|

시장보고서

상품코드

1910659

펩티드 합성 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Peptide Synthesis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

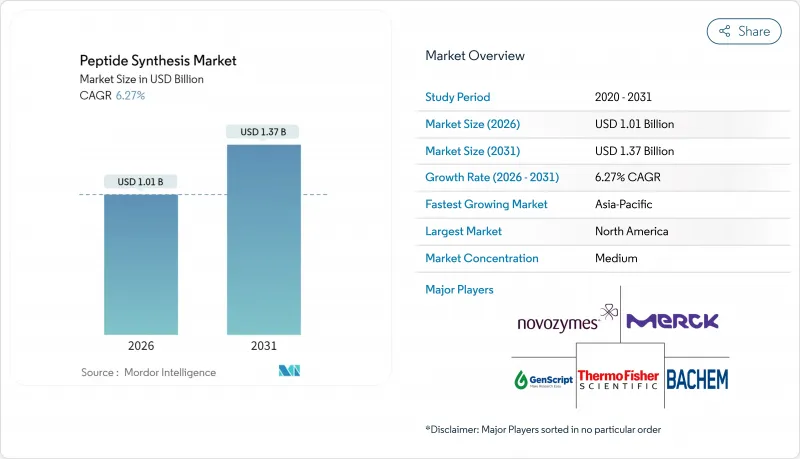

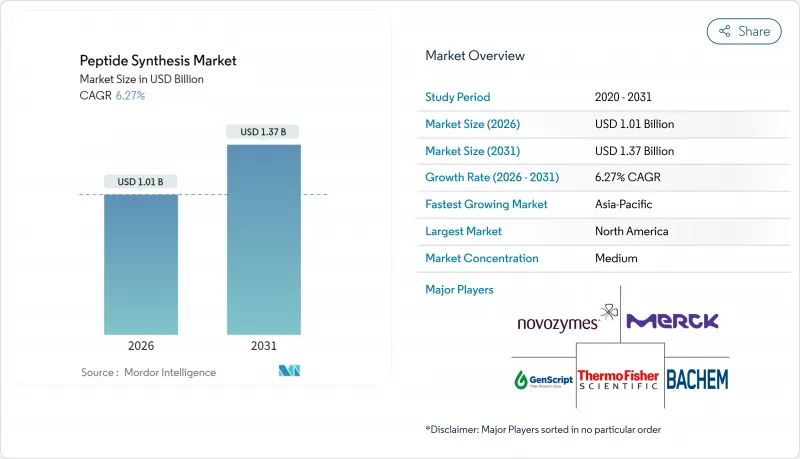

2026년 펩티드 합성 시장 규모는 10억 1,000만 달러로 추정되고 2025년 9억 5,000만 달러에서 성장했으며, 2031년에는 13억 7,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 CAGR은 6.27%를 나타낼 전망입니다.

펩티드계 의약품에 대한 강한 수요, 그 우수한 표적 특이성 및 저분자 화합물에 비해 전신 독성이 낮음이 주요 성장 요인이 되고 있습니다. 마이크로파 보조 고상 펩티드 합성(SPPS) 기술에 의해 반응 시간이 수시간에서 수분으로 단축되는 동시에, 조품 순도가 90% 이상으로 높아져 제조 생산성이 대폭 향상하고 있습니다. 수탁개발제조기관(CDMO)은 대사질환과 종양학 펩티드에 대한 급증하는 주문에 대응하기 위해 많은 투자를 하고 있습니다. CordenPharma사만으로도 GLP-1 생산 능력 확대에 9억 유로를 투자하고 있습니다. 규제 당국은 지속적으로 혁신을 추진하고 있으며, 미국 FDA가 2024년에 4개의 신규 펩티드 치료제를 승인했으며 복잡한 펩티드에 대한 신속한 심사 경로를 유지하고 있다는 증거입니다.

세계의 펩티드 합성 시장 동향과 전망

펩타이드 기반 치료제의 수용 확대

규제 당국은 2024년 기준에서 세계적으로 110건 이상의 펩티드를 승인했으며, 그 임상적 가치를 실증함과 동시에 펩티드 합성 시장을 견인했습니다. 미국 FDA는 2024년에 이메테르스타트와 올레잘센 등 4개의 신규 펩티드 의약품을 승인하여 이 치료법에 대한 신뢰를 보였습니다. 세마글루티드와 틸제파티드와 같은 블록버스터급 GLP-1 수용체 작용제는 유럽과 북미에서 10억 달러를 넘는 CDMO 생산 능력의 증강을 견인했습니다. 종양학 분야도 이에 추종하고 있으며, 177Lu-DOTATATE는 펩티드 약물 복합체가 표적 외작용을 저감하면서 표적 방사선 치료제를 전달하는 좋은 예입니다. 패스트트랙 지정과 유럽의약청(EMA)의 합성 펩티드에 관한 지침에 의해 승인 사이클이 단축되어 연구개발(R&D) 파이프라인이 활성화되고 있습니다. 이러한 요인들이 함께 예측되는 CAGR에 2.1%의 상승효과를 가져올 것으로 추정됩니다.

표적 요법이 필요한 만성 질환 증가

대사성 질환, 암, 신경퇴행성 질환이 세계적으로 증가하고 있으며, 펩티드가 우위성을 발휘하는 정밀의료약 수요가 높아지고 있습니다. 세계의 펩티드 치료제 시장은 2021년 333억 달러에서 2024년 393억 달러로 확대되었으며 만성 질환의 발생률을 반영하여 2030년까지 687억 달러에 이를 것으로 전망됩니다. 현재 150유형 이상의 개발 단계에 있는 펩티드가, 종래 「치료 불가능」으로 여겨진 단백질을 표적으로 하고 있습니다. 환화나 PEG화 등의 화학기술에 의해 반감기가 연장되어 주 1회의 투여가 가능해진 것이 이것을 뒷받침하고 있습니다. 고령화가 진행되는 세계 인구에서 독성이 감소된 프로파일은 노인에서 여러 질병을 앓고 있는 환자에게 적합하기 때문에 필요성이 더욱 높아지고 있습니다. 규제 당국은 펩티드 특화의 품질 프레임워크를 공표하고 있으며, 만성 질환 적응증에 대한 장벽을 저감하고 있습니다. 이러한 시너지 효과는 CAGR에 1.8%의 기여를 예상합니다.

높은 제조 비용과 확장성 문제

SPPS법에서는 펩티드 1kg당 약 1만 3,000kg의 폐기물이 발생합니다. 이것은 저분자 원약의 168-308kg에 비해 방대한 양이며, 용제 처리 비용과 환경 부하를 증가시킵니다. 원재료비는 제품원가의 60-70%를 차지하고 있어 특수아미노산이나 커플링시약은 여전히 고가로 공급불안정입니다. 정제 공정은 총 생산 시간을 3배로 증가시킬 수 있습니다. 분취 HPLC 사이클에서는 대량의 용제를 소비합니다만, 신흥의 멀티 칼럼 그라디언트 기술에 의해 용제 사용량을 50% 삭감할 수 있는 전망입니다. 30개의 아미노산을 초과하는 스케일 업은 커플링 불완전과 서열 결손을 급증시키고 과제를 심각하게 만듭니다. 전용 킬로라보의 설비투자는 5,000만 달러를 넘는 경우가 많아 중소기업의 손익분기점 도달 시기를 늦춥니다. 이러한 과제가 결합되어 CAGR에 -1.2%의 부정적인 영향을 미치고 있습니다.

부문 분석

고상 합성(SPPS)은 성숙한 공정 화학과 광범위한 시약의 가용성으로 2025년 펩티드 합성 시장 점유율의 71.62%를 유지했습니다. SPPS의 펩티드 합성 시장 규모는 제조업체가 낡은 장치를 마이크로파 반응기로 개조함으로써 커플링 효율을 향상시키고 용매 사용량을 삭감하기 위해 2031년까지 연평균 복합 성장률(CAGR) 5.71%로 확대될 것으로 예측되고 있습니다. 자동화 SPPS 라인에서는 현재, 200잔기까지의 서열로 95%의 단계적 수율이 달성되어 cGMP하에서의 Kg 규모 배치 생산이 가능하게 되었습니다. 낮은 제조 비용이 요구되는 단쇄 펩티드에는 액상 합성이 여전히 효과적이지만, 그 점유율은 확대가 아니라 안정합니다. SPPS의 연속유식 적응기술이 상업시험단계에 들어가 더 높은 부피생산성과 80%에 육박하는 용매회수율을 약속하고 있습니다.

무세포 합성 및 효소 합성은 기반 규모가 작은 것, 그린 케미스트리에 대한 요청이 높아지는 가운데 8.40%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있는 기술입니다. 발효 공정을 생략하는 무세포 플랫폼을 확립한 단백질 공학 기업은 리드 타임을 30% 단축하고, 물 사용량을 70% 삭감하고 있습니다. 효소적 리가제 반응은 상온 조건 하에서 거의 완전한 입체선택성을 나타내며, 부산물을 감소시키고 다운스트림 공정의 정제를 용이하게 합니다. 하이브리드 화학효소법에서는 경구 생체이용률을 향상시킨 안정된 래소펩티드가 합성되어 신규 골격구조에 대한 제약업계의 관심을 환기하고 있습니다. ISO 14001 인증이 계약의 전제조건이 되고 있으며, 환경을 배려한 방법이 새로운 아웃소싱 계약을 획득하는 기반을 구축하고 있습니다. 디지털 설계, 흐름 기술, 바이오촉매의 융합은 2030년 이후 SPPS의 이점을 낮출 것으로 예측됩니다.

지역별 분석

2025년 북미는 펩티드 합성 시장의 40.12%를 차지했습니다. 이것은 미국의 깊은 제약 생태계와 복잡한 생물학적 제제의 신속한 검토를 뒷받침하는 규제 자세에 의해 지원되었습니다. 2025년에는 2,000억 달러를 넘는 의약 연구개발비가 이 지역으로 흘러들어 펩티드 모달리티에 대한 배분 비율이 증가했습니다. FDA의 합성 펩타이드에 대한 지침은 심사 대기 기간을 단축하고 중소 혁신 기업이 퍼스트 인 클래스를 신청하는 것을 촉진하고 있습니다. CordenPharma의 콜로라도 주 생산 능력 확장과 Merck사가 Cyprumed사와 체결한 4억 9,300만 달러 규모의 경구 펩티드 라이선싱 계약 등 제제 기술 혁신에 대한 전략적 투자가 주목받고 있습니다. 첨단 제조 기술에 대한 연방 세액 공제도 국내 설비 투자를 더욱 강화하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 비용 경쟁력 있는 CDMO, 확대되는 인재 풀, 지원적인 산업 정책을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 7.54%를 나타낼 것으로 예측됩니다. 중국의 펩티드 CDMO 점유율은 바이오듀로와 아신켐과 같은 기업이 Kg 단위의 생산 능력을 확대하고 FDA 의약품 마스터 파일의 신청 건수를 증가시키고 있기 때문에 2020년 5%에서 2025년까지 9%로 상승했습니다. 한국은 2026년 개업 예정인 SK파마테코의 신시설에 2억 6,000만 달러를 투입해 GLP-1 및 종양 분야에서 지역적인 생산능력 확대를 지지하고 있습니다. 일본에서는 펩티드림사의 노바티스사와의 계약 확대가 나타내는 바와 같이, 창약 플랫폼 분야에서 주도적 입장을 유지하고 있습니다. 국내에서의 비만과 암의 이환율 상승도 대사 펩티드와 방사성 표지 펩티드의 지역 수요를 뒷받침하고 있습니다.

유럽에서는 스위스, 독일, 영국을 중심으로 견조한 생산량을 유지하고 있으며 품질 기준을 조화시키는 EMA의 상세한 펩티드 가이드라인의 혜택을 받고 있습니다. 스위스 단독으로 2024년에 27억 스위스 프랑의 바이오텍 투자를 모아 바켐사와 코덴파마사는 모두 바젤 근교에서 대규모 그린필드 프로젝트를 발표했습니다. 이 지역은 대학과 산업계의 견고한 연계에 힘입어 초기 단계의 혁신을 CDMO 파이프라인에 공급하고 있습니다. EU 그린딜 정책은 효소 합성 및 솔벤트 회수 기술의 채택을 가속화하고 저배출 설비로의 갱신에 대한 보조금을 제공합니다. 공급망의 탄력성 강화 전략은 EU와 북미 공장에서 듀얼 소싱을 촉진하고, 다른 GMP 코드가 존재하더라도 국경을 넘어서는 펩티드 유통을 원활하게 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 펩티드 베이스 치료제의 수용 확대

- 표적 요법을 필요로 하는 만성 질환 증가 경향

- 고상 합성 기술 및 자동화 합성 기술의 진전

- 수탁 개발·제조 서비스의 확대

- 생명 과학 연구에서 정부 및 민간 자금 증가

- 신규 펩티드의 신속 승인을 위한 규제 지원

- 시장 성장 억제요인

- 높은 생산비용과 확장성의 과제

- 엄격한 규제 및 품질 요건

- 전문 원료의 입수 어려움

- 저분자 의약품이나 생물학적 제제 등의 대체 요법과의 경쟁

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- 고상

- 수동 고상 단백질 합성(SPPS)

- 자동화 고상 단백질 합성(SPPS)

- 마이크로웨이브 보조 고상 단백질 합성(SPPS)

- 액상

- 배치 액상 단백질 합성(LPPS)

- 연속 유동 액상 단백질 합성(LPPS)

- 하이브리드 및 재조합

- 무세포 및 효소

- 고상

- 제품 유형별

- 기기

- 펩티드 합성기

- 절단 및 탈보호 시스템

- 정제(플립 HPLC)

- 동결건조기

- 시약 및 소모품

- 아미노산 빌딩 블록

- 수지

- 커플링 시약 및 활성화제

- 용제

- 효소

- 기타 시약 및 소모품

- 서비스

- 맞춤형 및 카탈로그 펩티드 합성

- GMP 펩티드 제조

- 펩티드 라이브러리 설계

- 번역 후 변형 서비스

- 기기

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 펩티드 CDMO 및 CRO

- 학술 및 연구 기관

- 진단 검사 기관

- 식품 및 영양 보조 식품 제조업체

- 화장품 제조업체

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AAPPTec

- AnaSpec

- Bachem Holding AG

- CEM Corporation

- CSBio

- Biosynth(Vivitide)

- Thermo Fisher Scientific Inc.

- GenScript

- JPT Peptide Technologies

- ProteoGenix

- Novozymes A/S(Novonesis)

- Polypeptide Group

- Merck KGaA(Sigma-Aldrich)

- AmbioPharm

- Peptide 2.0

- Lonza

- Almac Sciences

- Pepscan

- Bionova Scientific

- IRIS Biotech

- Senn Chemicals

제7장 시장 기회와 향후 전망

KTH 26.01.22The peptide synthesis market size in 2026 is estimated at USD 1.01 billion, growing from 2025 value of USD 0.95 billion with 2031 projections showing USD 1.37 billion, growing at 6.27% CAGR over 2026-2031.

Strong demand for peptide-based drugs, their superior target specificity, and lower systemic toxicity compared with small molecules are the principal growth engines. Microwave-assisted solid-phase peptide synthesis (SPPS) has compressed reaction times from hours to minutes while lifting crude purities above 90%, sharply improving manufacturing productivity. Contract development and manufacturing organizations (CDMOs) are investing heavily-CordenPharma alone has committed €900 million to expand GLP-1 production capacity-to satisfy surging orders for metabolic and oncology peptides. Regulatory agencies continue to foster innovation, evidenced by the U.S. FDA's approval of four novel peptide therapeutics in 2024 and its maintenance of fast-track pathways for complex peptides.

Global Peptide Synthesis Market Trends and Insights

Increasing Acceptance of Peptide-Based Therapeutics

Regulators have endorsed peptides with over 110 approvals globally as of 2024, validating their clinical value and propelling the peptide synthesis market. The U.S. FDA cleared four new peptide drugs in 2024-such as imetelstat and olezarsen-signaling confidence in the modality. Blockbuster GLP-1 receptor agonists, including semaglutide and tirzepatide, have sparked more than USD 1 billion in CDMO capacity additions across Europe and North America. Oncology is following suit; 177Lu-DOTATATE exemplifies how peptide-drug conjugates deliver targeted radiotherapeutics with fewer off-target effects. Fast-track designations and the EMA's synthetic peptide guidance shorten approval cycles, stimulating R&D pipelines. Collectively, these factors add an estimated +2.1% to the forecast CAGR.

Growing Prevalence of Chronic Diseases Requiring Targeted Therapies

Metabolic disorders, cancer, and neurodegenerative diseases are climbing worldwide, raising demand for precision drugs where peptides excel. The global peptide therapeutics market climbed from USD 33.3 billion in 2021 to USD 39.3 billion in 2024 and is on track to hit USD 68.7 billion by 2030, mirroring chronic-disease incidence. More than 150 investigational peptides now address previously "undruggable" proteins, aided by chemistries such as cyclization and PEGylation that extend half-life and allow once-weekly dosing. An aging global population amplifies the need because reduced toxicity profiles suit older, polymorbid patients. Regulatory bodies are publishing peptide-specific quality frameworks, lowering barriers for chronic-disease indications. The combined effect contributes an estimated +1.8% to CAGR.

High Production Costs and Scalability Challenges

SPPS generates roughly 13,000 kg of waste per kilogram of peptide, compared with 168-308 kg for small-molecule APIs, inflating solvent disposal bills and environmental footprints. Raw materials account for 60-70% of cost of goods, as specialized amino acids and coupling reagents remain expensive and prone to supply disruptions. Purification can triple overall production time; preparative HPLC cycles consume large solvent volumes, though emerging multicolumn gradient technologies promise 50% solvent cuts. Scale-up headaches intensify beyond 30 amino acids, where incomplete couplings and deletion sequences surge. Capital expenditures for dedicated kilo labs often exceed USD 50 million, stretching break-even timelines for smaller firms. Together these issues exert a -1.2% drag on CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Solid-Phase and Automated Synthesis Technologies

- Expansion of Contract Development and Manufacturing Services

- Stringent Regulatory and Quality Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid-phase synthesis retained 71.62% of the peptide synthesis market share in 2025 due to mature process chemistry and broad reagent availability. The peptide synthesis market size for SPPS is projected to advance at 5.71% CAGR through 2031 as manufacturers retrofit older instruments with microwave reactors that lift coupling efficiencies and slash solvent volumes. Automated SPPS lines now achieve 95% stepwise yields for sequences up to 200 residues, enabling kilogram-scale batches under cGMP. Liquid-phase synthesis remains viable for short peptides that demand low cost of goods, yet its share is stable rather than expanding. Continuous-flow adaptations of SPPS are entering commercial trials, promising even higher volumetric productivity and solvent recovery rates approaching 80%.

Cell-free and enzymatic synthesis, though starting from a smaller base, is the fastest-growing technique at an 8.40% CAGR as green-chemistry mandates gain traction. Protein-engineering firms have scaled cell-free platforms that bypass fermentation, trimming lead times by 30% and shrinking water consumption by 70%. Enzymatic ligation offers near-perfect stereoselectivity under ambient conditions, yielding fewer byproducts and easing downstream purification. Hybrid chemo-enzymatic routes have produced stable lasso peptides with improved oral bioavailability, stimulating pharma interest in novel scaffolds. ISO 14001 credentials are becoming contract prerequisites, positioning eco-friendly methods to capture new outsourcing contracts. The convergence of digital design, flow technology, and biocatalysis is expected to erode SPPS dominance beyond 2030.

The Peptide Synthesis Market Report is Segmented by Technique (Solid-Phase, Liquid-Phase, and More), Product Type (Equipment, Reagents & Consumables, and Services), End User (Pharmaceutical & Biotechnology Companies, Peptide CDMOs & CROs, Academic & Research Institutes, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.12% of the peptide synthesis market in 2025, anchored by the United States' deep pharmaceutical ecosystem and a regulatory stance that favors expedited review of complex biologics. More than USD 200 billion in drug R&D spending flowed through the region in 2025, with a growing share earmarked for peptide modalities. The FDA's guidance on synthetic peptides has shortened review queues, encouraging small innovators to file first-in-class applications. Capacity expansions such as CordenPharma's Colorado upgrade and Merck's USD 493 million oral-peptide licensing deal with Cyprumed spotlight strategic bets on formulation innovation. Federal tax credits for advanced manufacturing further bolster domestic capital spending.

Asia-Pacific is the fastest-growing geography, charting a 7.54% CAGR through 2031 on the back of cost-competitive CDMOs, expanding talent pools, and supportive industrial policies. China's peptide CDMO share is projected to rise from 5% in 2020 to 9% by 2025 as firms such as BioDuro and Asymchem scale kilogram capacities and file increasing numbers of FDA drug master files. South Korea is deploying USD 260 million for a new SK pharmteco facility slated to open in 2026, underpinning regional surge in GLP-1 and oncology capacity. Japan maintains a leadership position in discovery platforms, exemplified by PeptiDream's expanded Novartis pact. Rising domestic incidence of obesity and cancer also fuels regional demand for metabolic and radiolabeled peptides.

Europe maintains robust volume behind Switzerland, Germany, and the United Kingdom, benefiting from the EMA's detailed peptide guidance that harmonizes quality expectations. Switzerland alone attracted CHF 2.7 billion of biotech investment in 2024, with Bachem and CordenPharma both announcing large-scale greenfield projects near Basel. The region relies on strong university-industry linkages that feed early-stage innovation into CDMO pipelines. EU Green Deal policies accelerate adoption of enzymatic synthesis and solvent-recovery technologies, providing grants for low-emission equipment upgrades. Supply-chain resilience initiatives encourage dual sourcing across EU and North American plants, smoothing cross-border peptide flows despite variant GMP codes.

- AAPPTec

- AnaSpec

- Bachem Holding

- CEM

- CSBio

- Biosynth (Vivitide)

- Thermo Fisher Scientific

- Genscript

- JPT Peptide Technologies

- ProteoGenix

- Novozymes A/S (Novonesis)

- Polypeptide Group

- Merck

- AmbioPharm

- Peptide 2.0

- Lonza Group

- Almac Sciences

- Pepscan

- Bionova Scientific

- IRIS Biotech

- Senn Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Acceptance of Peptide-Based Therapeutics

- 4.2.2 Growing Prevalence of Chronic Diseases Requiring Targeted Therapies

- 4.2.3 Advancements In Solid-Phase and Automated Synthesis Technologies

- 4.2.4 Expansion of Contract Development and Manufacturing Services

- 4.2.5 Rising Government and Private Funding in Life Sciences Research

- 4.2.6 Regulatory Support for Fast-Track Approval of Novel Peptides

- 4.3 Market Restraints

- 4.3.1 High Production Costs and Scalability Challenges

- 4.3.2 Stringent Regulatory and Quality Requirements

- 4.3.3 Limited Availability of Specialized Raw Materials

- 4.3.4 Competition from Alternative Modalities Such as Small Molecules and Biologics

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technique

- 5.1.1 Solid-phase

- 5.1.1.1 Manual SPPS

- 5.1.1.2 Automated SPPS

- 5.1.1.3 Microwave-assisted SPPS

- 5.1.2 Liquid-phase

- 5.1.2.1 Batch LPPS

- 5.1.2.2 Continuous-flow LPPS

- 5.1.3 Hybrid & Recombinant

- 5.1.4 Cell-free / Enzymatic

- 5.1.1 Solid-phase

- 5.2 By Product Type

- 5.2.1 Equipment

- 5.2.1.1 Peptide Synthesizers

- 5.2.1.2 Cleavage & Deprotection Systems

- 5.2.1.3 Purification (Prep-HPLC)

- 5.2.1.4 Lyophilizers

- 5.2.2 Reagents & Consumables

- 5.2.2.1 Amino-acid Building Blocks

- 5.2.2.2 Resins

- 5.2.2.3 Coupling Reagents & Activators

- 5.2.2.4 Solvents

- 5.2.2.5 Enzymes

- 5.2.2.6 Other Reagents & Consumables

- 5.2.3 Services

- 5.2.3.1 Custom / Catalog Peptide Synthesis

- 5.2.3.2 GMP Peptide Manufacturing

- 5.2.3.3 Peptide Library Design

- 5.2.3.4 Post-translational Modification Services

- 5.2.1 Equipment

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Peptide CDMOs & CROs

- 5.3.3 Academic & Research Institutes

- 5.3.4 Diagnostic Laboratories

- 5.3.5 Food & Nutraceutical Producers

- 5.3.6 Cosmetic Manufacturers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 AAPPTec

- 6.3.2 AnaSpec

- 6.3.3 Bachem Holding AG

- 6.3.4 CEM Corporation

- 6.3.5 CSBio

- 6.3.6 Biosynth (Vivitide)

- 6.3.7 Thermo Fisher Scientific Inc.

- 6.3.8 GenScript

- 6.3.9 JPT Peptide Technologies

- 6.3.10 ProteoGenix

- 6.3.11 Novozymes A/S (Novonesis)

- 6.3.12 Polypeptide Group

- 6.3.13 Merck KGaA (Sigma-Aldrich)

- 6.3.14 AmbioPharm

- 6.3.15 Peptide 2.0

- 6.3.16 Lonza

- 6.3.17 Almac Sciences

- 6.3.18 Pepscan

- 6.3.19 Bionova Scientific

- 6.3.20 IRIS Biotech

- 6.3.21 Senn Chemicals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment