|

시장보고서

상품코드

1910618

호스피탈리티 부동산 관리 소프트웨어(PMS) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Hospitality Property Management Software (PMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

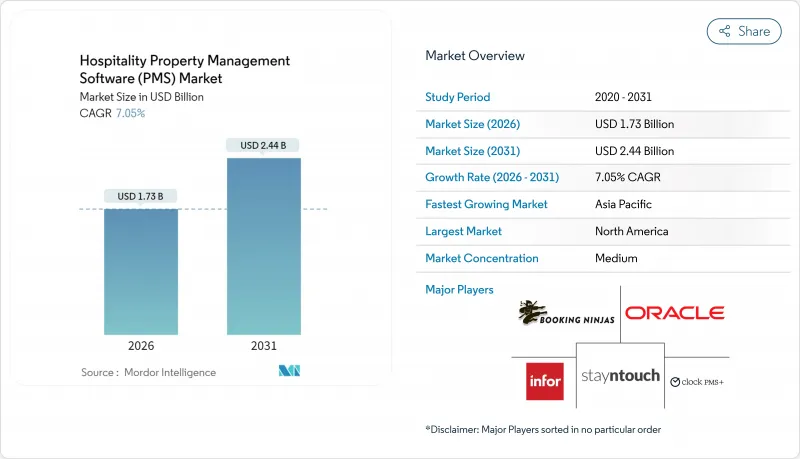

2026년 호스피탈리티 부동산 관리 소프트웨어 시장의 규모는 17억 3,000만 달러로 추정되며, 2025년 16억 2,000만 달러에서 성장하여 2031년에는 24억 4,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지는 CAGR 7.05%로 확대될 것으로 전망됩니다.

레거시 시스템에 대한 업데이트 수요 증가, 클라우드 마이그레이션 가속화, 인공지능을 활용한 수익 툴의 통합이 꾸준한 가치 확대를 지원하고 있습니다. 클라우드 구축은 온프레미스 하드웨어를 제거하여 비용 구조를 계속 재구성하고 있으며, API 퍼스트 아키텍처는 통합 시간을 단축하고 새로운 수익 분배 파트너십의 가능성을 열고 있습니다. 독립형 호텔이나 홈스테이 사업자가 글로벌 체인에 한정된 첨단 모듈을 도입하게 되면서 잠재적인 시장 규모가 확대되고 경쟁이 격화되고 있습니다. 한편, 아시아태평양에서는 지역 특화형 디지털화 프로그램이 전개되어 신흥 시장이 미래의 라이선스 성장에 크게 공헌할 전망입니다. 북미에서는 고급 기능의 도입에 주력하는 경향이 있습니다.

세계의 호스피탈리티 부동산 관리 소프트웨어(PMS) 시장의 동향 및 인사이트

중소규모 시설에서의 도입 확대

소규모 사업자는 구독 가격과 간소화된 배포 프로세스를 통해 현대적인 PMS 솔루션을 업그레이드가 아닌 전략적 필요성으로 파악할 수 있게 되었습니다. 독립형 호텔에서는 채널 관리와 게스트 경험 기능을 통합한 클라우드 기반 PMS 도입 후 두 자릿수의 수익 증가를 보고하고 있습니다. 초기 비용 절감으로 중소기업은 자본을 마케팅 및 서비스 혁신으로 전환하여 브랜드 인지도를 강화할 수 있습니다. 벤더측도 이에 응해, 도입 기간을 수개월에서 수주로 단축하는 셀프 서비스형 도입 마법사를 제공합니다. 그 결과 수천 개의 중소규모 시설에서 기능 도입이 가속화하는 선순환이 발생하여 호스피탈리티 PMS 시장의 확대로 이어지고 있습니다.

온프레미스에서 클라우드 기반 SaaS 모델로 빠르게 전환

클라우드 네이티브 제품군은 하드웨어 업데이트 주기를 필요로 하지 않으며 자동 버전 업데이트를 통해 시설의 보안과 규정 준수를 유지합니다. 시티즌M사의 7,500실 규모 도입 사례에서 알 수 있듯이, 대규모 이행에서도 수주 내로 실현이 가능합니다. 또한 지리적으로 분산된 팀 전체에서 상세한 의사결정을 지원하는 실시간 분석 기능을 제공합니다. 멀티테넌트 아키텍처는 재해 복구 프로토콜을 중앙 집중화하여 감사 부담과 보험료 완화를 실현합니다. 불규정한 설비 투자(CAPEX)에서 정기 구독 요금으로의 전환으로 CFO는 예측 가능성을 확보하고 호스피탈리티 부동산 관리 소프트웨어의 채택을 추진합니다.

레거시 시스템 및 타사 시스템과의 통합 복잡성

많은 전통적인 호텔은 20년 전에 구축된 맞춤형 예약 엔진과 POS 모듈을 지금도 운영하고 있으며 이는 원활한 데이터 교환을 방해하고 있습니다. 커스텀 커넥터는 예산 초과와 공사 연장을 초래할 수 있으며, 명확한 투자 회수가 예상될 수 있음에도 불구하고 업그레이드를 지연시키는 호텔도 존재합니다. 신규 및 기존 시스템을 병렬로 운영하면 교육 수요가 증가하고 운영상의 오류 위험도 높아집니다. 벤더는 로우코드 통합 툴킷의 확장으로 대응하고 있지만, 독자적인 데이터 스키마가 문서화되어 있지 않은 부분에서는 여전히 격차가 남아 있습니다. 레거시 시스템의 도태가 가속화될 때까지, 이러한 마찰은 호스피탈리티 부동산 관리 소프트웨어 시장의 일부 부문에서 단기 성장을 억제할 것입니다.

부문 분석

클라우드 플랫폼은 2025년 시장 가치의 64.92%를 차지하였으며 시설의 확장성과 유지 비용 절감이 우선시되는 가운데 그 우위성을 더욱 확대할 것으로 예측됩니다. 클라우드 도입은 호스피탈리티 부동산 관리 소프트웨어 시장에서 전술한 12.38%의 연평균 복합 성장률(CAGR)을 반영하여 2031년까지 20억 2,000만 달러에 이를 전망입니다. 시설측은 격오지에서도 빠른 응답 시간을 유지하는 세계 컨텐츠 전달 네트워크의 혜택을 이용합니다. 공급업체는 지속적인 기능 업데이트를 구독 계층에 통합하고 인적 개입 없이 보안 패치를 적용합니다. 워크로드를 오프사이트로 마이그레이션하면 여러 시설 간의 통합이 용이해지고 지역 그룹이 통합된 게스트 프로파일을 지원하는 데이터 웨어하우스를 공유할 수 있습니다.

데이터 주권에 관한 엄격한 법률이 시행되고 있는 지역에서는 온프레미스 도입이 계속되고 있지만, 하드웨어의 노후화에 의해 비용 차이는 확대하고 있습니다. 계절 변동 시에는 클라우드의 신축성이 매우 효과적이며, 리조트 시설은 성수기에 인스턴스를 스케일 업하고, 비수기에는 스케일 다운하여 자금을 절약할 수 있습니다. 주요 클라우드 PMS 제품군 주변의 향상된 API 에코시스템은 채팅봇과 IoT 객실 제어 시스템과의 간편한 협력을 가능하게 하여 새로운 서비스 조합을 실현합니다. 궁극적으로 자본 집약도가 낮은 클라우드 경제성은 호스피탈리티 부동산 관리 소프트웨어 시장에서 가장 빠르게 성장하는 채널을 지원합니다.

중소기업은 2025년에 57.05%의 수익을 차지하였고, 호스피탈리티 PMS 시장 내 점유율은 2031년까지 16억 8,000만 달러를 돌파할 전망입니다. 간단한 설치 마법사와 프리미엄 평가판은 사내에 기술 담당자를 보유할 수 없는 사업자의 도입 장벽을 줄여줍니다. 교육 모듈에는 다국어 지원 마이크로 학습 컨텐츠가 포함되어 있어 소규모 호텔에 전형적인 다양한 인재 구성에 적합합니다. 중소기업은 또한 직원이 개인 스마트폰에서 작동할 수 있는 장치 독립 인터페이스를 통해 PC 부족 현상을 피하고 있습니다.

대기업은 독자적인 플랫폼에서 세계 표준으로의 전환에 따라 업그레이드가 완만하지만 꾸준히 진행되고 있습니다. 그러나 복잡한 브랜드 기준은 조달 사이클과 통합 테스트를 장기화할 수 있습니다. 중소기업은 고객 접점 전체에서 데이터를 축적함에 따라 기존에는 체인점에 국한되었던 로열티 플러그인과 타겟형 메일 캠페인을 활용해 민주화를 뒷받침하고 있습니다. 이 변화는 단가가 낮더라도 호스피탈리티 부동산 관리 소프트웨어 시장에 상당한 매출을 제공합니다.

지역별 분석

북미는 오랜 세월에 걸친 벤더 관계, 높은 클라우드 보급률, 성숙한 유통 네트워크를 통해 2025년 시장 가치의 34.20%를 차지했습니다. 호텔 업계는 현재 속성 기반 판매 및 에너지 소비 대시보드와 같은 고급 기능의 활용에 주력하여 이익률의 회복력을 높이고 있습니다. 이 지역의 규제 측면에서의 안정성도 제3자 인증을 가속화하고 신흥 모듈의 시장 출시 기간을 단축하고 있습니다.

아시아태평양은 동남아시아의 중규모 호텔 파이프라인 확대와 정부 주도 디지털화 프로그램에 힘입어 12.18%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 필리핀에 본사를 둔 독립형 호텔에서만 2025년 클라우드 플랫폼의 액티브 사용자를 1만명 이상 증가시켰으며 이는 비약적인 도입 동향을 뒷받침하고 있습니다. 현지 사업자는 온프레미스형을 완전히 회피하고, 모바일 퍼스트 PMS(부동산 관리 시스템)를 도입하는 경우가 많습니다. 이들은 지역에서 널리 사용되는 QR 코드 결제 생태계와 원활하게 작동합니다.

유럽 시장은 여전히 규모가 크고 다양성을 띠고 있으며 ESG 보고서와 데이터 프라이버시 규정이 구매 판단에 영향을 미치고 있습니다. 연결환경이 불안정한 국경을 넘는 스키 리조트와 섬 시장에서는 다중 통화 대응과 강력한 오프라인 접근성이 중요시됩니다. 레거시 인터페이스의 어려움은 남아 있으며 EU의 지속가능성 지침이 업그레이드를 촉진하고 시설은 PMS 워크플로에 통합된 상세한 유틸리티 추적이 필요하기 때문에 호스피탈리티 PMS 시장에서 새로운 기회가 창출되었습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 촉진요인

- 중소규모 시설에서의 도입 확대

- 온프레미스에서 클라우드 기반 SaaS 모델로의 급속한 전환

- OTA 및 메타서치 통합 확대에 의한 통합 재고 추진

- API 퍼스트로 구성 가능한 PMS 아키텍처가 에코시스템 혁신을 실현

- AI 구동형 수익 관리 애드온에 의한 투자 이익률(ROI) 향상

- PMS에서의 이용 데이터 수집을 의무화하는 ESG 보고 요건

- 억제요인

- 레거시 시스템 및 타사 시스템과의 통합 복잡성

- 데이터 보안 및 개인 정보보호 컴플라이언스 비용 증가

- OTA API 요금 체계의 단계적 상승이 총 소유 비용을 증가시킴

- 독립계 호텔에서의 숙련된 IT 인재 부족

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 업계 생태계 분석

- 주요 이용 사례 및 사례 연구

- 거시 경제 동향 평가

- 투자분석

제5장 시장 규모 및 성장 예측

- 전개별

- 온프레미스

- 클라우드

- 부동산 규모별

- 소규모 및 중규모 부동산

- 대규모 부동산

- 물건 유형별

- 호텔 및 리조트

- 모텔 및 롯지

- 홈스테이 숙박시설

- 서비스 아파트

- 기타 물건 유형

- 소유형태별

- 독립 물건

- 가맹 시설

- 기능 모듈별

- 프런트 데스크 업무

- 예약

- 수익 관리

- 채널 관리

- 객실 관리

- 기타 모듈

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 싱가포르

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Oracle Corporation

- Infor, Inc.

- Agilysys, Inc.

- Mews Systems BV

- Planet Payment Group Holdings Limited

- StayNTouch, Inc.

- Cloudbeds, LLC

- Maestro PMS(Northwind Canada Inc.)

- Springer-Miller Systems, LLC

- Guestline Limited

- innRoad, Inc.

- AppFolio, Inc.

- RMS Cloud(RMS(Aust) Pty Ltd)

- Hotelogix(HMS InfoTech Pvt. Ltd.)

- Protel Hotelsoftware GmbH

- RoomKeyPMS(NSightUSA)

- SkyTouch Technology, Inc.

- Sabre Hospitality Solutions, LLC

- Frontdesk Anywhere, Inc.

- Clock Software Ltd.

제7장 시장 기회 및 미래 전망

CSM 26.01.28Hospitality Property Management Software market size in 2026 is estimated at USD 1.73 billion, growing from 2025 value of USD 1.62 billion with 2031 projections showing USD 2.44 billion, growing at 7.05% CAGR over 2026-2031.

