fleets secure bulk purchasing discounts, centralized maintenance, and umbrella insurance. Consolidators pursue bolt-on acquisitions to extend regional coverage, yet competition watchdogs have blocked anticompetitive moves such as the Apollo Tourism-Tourism Holdings proposal in Australia. Compliance costs linked to zero-emission mandates favor well-capitalized fleets that can finance depot chargers and technician re-training.

Private owners thrive where P2P platforms provide turnkey booking, verification, and insurance. Many reach higher annual utilization by targeting local events and niche formats such as pet-friendly campervans. Platform-provided maintenance networks allow small owners to meet safety inspections without building infrastructure. These dynamics position individual hosts as agile complements rather than direct substitutes, ultimately enriching choice across the RV rental market.

Online channels captured 61.10% of 2025 rentals and compound at an 7.89% rate, reflecting a decisive digital shift. Real-time inventory, dynamic pricing, and integrated payments shorten the booking window from weeks to days. Younger renters rely on mobile apps for trip planning, pushing operators to offer 360-degree vehicle tours and AI chat support.

Offline bookings remain relevant for complex itineraries where first-time users seek advice on vehicle class, campground selection, and route safety. Operators increasingly integrate chat-to-store models: customers start online, then finalize terms through showroom visits or video calls. This hybrid approach preserves the trust advantage of personal service while scaling the reach of the RV rental market.

The RV Rental Market is Segmented by Rental Supplier Type (Private and Individual Owners and Fleet Operators), Booking Type (Offline Booking and Online Booking), Product Type (Motorized RVs and Towable RVs), Rental Duration (Short-Term, Mid-Term and Long-Term), and Geography (North America, South America, Europe, Asia-Pacific and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 46.30% revenue share in 2025. The United States supplies an extensive campground grid, mature insurance products, and high disposable income that keep the rv rental market buoyant. California's Advanced Clean Trucks rule, already adopted by nine additional states, will require escalating zero-emission sales from 2025, creating upfront costs but long-term operating savings rvia.org. Canada benefits from expansive wilderness routes and tax incentives for domestic tourism, while Mexico shows early promise where highway upgrades and middle-class expansion widen addressable demand.

Asia-Pacific posts the fastest 11.18% CAGR through 2031. Japan leads with 165,000 registered campervans and over 500 certified RV parks as of 2024. China's car-rental ecosystem grows quickly on the back of domestic EV supply chains and new highway corridors. Australia remains a core backpacker circuit, though competition authorities oppose fleet mergers that could raise prices. India supplies a sizable pipeline of first-time travelers; supportive state tourism boards fund roadside amenities that lower entry barriers for the RV rental market.

Europe delivers steady growth as cross-border travel rules harmonize and low-emission zones expand. The Erwin Hymer Group captured 23.6% European market share in 2024 on USD 3.36 billion sales erwinhymergroup.com. Germany's autobahn network and dense dealer footprint foster high replacement demand, while France and Spain rely on coastal draws and established campsite cultures. Eastern EU members receive cohesion-funded road upgrades that gradually raise RV adoption rates. Electric-charging corridors from Norway to Italy enhance confidence in battery-powered motorhomes, positioning Europe as a test bed for zero-emission fleets.

- Cruise America

- Apollo Tourism & Leisure Ltd

- Outdoorsy, Inc.

- RVshare

- McRent

- Indie Campers

- RoadSurfer GmbH

- Camplify

- Yescapa

- El Monte RV

- Just Go Motorhome Hire

- Escape Campervans

- JUCY Rentals

- Spaceships Rentals

- Bunk Campers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Domestic Road-Trip Tourism

- 4.2.2 Expansion of Peer-To-Peer (P2P) Rental Platforms

- 4.2.3 Rising Disposable Income Among Millennials & Gen-Z

- 4.2.4 Telematics-Enabled Fleet Uptime Optimisation

- 4.2.5 Corporate Use of Rvs As Mobile Pop-Up Spaces

- 4.2.6 Zero-Emission RV Incentives Accelerating Electrified Fleets

- 4.3 Market Restraints

- 4.3.1 High Maintenance and Insurance Costs

- 4.3.2 Seasonality-Driven Low Asset Utilisation

- 4.3.3 Municipal Restrictions On Overnight RV Parking

- 4.3.4 Spare-Part Supply Bottlenecks Delaying Turnaround

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Rental Supplier Type

- 5.1.1 Private and Individual Owners

- 5.1.2 Fleet Operators

- 5.2 By Booking Type

- 5.2.1 Offline Booking

- 5.2.2 Online Booking

- 5.3 By Product Type

- 5.3.1 Motorized RVs

- 5.3.1.1 Class A Motorhomes

- 5.3.1.2 Class B Motorhomes

- 5.3.1.3 Class C Motorhomes

- 5.3.2 Towable RVs

- 5.3.2.1 Fifth-Wheel Trailers

- 5.3.2.2 Travel Trailers

- 5.3.2.3 Truck Campers

- 5.3.2.4 Sports Utility Trailers

- 5.3.1 Motorized RVs

- 5.4 By Rental Duration

- 5.4.1 Short-term (1-7 days)

- 5.4.2 Mid-term (8-30 days)

- 5.4.3 Long-term (More than 30 days)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Cruise America

- 6.4.2 Apollo Tourism & Leisure Ltd

- 6.4.3 Outdoorsy, Inc.

- 6.4.4 RVshare

- 6.4.5 McRent

- 6.4.6 Indie Campers

- 6.4.7 RoadSurfer GmbH

- 6.4.8 Camplify

- 6.4.9 Yescapa

- 6.4.10 El Monte RV

- 6.4.11 Just Go Motorhome Hire

- 6.4.12 Escape Campervans

- 6.4.13 JUCY Rentals

- 6.4.14 Spaceships Rentals

- 6.4.15 Bunk Campers