|

시장보고서

상품코드

1910548

지능형 가상 비서 - 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Intelligent Virtual Assistant (IVA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

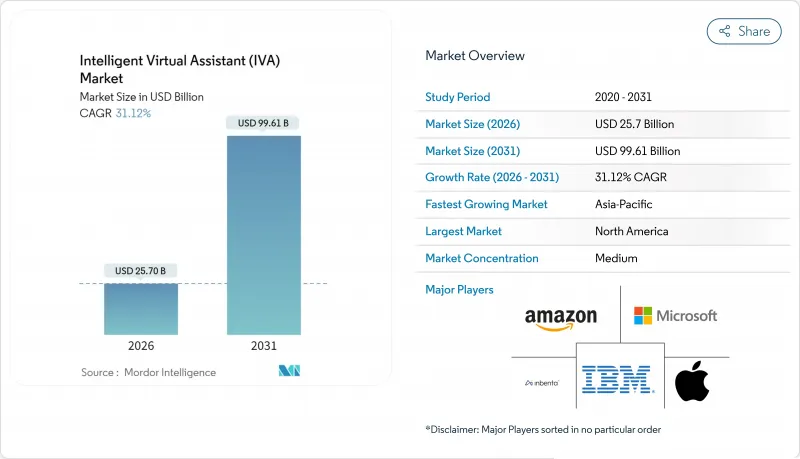

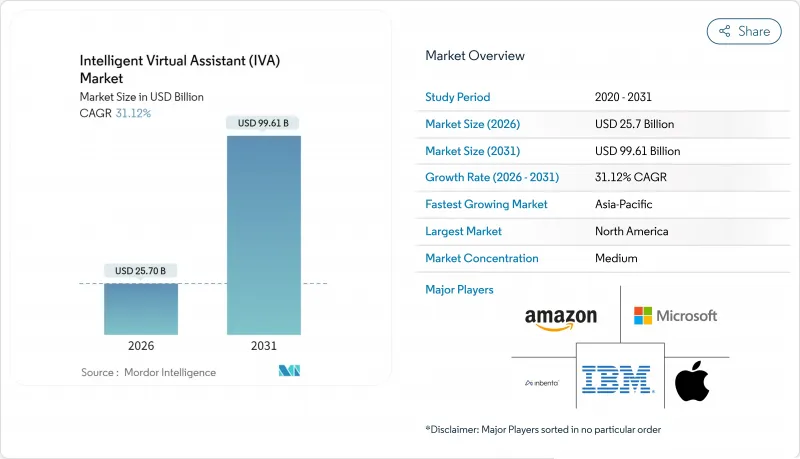

지능형 가상 비서 시장은 2025년 196억 달러에서 2026년 257억 달러로 성장하고 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 31.12%를 나타낼 전망입니다. 2031년까지 996억 1,000만 달러에 달할 것으로 예측되고 있습니다.

이 급속한 확대의 주요 요인은 다국어 대응의 대규모 언어 모델, 1대당 약 4만 달러로 판매되는 전용 AI 칩에 의한 단말 내 추론, 확대하는 클라우드 비용을 억제하려는 기업의 압력입니다. 생성형 AI의 도입이 명확한 비용 절감 효과를 보여주기 때문에 기업은 계속 투자하고 있습니다. 예를 들어, 주요 여행사는 IVA 주도 셀프 서비스 채널 도입 이후 연간 1,000만 달러의 비용 절감을 달성했다고 보고했습니다. 클라우드가 여전히 주류인 것, 하이퍼스케일 사업자에 대한 지속적인 지불을 피할 수 있는 에지 및 On-Premise 옵션의 우선순위가 증가하고 있습니다. 이 기세는 소비자용 하드웨어에서도 마찬가지로 두드러지며, 스마트 스피커나 차재 비서의 보급이 상시 접속형 대화 서비스에 대한 기대를 재구축하고 있습니다.

세계의 지능형 가상 비서 시장 동향과 인사이트

옴니채널 고객 서비스 챗봇 도입 확대

세계 은행은 2025년까지 챗봇 기술에 94억 달러를 투자했으며, 비용 억제의 필요성과 24시간 365일 서비스 기대가 강하게 일치하고 있음을 보여주었습니다. 자율해결률이 80-90%에 달하는 사례가 증가하고 있으며, 조기 도입한 은행에서는 생산성 향상이 40%에 달한 사례가 기록되어 있습니다. 소매업체는 텍스트, 음성 및 비주얼 채널을 단일 흐름으로 통합하고 상황에 따라 인간 운영자에게 원활하게 인수함으로써 고객 참여도가 40% 향상되었다고 보고합니다. 스토리지 기반 개인화를 통해 기기를 가로지르는 대화 기록을 저장하고 고객은 반복적으로 설명하지 않고 대화를 재개할 수 있습니다. 결과적으로 고객 만족도 점수를 높이고 컨택 센터의 작업 부하에서 측정 가능한 삭감을 실현했습니다.

스마트 스피커와 IoT 음성 단말기의 보급

자동차 제조업체 각 회사는 Cerence, Microsoft 및 NVIDIA의 음성 플랫폼을 활용하여 ChatGPT 스타일의 서비스를 인포테인먼트 시스템에 직접 통합합니다. 폭스바겐의 유럽 모델에는 이미 5개 언어 지원 클라우드 업데이트 비서가 탑재되어 있습니다. 자동차 분야를 제외한 가전제조업체와 웨어러블 브랜드는 개인정보 보호 및 지연 감소를 위해 로컬 음성 인식 기능을 통합합니다. 운전자 조사에 따르면 고급 기능을 사용할 수 있는 경우 77%가 차량용 음성 제어를 선택한다고 응답하고 있습니다. 벤더 각사가 동일한 코어 모델을 임베디드 실리콘에 이식하는 가운데, 지능형 가상 비서 시장은 가정·자동차·산업 환경에 있어서 새로운 일상 이용의 접점을 획득하고 있습니다.

지속적인 프라이버시와 데이터 보안에 대한 우려

EU의 인공지능법에서 개인정보보호 조항을 통해 공급업체는 설계 단계에서 데이터 최소화 및 암호화를 입증해야 합니다. 의료 분야에서 미국 ONC 규칙은 예측 알고리즘의 투명한 의사 결정 로그를 요구합니다. 금융기관은 추적 가능한 파이프라인과 차등 프라이버시 기술을 도입하고 있지만, 이러한 투자는 프로젝트 비용을 밀어 올리고 도입 사이클을 장기화하고 있습니다. 따라서 많은 경영진은 고객의 모든 발화를 자체 내부에 유지하는 On-Premise형 스택을 지지하고 있으며, 주권규칙을 충족하면서 동등한 클라우드 이용료에 비해 최대 80%의 비용 절감을 실현하고 있다고 보고되었습니다.

부문 분석

스마트 스피커는 2025년 수익의 45.68%를 차지하며 음악 및 동영상 서비스와의 번들 판매를 통해 확대를 계속하는 대규모 설치 기반을 뒷받침했습니다. 성숙 시장에서 성장이 둔화되고 있는 벤더는 고충실도 마이크와 로컬 언어 모델 추론 기능을 갖춘 프리미엄 플랜을 업셀하고 클라우드 호출을 삭감하고 있습니다. 한편, 자동차 비서는 2031년까지 연평균 복합 성장률(CAGR) 32.58%를 달성할 전망으로 하드웨어 카테고리 중 가장 높은 성장률을 보이고 있습니다. 폭스바겐 및 르노와 같은 자동차 제조업체는 Cerence의 화이트 라벨 제품을 활용하여 주행 중 대화형 내비게이션, 에어컨 제어 및 전자상거래 서비스를 제공합니다.

AR 헤드셋 및 산업용 스캐너를 위한 웨어러블/임베디드 IVA 모듈은 새로운 진입 경로를 제공하여 물류 및 현장 유지 보수 작업에서 작업자의 손을 해제하는 음성 명령을 실현합니다. 이러한 장치는 음성과 시선, 제스처, 촉각 피드백을 결합하여 사용자의 인체 공학적 편의성을 높입니다. 지능형 가상 비서 시장은 현재 거치형 스피커에서 완전 모바일 단말기까지 지속적으로 확산되고 있으며, 각 폼 팩터의 연산 능력 한계에 맞추어 신경망의 실적를 최적화하는 움직임이 진행되고 있습니다.

클라우드 배포는 쉬운 스케일링, 모델 업데이트, 기업 소프트웨어와의 통합성으로 인해 현재 지출의 67.35%를 차지합니다. 그러나 비용 예측 가능성과 데이터 현지화 방법은 On-Premise 및 에지 배포로의 결정적인 전환을 촉진하며, 이는 연간 33.72%의 성장률을 나타냅니다. On-Premise에서 생성된 AI 칩을 도입하는 기업에서는 추론 비용이 동등한 클라우드 이용료의 1/5로 줄어들고 있습니다. 규제 대상 업계가 기밀성이 높은 음성 로그를 방화벽 내로 마이그레이션함에 따라 On-Premise를 위한 지능형 가상 비서 시장 규모는 급증할 것으로 전망됩니다.

에지 네이티브 IVA는 100ms 미만의 대기 시간이 필요한 자동차, 항공우주 및 의료기기 분야에서 실시간 작업 부하를 지원합니다. 공급업체 각 회사는 현재 8GB 미만의 메모리에서 양자화 LLM을 호스팅하는 신경 처리 단위 코어를 출하 중입니다. 이 특화된 설계를 통해 에너지 소비를 줄이면서 대화의 맥락을 유지할 수 있어 운전 중 및 수술 지원 시나리오에서 중단 없는 운영에 필수적인 요구 사항을 충족합니다.

지역별 분석

북미는 조기 기업 투자, 풍부한 벤처 캐피탈 및 성숙한 벤더 생태계를 배경으로 36.55%의 점유율을 차지합니다. 유타, 콜로라도, 캘리포니아의 주법은 투명성을 강조하며 연방 정부의 NIST 프레임워크는 공통 위험 관리 용어를 제공합니다. 의료용 IVA는 ONC 기준을 충족시키기 위해 설명 가능성의 증거를 기록해야 하며, 이로써 공급자는 완전한 의사결정 추적을 공개할 플랫폼을 선택하도록 촉구되고 있습니다. 캐나다의 접근성 의무화 표준 EN 301 549 : 2024는 장애가 있는 사용자에게도 대응하는 종합적인 음성 기술에 대한 수요를 더욱 확고하게 하고 있습니다. 이 지역의 연구 개발 능력과 견고한 컴플라이언스 문화가 결합되어 상용 전개에 있어서 우위성을 유지하고 있습니다.

아시아태평양은 34.05%의 연평균 복합 성장률(CAGR)로 가장 빠르게 확대되고 있습니다. 중국의 국가 로드맵과 싱가포르의 10억 싱가포르 달러 규모의 예산 배분 등 정부의 AI 전략이 인재육성과 파일럿 프로그램을 지원하고 있습니다. 인도의 은행업계에서의 대화형 AI의 도입 사례는 다국어 대응의 IVA가 저비용으로 지점망의 확대를 실현하는 방법을 나타냅니다. 일본의 자동차 제조업체는 자동차 비서를 브랜드 차별화 요소로 추진하고, 엣지 AI 칩을 통합함으로써 불안정한 휴대폰 통신망을 극복하고 있습니다. 언어의 다양성은 여전히 장벽이지만 최근 다국어 LLM의 비약적 진보로 개발 기간이 단축되고 중견기업에도 지능형 가상 비서 시장이 개방되고 있습니다.

유럽은 혁신과 엄격한 거버넌스의 균형을 이루는 중요한 역할을 담당합니다. EU AI법은 분류·문서화·인적 감시를 포괄하는 통일규칙을 부과하여 공급자에게 투명성이 높은 모델 아키텍처를 촉구하고 있습니다. 자동차 제조업체는 기능 안전 기준과 새로운 설명 가능성 조항을 모두 준수하기 위해 AI 전문가와 협력합니다. EN 301 549의 접근성 지침은 종합적인 설계를 보장하고 의료 기관은 엄격한 바이어스 감사를 거쳐 처음으로 IVA 도구를 채택합니다. 프라이버시와 공평성을 인증할 수 있는 벤더는 공공 부문 입찰에서 우선적 지위를 획득하여 유럽 전체경쟁 구도를 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 옴니채널 고객서비스 챗봇의 도입 확대

- 스마트 스피커 및 IoT 음성 단말기의 보급

- 다국어 대규모 언어 모델 NLP의 획기적인 진전

- 콘택트 센터의 비용 억제 압력

- 노인 케어 및 디지털 치료 분야에 있어서 감정 인식형 IVA의 도입 상황

- 공공 부문 디지털 서비스의 접근성 요구 사항

- 시장 성장 억제요인

- 지속적인 프라이버시와 데이터 보안에 대한 우려

- 복잡한 문의에 있어서 고객의 인적 에이전트에의 선호

- AI의 설명 가능성과 다크 패턴에 대한 규제 당국의 감시

- 환각 현상에 기인하는 브랜드 평판 리스크

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 챗봇

- 스마트 스피커

- 차 내 지능형 가상 비서

- 웨어러블 및 임베디드 디바이스

- 배포 모드별

- 클라우드

- On-Premise 및 엣지

- 사용자 인터페이스 기술별

- 텍스트 기반(텍스트 투 텍스트)

- 음성 베이스(ASR+TTS)

- 다중 모드(음성+시각)

- 최종 사용자별

- 소매 및 전자상거래

- BFSI

- 헬스케어

- 통신 및 IT

- 여행 및 숙박

- 기타 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amazon.com Inc.

- Google LLC(Alphabet)

- Apple Inc.

- Microsoft Corp.

- IBM Corp.

- Meta Platforms Inc.

- Alibaba Group

- Baidu Inc.

- Samsung Electronics Co. Ltd.

- Xiaomi Inc.

- OpenAI

- Anthropic

- Harman International

- Nuance Communications Inc.

- Avaamo Inc.

- EdgeVerve Systems Ltd.

- Ipsoft Inc.(Amelia)

- Kore.ai Inc.

- Inbenta Technologies Inc.

- Creative Virtual Ltd.

- Serviceaide Inc.

- Rasa Technologies GmbH

- SoundHound AI Inc.

- Tencent Holdings Ltd.

제7장 시장 기회와 향후 전망

KTH 26.01.22The intelligent virtual assistant market is expected to grow from USD 19.60 billion in 2025 to USD 25.7 billion in 2026 and is forecast to reach USD 99.61 billion by 2031 at 31.12% CAGR over 2026-2031.

Multilingual large-language models, on-device inference enabled by specialized AI chips that retail for about USD 40,000 per unit, and corporate pressure to curb expanding cloud costs are the primary forces behind this rapid expansion. Enterprises continue to invest because generative AI deployments are demonstrating clear savings; a major travel company, for example, reports USD 10 million in annual cost reductions after introducing an IVA-led self-service channel. Edge and on-premise options that avoid recurring hyperscale fees are moving up the priority list, even though cloud remains dominant. The momentum is equally visible in consumer hardware, as the popularity of smart speakers and in-car assistants reshapes expectations for always-on conversational services.

Global Intelligent Virtual Assistant (IVA) Market Trends and Insights

Rising Adoption of Omnichannel Customer-Service Chatbots

Global banks expect to invest USD 9.4 billion in chatbot technology by 2025, a sign of how strongly cost-containment needs align with 24/7 service expectations. Autonomous resolution rates of 80-90% are increasingly common, and productivity gains reaching 40% have been logged by early banking adopters. Retailers cite engagement lifts of 40% when text, voice, and visual channels are fused into a single flow, creating smooth hand-offs to human agents when context demands. Memory-based personalization now preserves conversation history across devices, allowing customers to resume interactions without repetition. The result is higher customer-satisfaction scores alongside measurable savings in contact-center workloads.

Proliferation of Smart Speakers and IoT Voice End-Points

Automotive OEMs tap voice platforms from Cerence, Microsoft, and NVIDIA to add ChatGPT-style services directly to infotainment stacks.Volkswagen's European models already ship with a cloud-updated assistant that supports five languages. Beyond cars, appliance makers and wearable brands embed local speech recognition to protect privacy and cut latency. Driver surveys find that 77% would choose in-vehicle voice control when advanced features are available. As vendors port the same core models to embedded silicon, the intelligent virtual assistant market gains new daily-use entry points inside homes, cars, and industrial settings.

Persistent Privacy and Data-Security Concerns

The EU AI Act's privacy-preserving clauses force suppliers to demonstrate data-minimization and encryption by design. In healthcare, U.S. ONC rules demand transparent decision logs for predictive algorithms. Financial institutions add traceable pipelines and differential-privacy techniques, but those investments raise project costs and lengthen deployment cycles. Many chiefs therefore favor on-premise stacks that keep all customer utterances in situ, reporting cost reductions of up to 80% versus equivalent cloud bills while satisfying sovereignty rules.

Other drivers and restraints analyzed in the detailed report include:

- Breakthroughs in Multilingual Large-Language-Model NLP

- Contact-Center Cost-Containment Pressure

- Regulatory Scrutiny on AI Explainability and Dark-Patterns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart speakers generated 45.68% of 2025 revenue, underscoring the sizeable installed base that continues to expand through bundling with music or video services. Although growth moderates in mature markets, vendors are upselling premium tiers that feature high-fidelity microphones and local language-model inference to reduce cloud calls. At the same time, in-car assistants are on track to post 32.58% CAGR through 2031, the fastest among hardware categories. Automakers such as Volkswagen and Renault use white-label offerings from Cerence to deliver conversational navigation, climate control, and e-commerce services on the road.

Wearable and embedded IVA modules for AR headsets and industrial scanners supply a fresh entry path, enabling voice commands that free workers' hands in logistics and field maintenance. These devices often combine voice with gaze, gesture, or haptic feedback, elevating user ergonomics. The intelligent virtual assistant market now spans a continuum from stationary speakers to fully mobile endpoints, and suppliers are tailoring neural-network footprints to the computational limits of each form factor.

Cloud deployment still accounts for 67.35% of current spend because of easy scaling, model updates, and integration with enterprise software. Yet, cost predictability and data-localization laws are driving a decisive turn to on-prem and edge deployments that are growing 33.72% annually. Enterprises deploying generative AI chips on site report overall inference expenses as low as one-fifth of comparable cloud bills. The intelligent virtual assistant market size for on-prem projects is forecast to expand sharply as regulated verticals move sensitive voice logs inside the firewall.

Edge-native IVAs support real-time workloads in automotive, aerospace, and healthcare devices where sub-100-millisecond latency is mandatory. Suppliers are now shipping neural-processing-unit cores that host quantized LLMs with less than 8 GB of memory. This specialization lowers energy draw while keeping conversational context intact, a key requirement for uninterrupted driving or surgical assistance scenarios.

The AI Virtual Assistant Market Report is Segmented by Product (Chatbot, Smart Speaker, and More), Deployment Mode (Cloud and On-Premise), User Interface Technology (Text-Based (Text-To-Text), Voice-Based (ASR + TTS), and More), End-User (BFSI, Healthcare, Telecom and IT, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds 36.55% share on the strength of early enterprise investment, a deep venture capital pool, and a maturing vendor ecosystem. State-level laws in Utah, Colorado, and California emphasize transparency, while the federal NIST framework offers a common risk-management vocabulary. Healthcare IVAs must log explainability evidence to meet ONC standards, prompting providers to choose platforms that expose full decision traces. Canada's accessibility mandate EN 301 549:2024 further cements demand for inclusive voice technologies that work for users with disabilities. The region's R&D capability combined with a robust compliance culture maintains a lead in commercial deployments.

Asia Pacific is the fastest-expanding region at 34.05% CAGR. Government AI strategies, such as China's national roadmap and Singapore's SGD 1 billion allocation, underwrite talent development and pilot programs. Conversational AI adoption in India's banking arena demonstrates how multilingual IVAs extend branch reach at lower cost. Japanese automakers push in-car assistants as brand differentiators, integrating edge AI chips to overcome patchy cellular coverage. Linguistic diversity remains a hurdle, but recent multilingual LLM breakthroughs shrink development timelines and open the intelligent virtual assistant market to mid-tier enterprises.

Europe occupies a pivotal role, balancing innovation with stringent governance. The EU AI Act imposes harmonized rules that cover classification, documentation, and human oversight, nudging suppliers toward transparent model architectures. Automotive firms collaborate with AI specialists to comply with both functional safety norms and new explainability clauses. Accessibility guidance in EN 301 549 ensures inclusive design, while healthcare institutions adopt IVA tools only after rigorous bias audits. Vendors that can certify privacy and fairness gain preferred status in public-sector tenders, shaping competitive dynamics across the continent.

- Amazon.com Inc.

- Google LLC (Alphabet)

- Apple Inc.

- Microsoft Corp.

- IBM Corp.

- Meta Platforms Inc.

- Alibaba Group

- Baidu Inc.

- Samsung Electronics Co. Ltd.

- Xiaomi Inc.

- OpenAI

- Anthropic

- Harman International

- Nuance Communications Inc.

- Avaamo Inc.

- EdgeVerve Systems Ltd.

- Ipsoft Inc. (Amelia)

- Kore.ai Inc.

- Inbenta Technologies Inc.

- Creative Virtual Ltd.

- Serviceaide Inc.

- Rasa Technologies GmbH

- SoundHound AI Inc.

- Tencent Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption of omnichannel customer-service chatbots

- 4.2.2 Proliferation of smart speakers and IoT voice end-points

- 4.2.3 Breakthroughs in multilingual large-language-model NLP

- 4.2.4 Contact-center cost-containment pressure

- 4.2.5 Emotion-aware IVA uptake in elder-care and digital therapeutics

- 4.2.6 Accessibility mandates for public-sector digital services

- 4.3 Market Restraints

- 4.3.1 Persistent privacy and data-security concerns

- 4.3.2 Customer preference for human agents in complex queries

- 4.3.3 Regulatory scrutiny on AI explainability and dark-patterns

- 4.3.4 Hallucination-driven brand-reputation risk

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product (Value)

- 5.1.1 Chatbots

- 5.1.2 Smart Speakers

- 5.1.3 In-Car IVAs

- 5.1.4 Wearable / Embedded Devices

- 5.2 By Deployment Mode (Value)

- 5.2.1 Cloud

- 5.2.2 On-premise / Edge

- 5.3 By User Interface Technology (Value)

- 5.3.1 Text-based (Text-to-Text)

- 5.3.2 Voice-based (ASR + TTS)

- 5.3.3 Multimodal (Voice + Visual)

- 5.4 By End-User

- 5.4.1 Retail and eCommerce

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Telecom and IT

- 5.4.5 Travel and Hospitality

- 5.4.6 Other Industries

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Netherlands

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon.com Inc.

- 6.4.2 Google LLC (Alphabet)

- 6.4.3 Apple Inc.

- 6.4.4 Microsoft Corp.

- 6.4.5 IBM Corp.

- 6.4.6 Meta Platforms Inc.

- 6.4.7 Alibaba Group

- 6.4.8 Baidu Inc.

- 6.4.9 Samsung Electronics Co. Ltd.

- 6.4.10 Xiaomi Inc.

- 6.4.11 OpenAI

- 6.4.12 Anthropic

- 6.4.13 Harman International

- 6.4.14 Nuance Communications Inc.

- 6.4.15 Avaamo Inc.

- 6.4.16 EdgeVerve Systems Ltd.

- 6.4.17 Ipsoft Inc. (Amelia)

- 6.4.18 Kore.ai Inc.

- 6.4.19 Inbenta Technologies Inc.

- 6.4.20 Creative Virtual Ltd.

- 6.4.21 Serviceaide Inc.

- 6.4.22 Rasa Technologies GmbH

- 6.4.23 SoundHound AI Inc.

- 6.4.24 Tencent Holdings Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment