|

시장보고서

상품코드

1910578

중국의 포장 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

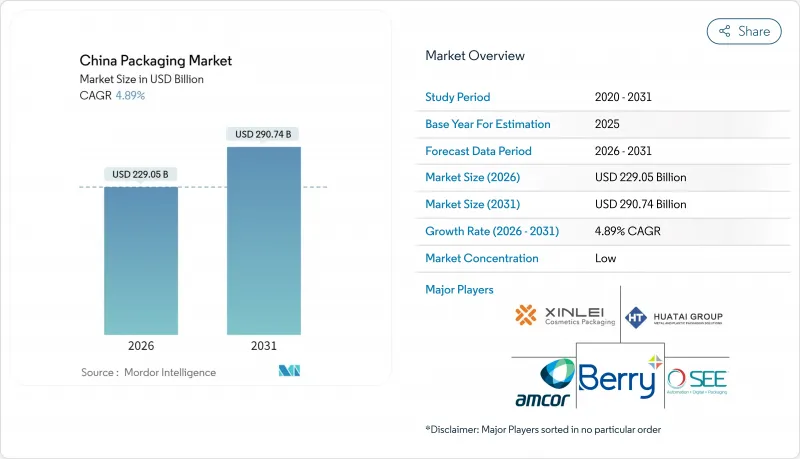

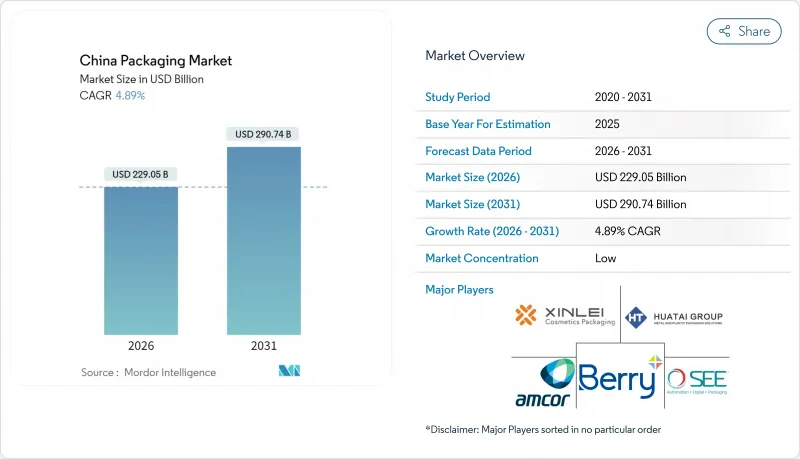

중국의 포장 시장 규모는 2026년 2,290억 5,000만 달러로 추정되며, 2025년 2,183억 7,000만 달러에서 성장을 지속하고 있습니다. 2031년까지 2,907억 4,000만 달러에 달할 것으로 예측되고, 2026년부터 2031년까지 CAGR 4.89%로 확대가 전망되고 있습니다.

세계 최대의 전자상거래 생태계를 배경으로 중국 포장 시장은 계속 확대되고 있습니다. 2024년에는 소포 취급량이 1,750억개에 달하고, 내구성이 뛰어나 자동화 대응 가능한 포장 형태에 대한 수요가 높아지고 있습니다. 또한 의무화된 택배 포장 기준(GB 43352-2023)으로 중국 포장 시장은 저독성 소재와 표준화된 치수로 전환하고 있습니다. 동시에 Nine Dragons Paper 등 국내 대기업 업체와 Amcor 등 세계 기업들은 규모의 경제, 스마트 공장 투자, 바이오 R&D 파이프라인을 활용하여 경쟁력 강화를 도모하고 있습니다. 일회용 플라스틱에 대한 규제 압력과 2025년 PET 음료 용기 회수율 96.48%가 결합되어 재생 소재나 섬유 기반의 포장 형태로의 이행이 가속화되고 있습니다.