Growing replacement of legacy systems, accelerated cloud migration, and the embedding of artificial-intelligence revenue tools underpin this steady value expansion. Cloud deployment continues to reshape cost structures by removing on-premise hardware, while API-first architectures cut integration time and open new revenue-sharing partnerships. Independent hotels and homestay operators now adopt sophisticated modules once limited to global chains, widening the total addressable pool and boosting competitive intensity. Meanwhile, region-specific digitalization programs in Asia-Pacific position emerging markets as outsized contributors to future license growth, even as North America focuses on advanced feature uptake.

Global Hospitality Property Management Software (PMS) Market Trends and Insights

Growing adoption among small- and medium-scale properties

Small operators now view modern PMS solutions as strategic necessities rather than discretionary upgrades, a shift enabled by subscription pricing and simplified onboarding. Independent hotels report double-digit revenue lifts after implementing cloud PMS that bundle channel management and guest-experience functions. Lower upfront cost structures let SMEs redirect capital toward marketing and service innovation, strengthening brand visibility. Vendors reciprocate by releasing self-service implementation wizards that cut deployment time from months to weeks. The result is a virtuous cycle in which feature uptake accelerates across thousands of lower-tier properties, broadening the Hospitality Property Management Software market footprint.

Rapid shift from on-premise to cloud-based SaaS models

Cloud-native suites eliminate hardware refresh cycles and provide automatic version updates that keep properties secure and compliant. Large migrations such as citizenM's 7,500-room rollout demonstrate that even enterprise portfolios can convert in weeks. Real-time access to analytics supports granular decision-making across geographically dispersed teams. Multitenant architectures also centralize disaster-recovery protocols, easing audit burdens and insurance premiums. With recurring subscription fees replacing lumpy capex, CFOs gain predictability, further propelling Hospitality Property Management Software market adoption.

Integration complexity with legacy and third-party systems

Many heritage properties still operate bespoke booking engines and point-of-sale modules built two decades ago, hampering smooth data exchange. Custom connectors frequently exceed budget and extend timelines, prompting some hotels to delay upgrades despite clear ROI. Dual-running old and new stacks inflates training needs and risks operational errors. Vendors respond by expanding low-code integration toolkits, yet gaps persist where proprietary data schemas remain undocumented. Until legacy attrition accelerates, this friction will temper near-term growth in segments of the Hospitality Property Management Software market.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven revenue-management add-ons boosting ROI

- API-first, composable PMS architectures unlocking ecosystem innovation

- Escalating OTA API-fee structure inflating total cost of ownership

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud platforms represented 64.92% of 2025 value and are forecast to widen their lead as properties prioritize scalability and lower upkeep. The Hospitality Property Management Software market size for cloud deployments is on track to reach USD 2.02 billion by 2031, reflecting the 12.38% CAGR cited earlier. Properties benefit from global content-delivery networks that sustain rapid response times, even in remote locations. Vendors bundle continuous feature updates into subscription tiers, pushing security patches without human intervention. Moving workloads off-site also facilitates multi-property consolidation, allowing regional groups to share data warehouses that power uniform guest profiles.

On-premise installations continue in jurisdictions with strict data-sovereignty laws, yet the cost differential widens as hardware ages. Cloud elasticity proves invaluable during seasonal swings, letting resorts scale instances in peak months and downgrade afterward to conserve cash. Enhanced API ecosystems around leading cloud PMS suites enable straightforward integrations with chatbots and IoT room controls, unlocking new service combinations. Ultimately, capital-light cloud economics underpin the fastest expanding channel of the Hospitality Property Management Software market.

SMEs held 57.05% revenue in 2025, and their share of the Hospitality Property Management Software market size is expected to surpass USD 1.68 billion by 2031. Easier set-up wizards and freemium trials lower adoption hurdles for operators lacking in-house technologists. Training modules often include micro-learning content in multiple languages, aligning with the diverse talent pool typical of small hotels. SMEs also value device-agnostic interfaces that staff can run from personal smartphones, circumventing PC shortages.

Large enterprises display slower yet steady upgrades as they phase out proprietary platforms in favor of global standards. However, complex brand standards can prolong procurement cycles and integration testing. As SMEs accumulate data across customer touchpoints, they leverage loyalty plug-ins and targeted email campaigns previously reserved for chains, reinforcing the democratization thesis. This shift contributes substantial volume to the Hospitality Property Management Software market, even if absolute ticket sizes are smaller.

Hospitality PMS Market Report is Segmented by Deployment (On-Premise, and Cloud), Property Size (SMEs and Large Enterprises), Property Type (Hotels and Resorts, and More), Ownership Model (Independent Properties and Chain-Affiliated Properties), Functionality Module (Front Desk and Operations, Booking and Reservations, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 34.20% of 2025 value because of long-standing vendor relationships, high cloud penetration, and mature distribution networks. Hotels now focus on advanced feature utilization, such as attribute-based selling and energy-consumption dashboards, to enhance margin resilience . The region's regulatory stability also speeds third-party certification, shortening time-to-market for emerging modules.

Asia-Pacific is the fastest growing at 12.18% CAGR, propelled by expanding mid-scale hotel pipelines in Southeast Asia and government-funded digital programs. Philippines-based independents alone added more than 10,000 active users to cloud platforms in 2025, validating leapfrog adoption dynamics. Local operators often bypass on-premise entirely, installing mobile-first PMS versions that synchronize seamlessly with QR-code payment ecosystems popular in the region.

Europe remains sizable but heterogeneous, with ESG reporting and data-privacy regulations shaping purchase decisions. Multi-currency support and strong offline access matter in cross-border ski or island markets that experience patchy connectivity. While legacy interface challenges persist, EU sustainability directives are catalyzing upgrades as properties need granular utility tracking embedded in PMS workflows, driving incremental opportunity within the Hospitality Property Management Software market.

- Oracle Corporation

- Infor, Inc.

- Agilysys, Inc.

- Mews Systems B.V.

- Planet Payment Group Holdings Limited

- StayNTouch, Inc.

- Cloudbeds, LLC

- Maestro PMS (Northwind Canada Inc.)

- Springer-Miller Systems, LLC

- Guestline Limited

- innRoad, Inc.

- AppFolio, Inc.

- RMS Cloud (RMS (Aust) Pty Ltd)

- Hotelogix (HMS InfoTech Pvt. Ltd.)

- Protel Hotelsoftware GmbH

- RoomKeyPMS (NSightUSA)

- SkyTouch Technology, Inc.

- Sabre Hospitality Solutions, LLC

- Frontdesk Anywhere, Inc.

- Clock Software Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption among small- and medium-scale properties

- 4.2.2 Rapid shift from on-premise to cloud-based SaaS models

- 4.2.3 Expansion of OTA/meta-search integrations driving unified inventory

- 4.2.4 API-first, composable PMS architectures unlocking ecosystem innovation

- 4.2.5 AI-driven revenue-management add-ons boosting ROI

- 4.2.6 ESG-reporting mandates requiring usage-data capture in PMS

- 4.3 Market Restraints

- 4.3.1 Integration complexity with legacy and third-party systems

- 4.3.2 Heightened data-security / privacy compliance costs

- 4.3.3 Escalating OTA API-fee structure inflating total cost of ownership

- 4.3.4 Shortage of skilled IT talent across independent hotels

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Property Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Property Type

- 5.3.1 Hotels and Resorts

- 5.3.2 Motels and Lodges

- 5.3.3 Homestay Accommodations

- 5.3.4 Serviced Apartments

- 5.3.5 Other Property Types

- 5.4 By Ownership Model

- 5.4.1 Independent Properties

- 5.4.2 Chain-affiliated Properties

- 5.5 By Functionality Module

- 5.5.1 Front Desk and Operations

- 5.5.2 Booking and Reservations

- 5.5.3 Revenue Management

- 5.5.4 Channel Management

- 5.5.5 Housekeeping

- 5.5.6 Other Modules

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Colombia

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 Infor, Inc.

- 6.4.3 Agilysys, Inc.

- 6.4.4 Mews Systems B.V.

- 6.4.5 Planet Payment Group Holdings Limited

- 6.4.6 StayNTouch, Inc.

- 6.4.7 Cloudbeds, LLC

- 6.4.8 Maestro PMS (Northwind Canada Inc.)

- 6.4.9 Springer-Miller Systems, LLC

- 6.4.10 Guestline Limited

- 6.4.11 innRoad, Inc.

- 6.4.12 AppFolio, Inc.

- 6.4.13 RMS Cloud (RMS (Aust) Pty Ltd)

- 6.4.14 Hotelogix (HMS InfoTech Pvt. Ltd.)

- 6.4.15 Protel Hotelsoftware GmbH

- 6.4.16 RoomKeyPMS (NSightUSA)

- 6.4.17 SkyTouch Technology, Inc.

- 6.4.18 Sabre Hospitality Solutions, LLC

- 6.4.19 Frontdesk Anywhere, Inc.

- 6.4.20 Clock Software Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment