|

시장보고서

상품코드

1910603

공작기계 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Machine Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

세계의 공작기계 시장 규모는 2026년 1,120억 3,000만 달러로 추정되고 있으며, 2025년 1,084억 7,000만 달러에서 성장이 예상됩니다. 2031년까지 1,316억 3,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 3.28%로 성장할 것으로 전망됩니다.

이 확장은 공급망 재구성, 무역 규칙 엄격화, 반도체 팹에 대한 기록적 투자 등의 배경에서 발생하며, 모두 초정밀 가공 능력을 필요로 합니다. ASML의 고 NA EUV 시스템(1대당 4억 달러 이상)은 차세대 리소그래피 기술이 나노미터 수준의 금속 절삭 및 마무리 성능의 기준을 끌어올리고 있는 좋은 예입니다. 자동차의 전동화와 항공우주 분야의 현대화가 진행되고 있는 가운데, 다축 가공 센터 수요가 높아지고 있어 Industry 4.0 프로젝트에서는 이송 속도나 공구 경로를 자기 최적화하는 AI 탑재 CNC 제어 장치의 채용이 증가하고 있습니다. 지역별 투자 동향에서는 아시아가 신규 생산 능력 증강의 대부분을 차지하고 있지만, 미국의 리쇼어링 우대책이나 유럽의 관세 불투명감에 의해 장래 수요는 보다 분산화된 공장 배치로 이행하고 있습니다. 직접 판매가 여전히 세계 유통 형태의 대부분을 차지하고 있지만, 전자상거래 플랫폼은 중가격대 CNC 모델이나 교환용 공구의 조달 사이클을 가속시키고 있습니다.

세계의 공작기계 시장 동향과 통찰

전기화 급확대가 정밀 e파워트레인 가공을 견인

전기자동차용 모터 공장에서는 공차가 마이크로 레벨로 요구되어 자동화된 고정자 삽입 및 헤어핀 권선 공정과 2차 마무리 공정을 필요로 하지 않는 5축 가공 센터의 조합이 일반적입니다. ZF는 2030년까지 EV 구동계 라인의 자동화율 70%를 목표로 하고 있으며 중국 공급업체는 2034년까지 연간 1억 2,000만대 이상의 전동 모터 생산을 전망하고 있습니다. General Motors와 Mercedes-Benz는 모두 전동 모터 하우징의 생산을 내제화하고 알루미늄 실리콘 합금을 절삭할 때 패스오프 채터링을 발생시키지 않는 기계를 우선하고 있습니다. 미크론 레벨의 형상 오차로 인한 전자기 노이즈를 억제하기 위해 공정 내 측정, 절삭유 관리, 폐루프 보상에 대한 수요가 높아지고 있습니다.

반도체 팹 확장과 관련된 초정밀 장치의 필요성

세계 300mm 팹 투자액은 2027년에 1,370억 달러에 달할 것으로 예측되며, 아메리카에서는 3년간 지출이 두배로 될 전망입니다. ASML의 수톤급 투영 광학계에는 1m의 이동 거리에서 50nm 미만의 형상 오차를 유지하는 다이아몬드 선삭 가공 및 에어 베어링 연삭 시스템이 요구됩니다. TSMC의 1,650억 달러 규모 애리조나 복합시설은 국가 수준의 반도체 프로그램이 조립 공정에서 중량 부품을 주 내에 유보할 수 있는 초정밀 기계 가공 공장의 지역 수요를 창출하는 좋은 예입니다. 클린 룸 대응성, 정압 슬라이드 웨이, 무오염 윤활 방식은 이 틈새 시장에 진입하는 장치 제조업체에 있어 현재는 기본 사양이 되고 있습니다.

고급 CNC 시스템의 고액 설비 투자와 장기 회수 기간

애틀랜타 연은의 조사에 따르면, 제조업체의 80%가 자본 투자 결정 전에 금리를 중시하고 있으며, 이러한 경향은 2025년의 프라임 속도 상승으로 더욱 강해지고 있습니다. 최상위 5축 가공 셀은 설치 비용이 300만 달러를 초과할 수 있으며, 중량 생산의 수주 생산 공장에서는 채산 회수 기간이 5년을 넘을 수 있습니다. 설비의 서비스로서의 계약은 잠정적인 해결책으로 대두되고 있지만, 소프트웨어의 업그레이드에 의해 초기 세대의 컨트롤러가 진부화했을 때의 잔존 가치 리스크에 대해서, 많은 CFO가 여전히 경계감을 안고 있습니다.

부문 분석

다축 부문은 2026년 공작기계 시장 규모의 262억 9,000만 달러를 차지하며, 2031년까지 연평균 복합 성장률(CAGR) 6.88%로 확대될 것으로 전망됩니다. 밀링 머신은 2025년 시점에서 28.05%의 점유율을 유지하는 최대 수익원이지만, 성장은 현재 복잡한 하우징을 단일 클램프로 마무리 가공하는 동시 5축 플랫폼에 집중되어 있습니다. 자동차 제조업체는 내연 기관용 실린더 블록 라인을 전동 구동용 케이싱 셀로 대체할 때 바닥 면적과 핸들링 비용 절감을 위해 다축 가공기를 채용하고 있습니다. 항공우주 제조업체는 고토크 경사 스핀들 가공기를 도입하여 1.2m 길이로 0.015mm의 평면 정밀도를 유지하면서 티타늄 스파를 가공하고 있습니다. 공구실 운영자는 여전히 3축 니 밀링 머신에 의존하고 있지만, 디지털 디스플레이 장치와 프로브 기능을 갖춘 개조 키트를 통해 유지보수 작업에서 경쟁을 유지하고 있습니다.

레이저 절단 시스템 수요는 회복 경향이 있습니다. AI 가이드 파라미터 마법사가 박판 스테인리스의 폐기율을 저감하고 있기 때문입니다. 방전 가공은 밀링 머신에서 경제적으로 가공하기 어려운 미세 코너 반경을 필요로 하는 금형 캐비티 분야에서 틈새를 유지합니다. 지향성 에너지 증착과 마무리 밀링을 결합한 하이브리드 기계는 사이클 타임 단축이 장비 비용을 초과하는 프로토타입 실험실에 도입되고 있습니다. 플라즈마 절단 및 워터젯 절단 플랫폼은 중공업 현장에서 활용되고 있지만, 두 기술 모두 왜곡된 강판에서 절단 품질 유지를 위해 폐루프식 높이 제어의 통합이 시작되고 있습니다.

CNC 플랫폼은 2025년 매출액의 68.55%를 차지했고 CAGR 6.08%로 상승하여 공작기계 시장의 중심적인 지위를 확고히 하고 있습니다. 신흥 컨트롤러는 GPU 가속 알고리즘을 채용해 STEP 파일을 최적화된 공구 경로로 직접 변환합니다. 이렇게 하면 단기 생산 부품의 프로그래밍 시간이 크게 단축됩니다. 중국의 First Automation는 서보 드라이브와 PLC 스택의 국산화를 위해 약 1억 위안을 조달했습니다. 해외 펌웨어 의존 위험을 줄이기 위한 전략적 노력이 두드러집니다. 기존의 수동식 기계는 소규모 공장이나 직업훈련 학교에서 여전히 사용되고 있지만, 신규 도입기는 제어장치 없이 구입하더라도 미래의 개조를 향한 서보 대응 프레임의 동향이 강해지고 있습니다. 하이브리드 적층 및 절삭 복합 시스템은 최첨단 기술로서 레이저 금속 적층과 5축 가공을 조합하여 항공우주용 브라켓에 있어서의 서포트 구조 제거 공정을 생략합니다.

디지털 트윈 기술에 의해 공구의 휨이나 열팽창을 시뮬레이트 가능하게 되어, 프로토타입 단계에서의 충돌을 방지하는 오프 머신 검증을 실현했습니다. ChatCNC(TM) 플러그인은 직육면체 형상을 자동 인식해, 황삭 가공부터 마무리 가공까지의 공정을 자동 생성합니다. 숙련되지 않은 프로그래머도 숙련자 수준의 사이클 타임을 달성할 수 있습니다. 예지 보전 플랫폼은 스핀들 이상을 심각한 고장이 발생하기 전에 감지하며, 운영자 모니터링이 최소한의 무인 운전 환경에서 특히 유용합니다.

본 공작기계 시장 보고서는 제품별(금속절삭공구, 금속성형공구), 기술별(기존 기계, CNC 기계 등), 최종 사용 산업별(자동차, 항공우주 및 방위 등), 판매채널별(직접 판매 등), 지역별(북미, 아시아태평양, 유럽 등)으로 분류되어 있습니다. 이 보고서는 위의 모든 부문에 대해 시장 규모 및 예측(금액 기준, 달러)을 제공합니다.

지역별 분석

전략적 전환 속에서 아시아태평양이 주도적 입장을 유지하는 한편, 북미는 국내 회귀를 진행하고 유럽은 역풍 속에서도 혁신을 추진하고 있습니다. 아시아태평양은 2026년 시점에서 세계 수익의 45.10%를 차지하고 6.05%의 연평균 복합 성장률(CAGR)이 전망되고 있습니다. 이는 각국 정부가 전기자동차(EV), 항공우주, 반도체 산업 클러스터에 대한 우대조치를 집중적으로 실시하고 있기 때문입니다. 중국에서는 미국의 중급기계에 25% 관세 도입을 상쇄하기 위해 소규모 공장에서 하이엔드 CNC 셀 공장으로의 고도화가 진행되고 있습니다. 인도의 생산 연동형 장려 프로그램은 300mm 웨이퍼 공장이나 방위용 기체 제조에 자본을 유도해 정밀 수평 가공기 및 수직 가공 센터의 수주를 창출하고 있습니다. 일본은 수십년에 걸친 모션 컨트롤 기술을 활용해, 복수 시프트 가동 사이클로 서브 미크론의 재현성을 유지하는 초정밀 연삭반을 수출하고 있습니다. 한편, 한국의 가전 대기업은 폴더블 스마트폰의 힌지 플레이트나 카메라 모듈용 가공 능력에 투자를 진행하고 있습니다. 베트남과 태국 등 ASEAN 국가들은 지리적 위험 분산을 중시하는 '중국 플러스 원' 조달 모델을 채용하는 OEM 제조업체로부터 점유율을 획득하고 있습니다.

북미에서는 전략적 제조업의 자립 재건을 목표로 하는 리쇼어링 정책의 혜택을 받고 있습니다. 미국에서는 우주 로켓 구조물용 대형 입형 선반의 생산 능력 증강에 따라 지역 공구 제조업체의 수주가 2001년 이래 최고인 11.9%에 달했습니다. 멕시코의 9.1% 증가는 니어쇼어 자동차 조립이 견인해, 누에보 레온주의 정부 지원 공업 단지에서는 24시간 허가 승인을 실현하고 있습니다. 캐나다는 광업 부문과 저탄소 에너지 프로젝트에서 공작기계 수주를 획득했지만 숙련 노동자 부족으로 인해 전반적인 기세가 억제되고 있으며, 이 제약은 대륙 전체에 공통적입니다.

유럽에서는 전력 비용 상승과 통화 변동에 의한 이익률의 압박에 직면하고 있지만, 고정밀 5축 가공기나 레이저 금속 적층 시스템 분야에서는 압도적인 우위성을 유지하고 있습니다. 독일 제조업체는 국내 수주 침체에 대응하고 애프터 서비스 계약 및 개조 사업(48시간 보증이 포함된 주축 교환 프로그램 포함)에 주력하고 있습니다. TRUMPF는 2025년 5억 3,000만 유로를 연구개발에 투자해 매출이 9% 감소했음에도 불구하고 빔소스 효율에서 우위를 유지했습니다. 북유럽 기업은 신규 기계 출하마다 탄소발자국 증명서를 제공함으로써 지속가능성의 리더십을 강조하고 있으며, 이 대처는 공공 부문 입찰에서 의무화되는 사례가 증가하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전동화의 흐름이 정밀 e파워트레인 가공을 견인

- Industry 4.0의 도입이 스마트 CNC 플랫폼 수요를 촉진

- 경량 합금 및 복합재료 보급에 불가결한 고속 다축 가공 공구

- 반도체 팹 확장에 수반하는 초고정밀 장치의 필요성

- 노후화(20년 이상) 공작기계의 세계적인 갱신 사이클

- 플렉서블 가공에 의한 다품종 소량 생산의 자동화

- 시장 성장 억제요인

- 특수강 및 직동 부품 비용 급등

- 고급 CNC 시스템의 고액 설비 투자와 장기 회수 기간

- 세계의 숙련 CNC 프로그래머 및 오퍼레이터 부족

- 적층 조형 기술로의 자본 전환

- 가치/공급망 분석

- 규제 전망(주요 정부 규제와 시책)

- 기술 개요

- 연결 및 자동화 기계

- 고도 제어 및 모션 시스템

- 디지털화 및 Industry 4.0

- AI에 의한 금속 절삭 정밀도의 향상

- 금속가공업계의 개요

- 지정학이 공작기계 시장에 미치는 영향

- 업계의 매력도 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액, 단위: 10억 달러)

- 제품별

- 금속 절삭 공구

- 밀링 머신

- 굴삭기

- 선반

- 연삭기

- 레이저 절단기

- 방전 가공기(EDM)

- 워터 제트 절단기

- 플라즈마 절단기

- 다축 가공 센터

- 기타(볼링 등)

- 금속 성형 공구

- 프레스(기계식, 유압식, 서보식)

- 단조 기계

- 벤딩 머신

- 기타(전단, 압출, 압연 등)

- 금속 절삭 공구

- 기술별

- 기존 기계(수동 또는 반자동)

- CNC 기계

- 적층 조형/하이브리드 기계

- 최종 사용 산업별

- 자동차

- 항공우주 및 방위

- 전기 및 전자 기기

- 산업기계 및 설비

- 의료기기

- 조선 및 해양

- 정밀 공학

- 에너지 및 전력

- 금속가공(청부공장 등)

- 기타 산업(철도, 기타 일반 제조업 등)

- 판매 채널별

- 직접 판매(OEM에서 최종 사용자로)

- 리셀러 및 도매업체

- 온라인 및 E커머스

- 기타(시스템 인티그레이터, 이벤트 및 전시회, 리빌더 및 재생품 업자 등)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 페루

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 북유럽 국가(덴마크, 핀란드, 아이슬란드, 노르웨이, 스웨덴)

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- ASEAN(인도네시아, 태국, 필리핀, 말레이시아, 베트남)

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 쿠웨이트

- 튀르키예

- 이집트

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Yamazaki Mazak Corporation

- DMG MORI Co. Ltd

- TRUMPF Group

- JTEKT Corporation

- Doosan Machine Tools

- Okuma Corporation

- Makino Milling Machine Co. Ltd

- Haas Automation Inc.

- FANUC Corporation

- Hyundai Wia Corp.

- Schuler AG

- Sandvik AB(Seco & Walter)

- GF Machining Solutions

- Fives Group

- GROB-Werke GmbH & Co. KG

- Hermle AG

- EMAG GmbH & Co. KG

- Hardinge Inc.

- HURCO Companies Inc.

- Amada Co. Ltd

제7장 시장 기회와 미래 전망

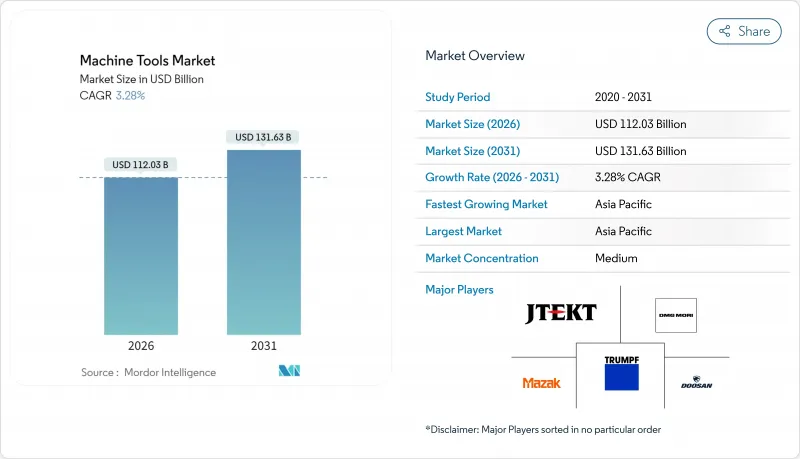

SHW 26.01.26The Machine Tools Market size in 2026 is estimated at USD 112.03 billion, growing from 2025 value of USD 108.47 billion with 2031 projections showing USD 131.63 billion, growing at 3.28% CAGR over 2026-2031.

This expansion occurs against a backdrop of realigned supply chains, stricter trade rules, and record investment in semiconductor fabs, each of which demands ultra-precision machining capacity. ASML's High-NA EUV systems, which cost more than USD 400 million apiece, exemplify how next-generation lithography is lifting the performance bar for nanometer-level metal cutting and finishing . Electrification in automotive and ongoing aerospace modernization are spurring purchases of multi-axis machining centers, while Industry 4.0 projects increasingly bundle AI-enabled CNC controls that self-optimize feed rates and tool paths. Regional investment patterns show Asia drawing the bulk of new capacity additions, yet reshoring incentives in the United States and tariff uncertainty in Europe are tilting future demand toward more diversified plant footprints. Direct sales still dominate the global distribution mix, but e-commerce portals are accelerating procurement cycles for mid-ticket CNC models and replacement tooling.

Global Machine Tools Market Trends and Insights

Electrification Surge Driving Precision e-Powertrain Machining

Electric-vehicle motor plants are pushing tolerances to micro-scale ranges, often pairing automated stator insertion and hairpin winding with five-axis machining centers that eliminate secondary finishing steps. ZF targets 70% automation for EV drive-train lines by 2030, and Chinese suppliers project annual output exceeding 120 million e-motors by 2034. General Motors and Mercedes-Benz have both insourced e-motor housing production, favouring machines that cut aluminum-silicon alloys without creating pass-off chatter. Demand is intensifying for in-process gauging, coolant management, and closed-loop compensation to suppress electromagnetic noise that would otherwise arise from micron-level form errors.

Semiconductor Fab Expansion Necessitating Ultra-Precision Equipment

Global 300 mm fab spending is forecast to hit USD 137 billion in 2027, with the Americas doubling outlays in three years. ASML's multi-ton projection optics require diamond-turning and air-bearing grinding systems that hold sub-50 nm form error over 1 m travel. TSMC's USD 165 billion Arizona complex exemplifies how sovereign chip programs create local pull for ultraprecision machine shops that can keep heavy components in-state during assembly. Clean-room compatibility, hydrostatic slideways, and contamination-free lubrication schemes are now baseline specifications for equipment makers serving this niche.

High Capex & Lengthy Payback for Advanced CNC Systems

Atlanta Fed surveys reveal that 80% of manufacturers weigh interest rates heavily before committing to capital equipment, a dynamic amplified by prime-rate increases in 2025. A top-tier five-axis cell can exceed USD 3 million installed, pushing breakeven past five years for medium-volume job shops. Equipment-as-a-service contracts are emerging as an interim solution, though many CFOs remain wary of residual value risk once software upgrades render early-generation controllers obsolete.

Other drivers and restraints analyzed in the detailed report include:

- Industry 4.0 Adoption Boosting Demand for Smart CNC Platforms

- Lightweight Alloy & Composite Uptake Requiring High-Speed Multi-Axis Tools

- Surging Specialty Steel & Linear-Motion Component Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The multi-axis segment started 2026 commanding USD 26.29 billion of the machine tools market size and is heading toward a 6.88% CAGR to 2031. Milling machines retain the biggest revenue pool with 28.05% share in 2025, yet growth now concentrates on simultaneous five-axis platforms that finish complex housings in one clamp. Automakers replacing ICE cylinder-block lines with e-drive casing cells embrace multi-axis machines to lower floor-space and handling costs. Aerospace primes add high-torque tilt-spindle centres to mill titanium spars while maintaining 0.015 mm flatness over 1.2 m lengths. Toolroom operators still rely on three-axis knee mills, but retrofit kits with digital readouts and probing keep them competitive for maintenance work.

Demand for laser cutting systems is rebounding as AI-guided parameter wizards reduce scrap rates on thin-gauge stainless. Electrical-discharge machining maintains a niche in tool-and-die cavities that require micro-corner radii which mills cannot reach economically. Hybrid machines that mix directed-energy deposition with finish milling are entering prototype labs where cycle-time savings outweigh equipment cost. Plasma and waterjet platforms serve heavy-fabrication yards; however, both are starting to integrate closed-loop height control to maintain cut quality on warped plates.

CNC platforms represented 68.55% revenue in 2025 and will climb at 6.08% CAGR, solidifying their position at the heart of the machine tools market. Emerging controllers employ GPU-accelerated algorithmsthat translate STEP files directly to optimized toolpaths, slashing programming time for short-run parts. China's First Automation secured nearly RMB 100 million to localize servo drives and PLC stacks, highlighting strategic efforts to de-risk foreign firmware dependencies. Conventional manual machines endure in small workshops and vocational schools, yet new builds are trending toward servo-ready frames even when purchased without controls, anticipating future retrofits. Hybrid additive-subtractive systems occupy the cutting edge, combining laser metal deposition with five-axis milling to eliminate support-structure removal steps in aerospace brackets.

Digital twins now simulate tool deflection and thermal drift, allowing off-machine validation that prevents collision during first-article runs. ChatCNC(TM) plug-ins recognise prismatic features and auto-generate rough-to-finish sequences, enabling less-experienced programmers to achieve veteran-level cycle times. Predictive analytics platforms flag spindle anomalies well before catastrophic failure, an especially valuable feature for lights-out processing where operator oversight is minimal.

The Machine Tools Market Report is Segmented by Product (Metal Cutting Tools, Metal Forming Tools), by Technology (Conventional Machines, CNC Machines, and More), by End-User Industry (Automotive, Aerospace & Defense, and More), by Sales Channel (Direct Sales, and More), and by Geography (North America, Asia-Pacific, Europe, and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

Geography Analysis

Asia-Pacific Leads Amid Strategic Shifts, While North America Reshores and Europe Innovates Through Headwinds. Asia-Pacific entered 2026 with 45.10% of global revenue and a 6.05% CAGR outlook as governments funnel incentives into EV, aerospace, and semiconductor clusters. China is upgrading small-batch workshops into high-end CNC cell factories to offset looming 25% U.S. tariffs on mid-range machinery. India's production-linked incentive program is steering capital toward 300 mm wafer fabs and defence airframe work, generating orders for precision horizontals and vertical machining centres. Japan leverages decades of motion-control know-how to export ultra-precision grinders that hold sub-micron repeatability across multi-shift duty cycles, while South Korea's consumer-electronics conglomerates invest in machining capacity for foldable-phone hinge plates and camera modules. ASEAN nations such as Vietnam and Thailand gain share as OEMs adopt a China-plus-one sourcing model that values geographic risk dispersion.

North America benefits from reshoring policies aimed at rebuilding strategic manufacturing self-reliance. United States consumption reached its highest 11.9% share since 2001 as regional tool builders added capacity for large-format vertical lathes used in space-launch structures. Mexico's 9.1% uptick stems from near-shore vehicle assembly, with state-backed industrial parks in Nuevo Leon offering 24-hour permit approvals. Canada draws machine-tool orders from the mining sector and low-carbon energy projects, though overall momentum is tempered by skilled-labour shortages, a constraint echoed across the entire continent.

Europe faces margin erosion from elevated electricity costs and currency volatility, yet it preserves a commanding lead in high-accuracy five-axis and laser-metal-deposition systems. German builders are responding to soft domestic orders by pushing into after-sales contracts and retrofits, including spindle-exchange programmes that guarantee 48-hour turnaround. TRUMPF invested EUR 530 million in R&D during 2025 to maintain its edge in beam-source efficiency despite a 9% revenue dip. Nordic firms highlight sustainability leadership by offering carbon-footprint certificates with each new machine shipment, a feature increasingly mandated in public-sector tenders.

- Yamazaki Mazak Corporation

- DMG MORI Co. Ltd

- TRUMPF Group

- JTEKT Corporation

- Doosan Machine Tools

- Okuma Corporation

- Makino Milling Machine Co. Ltd

- Haas Automation Inc.

- FANUC Corporation

- Hyundai Wia Corp.

- Schuler AG

- Sandvik AB (Seco & Walter)

- GF Machining Solutions

- Fives Group

- GROB-Werke GmbH & Co. KG

- Hermle AG

- EMAG GmbH & Co. KG

- Hardinge Inc.

- HURCO Companies Inc.

- Amada Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification Surge Driving Precision e-Powertrain Machining

- 4.2.2 Industry 4.0 Adoption Boosting Demand for Smart CNC Platforms

- 4.2.3 Lightweight Alloy & Composite Uptake Requiring High-Speed Multi-Axis Tools

- 4.2.4 Semiconductor Fab Expansion Necessitating Ultra-Precision Equipment

- 4.2.5 Global Replacement Cycle of Ageing (>20 yrs) Machine Tool Fleet

- 4.2.6 Automation of High-Mix/Low-Volume Production Via Flexible Machining

- 4.3 Market Restraints

- 4.3.1 Surging Specialty Steel & Linear-Motion Component Costs

- 4.3.2 High Capex & Lengthy Payback for Advanced CNC Systems

- 4.3.3 Worldwide Shortage of Skilled CNC Programmers/Operators

- 4.3.4 Capital Diversion to Additive Manufacturing Technologies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (Key Government Regulations & Initiatives)

- 4.6 Technology Snapshot

- 4.6.1 Connected & Automated Machines

- 4.6.2 Advanced Controls / Motion Systems

- 4.6.3 Digitalisation & Industry 4.0

- 4.6.4 AI-Enhanced Metal Cutting Accuracy

- 4.7 Metalworking Industry Snapshot

- 4.8 Impact of Geopolitics on the Machine Tools Market

- 4.9 Industry Attractiveness - Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Product

- 5.1.1 Metal Cutting Tools

- 5.1.1.1 Milling Machines

- 5.1.1.2 Drilling Machines

- 5.1.1.3 Turning (Lathe) Machines

- 5.1.1.4 Grinding Machines

- 5.1.1.5 Laser Cutting Machines

- 5.1.1.6 Electrical Discharge Machines (EDM)

- 5.1.1.7 Waterjet Cutting Machines

- 5.1.1.8 Plasma Cutting Machines

- 5.1.1.9 Multi-Axis Machining Centres

- 5.1.1.10 Others (Boring, etc.)

- 5.1.2 Metal Forming Tools

- 5.1.2.1 Presses (Mechanical, Hydraulic, Servo)

- 5.1.2.2 Forging Machines

- 5.1.2.3 Bending Machines

- 5.1.2.4 Others (Shearing, Extrusion, Rolling, etc.)

- 5.1.1 Metal Cutting Tools

- 5.2 By Technology

- 5.2.1 Conventional Machines (Manually or Semi-Manually)

- 5.2.2 CNC Machines

- 5.2.3 Additive Manufacturing / Hybrid Machines

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defence

- 5.3.3 Electrical & Electronics

- 5.3.4 Industrial Machinery & Equipment

- 5.3.5 Medical Devices

- 5.3.6 Shipbuilding & Marine

- 5.3.7 Precision Engineering

- 5.3.8 Energy & Power

- 5.3.9 Metal Fabrication (Job Shops, etc.)

- 5.3.10 Other Industries (Railway, Other General Manufacturing, etc.)

- 5.4 By Sales Channel

- 5.4.1 Direct Sales (OEMs to End Users)

- 5.4.2 Dealers & Distributors

- 5.4.3 Online / E-commerce

- 5.4.4 Others (System Integrators, Events & Exhibitions, Rebuilders & Refurbished, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Yamazaki Mazak Corporation

- 6.4.2 DMG MORI Co. Ltd

- 6.4.3 TRUMPF Group

- 6.4.4 JTEKT Corporation

- 6.4.5 Doosan Machine Tools

- 6.4.6 Okuma Corporation

- 6.4.7 Makino Milling Machine Co. Ltd

- 6.4.8 Haas Automation Inc.

- 6.4.9 FANUC Corporation

- 6.4.10 Hyundai Wia Corp.

- 6.4.11 Schuler AG

- 6.4.12 Sandvik AB (Seco & Walter)

- 6.4.13 GF Machining Solutions

- 6.4.14 Fives Group

- 6.4.15 GROB-Werke GmbH & Co. KG

- 6.4.16 Hermle AG

- 6.4.17 EMAG GmbH & Co. KG

- 6.4.18 Hardinge Inc.

- 6.4.19 HURCO Companies Inc.

- 6.4.20 Amada Co. Ltd