중국의 포장 시장 동향과 통찰

전자상거래 소포량의 폭발적 성장

중국의 포장 시장은 소포 취급량과 밀접한 관련이 있으며, 2024년에는 1,750억 개에 달했습니다. 이것에 의해 완충재, 변조 방지 씰, 자동 분류 대응성에 대한 전례가 없는 압력이 높아지고 있습니다. 주요 도시의 풀필먼트 센터에서는 현재, AI 라우팅 시스템을 도입해, 독으로부터 배송처까지의 리드 타임을 35% 단축했습니다. 이로 인해 가공업자는 구조적 강도를 손상시키지 않고 로트 크기를 줄일 수 있습니다. 골판지 가공업자는 물류 플랫폼과 연계한 바코드 및 QR코드에 대응하는 고속 디지털 인쇄 라인에 투자를 진행해, 라스트 마일 추적을 가능하게 하고 있습니다. 모듈식 카톤 설계를 채용하는 시장 진출기업은 공극률을 2자리 삭감했다고 보고하고 있으며, 택배업자가 용적 과금으로 이행하기 때문에, 이것은 최우선 과제가 되고 있습니다. 이러한 진전이 중국 포장 시장의 성장을 뒷받침하는 동시에 데이터 캐리어 기능을 포장 기재에 직접 통합할 수 있는 가공업자에게 이익을 가져오고 있습니다.

지속 가능한 종이 기반 형식에 대한 선호도 증가

중국의 정책 의제는 재활용 가능한 원재료를 선호하고 있으며, 음료, 개인 관리, EC 배송용 봉투 등에서 브랜드 소유자가 섬유 기반 솔루션을 선호하도록 촉구하고 있습니다. 국무원의 환경 배려형 배송 규칙에 따라 소매업체는 매장에서의 회수 시설 제공과 포장 삭감 지표 공개를 의무화하고 있습니다. 컨테이너 보드 공장은 습기 침입을 줄이는 코팅 기술의 혁신에 힘입어 고성능 경량 등급으로 전환하고 있습니다. 생산 능력 확대의 예로는 Anhui Linping을 위한 Valmet의 OptiConcept M 보드 라인이 2025년 말까지 가동 예정(40-6,000만 유로/43-6,400만 달러) 등을 들 수 있습니다. 섬유 기반의 채용은 소비자의 인지도 향상도 뒷받침하고 있어, 전국 조사에서는 68%의 쇼핑객이, 성능이 동등하면 온라인 식료품 배송에 종이 포장을 선호한다고 대답하고 있습니다.

플라스틱 금지 규제 및 확대 생산자책임제도

중국에서는 소매 및 택배 유통에 일회용 플라스틱 제품의 사용 금지 범위가 확대되고 있어 컴플라이언스 비용 증가와 소재 대체 가속을 초래하고 있습니다. EPR(확대생산자책임) 제도에서는 생산자가 재활용시스템의 자금조달을 의무화하고 있으며, 통일적인 시행기준이 부족하여 비용 전가 전략의 책정이 복잡해지고 있습니다. 브랜드 각사는 식품 접촉용 PET 및 PP 포장재에 대한 리사이클 함유율 기준의 동향에 불투명감을 안고 있습니다. 주요 컨버터 기업은 폐쇄 루프 종이 시스템 구축으로 리스크 헤지를 도모하고, 다른 기업은 원료 확보를 위해 폐기물 관리 기업과의 합작 사업을 진행하고 있습니다. 기준이 안정될 때까지 중국 포장 시장에서의 자본 배분은 신규 폴리머 프로젝트보다 기존 설비의 개수에 치우칠 전망입니다.

부문 분석

2025년 종이 및 판지 부문은 중국 포장 시장 점유율의 42.65%를 차지했습니다. 골판지 상자가 EC 물류를 지원하고 섬유 재활용에 대한 소비자 신뢰도가 높은 수준을 유지했기 때문입니다. 이 부문은 PET 음료 병 재활용률 96.48% 달성이라는 중국의 노력에 혜택을 받고 있으며, 이로써 세간의 주목이 셀룰로오스계 순환 시스템으로 이행하고 있습니다. 제지 공장의 개수는 고강도 경량 등급을 지향하고 있으며, 운송업자가 중국 국가 표준 GB 43352-2023의 치수 및 적재 시험을 통과할 수 있게 하고 있습니다. 동시에 수출용 골판지 수요가 2031년까지 연률 5%대 전반에 성장함에 따라 종이 및 판지의 중국 포장 시장 규모도 확대될 것으로 전망됩니다.

기타 소재(바이오 베이스 폴리머, 황마 혼방 필름, 리그닌 복합재)는 저수준이면서 7.09%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장을 기록합니다. 학술적 돌파구에 의해 황마 교배로 24.42%의 섬유 수량 향상이 확인되어 내습성 전분 황마 라이너의 양산화가 가속됐습니다. 리그닌 바이오 나노 복합재는 과자 포장에 적합한 항산화 특성을 가지며 합성 첨가제를 사용하지 않는 능동 포장 수요를 충족합니다. 바이오 폴리머의 비용 경쟁력 확보는 여전히 과제이지만, 주요 FMCG 기업은 EPR 수수료 환급을 계기로 이러한 소재의 실증 시험을 진행하고 있습니다.

주요 포장 형태(판지, 병, 블리스터 팩)는 중국 포장 시장 규모의 69.20%를 차지하며 제품 보호 및 진열 효과에 여전히 중요합니다. 식품 안전 기대와 QR 코드 추적 규칙은 고속 충전 라인과 장식 기술에 대한 지속적인 설비 투자를 보장합니다. 규제환경은 또한 영양보조식품에 대한 변조 방지 씰을 요구하고 다층 라미네이트 수요를 지속하고 있습니다.

3차 포장은 CAGR 5.93%로 확대되고 있습니다. 이는 풀필먼트 센터에서 팔레타이징 자동화와 크로스 보더 EC에 의한 내하중 요구 3배 증가가 배경에 있습니다. 수출 택배업자는 내압성이 있는 RFID 대응 팔레트를 지정하고 있으며, 이들은 창고 관리 시스템에 실시간 데이터를 제공함으로써 매력적인 이익 창출원이 되고 있습니다. 재생 섬유와 바이오 수지를 사용한 복합 팔레트 블록을 제공하는 신규 진출기업은 온라인 소매업체의 리드 타임을 단축하고 중국 포장 시장의 성장 곡선을 강화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전자상거래 소포량의 폭발적 증가

- 지속 가능한 종이 기반 형식에 대한 선호도 증가

- 편의/즉석 식품 포장에 대한 수요

- 의약품 콜드체인 확대

- 스마트 물류(IoT) 대응의 추적 가능 포장

- 초저온 바이오 의약품 포장의 급증

- 시장 성장 억제요인

- 플라스틱 금지 규제 및 확대 생산자 책임 제도

- 펄프 및 폴리머 원료 비용의 변동성

- 지역별 재활용 인프라의 정비 상황에 편차가 발생

- 재사용 가능한 토트백의 시험 도입이 도시의 골판지 수요를 침식

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장에 대한 거시경제 동향의 평가

제5장 시장 규모와 성장 예측

- 포장 재료별

- 플라스틱

- 종이 및 판지

- 유리

- 금속

- 기타 소재

- 포장 유형별

- 1차 포장

- 2차 포장

- 3차 포장

- 포장 형태별

- 경질 포장

- 연질 포장

- 최종 사용 산업별

- 식품 및 음료

- 의료 및 의약품

- 미용 및 퍼스널케어

- 산업용

- 기타 최종 사용 산업

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Nine Dragons Paper(Holdings) Ltd.

- Lee and Man Paper Manufacturing Ltd.

- Shanying International Holdings Co., Ltd.

- Hexing Packaging Co., Ltd.

- Greatview Aseptic Packaging Co., Ltd.

- Wuxi Huatai Co.,Ltd

- Shanghai Zijiang Enterprise Group Co., Ltd.

- YUTO Packaging Technology Co., Ltd.

- Zhejiang Xinlei Packaging Co., Ltd.

- Guangdong Champ New Material Co., Ltd.

- Crown Holdings, Inc.

- Amcor Plc

- Berry Global Group, Inc.

- International Paper Company

- WestRock Company

- Sealed Air Corporation

- Tetra Pak(China) Ltd.

- Beijing Hualian Printing Co., Ltd.

- Zhejiang Jiashan Dingxin Packaging Co., Ltd.

- Shenzhen Yutong Packaging Technology Co., Ltd.

제7장 시장 기회와 미래 전망

SHW 26.01.26The China packaging market size in 2026 is estimated at USD 229.05 billion, growing from 2025 value of USD 218.37 billion with 2031 projections showing USD 290.74 billion, growing at 4.89% CAGR over 2026-2031.

The China packaging market continues to expand on the back of the world's largest e-commerce ecosystem; parcel volumes touched 175 billion units in 2024, intensifying demand for durable, automation-ready pack formats. Mandatory express packaging standards (GB 43352-2023) are also steering the China packaging market toward low-toxicity substrates and standardised dimensions. Concurrently, large domestic producers such as Nine Dragons Paper and global majors like Amcor are leveraging scale, smart-factory investments and bio-based R&D pipelines to strengthen competitive positions. Regulatory pressure on single-use plastics, coupled with a 96.48% PET beverage recovery rate in 2025, is accelerating the shift to recycled and fibre-based formats.

China Packaging Market Trends and Insights

Explosive Growth of E-commerce Parcel Volume

The China packaging market is tightly linked to parcel throughput, which reached 175 billion units in 2024, driving unprecedented pressure on cushioning, tamper-evident seals and automated sorting compatibility. Fulfilment centres in Tier 1 cities now rely on AI routing systems that reduce dock-to-door lead-times by 35%, obliging converters to shorten run lengths without compromising structural integrity. Corrugated converters are investing in high-speed digital print lines that align barcodes and QR codes with logistics platforms, supporting last-mile traceability. Market participants adopting modular carton designs report double-digit reductions in void space, a priority as courier firms pivot toward volumetric pricing. These developments sustain the momentum of the China packaging market while rewarding converters able to integrate data carrier features directly into pack substrates.

Rising Preference for Sustainable Paper-Based Formats

China's policy agenda prioritises recyclable inputs, prompting brand owners to favour fibre-based solutions across beverages, personal care and e-commerce mailers. The State Council's eco-friendly delivery rules oblige retailers to offer in-store take-back facilities and publicly disclose packaging reduction metrics. Containerboard mills are shifting to higher-performance lightweight grades, helped by coating innovations that mitigate moisture ingress. Capacity expansions include Valmet's OptiConcept M board line for Anhui Linping, scheduled online by end-2025 (EUR 40-60 million; USD 43-64 million). Fibre-based adoption also benefits from consumer recognition: nationwide surveys show 68% of shoppers prefer paper wrappers for online grocery deliveries when performance is comparable.

Plastic-Ban and Extended-Producer-Responsibility Rules

China prohibits a widening list of single-use plastics in retail and courier channels, increasing compliance costs and accelerating material substitutions. Producers must finance recycling systems under EPR, and the absence of uniform provincial enforcement complicates cost pass-through strategies. Brands face uncertainty over forthcoming recycled-content thresholds for PET and PP food-contact packs. Leading converters are hedging by building closed-loop paper systems; others form joint ventures with waste-management firms to secure feedstock. Until standards stabilise, capital allocation in the China packaging market skews toward retrofits rather than green-field polymer projects.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Convenience/RTD Food Packs

- Pharmaceutical Cold-Chain Expansion

- Volatile Pulp and Polymer Feedstock Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and Paperboard captured 42.65% of China packaging market share in 2025 as corrugated boxes underpinned e-commerce fulfilment and consumer confidence in fibre recyclability remained high. The segment benefits from China's 96.48% PET beverage recycling milestone that shifts public attention to cellulose-based loops. Mill revamps are oriented toward high-strength light-weight grades, enabling shippers to meet express standard GB 43352-2023 dimensional and stacking tests. Concurrently, the China packaging market size for Paper and Paperboard is expected to rise in tandem with export-oriented corrugated demand growing at a mid-single-digit pace to 2031.

Other Materials-bio-based polymers, jute-blend films and lignin composites-record the fastest 7.09% CAGR, albeit from a low base. Academic breakthroughs reveal jute hybridisation delivering 24.42% fibre-yield gains, accelerating scale-up of moisture-resistant starch-jute liners. Lignin-bionanocomposites imbue antioxidant properties suitable for confectionery wraps, meeting demand for active packaging without synthetic additives. Investment hurdles linger-biopolymer cost parity remains elusive-but leading FMCG firms are piloting such materials, incentivised by EPR fee rebates.

Primary formats-cartons, bottles, blister packs-represent 69.20% of the China packaging market size and remain critical to product protection and shelf appeal. Food-safety expectations and QR-code traceability rules ensure persistent capital expenditure in high-speed filling lines and decoration technologies. The regulatory environment also requires tamper-proof seals for nutraceuticals, sustaining demand for multi-layer laminates.

Tertiary packaging grows at 5.93% CAGR as fulfilment centres automate palletising and cross-border e-commerce triples load-bearing requirements. Export couriers specify crush-proof, RFID-enabled pallets that feed real-time data to warehouse-management systems, creating an attractive profit pool. Market entrants offering composite pallet blocks made with recycled fibre and bio-resins shorten lead times for online retailers and reinforce the growth curve of the China packaging market.

The China Packaging Market Report is Segmented by Packaging Material (Plastic, Paper and Paperboard, Glass, and More), Types of Packaging (Primary Packaging, Secondary Packaging, and Tertiary Packaging), Packaging Format (Rigid Packaging, and Flexible Packaging), End-User Industry (Food and Beverage, Healthcare and Pharmaceutical, Beauty and Personal Care, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Nine Dragons Paper (Holdings) Ltd.

- Lee and Man Paper Manufacturing Ltd.

- Shanying International Holdings Co., Ltd.

- Hexing Packaging Co., Ltd.

- Greatview Aseptic Packaging Co., Ltd.

- Wuxi Huatai Co.,Ltd

- Shanghai Zijiang Enterprise Group Co., Ltd.

- YUTO Packaging Technology Co., Ltd.

- Zhejiang Xinlei Packaging Co., Ltd.

- Guangdong Champ New Material Co., Ltd.

- Crown Holdings, Inc.

- Amcor Plc

- Berry Global Group, Inc.

- International Paper Company

- WestRock Company

- Sealed Air Corporation

- Tetra Pak (China) Ltd.

- Beijing Hualian Printing Co., Ltd.

- Zhejiang Jiashan Dingxin Packaging Co., Ltd.

- Shenzhen Yutong Packaging Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of e-commerce parcel volume

- 4.2.2 Rising preference for sustainable paper-based formats

- 4.2.3 Demand for convenience/RTD food packs

- 4.2.4 Pharmaceutical cold-chain expansion

- 4.2.5 Smart-logistics (IoT) enabled track-and-trace packs

- 4.2.6 Ultra-low-temperature bio-pharma packaging surge

- 4.3 Market Restraints

- 4.3.1 Plastic-ban and extended-producer-responsibility rules

- 4.3.2 Volatile pulp and polymer feedstock costs

- 4.3.3 Patchy provincial recycling infrastructure

- 4.3.4 Reusable tote pilots eroding urban corrugated demand

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Packaging Material

- 5.1.1 Plastic

- 5.1.2 Paper and Paperboard

- 5.1.3 Glass

- 5.1.4 Metal

- 5.1.5 Other Materials

- 5.2 By Types of Packaging

- 5.2.1 Primary Packaging

- 5.2.2 Secondary Packaging

- 5.2.3 Tertiary Packaging

- 5.3 By Packaging Format

- 5.3.1 Rigid Packaging

- 5.3.2 Flexible Packaging

- 5.4 By End-user Industry

- 5.4.1 Food and Beverages

- 5.4.2 Healthcare and Pharmaceutical

- 5.4.3 Beauty and Personal Care

- 5.4.4 Industrial

- 5.4.5 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nine Dragons Paper (Holdings) Ltd.

- 6.4.2 Lee and Man Paper Manufacturing Ltd.

- 6.4.3 Shanying International Holdings Co., Ltd.

- 6.4.4 Hexing Packaging Co., Ltd.

- 6.4.5 Greatview Aseptic Packaging Co., Ltd.

- 6.4.6 Wuxi Huatai Co.,Ltd

- 6.4.7 Shanghai Zijiang Enterprise Group Co., Ltd.

- 6.4.8 YUTO Packaging Technology Co., Ltd.

- 6.4.9 Zhejiang Xinlei Packaging Co., Ltd.

- 6.4.10 Guangdong Champ New Material Co., Ltd.

- 6.4.11 Crown Holdings, Inc.

- 6.4.12 Amcor Plc

- 6.4.13 Berry Global Group, Inc.

- 6.4.14 International Paper Company

- 6.4.15 WestRock Company

- 6.4.16 Sealed Air Corporation

- 6.4.17 Tetra Pak (China) Ltd.

- 6.4.18 Beijing Hualian Printing Co., Ltd.

- 6.4.19 Zhejiang Jiashan Dingxin Packaging Co., Ltd.

- 6.4.20 Shenzhen Yutong Packaging Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment