|

시장보고서

상품코드

1910858

IT 인재파견 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)IT Staffing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

IT 인재파견 시장은 2025년 1,233억 달러에서 2026년에는 1,277억 5,000만 달러로 성장해 2026년부터 2031년에 걸쳐 CAGR 3.61%를 나타낼 것으로 예상됩니다. 2031년까지 1,524억 7,000만 달러에 달할 전망입니다.

이 꾸준한 확대는 기업이 인재 전략을 대량 채용에서 전문 기술 획득으로 재조정하고 있음을 반영하며 클라우드, 인공지능, 사이버 보안에 대한 지출 우선순위에 따라 이러한 변화가 더욱 강화되고 있습니다. 일시적 및 계약 기반의 고용 형태가 여전히 주류이지만, 성장은 공급자에게 납품 위험을 이전하는 작업 명세서(SOW) 모델로 전환하고 있습니다. 생성형 AI 엔지니어링, 엣지 컴퓨팅, 사이버 탄력성에 대한 수요가 구인 요구 사항을 재구성하는 동안 지속적인 세계 기술 부족은 임금 상승 압력을 유지합니다. 동시에 전 세계 2,000개 기업의 공급업체 통합이 진행됨에 따라 매니지드 서비스 제공업체의 이익률은 압박되고 기존 고객과의 거래 점유율은 확대되고 있습니다.

세계의 IT 인재파견 시장 동향과 인사이트

AI, 클라우드, IoT 중심의 디지털 전환 프로젝트 도입 가속화

세계 기술직 구인의 AI 또는 머신러닝 스킬의 요구 비율은 전년 대비 9%에서 14%로 증가하고 있습니다. 클라우드 마이그레이션에는 전문적인 DevOps 엔지니어와 보안 아키텍트가 요구되며, 2030년까지 1,395억 8,000만 달러에 이를 것으로 예상되는 엣지 컴퓨팅 투자에는 인프라와 IoT를 융합한 인재가 필수적입니다. NTT DATA가 20만명의 직원을 대상으로 생성형 AI 연수를 실시할 계획은 진행 중인 리스킬 규모의 크기를 더욱 뒷받침하고 있습니다. AI 알고리즘, 클라우드 리소스 및 디바이스 네트워크를 연계하는 학제 간 프로젝트 팀은 IT 인재파견 시장의 지속적인 확장을 이끌고 있습니다.

분산 인력이 필요한 원격 하이브리드 근무 모델 확대

델 테크놀로지스 직원의 65%가 공식적인 유연한 근무 형태를 이용하고 있으며, 장소를 가리지 않는 채용이 정착되고 있음을 보여줍니다. 고용주는 보다 광범위한 인력 풀에 접근할 수 있는 반면, 국경을 넘어선 컴플라이언스와 증가하는 임금 격차 해소의 기대를 다루어야 합니다. 맨파워그룹의 2025년 전망에 따르면 41%의 기업이 인원 증가를 계획했으며 기술직이 수요 톱을 차지했습니다. 경쟁 입찰은 대륙을 넘어 퍼져 보상 수준을 끌어올리는 것과 동시에 급여를 넘은 정착 촉진책의 강화를 인재 소개 회사에 육박하고 있습니다.

틈새 기술 분야의 지속적인 세계 기술 부족

미해결 디지털 스킬 부족은 2034년까지 세계 경제에 손실을 초래할 것으로 추정되고 있으며, 양자 기술, 고급 AI, 제로 트러스트 보안 전문 지식의 구조적인 공급 제약이 부각되고 있습니다. 대학은 커리큘럼 갱신에 뒤처져 있으며, 졸업생들이 이러한 전문 분야에 착수하기까지 몇년단위의 시간 지연이 발생하고 있습니다. 이 인력 부족은 보상 패키지를 밀어 올리고 프로젝트 기간을 연장하기 때문에 기업은 단기 투자 이익률(ROI)을 해치는 집중적인 재기술화 이니셔티브에 자금을 투입해야 합니다.

부문 분석

소프트웨어 개발자는 2025년 시점에서 IT 인재파견 시장의 37.05%를 차지했으며 정착한 용도 근대화 프로젝트를 반영했습니다. 생성형 AI 엔지니어는 2031년까지 연평균 복합 성장률(CAGR) 11.75%를 나타낼 것으로 예측되며, 프롬프트 설계, 모델 감사, 대규모 언어 모델(LLM)의 미세 조정에 대한 수요가 증가하고 있습니다. 에지 클라우드 파이프라인이 확대됨에 따라 데이터 및 AI 엔지니어링 분야의 IT 인재파견 시장 규모는 급격히 확대될 것으로 전망됩니다. 급여 수준은 하이브리드 AI 개발 전문 지식을 제공할 때 기업이 요구할 수 있는 프리미엄 가격을 제안합니다.

기존의 테스터나 QA직은 자동화의 역풍을 받아 많은 전문가가 AI 탑재 검증 툴로 이행하고 있습니다. 시스템 분석가는 통합 아키텍처로, 네트워크 전문가는 AI 기반 위협 모니터링에 능숙합니다. 신기술(양자 개발, 블록체인 아키텍처, IoT 디바이스 보안)은 IT 인재파견 시장의 작지만 급성장하는 분야로 존재감을 늘리고 있습니다.

BFSI(은행 및 금융 및 보험)는 2025년 시점에서 24.15%의 점유율을 유지해 최대의 채용 분야이며, 오픈뱅킹 대응과 핀테크 플랫폼의 업그레이드가 견인했습니다. 의료 분야는 전자 건강 기록의 근대화와 AI 지원 진단에 의해 10.25%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장 분야로 대두하고 있습니다. 원격 의료 및 환자 데이터 상호 운용성 기준의 정착에 따라 의료 프로젝트를 위한 IT 인재파견 시장 규모 확대가 예상됩니다.

제조에서는 IoT와 예지보전 인력이 필요한 스마트 팩토리의 도입이 우선됩니다. 소매·EC 업계에서는 옴니 채널 구축이 계속되고, 공공 기관에서는 사이버 보안과 시민 서비스 디지털화의 예산이 확보되고 있습니다. 에너지, 자동차, 스마트시티 프로그램은 '기타 산업' 카테고리로 분류되어 각각 특화된 스킬셋을 요구하며 IT 인재파견 시장에 다양한 인재 파이프라인을 제공합니다.

지역별 분석

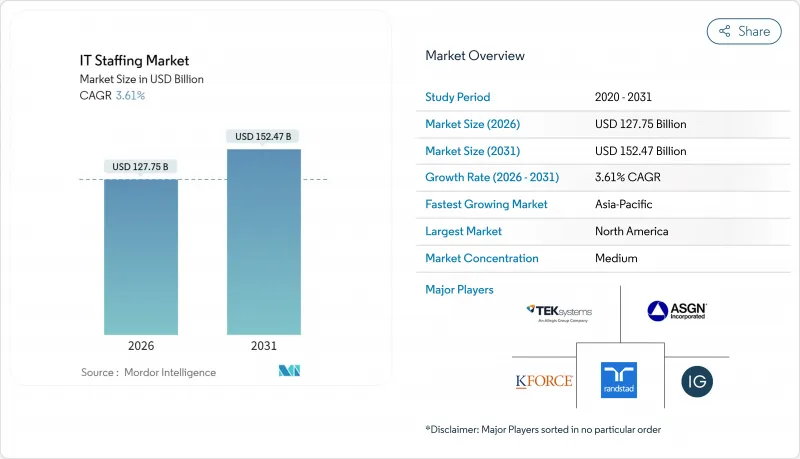

북미는 2025년에 44.05%의 점유율을 유지하며 고급 기술 생태계, 대규모 디지털 예산 및 엄격한 보안 요구사항을 뒷받침했습니다. 지속적인 비자 정책 변경과 임금 상승으로 인재 확보가 어려워지고 있으며 캐나다와 라틴아메리카로의 니어 쇼어링이 증가하고 있습니다. 미국은 실리콘 밸리의 소프트웨어 프로젝트와 월스트리트의 클라우드 쇄신에 의해 수요를 견인하고 캐나다는 토론토와 몬트리올에서 비용 우위의 거점을 제공합니다.

아시아태평양은 8.15%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장을 기록할 전망입니다. 인도의 IT 서비스 확대, 일본의 리스킬 시책, 싱가포르의 지역 본사 유치가 견인역입니다. 다국적기업의 조달처 다양화에 의해 이 지역의 매니지드 서비스 연간 계약액은 2024년에 32% 증가했습니다. 중국의 플랫폼 회복과 한국의 반도체 연구 개발이 전문 인력 수요를 더욱 밀어 올리고 있습니다.

유럽에서는 독일과 영국에서 안정적인 수요가 지속되는 반면, 동유럽 국가들은 순수한 비용 우위에서 틈새 전문센터로 진화하고 있습니다. GDPR(EU 개인정보보호규정) 대응으로 사이버 보안 수요는 높은 수준을 유지합니다. 중동 및 아프리카는 뒷받침되는 꾸준한 성장을 보여 사우디아라비아의 스마트 시티 프로젝트와 남아프리카의 영어 서비스 거점이 현저한 수요원이 되고 있습니다. 이러한 시장의 통화 조정 후 임금 격차는 세계의 IT 인재파견 시장에서 공급자의 이익률 전략을 형성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 시장 성장 촉진요인

- AI·클라우드·IoT를 중심으로 한 디지털 전환 프로젝트의 도입 가속

- 분산형 인재를 필요로 하는 리모트 및 하이브리드 근무 모델의 확대

- 사이버 보험 의무화에 의한 사이버 탄력 인재 수요 급증

- 팬데믹 후의 디지털 변혁 예산의 회복이 인재 증강 수요를 촉진

- 생성형 AI 감독직(프롬프트 엔지니어, 모델 감사인)의 출현

- 세계 2000 기업의 공급업체 통합이 MSP 주도의 볼륨딜을 촉진

- 시장 성장 억제요인

- 틈새 기술 분야의 지속적인 세계 기술 부족

- 임금 인플레이션이 MSP 청구 단가의 이익률을 압박

- AI 기반의 셀프 서비스 채용 플랫폼이 인재 소개 회사 배제

- 데이터 주권법의 강화에 의해 국경을 넘은 인재 배치 제한

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 업계 생태계 분석

- 주요 이용 사례와 사례 연구

- 거시 경제 동향 평가

- 투자분석

제5장 시장 세분화

- 스킬 세트별

- 소프트웨어 개발자

- 테스터 및 QA 엔지니어

- 시스템 분석가 및 비즈니스 분석가

- 기술 지원 전문가

- 네트워크 및 보안 전문가

- 데이터 및 AI 엔지니어

- 기타 스킬 세트

- 최종 사용자 업계별

- 통신

- 은행, 금융 서비스 및 보험(BFSI)

- 헬스케어 및 생명과학

- 제조

- 소매업 및 전자상거래

- 정부 및 공공 부문

- 기타 산업

- 인재파견 서비스 유형별

- 임시 및 계약 인재파견

- 정규직 배치

- 작업명세서(SOW) 및 프로젝트 기반

- 매니지드 서비스 제공업체(MSP) 및 아웃소싱 인재파견

- 기업 규모별

- 대기업

- 중소기업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 싱가포르

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- TEKsystems Inc.(Allegis Group Holdings Inc.)

- ASGN Incorporated

- Insight Global LLC

- Randstad NV

- Kforce Inc.

- Artech Information Systems LLC

- Consulting Solutions International Inc.

- MATRIX Resources Inc.

- NTT DATA Corporation

- Beacon Hill Staffing Group LLC

- Experis IT(ManpowerGroup Global Inc.)

- Akkodis(Adecco Group AG)

- Kelly Services Inc.

- Motion Recruitment Partners LLC

- Robert Half International Inc.

- Genesis10 Inc.

- Collabera LLC

- PERSOL Holdings Co., Ltd.

- Aquent LLC

- CGI Inc.

제7장 시장 기회와 향후 전망

KTH 26.01.26The IT staffing market is expected to grow from USD 123.30 billion in 2025 to USD 127.75 billion in 2026 and is forecast to reach USD 152.47 billion by 2031 at 3.61% CAGR over 2026-2031.

This steady expansion reflects enterprises realigning talent strategies toward specialized skill acquisition rather than volume hiring, a change reinforced by cloud, artificial intelligence, and cybersecurity spending priorities. Temporary and contract engagements remain the dominant hiring mechanism, yet growth is gravitating toward Statement-of-Work models that shift delivery risk to providers. Generative-AI engineering, edge computing, and cyber-resilience needs are reshaping job requisitions, while persistent global skill shortages sustain upward wage pressure. At the same time, vendor consolidation across Global-2000 clients compresses margins for managed service providers but also deepens their wallet share with retained customers.

Global IT Staffing Market Trends and Insights

Accelerated Adoption of AI-, Cloud- and IoT-Centric Digital-Transformation Projects

Fourteen percent of global tech job postings now demand AI or machine-learning skills, up from 9% a year earlier . Cloud migrations call for specialized DevOps engineers and security architects, while edge-computing investments that are projected to reach USD 139.58 billion by 2030 require blended infrastructure-plus-IoT talent. NTT DATA's program to train 200,000 employees in generative AI further underscores the scale of reskilling underway . Interdisciplinary project teams that connect AI algorithms, cloud resources, and device networks are therefore driving sustained expansion in the IT staffing market.

Expansion of Remote and Hybrid Work Models Requiring Distributed Talent

Sixty-five percent of Dell Technologies personnel use formal flexibility arrangements, signaling lasting normalization of location-agnostic hiring. Employers gain access to broader talent pools, yet must navigate cross-border compliance and rising pay parity expectations. ManpowerGroup's 2025 outlook shows 41% of firms plan to add headcount, with technology roles topping demand charts. Competitive bidding now spans continents, increasing compensation levels and compelling agencies to enhance retention packages that extend beyond salary.

Persistent Global Skill Shortages in Niche Technologies

It is estimates that unresolved digital-skills gaps could cost the global economy by 2034, underscoring structural supply constraints for quantum, advanced AI, and zero-trust security expertise. Universities have not kept curriculum pace, creating multiyear lags before new graduates enter these specializations. The scarcity elevates compensation packages and lengthens project timelines, compelling enterprises to bankroll intensive reskilling initiatives that erode near-term ROI.

Other drivers and restraints analyzed in the detailed report include:

- Surging Demand for Cyber-Resilience Staff Driven by Cyber-Insurance Mandates

- Digital-Transformation Budget Rebound Post-Pandemic Fuels Staff-Augmentation Demand

- Wage Inflation Compressing MSP Bill-Rate Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software developers accounted for 37.05% of IT staffing market share in 2025, reflecting entrenched application modernization projects. Generative-AI engineers are projected to register a 11.75% CAGR through 2031, underscoring growing demand for prompt design, model auditing, and LLM fine-tuning. The IT staffing market size for data and AI engineering is projected to escalate sharply as edge-cloud pipelines scale. Salary corridors signal premium pricing that providers can command when supplying hybrid AI-development expertise.

Traditional testers and QA roles face automation headwinds, pushing many professionals toward AI-enabled verification tools. Systems analysts are pivoting to integration architecture, and network specialists are upskilling in AI-driven threat monitoring. Emerging skills-quantum development, blockchain architecture, and IoT device security-collectively remain a small but rapidly expanding slice of the IT staffing market.

BFSI remained the largest adopter with 24.15% share in 2025, driven by open-banking compliance and fintech platform upgrades. Healthcare emerges as the fastest-growing vertical at 10.25% CAGR, propelled by electronic-health-record modernization and AI-assisted diagnostics. The IT staffing market size for healthcare projects is expected to widen as telemedicine and patient-data interoperability standards take hold.

Manufacturing prioritizes smart-factory deployments requiring IoT and predictive-maintenance talent. Retail and e-commerce continue omnichannel build-outs, while public sector agencies earmark cybersecurity and citizen-service digitization budgets. Energy, automotive, and smart-city programs fill the "Other Industries" category, each demanding bespoke skill combinations and feeding diverse pipelines for the IT staffing market.

IT Staffing Market Report is Segmented by Skill Set (Software Developer, Testers and QA Engineers, Systems Analyst, Technical Support Professionals, Networking and Security Experts, and More), End-User Industry (Telecom, BFSI, and More), Staffing Service Type (Contract Staffing, and More), Enterprise Size (Large Enterprises, and SMEs), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 44.05% share in 2025, supported by deep tech ecosystems, large digital budgets, and rigorous security mandates. Continuous visa policy shifts and wage escalation challenge talent availability, prompting more near-shoring to Canada and Latin America. The United States leads demand due to Silicon Valley software projects and Wall Street cloud overhauls, while Canada provides cost-advantaged hubs in Toronto and Montreal.

Asia-Pacific is the fastest-growing region at an 8.15% CAGR, buoyed by India's IT services scale-up, Japanese reskilling initiatives, and Singapore's regional headquarters attraction. Managed-services annual contract value in the region rose 32% in 2024 as multinationals diversified sourcing. China's platform rebound and Korea's semiconductor R&D add further pull on specialist headcount.

Europe posts stable demand in Germany and the United Kingdom, even as Eastern European destinations evolve from pure cost-arbitrage to niche specialist centers. GDPR compliance maintains high cybersecurity uptake. Middle East and Africa trail but register steady growth; Saudi Arabia's smart-city projects and South Africa's English-language service hubs are notable demand pockets. Currency-adjusted wage differentials across these markets shape provider margin strategies within the global IT staffing market.

- TEKsystems Inc. (Allegis Group Holdings Inc.)

- ASGN Incorporated

- Insight Global LLC

- Randstad N.V.

- Kforce Inc.

- Artech Information Systems LLC

- Consulting Solutions International Inc.

- MATRIX Resources Inc.

- NTT DATA Corporation

- Beacon Hill Staffing Group LLC

- Experis IT (ManpowerGroup Global Inc.)

- Akkodis (Adecco Group AG)

- Kelly Services Inc.

- Motion Recruitment Partners LLC

- Robert Half International Inc.

- Genesis10 Inc.

- Collabera LLC

- PERSOL Holdings Co., Ltd.

- Aquent LLC

- CGI Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated adoption of AI-, Cloud- and IoT-centric digital-transformation projects

- 4.2.2 Expansion of remote and hybrid work models requiring distributed talent

- 4.2.3 Surging demand for cyber-resilience staff driven by cyber-insurance mandates

- 4.2.4 Digital-transformation budget rebound post-pandemic fuels staff-augmentation demand

- 4.2.5 Generative-AI supervision roles (prompt engineers, model auditors) emerge

- 4.2.6 Vendor consolidation among Global-2000 clients boosts MSP-led volume deals

- 4.3 Market Restraints

- 4.3.1 Persistent global skill shortages in niche technologies

- 4.3.2 Wage inflation compressing MSP bill-rate margins

- 4.3.3 AI-based self-service hiring platforms disintermediate agencies

- 4.3.4 Tightening data-sovereignty laws restrict cross-border staff deployment

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porterss Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Skill Set

- 5.1.1 Software Developers

- 5.1.2 Testers and QA Engineers

- 5.1.3 Systems Analysts / Business Analysts

- 5.1.4 Technical Support Professionals

- 5.1.5 Networking and Security Experts

- 5.1.6 Data and AI Engineers

- 5.1.7 Other Skill Sets

- 5.2 By End-User Industry

- 5.2.1 Telecom

- 5.2.2 Banking, Financial Services and Insurance (BFSI)

- 5.2.3 Healthcare and Life Sciences

- 5.2.4 Manufacturing

- 5.2.5 Retail and e-Commerce

- 5.2.6 Government and Public Sector

- 5.2.7 Other Industries

- 5.3 By Staffing Service Type

- 5.3.1 Temporary / Contract Staffing

- 5.3.2 Permanent Placement

- 5.3.3 Statement-of-Work (SOW) / Project-based

- 5.3.4 Managed Service Provider (MSP) / Outsourced Staffing

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TEKsystems Inc. (Allegis Group Holdings Inc.)

- 6.4.2 ASGN Incorporated

- 6.4.3 Insight Global LLC

- 6.4.4 Randstad N.V.

- 6.4.5 Kforce Inc.

- 6.4.6 Artech Information Systems LLC

- 6.4.7 Consulting Solutions International Inc.

- 6.4.8 MATRIX Resources Inc.

- 6.4.9 NTT DATA Corporation

- 6.4.10 Beacon Hill Staffing Group LLC

- 6.4.11 Experis IT (ManpowerGroup Global Inc.)

- 6.4.12 Akkodis (Adecco Group AG)

- 6.4.13 Kelly Services Inc.

- 6.4.14 Motion Recruitment Partners LLC

- 6.4.15 Robert Half International Inc.

- 6.4.16 Genesis10 Inc.

- 6.4.17 Collabera LLC

- 6.4.18 PERSOL Holdings Co., Ltd.

- 6.4.19 Aquent LLC

- 6.4.20 CGI Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment