|

시장보고서

상품코드

1910836

선외기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Outboard Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

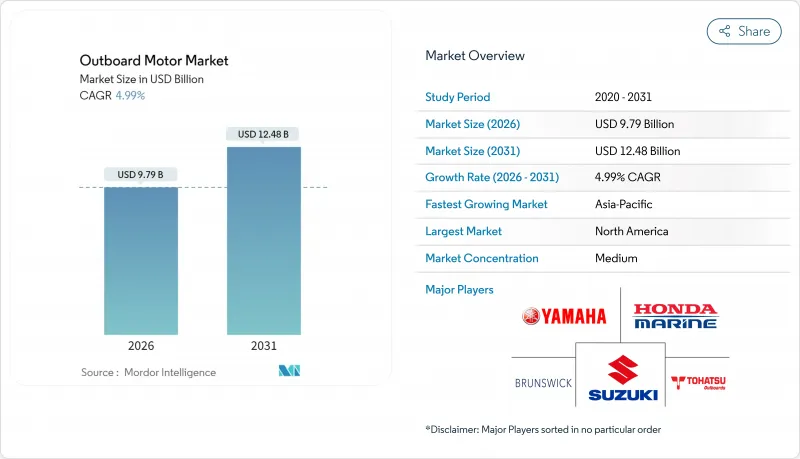

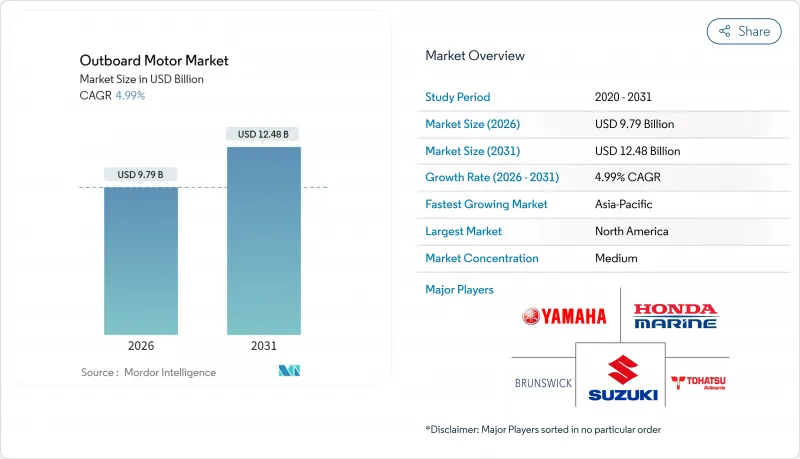

2026년 선외기 시장 규모는 97억 9,000만 달러로 추정되고, 2025년 93억 2,000만 달러에서 성장하며, 2031년에는 124억 8,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년까지의 연평균 성장률(CAGR)은 4.99%를 나타낼 전망입니다.

성장은 팬데믹 후에 처음으로 보트를 구입한 신규 소유자의 기반 확대(현재는 정기적인 교체·업그레이드 사이클을 견인), 고성능 배용 중급 가솔린 모델의 지속적인 인기, 규제 우대 조치나 환경 의식이 높은 소비자를 끌어들이는 클린 추진 기술에 있어서 급속한 혁신에 의해 지지되고 2024년 이후에 실시된 공급망 대책(알루미늄 보트 생산에의 수직 통합이나 전자 부품의 복수 조달 등)에 의해 비용 변동이 서서히 완화되고, 투입 가격이 변동해도 제조업체는 이익률을 유지할 수 있게 되어 있습니다. 한편, 미국 및 유럽연합(EU)의 배출가스 규제 강화는 첨단 4행정과 전동 파워트레인을 유리하게 하고 있으며, 저배기 가스 및 대체 연료 플랫폼에 대한 조사비 지출을 촉진하고 있습니다. 전동전문 제조업체가 종래 내연기관 제조업체가 지배하고 있던 고마력 분야에 진출함에 따라 경쟁 압력은 강해지고, 성능, 가격, 환경 성능에 의해 선외기 시장은 더욱 세분화되고 있습니다.

세계의 선외기 시장 동향과 인사이트

코로나 사후의 새로운 보트 소유 붐

2020년부터 2021년에 처음으로 보트를 구입한 신규 참가자는 엔트리 레벨의 보트에서 고출력 모델로 교체함으로써 선외기 시장에서의 교체 수요를 지지하고 있습니다. 미국의 신규 보트 판매량은 2020년 4월부터 5월에 걸쳐 급증했으며, 소유자 조사에 따르면 이러한 소유자의 대부분은 현재도 보트를 계속 소유하고 있으며, 많은 소유자가 5년 이내에 추진 시스템 업그레이드를 계획하고 있는 것으로 나타났습니다. 제조업체는 이 층을 대상으로 엔진 교환 패키지와 금융 인센티브를 조합한 판매 전략을 전개하고 있어, 소유자가 보다 대형의 엔진, 스마트 제어 시스템, 연비 효율이 높은 기술을 요구해 딜러를 반복해 방문하는 것으로, 평생 고객 가치의 확보를 도모하고 있습니다.

해외 배의 고출력(300 마력 초과) 리파워링

오프쇼어 낚시 애호가나 전세 사업자는 신규 배 구입을 피하면서 자동차 수준의 가속 성능을 얻기 위해 기존 선체에 머큐리 마린의 5.7L V10 벨라드 등 300마력을 넘는 아웃 보드를 3기 또는 4기 탑재하는 케이스가 증가하고 있습니다. 개조 비용은 신규 선체의 5분의 2 이하이면서 동등한 최고 속도 향상을 실현하기 위해 리파워링은 엔진 제조업체에 있어서 고이익률의 성장 분야가 되고 있습니다.

스테이지 V/EPA SI 배출가스 규제 강화

질소산화물(NOx), 일산화탄소(CO), 미립자 물질에 대한 배출 규제가 엄격화됨에 따라 중소 제조업체는 고가의 촉매 후처리 장치에 대한 투자를 촉구하거나 규제 대상 시장에서 철수해야 합니다. 중형 엔진 부문이 가장 영향을 받기 쉽고 소비자가 상당한 가격 상승을 기피하기 때문에 규제 대응 솔루션이 비용 중립이 될 때까지 판매 수량 증가가 둔화되는 경향이 있습니다.

부문 분석

2025년 가솔린 선외기는 시장 점유율의 80.74%를 차지하며 선외기 시장 규모에서 가장 큰 단일 수익원이 되었습니다. 현재 4스트로크 설계는 300마력 이상의 출력대에 도달하고, 보다 슬림한 기어 케이스와 디지털 전환 시스템에 의해 EPA 스테이지 III 규제를 충족하는 것으로, 해안 낚시 애호가나 고성능 크루저 유저로부터의 지지를 유지하고 있습니다. 제조업체는 애프터마켓용 프로펠러 키트나 조이스틱 제어장치를 크로스 프로모션 해, 라이프 사이클 가치를 높이는 것과 동시에, 에너지 전환기에서도 내연 기관의 중요성을 유지하고 있습니다.

전기 추진 시스템은 미국 동서 양해안의 항만 선박 규제 및 탄소 신용 대출 프로그램에 밀려 5.02%의 연평균 복합 성장률(CAGR)로 전력 성장의 최고를 달리고 있습니다. 토르키드사의 50kW 「Deep Blue」나 야마하의 48V 「HARMO」플랫폼은 엄격한 소음·배출 규제를 가지는 정박지에서 정숙성과 순시 토크 성능이 어떻게 평가되는지를 나타내고 있습니다. 배터리 교체 스테이션과 플로팅 태양광 충전 폰툰은 임대선대의 항속거리 불안을 줄여줍니다. 이는 코치 보트나 단거리 수상 택시와 같은 명확한 가동 사이클을 가진 선박이 운영상의 제약 없이 완전 전동화될 수 있음을 입증합니다.

레크리에이션 보트 시장은 2020년 록다운 기간 동안 신정 판매가 급증한 결과 2025년에는 선외기 시장 규모의 75.68%를 차지했습니다. OEM 제조업체는 원활한 사용자 경험을 중시하는 라이프 스타일 지향 구매자를 위해 컬러 매칭 카울링, 터치 스크린 식 조타실 디스플레이, 플러그 앤 플레이 지원 모바일 앱을 번들 판매합니다. 구독 유지 보수 계획 및 연장 보증으로 레크리에이션 소유자는 딜러가 예측 가능한 수익원으로 전환합니다.

순찰, 어업, 전세 및 양식업을 포함한 상용선대는 5.16%의 연평균 복합 성장률(CAGR)로 더욱 빠르게 확대되고 있습니다. 총 소유 비용의 관점에서 연료 효율이 뛰어난 4 스트로크 엔진과 다운 타임을 최소화하는 디젤 모델이 선택되었습니다. 정부는 경기자극책 예산을 활용하여 법집행정의 근대화를 추진하고 있습니다. 한편 대규모 양식장에서는 지속가능성 목표 달성을 위해 보조정의 전동화를 추진하고 있습니다. 그 결과, 상용채널의 단가는 레저 평균의 1.25배에 이르며, 판매량이 감소하더라도 매출의 성장을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 시점에서 선외기 시장의 38.32%를 차지하고 미국의 다수의 등록 선박과 이용률을 높이는 성숙한 마리나 네트워크가 기반이 되었습니다. EPA의 대기 오염 규제에 의해 기화기식 2 스트로크기의 급속한 갱신이 진행되고, 플로리다주, 캘리포니아주, 미네소타주의 소음 규제가 4 스트로크기의 보급을 가속시키고 있습니다. 딜러의 통합으로 모든 출력 클래스의 제품을 재고할 수 있는 지역 슈퍼 스토어가 탄생하여 여름 시즌의 다운타임을 최소화하는 이동식 서비스 유닛을 제공할 수 있게 되었습니다.

아시아태평양은 2031년까지 5.13%라는 최고 지역 CAGR을 나타낼 전망입니다. 중국, 인도, 태국, 인도네시아에서 중산계급의 가처분소득 증가가 견인역이 됩니다. 베트남과 필리핀 정부는 새로운 해안 배출 규제에 대응하기 위해 내구성이 뛰어난 중형 4 스트로크 엔진으로 전통적인 어선단을 근대화하고 있으며, 이것이 대규모 갱신 사이클을 창출하고 있습니다. 중국 국내 제조업체는 소형 휴대용 전기 기기를 공급하고 있지만, 100마력 이상의 분야에서는 성능 평가의 높이로부터, 수입된 일본 및 미국 브랜드가 시장을 독점하고 있습니다.

유럽은 여전히 규제 주도의 고부가가치 시장이며, 스테이지 V 배출 규제에 의해 이미 대부분의 내륙 수로에서 구식 2 스트로크 엔진은 배제되고 있습니다. 스칸디나비아의 호수지대에서는 HVO 연료 급유 독의 시험 도입이 진행되어 기존의 4 스트로크 선대의 CO2 배출량을 최대 80% 삭감 가능하게 되었습니다. 한편, 암스테르담이나 베니스 운하에서는 제로 방출 규제가 시행되어 림 구동식 전동 모터가 권장되고 있습니다. 남유럽 전세 업계는 유행 이후 급회복하고 150-200마력의 조이스틱 제어식 트윈 선외기로 선대를 갱신하고 있기 때문에 지역 전체의 단가가 상승하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- COVID-19 후의 최초의 보트 소유에 있어서 장기적인 붐

- 고마력(300마력을 넘는) 오프쇼어정의 엔진 교환 수요의 급증

- 규제 전환 : 4행정 효율화로의 전환

- 상업 순찰기관이 저황 디젤 선외기로 이행

- 카본 크레디트 자금에 의한 코치정 및 안전용 딩기의 전동화

- 지속 가능한 드롭 인형 선박 연료의 파일럿 도입

- 시장 성장 억제요인

- 스테이지 V/EPA Si 배출규제의 단계적 강화

- 중급 유닛용 알루미늄 및 전자 부품공급망 변동성

- 레어 어스 의존에 의한 전동 선외기 부품 비용의 상승

- 딜러 네트워크의 통합이 지방 서비스에 대한 액세스를 제한

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자·소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액(달러) 및 수량(단위))

- 전원별

- 가솔린

- 디젤

- 전기

- 하이브리드, 프로판 및 LPG

- 용도별

- 레저용

- 상업용

- 추력 등급별

- 휴대용

- 중형

- 고출력

- 마력 범위별

- 30마력 미만

- 30-99마력

- 100-199마력

- 200-299마력

- 300마력 이상

- 최종 사용자별

- OEM 보트 제조사

- 애프터마켓 및 리파워링

- 판매 채널별

- 직접 해양 딜러

- 온라인 전용 업체

- 보트 OEM 통합업체

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 멕시코

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Brunswick Corp.(Mercury Marine)

- Yamaha Motor Co. Ltd

- Suzuki Motor Corp.

- Honda Motor Co. Ltd

- Tohatsu Corp.

- Cox Marine

- OXE Marine AB

- Vision Marine Technologies

- Torqeedo GmbH

- Minn Kota(MotorGuide)

- DEUTZ AG

- Hidea Power Machinery

- Parsun Power Machine Co. Ltd

- Selva SpA

- LEHR LLC

- Pure Watercraft

- AB Volvo

- GARMIN-Navico Group

제7장 시장 기회와 향후 전망

KTH 26.01.26Outboard Motor Market size in 2026 is estimated at USD 9.79 billion, growing from 2025 value of USD 9.32 billion with 2031 projections showing USD 12.48 billion, growing at 4.99% CAGR over 2026-2031.

Growth is sustained by an enlarged base of post-pandemic first-time boat owners who now drive recurring replacement and upgrade cycles, the enduring popularity of mid-range gasoline models for performance craft, and rapid innovation in clean-propulsion alternatives that attract regulatory incentives and eco-conscious consumers. Supply-chain measures undertaken since 2024-such as vertical integration into aluminum boat production and multisourcing of electronics-are gradually easing cost volatility, enabling manufacturers to protect margins even as input prices fluctuate. Meanwhile, tightening emissions standards in the United States and the European Union favor advanced four-stroke and electric powertrains, pushing research spending toward low-emission and alternative-fuel platforms. Competitive pressure intensifies as electric specialists expand into higher-horsepower brackets once dominated by internal-combustion incumbents, further segmenting the outboard motors market by performance, price, and environmental profile.

Global Outboard Motor Market Trends and Insights

Boom in post-COVID first-time boat ownership

New entrants who bought their first boats in 2020-2021 continue to underpin replacement demand within the outboard motors market as they trade up from entry-level craft to higher-horsepower models. U.S. monthly new-boat sales jumped exponentially from April to May 2020, and retention surveys show that most of these owners remain active, with many planning propulsion upgrades within five years. Manufacturers target this cohort with bundled re-power packages and financing incentives, locking in lifetime customer value as owners repeatedly revisit dealerships for bigger engines, smart controls, and fuel-efficient technologies.

High-horsepower (>300 hp) re-powering of offshore craft

Offshore anglers and charter operators increasingly install triple or quad 300-plus-hp outboards-such as Mercury Marine's 5.7 L V10 Verado-on existing hulls to achieve automobile-like acceleration without purchasing new boats. Retrofits often cost two-fifth less than a new hull yet deliver comparable top-speed gains, making re-powering a high-margin growth pocket for engine makers.

Tightening Stage V / EPA SI emissions limits

Stricter caps on NOx, CO, and fine particulates mean small manufacturers must invest in costly catalytic after-treatment or exit regulated markets. Mid-range engine brackets are most exposed because consumers resist significant price increases, eroding volume growth until compliance solutions become cost-neutral.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory shift toward four-stroke efficiency

- Commercial patrol agencies are adopting low-sulfur diesel outboards

- Volatility in aluminum & electronics supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gasoline outboards represented 80.74% of the outboard motors market share in 2025, translating into the largest single revenue pool within the outboard motors market size. Four-stroke designs now reach 300-plus hp brackets with slimmer gearcases and digital-shift systems that meet EPA Stage III limits, sustaining loyalty among offshore anglers and performance cruisers. Manufacturers cross-promote aftermarket propeller kits and joystick controls to lift lifecycle value and keep internal-combustion engines relevant during the energy transition.

Electric propulsion is pacing the power-source growth leaderboard at 5.02% CAGR, propelled by harbor-craft mandates and carbon-credit financing programs on both coasts of the United States. Torqeedo's 50 kW Deep Blue and Yamaha's 48 V HARMO platform illustrate how quiet, instant-torque solutions win over marinas with strict noise and emission bylaws. Battery swap stations and floating solar charging pontoons reduce range anxiety for rental fleets. This demonstrates that well-defined duty cycles like coach boats and short-haul water taxis can go fully electric without operational penalties.

Recreational boating consumed 75.68% of the outboard motors market size in 2025 after new-boat sales spiked during the 2020 lockdowns. OEMs bundle color-matched cowlings, touchscreen helm displays, and plug-and-play mobile apps to upsell lifestyle buyers who value seamless user experiences. Subscription-based maintenance plans and extended warranties convert recreational owners into predictable annuity streams for dealers.

Commercial fleets, including patrol, fishing, charter, and aquaculture, are expanding faster at a 5.16% CAGR. Their total-cost-of-ownership equations favor fuel-sipping four-strokes and diesel models that minimize downtime. Governments tap stimulus budgets to modernize enforcement craft, while large-scale fish farms electrify auxiliary tenders to meet sustainability targets. As a result, per-unit ASPs in commercial channels run one-fourth above the recreational average, powering top-line growth even at lower volumes.

The Outboard Motor Market Report is Segmented by Power Source (Gasoline, Diesel, and More), Application Type (Recreational and Commercial), Thrust Class (Portable, Mid-Range, and High-Power), Horse-Power Range (Less Than 30 HP and More), End-User (OEM Boat Builders and After-Market/Re-Power), Sales Channel (Direct Marine Dealer and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America held 38.32% of the outboard motors market share in 2025, anchored by the United States' multiple registered boats and a mature marina network that promoted high utilization. EPA clean-air regulations prompt rapid turnover of carbureted two-strokes, and state noise rules in Florida, California, and Minnesota accelerate four-stroke adoption. Dealer consolidation yields regional super-stores capable of stocking every power class and offering mobile service units that keep downtime low during peak summer months.

Asia-Pacific is set to record the highest regional CAGR at 5.13% through 2031, propelled by rising middle-class disposable income in China, India, Thailand, and Indonesia. Governments in Vietnam and the Philippines are modernizing artisanal fishing fleets with durable mid-range four-strokes to comply with new coastal-emission codes, creating sizeable replacement cycles. Domestic manufacturers in China supply more minor portable electrics, yet imported Japanese and American brands dominate 100-plus-hp brackets due to performance reputation.

Europe remains a high-value, regulation-led arena where Stage V emissions have already eliminated legacy two-strokes on most inland waterways. Scandinavian lake districts are pilot zones for HVO fueling docks that let existing four-stroke fleets cut CO2 output by up to four-fifth. At the same time, Amsterdam and Venice canals enforce zero-emission mandates favoring rim-drive electric motors. Southern Europe's charter sector rebounds strongly post-pandemic, renewing fleets with joystick-controlled twin outboards rated 150-200 hp, lifting unit ASPs across the region.

- Brunswick Corp. (Mercury Marine)

- Yamaha Motor Co. Ltd

- Suzuki Motor Corp.

- Honda Motor Co. Ltd

- Tohatsu Corp.

- Cox Marine

- OXE Marine AB

- Vision Marine Technologies

- Torqeedo GmbH

- Minn Kota (MotorGuide)

- DEUTZ AG

- Hidea Power Machinery

- Parsun Power Machine Co. Ltd

- Selva SpA

- LEHR LLC

- Pure Watercraft

- AB Volvo

- GARMIN - Navico Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Prolonged Boom In First-Time Boat Ownership Post-Covid-19

- 4.2.2 Surge In High-Horse-Power (More than 300 Hp) Re-Powering Of Offshore Craft

- 4.2.3 Regulatory Pivot Toward Four-Stroke Efficiency

- 4.2.4 Commercial Patrol Agencies Shifting To Low-Sulfur Diesel Outboards

- 4.2.5 Carbon-Credit-Funded Electrification Of Coach & Safety Dinghies

- 4.2.6 Pilot Roll-Out Of Sustainable Drop-In Marine Fuels

- 4.3 Market Restraints

- 4.3.1 Progressive Tightening Of Stage V / Epa Si Emission Limits

- 4.3.2 Supply-Chain Volatility In Aluminium & Electronics For Mid-Range Units

- 4.3.3 Rare-Earth Dependency Raising E-Outboard Motor Bom Costs

- 4.3.4 Dealer-Network Consolidation Limiting Rural Service Accessibility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Power Source

- 5.1.1 Gasoline

- 5.1.2 Diesel

- 5.1.3 Electric

- 5.1.4 Hybrid / Propane / LPG

- 5.2 By Application Type

- 5.2.1 Recreational

- 5.2.2 Commercial

- 5.3 By Thrust Class

- 5.3.1 Portable

- 5.3.2 Mid-range

- 5.3.3 High-power

- 5.4 By Horse-Power Range

- 5.4.1 Less than 30 hp

- 5.4.2 30-99 hp

- 5.4.3 100-199 hp

- 5.4.4 200-299 hp

- 5.4.5 More than or equal to 300 hp

- 5.5 By End-User

- 5.5.1 OEM Boat Builders

- 5.5.2 After-Market / Re-Power

- 5.6 By Sales Channel

- 5.6.1 Direct Marine Dealer

- 5.6.2 Online Pure-Play

- 5.6.3 Boat-OEM Integrated

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Mexico

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia and New Zealand

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle-East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle-East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Brunswick Corp. (Mercury Marine)

- 6.3.2 Yamaha Motor Co. Ltd

- 6.3.3 Suzuki Motor Corp.

- 6.3.4 Honda Motor Co. Ltd

- 6.3.5 Tohatsu Corp.

- 6.3.6 Cox Marine

- 6.3.7 OXE Marine AB

- 6.3.8 Vision Marine Technologies

- 6.3.9 Torqeedo GmbH

- 6.3.10 Minn Kota (MotorGuide)

- 6.3.11 DEUTZ AG

- 6.3.12 Hidea Power Machinery

- 6.3.13 Parsun Power Machine Co. Ltd

- 6.3.14 Selva SpA

- 6.3.15 LEHR LLC

- 6.3.16 Pure Watercraft

- 6.3.17 AB Volvo

- 6.3.18 GARMIN - Navico Group