|

시장보고서

상품코드

1910846

제약용 유리 바이알 및 앰풀 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pharmaceutical Glass Vials And Ampoules - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

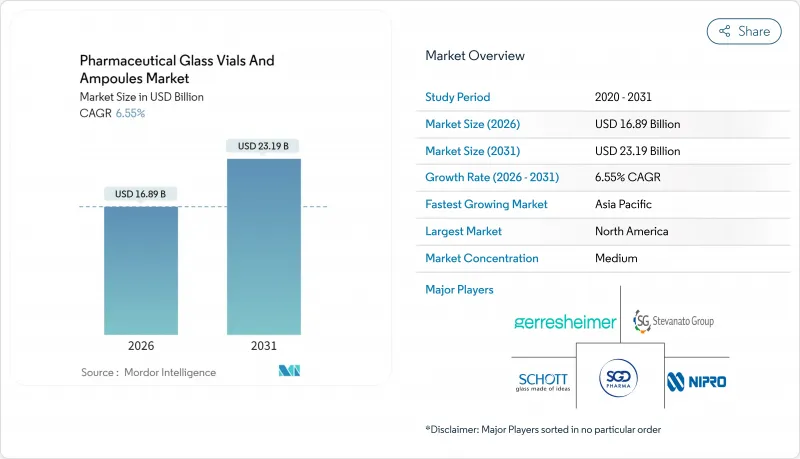

2026년 제약용 유리 바이알 및 앰풀 시장 규모는 168억 9,000만 달러로 추정되며, 2025년 158억 5,000만 달러에서 성장할 전망입니다. 2031년까지의 예측으로는 231억 9,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 6.55%를 나타낼 것으로 예상됩니다.

바이오 의약품 파이프라인의 확대, mRNA 치료제에 대한 엄격한 콜드체인 요건, 세계의 직렬화 의무화 등 견조한 기반이 폴리머 대체품보다 유리를 유리하게 유지하고 있습니다. 화학적 불활성성과 열안정성에 의해 고가치 주사제를 용출물이나 파손으로부터 보호하는 특성으로부터, 제1종 붕규산 유리가 우위성을 유지하고 있습니다. 레이디 투 유스(RTU) 멸균 플랫폼 등의 기술 혁신은 오염 위험을 줄이고 충전 및 마무리 공정의 사이클 타임을 단축함으로써 공급업체의 가격 결정력을 강화하고 있습니다. 지역별로는 아시아태평양이 바이알 제조 분야에 특히 큰 자본 유입을 기록하는 반면 북미는 FDA의 엄격한 기준에 따라 지배적인 점유율을 유지하고 있습니다. 경쟁의 치열성은 중간 정도이며, 주요 기업들은 표면 코팅 기술, 수소 연소로, 자동 시각 검사에 대한 투자를 집중시키고, 비용 중심 환경에서도 이익률을 지키고 있습니다.

세계의 제약용 유리 바이알 및 앰풀 시장 동향과 전망

유행 후 백신 개발이 바이알 수요 견인

계절적인 캠페인 종료 후에도 세계의 백신 개발은 감속하지 않고, RSV, 말라리아, 복합 부스터를 표적으로 한 다병원체 프로그램이 확대되고 있습니다. SCHOTT사의 11억 3,000만 달러 규모의 설비 증강 등에 의해 다회 투여용 제제 수요에 대응하기 위해, 소용량 유형 I 바이알의 생산 능력이 향상하고 있습니다. 규제 당국은 1상 시험 단계부터 최종 용기의 안정성 시험을 요구하고 있으며, 이에 따라 프로그램당 유리 소비량이 약 40% 증가하고 있습니다. 소아용 제제에서는 종종 2mL 및 5mL 바이알이 지정되어 치수 정밀도와 엄격한 입자 임계값에 대한 요구가 증가하고 있습니다. 이러한 동향이 더해져, 유행성 비축이 정상화한 후의 조달 일시정지가 간헐적으로 발생하는 것, 코어가 되는 바이알 수요는 장기적으로 증가 경향을 강화하고 있습니다.

생물학적 제형은 화학적으로 불활성인 붕규산 유리로 전환

대형 분자 파이프라인에서는 알칼리 용출이나 표면 반응성에 내성이 있는 용기가 요구됩니다. 2024년에 발표된 FDA 지침은 개발자를 어둡게 유형 I 붕규산 유리로 유도하는 적합성 시험 프로토콜을 강조하고 있습니다. 스테바나트의 EZ-fill 플랫폼은 추출물을 1ppm 미만으로 줄이고 공정 비교성이 심각하게 검토되는 바이오시밀러 상시에서 매력적인 임계값입니다. 재무 계산은 명확합니다. 단일 제품의 회수로 5,000만 달러의 완제품 가치가 사라질 수 있으며 고단가 유리는 안정성 부족에 대한 합리적인 헤지가 됩니다. 결과적으로, 고분자 용기가 위험이 낮은 상품 충전 시장을 침식하는 동안 붕규산 유리 공급업체는 프리미엄 가격을 유지합니다.

폴리머 바이알이 범용 유리 용기의 점유율을 침식

웨스트사의 크리스탈 제니스 라인 등의 환상 올레핀계 폴리머 용기는 진단 시약이나 초기 단계의 생물학적 제제 분야에서 수주를 획득하고 있습니다. 이러한 분야에서는 파손 내성과 유연한 리드 타임이 장기적인 적합성보다 우선하기 때문입니다. 취급 손실이나 2차 포장을 고려하면, 단위당 경제성은 폴리머가 20-30% 유리합니다. FDA 적합성 장애물이 상업적 치료제 분야에서 고분자 채용을 막는 반면, 고용량 및 저위험 분야에서는 대체 위험이 여전히 존재합니다. 따라서 표준 블로우 바이알 공급업체는 저렴한 가격대의 수량 압축에 직면하여 높은 마진 코팅 가공품 및 RTU(즉시 사용 가능) 형식으로의 전략적 전환을 강요하고 있습니다.

부문 분석

2025년 매출의 64.71%를 보로실리케이트 유리(유형 I)가 차지하고, 그 확고한 규제상의 수용성과 방대한 안정성 데이터 뱅크가 뒷받침되었습니다. 제약용 유리 바이알 및 앰풀 시장에 있어서 본소재가 차지하는 규모는 다른 소재를 능가하고 있어 리스크 회피적인 제약 기업이 신규 신청시에 알려진 성능 범위를 우선하기 때문입니다. 그러나 유전자 치료제의 페이로드가 추출 가능한 허용치를 더욱 낮추는 중 하이브리드 및 코팅 가공품이 7.4%라는 가장 빠른 CAGR을 나타낼 전망입니다. SCHOTT사의 Everic 시리즈는 플라즈마 처리 표면이 입자 발생을 줄이는 실례를 보여 주며, 이 지표는 USP<790>가이드라인 하에서 점점 엄격하게 심사되고 있습니다. 소송비용이 급증하는 가운데 조달부문은 강화유리의 프리미엄 비용과 생물학적 제제의 배치 불량에 의한 괴멸적 손실을 비교 검토하고 품질이 단가 경제성을 웃도는 가격 탄력성이 낮은 틈새 시장을 형성하고 있습니다. 소다 석회 유리(유형 II 및 III)는 주로 레거시 저분자 주사제 및 진단 시약 분야에서 살아 있지만, 그 점유율은 고품질 재료로 밀려 꾸준히 축소되고 있습니다. 알루미늄 규산염 배합 유리는 틈새 존재이며, 고가치의 항암제 원약의 동결건조 등 극단적인 열충격 환경하에서의 사용에 한정되어 있습니다.

향후 5년간의 전망에서는 붕규산 유리가 주요 점유율을 유지하는 한편, 고 pH 바이러스 벡터 현탁액용으로 설계된 표면 개질 하이브리드 유리에 점증적인 점유율을 양보할 것이 및 분석가는 예측했습니다. 수소 보조로 및 전기용해로에 대한 공급업체 투자는 재료 클래스 간의 탄소 강도 격차를 줄이고 ESG 주도의 조달 요건에 대응할 수 있습니다. 조기 도입의 CDMO 기업은 용기 사양의 컨설팅을 기술 이전 패키지에 짜넣어, 프로세스 밸리데이션 단계에서 하이브리드 유리를 사실상 고정화합니다. 이로 인해 프리미엄 등급의 여러 해에 걸친 수요 가시성이 확립되었습니다.

2025년 단위 수요의 45.88%를 백신이 차지했고, 지속적인 소아 예방접종과 신흥 여행 건강 분야가 이를 지원하고 있습니다. 수요량의 예측 가능성으로 인해, 바이알 형상은 표준화된 목 치수로 수렴하여 교체 가능한 스토퍼와 자동 충전 라인의 실현을 촉진하고 있습니다. 한편, 바이오 의약품과 바이오시밀러는 특허가 끝난 후의 단일클론항체상시를 원동력으로 8.09%라는 최고 성장률을 자랑합니다. 여기에서는 고가격 치료제의 폐기 삭감을 목적으로 한 소용량 충전으로의 전환가 진행되어, 제약용 유리 바이알 및 앰풀 시장 점유율이 변화하고 있습니다. RTU 네스트 & 튜브 형식은 다제품 시설에서 가동하는 바이오 의약품 라인에 적합하여 신속한 전환에 의한 종합 설비 효율(OEE) 향상을 실현합니다.

저분자 주사제는 포장이 아닌 약물 안정성이 보존 기간을 제한하는 분야에서 존재 의의를 유지합니다. 그러나 자동 주사기와 프리필드 주사기의 보급 확대로 기존 바이알 수요가 점차 변화하고 있습니다. 인슐린은 확립된 콜드체인 인프라에 의해 안정적인 유통량을 유지하고 있지만, 지속 투여 장치가 용기 수요 예측의 재조정을 시작하고 있는 상황입니다. 진단 시약은 비용에 민감하지만, 용매의 극성이나 완충액이 중합체 용기를 침식하는 경우 여전히 유리 용기가 지정됩니다. 이에 따라 폴리머 용기의 진보가 진행되고 있는 가운데도 일정한 기준선 수요가 확보되고 있습니다.

지역별 분석

북미는 2025년 수익의 38.92%를 차지하며, 확대되는 바이오 의약품 생산 능력, 바이오 의약품 제조 판매 승인 신청(BLA) 파이프라인 및 제1종 붕규산 유리를 우선하는 FDA의 엄격한 용기 폐쇄 프로토콜에 의해 지원되었습니다. 캐나다의 연방 바이오제조 이니셔티브는 추가 수요를 낳고 여러 해에 걸친 오프테이크 계약에 의한 지역 공급 확약을 강화하고 있습니다. 아시아태평양의 제약용 유리 바이알 및 앰풀 시장 규모는 절대치로는 작은 것으로, 중국의 GMP 강화와 인도의 노 근대화를 보조하는 생산 연동형 인센티브를 배경으로, CAGR 9.02%를 나타낼 전망입니다. 한국과 싱가포르의 위탁 포장업체는 ICH 기준을 충족하는 경쟁력 있는 가격의 RTU 제품으로 세계 브랜드를 유치하여 일본과 호주 리드 타임을 단축하고 있습니다.

유럽은 전통적인 제조업체와 강력한 지속가능성의 틀에 힘입어 견고한 점유율을 유지하고 있습니다. 그러나 탄소 크레딧의 비용 상승이 이익률을 압박하고 있으며, 조달 부문은 태국과 인도네시아 공장을 이용하여 상품량을 확보하는 혼합 조달 모델의 평가를 강요받고 있습니다. 라틴아메리카는 미국 제약 회사의 니어 쇼어링 전략의 혜택을 받고 있으며, 특히 멕시코에서는 USMCA의 무역 규정에 따라 바이알 공급과 관련된 통관 장애물이 완화되었습니다. 중동 및 아프리카는 여전히 발전의 초기 단계이지만 전략적으로 중요한 지역입니다. 걸프 협력 회의(GCC) 회원국은 현지 조달 비율을 규정한 백신 충전·마무리의 허브에 자금을 제공하고 있어 1차 용기에 대한 새로운 지역 수요의 도래를 예감시킵니다. 전반적으로 지리적 분산은 단일 지역에서 혼란의 위험을 줄이지만 공급업체는 다양한 규제 상황에서 품질 시스템을 조화시켜야합니다. 여러 거점의 인증은 제안 의뢰서 평가에서 결정적인 기준으로 부상하고 있으며, 소규모 지역 생산자는 제휴와 통합을 강요받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 팬데믹 후 백신 개발 파이프라인이 바이알 수요 촉진

- 생물학적 제제는 화학적으로 불활성인 붕규산 유리로 이행

- 유리를 유리하게 하는 지속가능성과 재활용성에 관한 규제

- 색분해 앰풀에 대한 RFID 직렬화 의무화

- mRNA 콜드체인에는 초저온 확장 유리가 필요

- 시장 성장 억제요인

- 폴리머제 바이알이 범용 유리 제품의 점유율을 침식

- 취약성/파손에 의한 리콜이 증가하여 리스크 경감 비용이 상승

- 고 pH 유전자 치료 충전제에서의 나트륨 이온 용출

- 탄소 가격 설정의 압력에 직면한 에너지 집약형로

- 업계 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 소재 유형별

- 제1형 붕규산 유리

- 제2/3형 소다-라임 유리

- 알루미늄-규산 유리

- 하이브리드 및 표면 코팅 유리

- 용도별

- 백신

- 인슐린

- 생물학적 제형 및 바이오시밀러

- 소분자 주사제

- 진단 시약

- 최종 사용자별

- 제약 제조업체

- 바이오테크놀러지 기업

- CDMO 및 CMO

- 연구 및 학술 실험실

- 병원 및 진료소

- 제조 기술별

- 관형 유리 성형

- 성형 유리 성형

- 즉시 사용 가능(RTU) 멸균

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 케냐

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- SCHOTT AG

- Gerresheimer AG

- Stevanato Group SpA

- Nipro Corporation

- SGD SA(SGD Pharma)

- Corning Incorporated

- Bormioli Pharma SpA

- Stoelzle Oberglas GmbH

- Accu-Glass LLC

- APPL Solutions Pvt Ltd

- Shandong Pharmaceutical Glass Co., Ltd

- Chongqing Zhengchuan Pharmaceutical Packaging Co., Ltd

- Cangzhou Four Star Glass Co., Ltd

- Origin Pharma Packaging Ltd

- DWK Life Sciences GmbH

- West Pharmaceutical Services Inc.

- Sisecam Cambalkon Sanayi AS

- Stoelzle Glass Group

- Ardagh Group SA

- Beatson Clark Ltd

제7장 시장 기회와 향후 전망

KTH 26.01.26pharmaceutical glass vials and ampoules market size in 2026 is estimated at USD 16.89 billion, growing from 2025 value of USD 15.85 billion with 2031 projections showing USD 23.19 billion, growing at 6.55% CAGR over 2026-2031.

Robust fundamentals including expanding biologics pipelines, demanding cold-chain requirements for mRNA therapeutics, and global serialization mandates continue to favor glass over polymer alternatives. Type I borosilicate retains primacy because its chemical inertness and thermal stability safeguard high-value injectables from leachables and breakage. Technology upgrades such as ready-to-use (RTU) sterile platforms lower contamination risk and trim fill-finish cycle times, strengthening supplier pricing power. Regionally, Asia-Pacific registers outsized capital inflows into vial manufacturing, while North America's stringent FDA standards solidify its dominant share position. Competitive intensity remains moderate, with leaders funneling investment into surface-coating science, hydrogen-fired furnaces, and automated visual inspection to defend margins in an otherwise cost-sensitive environment.

Global Pharmaceutical Glass Vials And Ampoules Market Trends and Insights

Post-pandemic Vaccine Pipeline Boosts Vial Demand

Global vaccine development no longer tapers after seasonal campaigns; instead, multi-pathogen programs targeting RSV, malaria, and combination boosters are expanding. Capacity additions such as SCHOTT's USD 1.13 billion upgrade elevate small-volume Type I production to meet multi-dose presentation needs. Regulators insist on final-container stability testing from Phase I onward, lifting glass consumption per program by roughly 40%. Pediatric formulations often specify 2 mL and 5 mL vials, accentuating demand for dimensional accuracy and stringent particulate thresholds. These dynamics collectively reinforce a secular uplift in core vial volumes despite intermittent procurement pauses once pandemic stockpiles normalize.

Biologics Shift Toward Chemically Inert Borosilicate

Large-molecule pipelines demand containers that resist alkali leaching and surface reactivity. FDA guidance released in 2024 underscores compatibility testing protocols that implicitly steer developers toward Type I borosilicate. Stevanato's EZ-fill platform reduces extractables below 1 ppm, a threshold attractive to biosimilar launches where process comparability is scrutinized. The financial calculus is direct: a single product recall can erase USD 50 million in finished-goods value, making higher unit-price glass a rational hedge against stability failures. Consequently, borosilicate suppliers preserve premium pricing even while polymer containers nibble away at low-risk, commodity fills.

Polymer Vials Cannibalising Commodity Glass Share

Cyclic olefin polymer containers such as West's Crystal Zenith line secure orders for diagnostic reagents and early-phase biologics, where break-resistance and flexible lead times outrank lifetime compatibility. Unit economics favor polymers by 20-30% once handling losses and secondary packaging are tallied. Although FDA compatibility hurdles deter polymer uptake for commercial therapeutics, high-volume, lower-risk segments remain vulnerable to substitution. Suppliers of standard blown V-ials therefore experience volume compression at the low end, prompting a strategic pivot toward higher-margin, coated or RTU formats.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and Recyclability Regulations Favour Glass

- RFID-Serialisation Mandates for Colour-Coded Ampoules

- Fragility/Breakage Recalls Increase Risk-Mitigation Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type I borosilicate retained 64.71% of 2025 revenues, underscoring its entrenched regulatory acceptance and vast stability data bank. The pharmaceutical glass vials and ampoules market size attributed to this material outpaces all other substrates because risk-averse drug makers prioritize known performance envelopes when filing new applications. Hybrid and coated variants, however, deliver the fastest 7.4% CAGR as gene-therapy payloads push extractable allowances ever lower. SCHOTT's Everic series demonstrates how plasma-enhanced surfaces reduce particle generation, a metric increasingly scrutinized under USP <790> guidelines. As litigation costs soar, procurement teams weigh the premium of enhanced glass against the catastrophic downside of biologic batch failures, creating a price-in-elastic niche where quality trumps unit economics. Soda-lime glass-types II and III-survive mostly in legacy, small-molecule injectables and diagnostic reagents, but their share steadily erodes in favor of higher-grade materials. Aluminum-silicate formulations remain niche, reserved for extreme thermal-shock scenarios such as freeze-drying of high-value oncology APIs.

Across a five-year horizon, analysts expect borosilicate to retain a majority stake yet cede incremental share to surface-engineered hybrids designed for high-pH viral vector suspensions. Supplier investments in hydrogen-assisted furnaces and electric melting reduce the carbon intensity gap between material classes, accommodating ESG-driven sourcing mandates. Early-adopter CDMOs are bundling container specification counseling into tech-transfer packages, effectively locking in hybrid glass at the process-validation stage and cementing multiyear demand visibility for premium grades.

Vaccines accounted for 45.88% of 2025 unit demand, undergirded by ongoing pediatric immunization and emerging travel-health indications. Given volume predictability, vial formats have converged on standardized neck dimensions facilitating interchangeable stoppers and automated filling lines. Meanwhile, biologics and biosimilars claim the highest 8.09% growth trajectory, fueled by monoclonal antibody launches post-patent cliff. Here, the pharmaceutical glass vials and ampoules market share shifts toward smaller fill volumes that mitigate wastage for high-price therapies. RTU nest-and-tub formats resonate with biologics lines operating in multiproduct facilities, offering rapid changeovers that boost overall equipment effectiveness.

Small-molecule injectables preserve relevance where drug stability, not packaging, constrains shelf life; however, rising adoption of auto-injectors and prefilled syringes gradually siphons volume from traditional vials. Insulin maintains steady throughput thanks to entrenched cold-chain infrastructure, but continuous-delivery devices are beginning to recalibrate container demand forecasts. Diagnostic reagents, although cost-sensitive, continue to specify glass where solvent polarity or buffered media attack polymer walls, ensuring a residual baseline volume even amid polymer advances.

The Pharmaceutical Glass Vials and Ampoules Market Report is Segmented by Material Type (Type I Borosilicate Glass, Type II/III Soda-Lime Glass and More), Application (Vaccines, Insulin and More), End User (Pharmaceutical Manufacturers, Biotechnology Companies and More), Manufacturing Technology (Tubular Glass Forming, Moulded Glass Forming and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38.92% of 2025 revenues, buoyed by expansive biologics capacity, Biologics License Application pipelines, and the FDA's strict container-closure protocols that privilege Type I borosilicate. Canada's federal bio-manufacturing initiative adds incremental demand, reinforcing regional supply commitments with multi-year offtake agreements. The pharmaceutical glass vials and ampoules market size in Asia-Pacific, while smaller in absolute terms, grows at a 9.02% CAGR on the back of Chinese GMP enhancements and Indian production-linked incentives that subsidize furnace modernization. Contract packagers in South Korea and Singapore lure global brands with competitively priced RTU offerings that meet ICH standards, trimming lead times into Japan and Australia.

Europe commands robust share underpinned by legacy manufacturers and a strong sustainability framework; yet rising carbon-credit costs pressure margins, nudging procurement to evaluate mixed sourcing models tapping Thai and Indonesian plants for commodity volumes. Latin America benefits from near-shoring strategies by U.S. pharma, particularly in Mexico where USMCA trade provisions smooth customs hurdles for vial supply. The Middle East and Africa remain nascent but strategic, with Gulf Cooperation Council nations funding vaccine fill-finish hubs that stipulate local content thresholds, foreshadowing fresh regional demand for primary containers. Collectively, geographic diversification mitigates single-region disruption risk, but it forces suppliers to harmonize quality systems across heterogeneous regulatory landscapes. Multisite qualification emerges as a decisive criterion in request-for-proposal scoring, pushing small regional producers to partner or consolidate.

- SCHOTT AG

- Gerresheimer AG

- Stevanato Group S.p.A.

- Nipro Corporation

- SGD S.A. (SGD Pharma)

- Corning Incorporated

- Bormioli Pharma S.p.A.

- Stoelzle Oberglas GmbH

- Accu-Glass LLC

- APPL Solutions Pvt Ltd

- Shandong Pharmaceutical Glass Co., Ltd

- Chongqing Zhengchuan Pharmaceutical Packaging Co., Ltd

- Cangzhou Four Star Glass Co., Ltd

- Origin Pharma Packaging Ltd

- DWK Life Sciences GmbH

- West Pharmaceutical Services Inc.

- Sisecam Cambalkon Sanayi A.S.

- Stoelzle Glass Group

- Ardagh Group S.A.

- Beatson Clark Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-pandemic vaccine pipeline boosts vial demand

- 4.2.2 Biologics shift toward chemically inert borosilicate

- 4.2.3 Sustainability and recyclability regulations favour glass

- 4.2.4 RFID-serialisation mandates for colour-coded ampoules

- 4.2.5 mRNA cold-chain needs ultra-low expansion glass

- 4.3 Market Restraints

- 4.3.1 Polymer vials cannibalising commodity glass share

- 4.3.2 Fragility/breakage recalls increase risk-mitigation cost

- 4.3.3 Sodium-ion leaching in high-pH gene-therapy fills

- 4.3.4 Energy-intensive furnaces face carbon-pricing pressure

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Type I Borosilicate Glass

- 5.1.2 Type II/III Soda-Lime Glass

- 5.1.3 Aluminum-Silicate Glass

- 5.1.4 Hybrid / Surface-Coated Glass

- 5.2 By Application

- 5.2.1 Vaccines

- 5.2.2 Insulin

- 5.2.3 Biologics and Biosimilars

- 5.2.4 Small-Molecule Injectables

- 5.2.5 Diagnostic Reagents

- 5.3 By End User

- 5.3.1 Pharmaceutical Manufacturers

- 5.3.2 Biotechnology Companies

- 5.3.3 CDMOs / CMOs

- 5.3.4 Research and Academic Laboratories

- 5.3.5 Hospitals and Clinics

- 5.4 By Manufacturing Technology

- 5.4.1 Tubular Glass Forming

- 5.4.2 Moulded Glass Forming

- 5.4.3 Ready-to-Use (RTU) Sterile

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 SCHOTT AG

- 6.4.2 Gerresheimer AG

- 6.4.3 Stevanato Group S.p.A.

- 6.4.4 Nipro Corporation

- 6.4.5 SGD S.A. (SGD Pharma)

- 6.4.6 Corning Incorporated

- 6.4.7 Bormioli Pharma S.p.A.

- 6.4.8 Stoelzle Oberglas GmbH

- 6.4.9 Accu-Glass LLC

- 6.4.10 APPL Solutions Pvt Ltd

- 6.4.11 Shandong Pharmaceutical Glass Co., Ltd

- 6.4.12 Chongqing Zhengchuan Pharmaceutical Packaging Co., Ltd

- 6.4.13 Cangzhou Four Star Glass Co., Ltd

- 6.4.14 Origin Pharma Packaging Ltd

- 6.4.15 DWK Life Sciences GmbH

- 6.4.16 West Pharmaceutical Services Inc.

- 6.4.17 Sisecam Cambalkon Sanayi A.S.

- 6.4.18 Stoelzle Glass Group

- 6.4.19 Ardagh Group S.A.

- 6.4.20 Beatson Clark Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment