|

시장보고서

상품코드

1910719

북미의 상업용 LED 조명 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2032년)North America Commercial LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2032) |

||||||

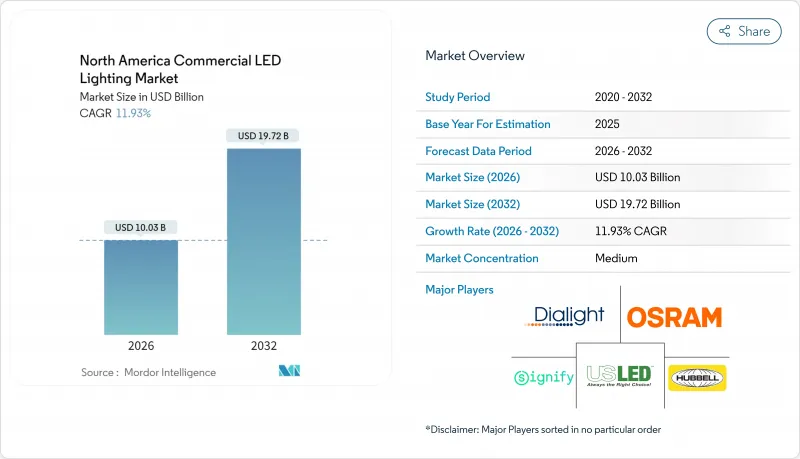

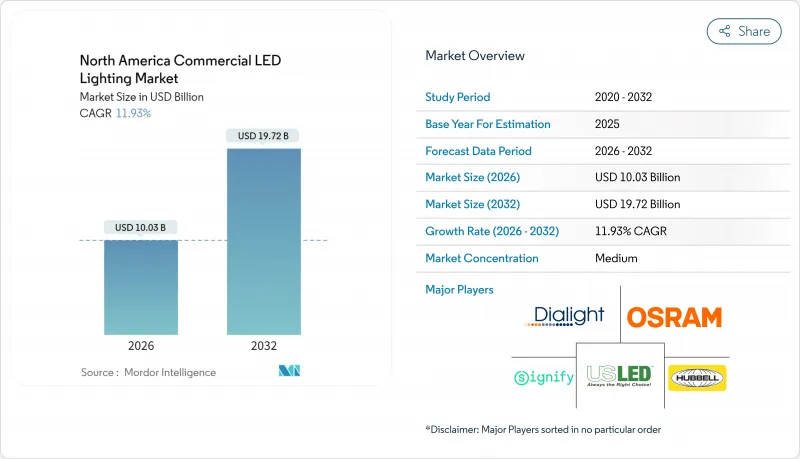

북미의 상업용 LED 조명 시장은 2025년 896만 달러에서 2026년에는 1,003만 달러로 성장해 2026년부터 2032년에 걸쳐 CAGR 11.93%를 나타낼 전망입니다. 2032년까지 1,972만 달러에 달할 것으로 예측되고 있습니다.

북미의 상업용 LED 조명 시장은 순수한 효율성 중심의 업그레이드에서 스마트 빌딩 구상을 따르는 완전 네트워크화 센서 풍부한 시스템으로 이행하고 있습니다. 규제 강화, 특히 2028년 7월 시행되는 미국 에너지성에 의한 120루멘/와트 의무화에 의해 구의 형광등 기술이 도태되는 한편, 기업의 넷 제로 목표가 개수 수요의 지속적인 추진력이 되고 있습니다. 조명기구 전체의 가격 저하로 총소유비용(TCO)의 우위성이 더욱 확대되고, 중규모 시설에서도 광범위한 도입이 경제적으로 실현 가능하게 되었습니다. 동시에 인간 중심의 조명 기능과 IoT 연결성이 에너지 절약 효과를 넘어서는 가치 제안을 강화하고 있습니다. 각 공급업체는 상용 제품의 이익률 압박과 프리미엄 소프트웨어 지원 솔루션의 기회와 균형을 맞추고 경쟁 격화가 진행되고 있습니다.

북미의 상업용 LED 조명 시장 동향과 인사이트

엄격한 에너지 절약 규제와 건축 기준이 시장 변화를 추진

연방 및 주정부 정책은 북미의 상업용 LED 조명 시장 전반에 걸쳐 높은 효율 기준과 고급 제어 요구 사항을 의무화하고 구매 기준을 재구성합니다. 에너지부는 2028년 7월 이후에 판매되는 범용 램프에 대해 최소 120lm/W의 효율을 의무화할 방침이며, 상업용 소켓의 약 절반을 차지하는 콤팩트 형광등의 조기 폐지를 가속시킵니다. 동시에 ASHRAE/IES 90.1-2022는 보다 엄격한 조명 전력 밀도와 자연광 대응 제어를 규정하고 통합 센서를 갖춘 LED 시스템을 우위로 합니다. 캘리포니아 주 Title 24 Part 6은 더욱 적극적인 일정을 추진하고 지역 개보수 활동의 급증을 가져옵니다. 이러한 다층 규제는 진입 장벽을 높이고 적합 제품 포트폴리오와 인증 노하우를 보유한 기존 제조업체들에게 유리하게 작용합니다. 그 결과, 북미의 상업용 LED 조명 시장은 예측 가능한 수요 가시성을 획득하고, 공급업체는 부품 조달을 확대하고 가격을 안정시킬 수 있습니다.

LED 조명 기구의 가격저하와 총소유비용(TCO) 우위성이 상업 분야에서 도입을 가속

LED 패키지와 드라이버의 급속한 비용 압축으로 인해 초기 조명기구 가격이 떨어지고 많은 상업시설 개조 프로젝트에서 2년 미만의 투자 회수 기간을 정당화할 수 있게 되었습니다. 현대적인 트로퍼 설계는 110lm/W의 효율(형광등 기준 대비 40% 향상)을 실현하여 정격 수명을 약 8만 5,000시간으로 연장. 이에 따라 유지 보수 사이클이 비례하여 단축되어 시설 관리자의 운영 경비 절감에 기여하고 있습니다. 고천장 조명의 LED화로 물류센터에서는 50-70%의 에너지 절약 효과를 달성하고 대규모 시설에서는 연간 10만 달러 규모의 광열비 절감을 실현하고 있습니다. 또한 미국 여러 주에서 도입되고 있는 광열비 보조 제도에 의해 자본 비용이 10-15% 삭감되어 자금 조달 판단을 LED 도입으로 확실히 이끌어 냅니다. 이러한 경제적 요인이 합쳐져 예산 제약이 있는 부동산 소유자에게도 투자 회수의 계산이 매력적이 되고 있는 가운데 북미 상업용 LED 조명 시장의 단기적인 성장세를 더욱 강화하고 있습니다.

가격 하락이 공급업체의 이익률을 압박하고 경쟁 압력이 격화

기본 조명기구의 코모디티화가 가격 하락 압력을 가속시켜, 제조업체의 수익성 유지를 곤란하게 하고 있습니다. 시그니파이 등 시장 리더에서 중견 브랜드에 이르기까지 평균 판매 가격 하락에 따라 투자자들이 성장 전망에 의문을 제기하는 동안 주가 변동에 직면하고 있습니다. 액티 브랜즈는 이 동향에 대항해, 인텔리전트 스페이스 솔루션을 우선. 2024 회계연도에 16.7%의 성장을 달성했고 매출이 감소했음에도 불구하고 주당 24.9%의 이익을 올렸습니다. 규모와 전문성이 부족한 중소 제조업체는 합병이나 철수를 검토하고 있어 북미 상업용 LED 조명 시장에서의 통합이 가속하고 있습니다. 관세 불확실성, 특히 멕시코 조립 조명기구에 대한 25% 관세 부과안은 비용 위험을 증가시키고 경계 공급망을 가진 공급업체의 가격 전략을 복잡하게 합니다.

부문 분석

사무실 분야는 2025년 북미 상업용 LED 조명 시장 점유율의 29.65%를 차지했습니다. 이것은 ESG 목표 달성과 직원 체험 향상을 목적으로 한 대규모 기업용 리노베이션이 배경에 있습니다. 오피스에서는 에너지 효율화와 개일 리듬 지원 강화를 위해 인간 중심 설계의 조광 가능 백색 조명기구와 재실 센서의 도입이 증가하고 있습니다. 이러한 고부가가치 요건은 평균 판매가격의 높은 정지를 지원하고, 공급업체 각사는 다른 분야에서의 이익률 저하를 상쇄할 수 있습니다. 동시에 시설 관리자는 HVAC(냉난방 환기) 시스템 및 액세스 제어 시스템과 원활하게 통합되는 네트워크 대응 기구를 선호하고 있으며, 북미의 상업용 LED 조명 시장에서 통합 빌딩 플랫폼으로의 전환을 추진하고 있습니다.

소매 환경은 현재 매출 규모가 작고 2032년까지 연평균 복합 성장률(CAGR) 16.95%로 가장 빠르게 성장하는 부문입니다. 소매업체는 상품의 가시성을 높이고 구매자의 기분을 형성하는 전략적 악센트 조명으로 최대 25%의 매출 향상을 보고합니다. 체인점에서는 브랜드 체험의 갱신에 맞추어 조명을 보다 자주 쇄신하기 위해, 지속적인 수요 사이클이 태어나고 있습니다. 접객, 의료 및 교육 분야는 환자실의 일일 리듬 지원부터 교실의 눈부심 제어 다운라이트에 이르기까지 특별한 요구 사항과 함께 제조업체에게 차별화된 기회를 제공합니다. 산업·창고시설에서는 단기간에 투자 회수가 가능한 하이베이 리노베이션이 도입되고 있지만, 경쟁 구도은 여전히 가격에 민감합니다. 이러한 산업 횡단 기세는 북미 상업용 LED 조명 시장의 확산을 지원하고 단일 섹터 감속으로부터 시장을 보호합니다.

북미의 상업용 LED 조명 시장은 용도별(소매점포, 오피스, 접객, 건축조명, 의료시설 등), 형상별(트로파, 다운라이트, 하이베이, 트럭라이트, 펜던트 조명 등), 유통 채널별(직접 판매, 소매/도매, ESCO/조명 서비스 제공업체, 온라인/이커머스), 지역별로 분류됩니다. 시장 예측은 금액(달러) 기준으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 에너지 절약 규제 및 건축 기준

- LED 조명기구의 가격 저하와 총소유비용(TCO)의 우위성

- 스마트하고 접속 가능한 IoT 대응 조명의 성장

- 인간 중심·건강 중시의 조명으로 이행

- 기업의 넷 제로 및 ESG 목표가 개수를 가속

- 실내 수직 농법 및 마이크로 플루필먼트 허브에서의 수요

- 시장 성장 억제요인

- 가격 하락에 의한 공급업체 이익률의 압박

- 기존 시설에 있어서 개수·설치 비용의 높이

- 중요 부품의 부족(형광체, 드라이버, IC)

- OLED/마이크로 LED 조명 패널과의 경쟁

- 가치/공급망 분석

- 규제 상황

- 기술 전망

제5장 시장 규모와 성장 예측(금액 기준, 2022-2030년)

- 용도별

- 소매점(쇼룸, 쇼핑몰, 점포)

- 사무실

- 접객(레스토랑, 카지노, 호텔)

- 건축(장식용)

- 의료 시설

- 교육 기관

- 산업 및 창고

- 실외 상업용(주차장, 외관)

- 형태별

- 트로퍼

- 다운라이트

- 하이베이

- 트랙 조명

- 펜던트 조명

- 패널 조명

- 선형 스트립

- 기타

- 유통 채널별

- 직접 판매

- 소매 및 도매

- 에너지 서비스 회사(ESCO) 및 조명 서비스 제공업체

- 온라인 및 전자상거래

- 국가별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장 점유율 분석

- 기업 프로파일

- Signify Holding(Philips Lighting & Cooper Lighting)

- Acuity Brands Inc.

- Hubbell Inc.

- Cree Lighting(IDEAL Industries)

- Dialight PLC

- US LED Ltd.

- Osram Licht AG

- Technical Consumer Products Inc.

- Current Lighting Solutions LLC(GE Current)

- Zumtobel Group

- Lutron Electronics Co.

- Legrand SA

- Leviton Manufacturing Co.

- Samsung Electronics America

- LG Innotek USA

- Nichia America Corp.

- Orion Energy Systems Inc.

- Energy Focus Inc.

- Digital Lumens Inc.

- Fagerhult Group(North America)

- Revolution Lighting Technologies

- Cooper Lighting Solutions

제7장 시장 기회와 향후 전망

KTH 26.01.26The North America Commercial LED Lighting market is expected to grow from USD 8.96 million in 2025 to USD 10.03 million in 2026 and is forecast to reach USD 19.72 million by 2032 at 11.93% CAGR over 2026-2032.

The North America Commercial LED Lighting market is transitioning from purely efficiency-driven upgrades toward fully networked, sensor-rich systems that align with smart-building initiatives. Regulatory tightening most notably the Department of Energy's 120 lumens-per-watt mandate effective July 2028 removes legacy fluorescent technologies, while corporate net-zero targets sustain retrofit momentum. Price declines across luminaires deepen the total-cost-of-ownership advantage, making broad adoption economical even for mid-sized facilities. Simultaneously, human-centric lighting features and IoT connectivity strengthen value propositions that go beyond energy savings. Competitive intensity increases as vendors balance margin pressure from commodity products with opportunities in premium, software-enabled solutions.

North America Commercial LED Lighting Market Trends and Insights

Stringent Energy-Efficiency Regulations and Building Codes Drive Market Transformation

Federal and state policies reshape purchasing criteria across the North America Commercial LED Lighting market by enforcing higher efficacy thresholds and advanced control requirements. The Department of Energy will compel all general-service lamps sold after July 2028 to deliver at least 120 lm/W, accelerating retirement of compact fluorescent lamps that still populate nearly half of commercial sockets ASHRAE/IES 90.1-2022 concurrently sets stricter lighting power densities and daylight-responsive controls that favor LED systems with integrated sensors. California's Title 24 Part 6 pushes even more aggressive timelines, creating regional surges in retrofit activity. These layered regulations raise entry barriers, benefiting incumbent manufacturers with compliant product portfolios and certification expertise. Consequently, the North America Commercial LED Lighting market gains predictable demand visibility, allowing vendors to scale component procurement and stabilize pricing.

Declining LED Luminaire Prices and Total-Cost-of-Ownership Advantage Accelerate Commercial Adoption

Rapid cost compression across LED packages and drivers lowers upfront fixture prices, enabling projects to justify payback periods shorter than two years in many commercial retrofits. Contemporary troffer designs deliver 110 lm/W efficacy-40% higher than fluorescent references-while extending rated life to roughly 85,000 hours; maintenance cycles drop proportionally, cutting operating expenses for facility managers . High-bay conversions record energy savings of 50-70% in distribution centers, generating six-figure annual utility reductions in large venues. Utility incentives across multiple U.S. states further shave 10-15% from capital costs, tipping financing decisions decisively toward LED. Together, these economic levers reinforce the North America Commercial LED Lighting market's momentum in the short term as payback math becomes compelling even for budget-constrained property owners

Price Erosion Squeezing Vendor Margins Intensifies Competitive Pressure

Commoditization in basic luminaires fuels downward price pressure, challenging manufacturers to protect profitability. Market leaders such as Signify and mid-tier brands alike witness share price volatility as investors question growth prospects amid falling average selling prices Acuity Brands counters the trend by prioritizing intelligent-spaces solutions, which expanded 16.7% in fiscal 2024 and lifted earnings per share 24.9% despite a topline dip. Smaller manufacturers lacking scale or specialization explore mergers or exit, accelerating consolidation within the North America Commercial LED Lighting market. Tariff uncertainty-especially proposals to levy 25% duties on Mexican-assembled luminaires-adds cost risk, complicating pricing strategies for vendors with cross-border supply chains.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Smart, Connected, and IoT-Enabled Lighting Creates New Value Propositions

- Shift Toward Human-Centric and Wellness-Focused Lighting Drives Premium Segment Growth

- High Retrofit and Installation Costs in Legacy Facilities Limit Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The office category commanded 29.65% of the North America Commercial LED Lighting market share in 2025, underpinned by large-scale corporate retrofits aimed at meeting ESG commitments and boosting employee experience. Offices increasingly deploy human-centric, tunable-white luminaires and occupancy sensors to optimize energy while enhancing circadian support. These premium requirements sustain higher average selling prices, helping vendors offset margin compression elsewhere. Concurrently, facility managers prefer networked fixtures that integrate seamlessly with HVAC and access-control systems, reinforcing the North America Commercial LED Lighting market's shift toward converged building platforms.

Retail environments, while smaller in revenue today, are the fastest-growing segment at a 16.95% CAGR through 2032. Merchandisers cite sales uplifts up to 25% from strategic accent lighting that sharpens product visibility and shapes shopper mood. Store chains also refresh lighting more frequently to align with brand-experience updates, creating recurring demand cycles. Hospitality, healthcare, and education follow with specialized requirements-ranging from circadian support in patient rooms to glare-controlled downlights in classrooms-offering differentiated avenues for manufacturers. Industrial and warehouse settings deploy high-bay retrofits that realize quick paybacks, but the competitive landscape there remains price-sensitive. Collectively, cross-vertical momentum sustains the breadth of the North America Commercial LED Lighting market, protecting it against single-sector slowdowns.

North America Commercial LED Lighting Market is Segmented by Application (Retail Stores, Office, Hospitality, Architectural, Healthcare Facilities, and More), Form Factor (Troffers, Downlights, High-Bay, Track Lights, Suspended Pendants, and More), Distribution Channel (Direct Sales, Retail/Wholesale, ESCO/Lighting-as-a-Service Providers, Online/E-commerce), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Signify Holding (Philips Lighting & Cooper Lighting)

- Acuity Brands Inc.

- Hubbell Inc.

- Cree Lighting (IDEAL Industries)

- Dialight PLC

- US LED Ltd.

- Osram Licht AG

- Technical Consumer Products Inc.

- Current Lighting Solutions LLC (GE Current)

- Zumtobel Group

- Lutron Electronics Co.

- Legrand S.A.

- Leviton Manufacturing Co.

- Samsung Electronics America

- LG Innotek USA

- Nichia America Corp.

- Orion Energy Systems Inc.

- Energy Focus Inc.

- Digital Lumens Inc.

- Fagerhult Group (North America)

- Revolution Lighting Technologies

- Cooper Lighting Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent energy-efficiency regulations and building codes

- 4.2.2 Declining LED luminaire prices and TCO advantage

- 4.2.3 Growth of smart, connected and IoT-enabled lighting

- 4.2.4 Shift toward human-centric and wellness-focused lighting

- 4.2.5 Corporate net-zero and ESG targets accelerating retrofits

- 4.2.6 Demand from indoor vertical farming and micro-fulfilment hubs

- 4.3 Market Restraints

- 4.3.1 Price erosion squeezing vendor margins

- 4.3.2 High retrofit and installation costs in legacy facilities

- 4.3.3 Critical component shortages (phosphors, drivers, ICs)

- 4.3.4 Competition from OLED / micro-LED illumination panels

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

5 MARKET SIZE and GROWTH FORECASTS (VALUE, 2022-2030)

- 5.1 By Application

- 5.1.1 Retail Stores (Showrooms, Malls, Shops)

- 5.1.2 Office

- 5.1.3 Hospitality (Restaurants, Casinos, Hotels)

- 5.1.4 Architectural (Decorative)

- 5.1.5 Healthcare Facilities

- 5.1.6 Educational Institutions

- 5.1.7 Industrial and Warehouse

- 5.1.8 Outdoor Commercial (Parking, Facades)

- 5.2 By Form Factor

- 5.2.1 Troffers

- 5.2.2 Downlights

- 5.2.3 High-Bay

- 5.2.4 Track Lights

- 5.2.5 Suspended Pendants

- 5.2.6 Panel Lights

- 5.2.7 Linear Strips

- 5.2.8 Others

- 5.3 By Distribution Channel

- 5.3.1 Direct Sales

- 5.3.2 Retail / Wholesale

- 5.3.3 ESCO / Lighting-as-a-Service Providers

- 5.3.4 Online / E-commerce

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 Signify Holding (Philips Lighting & Cooper Lighting)

- 6.2.2 Acuity Brands Inc.

- 6.2.3 Hubbell Inc.

- 6.2.4 Cree Lighting (IDEAL Industries)

- 6.2.5 Dialight PLC

- 6.2.6 US LED Ltd.

- 6.2.7 Osram Licht AG

- 6.2.8 Technical Consumer Products Inc.

- 6.2.9 Current Lighting Solutions LLC (GE Current)

- 6.2.10 Zumtobel Group

- 6.2.11 Lutron Electronics Co.

- 6.2.12 Legrand S.A.

- 6.2.13 Leviton Manufacturing Co.

- 6.2.14 Samsung Electronics America

- 6.2.15 LG Innotek USA

- 6.2.16 Nichia America Corp.

- 6.2.17 Orion Energy Systems Inc.

- 6.2.18 Energy Focus Inc.

- 6.2.19 Digital Lumens Inc.

- 6.2.20 Fagerhult Group (North America)

- 6.2.21 Revolution Lighting Technologies

- 6.2.22 Cooper Lighting Solutions

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment