|

시장보고서

상품코드

1910887

플라스틱 사출 성형 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Plastics Injection Molding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

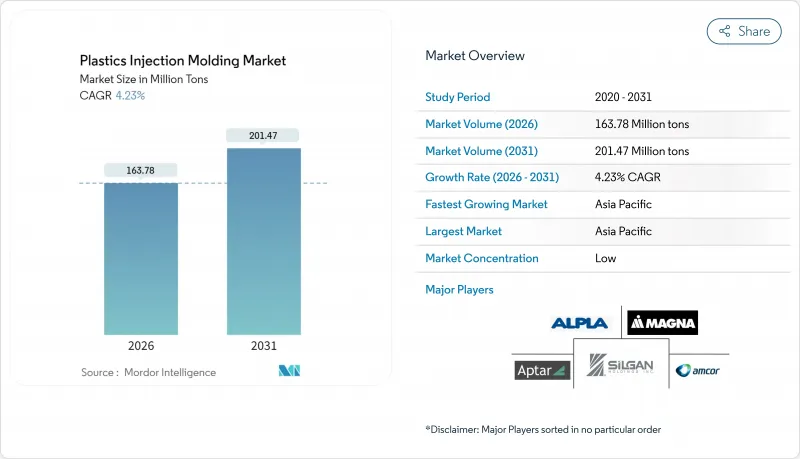

플라스틱 사출 성형 시장은 2025년 1억 5,713만 달러로 평가되었으며, 2026년 1억 6,378만 달러에서 2031년까지 2억 147만 달러에 도달할 것으로 예상됩니다. 예측 기간(2026-2031년)의 CAGR은 4.23%를 나타낼 것으로 전망됩니다.

이러한 지속적인 확대는 포장, 자동차, 전자기기, 의료기기 분야에서 비용 효율적인 대량 생산에 있어 본 기술이 핵심적인 역할을 하고 있음을 보여줍니다. 전자상거래의 성장, 전기자동차(EV) 생산의 가속, 순환형 사회를 향한 규제 추진이 함께 플라스틱 사출 성형 시장의 응용 기반을 확대하고 있습니다. 한편, 에너지 효율이 뛰어난 전동식 성형기와 선진적인 재료 배합 기술이 생산자의 원재료 비용 상승을 상쇄하는 데 도움이 되고 있습니다. 아시아태평양의 전자기기 산업 클러스터의 확대, 북미에서의 리쇼어링(생산 회귀)의 대처, 유럽의 재생 가능성 규제에 있어서 선행자 우위성 등 지역적 요인이 각 지역의 기회를 확대하고 있습니다. 한편, 원유가격 연동에 의한 수지가격의 변동과 세계 플라스틱규제의 강화는 이익률을 억제하고, 재생원료에 대한 투자, 디지털 품질관리, 사용후 제품의 추적 가능성 시스템에 대한 투자를 촉구하고 있습니다.

세계의 플라스틱 사출 성형 시장 동향과 인사이트

전자상거래로 인한 포장 수요 급증

폭발적으로 증가하는 소포량에 따라 내구성이 있지만 경량의 보호 솔루션에 대한 요구가 높아지고 있습니다. 이로 인해 브랜드 소유자는 강도를 손상시키지 않고 재료 사용량을 최소화하는 단일 소재의 폴리에틸렌 및 폴리 프로파일렌 포장을 지정하는 경향이 강해지고 있습니다. 2025년에 시행된 EU 포장·포장 폐기물 규제(PPWR)에서는 2030년까지 PET 식품 포장에 30%의 재생재 함유를 의무화하고 있어 고재생재 배합에 대응하기 위한 금형이나 공정 파라미터의 재설계가 가속하고 있습니다. 미국 14주에 도입된 확대 생산자 책임(EPR) 제도는 추가 비용 요인이 되어 환경 배려 설계를 촉진함과 동시에 고급 수지 재생 라인을 가지는 컨버터 기업을 우대합니다. 이러한 규제의 시너지 효과로 플라스틱 사출 성형 시장 수요 증가가 가속화되고 있으며, 특히 얇은 용기·캡 분야에서는 사이클 타임 단축에 의한 재료 절약과 생산성 향상이 실현되고 있습니다. 선진적인 성형 제조업체는 선별 공정의 효율화를 도모하기 위해 인몰드 라벨링이나 디지털 워터마크 기술을 도입하고 있어, 이것에 의해 사용한 수지공급 가능성이 높아져, 원료의 계속적인 확보가 보증됩니다.

자동차 및 EV의 경량화 요건

자동차 제조업체는 엄격한 평균 CO2 배출 목표 달성 및 EV 항속 거리 극대화를 위해 플라스틱 대체를 강화하고 있습니다. 테슬라의 기가 캐스팅 전략은 대형 알루미늄 주조 부품으로 인한 부품 수 감소 효과를 보이지만 주조 구조와 통합되는 사출 성형의 내부 및 외부 트림 수요를 확대하고 있습니다. 배터리 제조업체는 난연성 샌드위치 구조 벽을 채용한 열가소성 수지 하우징을 모색하고 있으며, 강재 대체품에 비해 차량당 최대 40kg의 경량화를 실현합니다. 이 전환은 Engel의 고전압 배터리 인클로저 프로토타입으로 대표됩니다. ISO 14040 라이프사이클 평가는 재료 선택에 대한 영향력을 증가시키고 복합 금속 부품보다 재생 가능한 수지를 선호합니다. 이러한 동향으로 폴리아미드, 폴리카보네이트, 재생 폴리프로필렌 등 엔지니어링 등급 폴리머 수요가 높아지고, 차량당 사용량 증가와 새로운 EV 플랫폼용 금형 수요의 지속으로 플라스틱 사출 성형 시장의 가치 기반이 확대되고 있습니다.

원유 연동에 의한 수지 가격의 변동성

지정학적 혼란에 원유 지표가 반응함에 따라 폴리에틸렌과 폴리프로필렌의 스팟 가격이 상승했습니다. 2025년에 도입된 미국 관세로 인해 일부 수지 등급의 착륙 비용이 10-15% 상승한 반면 중국에서 추정 500만t 규모공급 과잉이 아시아 지역의 가격을 밀어내고 지역간 결정 스프레드를 확대시켰습니다. 수지 판매업자는 전례 없는 불확실성을 지적하고 있으며, 가공업자의 82%가 가격 급등에 대비해 복수 조달처 전략을 추진 중입니다. 마진의 변동성은 장기 금형 투자를 억제하고 플라스틱 사출 성형 시장 전체에서 생산 능력 증강의 허들을 끌어올리는 것과 동시에, 가공업자를 헤지 수단이나 포뮬러 가격 계약으로 향하게 하고 있습니다.

부문 분석

폴리에틸렌은 2025년 플라스틱 사출 성형 시장에서 36.05%의 압도적 점유율을 획득했고 재생재 사용 의무화에 의해 재활용성의 우위성이 강화되기 때문에 2031년까지 연평균 복합 성장률(CAGR) 5.02%를 나타낼 전망입니다. 이 주도적 지위는 수지의 내약품성을 살린 얇은 포장, 캡·클로저 시스템, 신흥의 자동차용 연료전지 부품에 의해 지지되고 있습니다. 폴리프로필렌은 자동차 인테리어 트림, HVAC 하우징, 가전 부품 분야에서 높은 내열 변형 온도와 강성 중량비를 활용하여 약간의 차이로 계속됩니다. 아크릴로니트릴·부타디엔·스티렌(ABS)은 소비자용 전자기기 케이스로 틈새 시장을 유지하는 한편, 폴리스티렌은 규제 강화에 의해 일회용 칼라리 분야에서 구조적인 감소 경향에 있습니다.

탈중합 및 솔벤트 기반 정제가 가능한 고급 재활용 시설은 사용된 폴리에틸렌의 품질을 향상시키고 버진 수지를 직접 대체할 수 있어 가공업자의 스코프 3 배출량 감소에 기여하고 있습니다. 폴리카보네이트는 헤드 램프 렌즈나 투명 보호 실드로의 채용이 꾸준히 진행되어, 특정의 자동차 모델에서는 두꺼운 유리를 대신하는 얇은 유리 옵션으로서 채용되고 있습니다. 피마자유 유래의 바이오 베이스 폴리아미드는 고유의 난연성과 저탄소 강도에 의해 엔진 룸 부품에서의 채용이 주목받고 있습니다. 이러한 소재 수준의 전환은 플라스틱 사출 성형 시장의 다양화를 촉진하는 동시에 고객의 환경, 사회, 거버넌스(ESG) 목표 달성을 지원합니다.

플라스틱 사출 성형 보고서는 원재료 유형(폴리프로필렌, 아크릴로니트릴·부타디엔·스티렌, 폴리스티렌, 폴리에틸렌, 폴리염화비닐 등), 용도별(포장, 건축 및 건설, 소비재, 전자 기기, 자동차 및 운송, 의료, 기타 용도), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카).

지역별 분석

아시아태평양은 2025년에 플라스틱 사출 성형 시장의 34.10%를 차지했고 중국, 인도, 동남아시아에서 전자기기 및 자동차 생산의 확대에 따라 2031년까지 연평균 복합 성장률(CAGR) 5.24%를 나타낼 전망입니다. 정부의 장려책, 낮은 인건비, 하류의 조립공장에의 근접성이 생산 능력의 증강을 지원하고 있습니다. 일본에서는 80% 이상의 공장에서 디지털 트윈과 카본 실적 관리 툴을 도입하여 생산성과 지속가능성 향상을 도모하고 있습니다. 북미에서는 리쇼어링과 니어쇼어링이 진행 중이며 멕시코에서는 2023년 439억 달러의 외국 직접투자(FDI)를 획득했습니다. 이에 따라 자동차 내장 부품용 금형 수입과 턴키 셀 설치가 촉진되고 있습니다.

미국에서는 1조 4,000억 달러 규모의 재공업화 계획이 반도체, EV 배터리, 의료기기의 생산 능력을 뒷받침해 국내 수지 수요를 끌어올릴 전망입니다. 캐나다 온타리오 주에 있는 금형 제조 클러스터는 소비자를 위한 포장 프로그램을 위한 높은 캐비테이션 금형 공급을 계속하고 있지만 임금 프리미엄이 자동화 추진을 촉구하고 있습니다.

유럽의 컨버터는 2030년까지 PET 포장재의 재생재 함량 30% 달성을 의무화하는 PPWR 규제에 대응하기 위해 탈중합 처리 및 용매 기반 정제 플랜트에 대한 투자를 진행하고 있습니다. 독일의 엔지니어링 기술은 고급 차량용 다성분 성형을 지원하고 프랑스에서는 소비자의 환경 지향에 따른 바이오 화장품 포장의 확대가 진행되고 있습니다. 남미는 브라질의 자동차 수요에 의존하고 있으며, 현지 조달 규정에 따라 국내 플라스틱 부품 생산 증가가 촉진되고 있습니다.

중동 및 아프리카에서는 사우디아라비아의 폴리머 하류 투자와 현지 부품 생산 촉진을 목적으로 한 남아프리카의 금형 조성 제도에 의해 확대가 진행되고 있습니다. 이러한 다양한 지역 동향이 함께 플라스틱 사출 성형 시장의 지리적 확산이 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전자상거래의 급증 및 포장 수요의 견인

- 자동차 및 EV에서의 경량화 요건

- 일회용 의료용 일회용 제품에 대한 수요 증가

- 아시아태평양의 전자 기기 제조 산업화

- OEM에 의한 사출 성형 EV 배터리 하우징의 채용

- 시장 성장 억제요인

- 원유 가격 연동에 의한 수지 가격의 변동성

- 세계의 플라스틱 규제 강화

- 전전동식 고톤수 프레스기에 있어서 설비 투자와 기능 부족

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 원재료 유형별

- 폴리프로필렌

- 아크릴로니트릴 부타디엔 스티렌(ABS)

- 폴리스티렌

- 폴리에틸렌

- 폴리염화비닐(PVC)

- 폴리카보네이트

- 폴리아미드

- 기타 원재료

- 용도별

- 포장

- 건축 및 건설

- 소비재

- 전자기기

- 자동차 및 운송

- 헬스케어

- 기타 용도

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/순위 분석

- 기업 프로파일

- ALPLA

- Amcor PLC

- Antolin

- AptarGroup, Inc.

- BERICAP

- CVA Plastics

- EVCO Plastics

- FORVIA Faurecia

- HTI Plastics

- Husky Technologies

- IAC Group

- Magna International Inc.

- Marelli Holdings Co. Ltd

- Naber Plastics BV

- Quantum Plastics

- SCHAUENBURG Industrietechnik

- SEKISUI CHEMICAL CO., LTD.

- Silgan Holdings Inc.

- The Rodon Group

- TOYOTA BOSHOKU CORPORATION

제7장 시장 기회와 향후 전망

KTH 26.01.26The Plastics Injection Molding Market was valued at USD 157.13 million tons in 2025 and estimated to grow from USD 163.78 million tons in 2026 to reach USD 201.47 million tons by 2031, at a CAGR of 4.23% during the forecast period (2026-2031).

This sustained expansion underscores the technology's centrality to cost-effective, large-volume manufacturing in packaging, automotive, electronics and medical devices. E-commerce growth, accelerating electric-vehicle (EV) production and regulatory pushes for circularity collectively widen the application base of the plastics injection molding market, while energy-efficient all-electric machines and advanced material formulations help producers offset rising input costs. Asia-Pacific's growing electronics clusters, North American reshoring initiatives and Europe's first-mover stance on recyclability regulations all amplify regional opportunities. At the same time, volatile crude-oil-linked resin pricing and tightening global anti-plastic rules temper profit margins and compel investments in recycled feedstocks, digital quality control and end-of-life traceability systems.

Global Plastics Injection Molding Market Trends and Insights

Surge in E-commerce-Driven Packaging Demand

Explosive parcel volumes have heightened requirements for durable yet lightweight protective solutions, prompting brand owners to specify mono-material polyethylene and polypropylene packages that minimize material use without compromising strength. The EU Packaging and Packaging Waste Regulation (PPWR), effective 2025, mandates 30% recycled content in PET food packaging by 2030, accelerating redesign of tooling and process parameters to handle higher-recycled blends. U.S. Extended Producer Responsibility (EPR) fees across 14 states create an additional cost signal that rewards eco-modulated designs and favors converters with advanced resin reclamation lines. These converging mandates bolster volume growth in the plastics injection molding market, particularly in thin-wall container and closure segments where cycle-time reductions deliver material savings and higher throughput. Progressive molders are adopting in-mold labeling and digital watermarking to streamline sorting, increasing the likelihood of post-consumer resin availability and ensuring feedstock continuity.

Lightweighting Requirements in Automotive and EVs

Automotive OEMs have intensified plastics substitution to achieve stringent fleet-average CO2 targets and maximize EV range. Tesla's gigacasting strategy showcases how large aluminum castings reduce part counts, but it simultaneously expands demand for injection-molded interior and exterior trims that integrate with cast structures. Battery manufacturers are exploring thermoplastic housings with flame-retardant sandwich walls that cut up to 40 kg per vehicle compared with steel alternatives, a shift exemplified by Engel's high-voltage battery enclosure prototype. ISO 14040 life-cycle assessments increasingly influence material choices, favoring recyclable resins over multi-material metal assemblies. These trends elevate engineering-grade polymers such as polyamide, polycarbonate and recycled polypropylene, widening the value pool of the plastics injection molding market through higher content per vehicle and sustained tooling demand for new EV platforms.

Volatile Crude-Oil-Linked Resin Pricing

Polyethylene and polypropylene spot prices rose as crude benchmarks responded to geopolitical disruptions. U.S. tariffs introduced in 2025 raised landed costs of some resin grades by 10-15%, while Chinese oversupply, estimated at an additional 5 million tons of capacity, depressed Asian quotes and widened inter-regional arbitrage spreads. Resin distributors cite unprecedented uncertainty, with 82% of converters pursuing multisourcing strategies to guard against price spikes. Margin volatility discourages long-term tooling commitments, raising the hurdle rate for capacity additions across the plastics injection molding market and nudging processors toward hedging instruments and formula-pricing contracts.

Other drivers and restraints analyzed in the detailed report include:

- Growing Need for Single-Use Medical Disposables

- OEM Adoption of Injection-Molded EV Battery Housings

- Tightening Global Anti-Plastic Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene secured a commanding 36.05% share of the plastics injection molding market in 2025 and is on track for a 5.02% CAGR through 2031 as recycled-content mandates reinforce its recyclability advantage. This leadership is fueled by thin-wall packaging, cap-and-closure systems and emerging automotive fuel-cell components that capitalize on the resin's chemical resistance. Polypropylene follows closely in interior automotive trims, HVAC housings and appliance parts, leveraging high heat deflection and stiffness-to-weight ratios. Acrylonitrile butadiene styrene retains niche in consumer electronics casings, while polystyrene faces structural decline in single-use cutlery amid regulatory crackdowns.

Advanced recycling facilities capable of depolymerization and solvent-based purification are improving the quality of post-consumer polyethylene, enabling drop-in replacement for virgin resin and lowering scope-3 emissions for converters. Polycarbonate uptake advances steadily in headlamp lenses and transparent protective shields, with thin-gauge glazing options replacing heavier glass in certain automotive models. Bio-based polyamides produced from castor-bean oil are gaining interest in under-hood parts due to inherent flame retardancy and lower carbon intensity. These material-level shifts deepen the diversification of the plastics injection molding market while supporting clients' environmental, social and governance (ESG) objectives.

The Plastics Injection Molding Report is Segmented by Raw Material Type (Polypropylene, Acrylonitrile Butadiene Styrene, Polystyrene, Polyethylene, Polyvinyl Chloride, and More), Application (Packaging, Building and Construction, Consumer Goods, Electronics, Automotive and Transportation, Healthcare, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific held 34.10% of the plastics injection molding market in 2025 and is expanding at a 5.24% CAGR to 2031 as China, India, and Southeast Asia scale electronics and automotive output. Government incentives, lower labor costs, and proximity to downstream assembly plants underpin capacity additions. Japan is leveraging digital twins and carbon-footprint dashboards across more than 80% of factories to heighten productivity and sustainability. North America benefits from reshoring and nearshoring, with Mexico securing USD 43.9 billion in FDI during 2023 that spurs tooling imports and turnkey cell installations for automotive interiors.

The United States' USD 1.4 trillion reindustrialization plan supports semiconductor, EV battery and medical-device capacity that will boost domestic resin offtake. Canada's mold-making clusters in Ontario continue to supply high-cavitation tools for consumer-packaging programs, though wage premiums encourage higher degrees of automation.

European converters are investing in depolymerization and solvent-based purification plants to meet PPWR requirements for 30% recycled content in PET packaging by 2030. Germany's engineering prowess underpins advanced multi-component molding for premium vehicles, while France scales bio-based cosmetic packaging aligned with consumer eco-preferences. South America depends on Brazilian automotive demand, with localized content rules compelling higher domestic plastic part production.

The Middle East and Africa are expanding through Saudi Arabia's polymer downstream investments and South Africa's tooling grant scheme aimed at stimulating localized part production. These diverse regional dynamics collectively broaden the geographic footprint of the plastics injection molding market.

- ALPLA

- Amcor PLC

- Antolin

- AptarGroup, Inc.

- BERICAP

- CVA Plastics

- EVCO Plastics

- FORVIA Faurecia

- HTI Plastics

- Husky Technologies

- IAC Group

- Magna International Inc.

- Marelli Holdings Co. Ltd

- Naber Plastics BV

- Quantum Plastics

- SCHAUENBURG Industrietechnik

- SEKISUI CHEMICAL CO., LTD.

- Silgan Holdings Inc.

- The Rodon Group

- TOYOTA BOSHOKU CORPORATION

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-Commerce?Driven Packaging Demand

- 4.2.2 Lightweighting Requirements in Automotive and EVs

- 4.2.3 Growing Need for Single-Use Medical Disposables

- 4.2.4 Industrialisation in APAC Electronics Manufacturing

- 4.2.5 OEM Adoption of Injection-Molded EV Battery Housings

- 4.3 Market Restraints

- 4.3.1 Volatile Crude-Oil-Linked Resin Pricing

- 4.3.2 Tightening Global Anti-Plastic Regulations

- 4.3.3 Cap-Ex and Skills Gap for All-Electric High-Tonnage Presses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Raw Material Type

- 5.1.1 Polypropylene

- 5.1.2 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.3 Polystyrene

- 5.1.4 Polyethylene

- 5.1.5 Polyvinyl Chloride (PVC)

- 5.1.6 Polycarbonate

- 5.1.7 Polyamide

- 5.1.8 Other Raw Materials

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Building and Construction

- 5.2.3 Consumer Goods

- 5.2.4 Electronics

- 5.2.5 Automotive and Transportation

- 5.2.6 Healthcare

- 5.2.7 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ALPLA

- 6.4.2 Amcor PLC

- 6.4.3 Antolin

- 6.4.4 AptarGroup, Inc.

- 6.4.5 BERICAP

- 6.4.6 CVA Plastics

- 6.4.7 EVCO Plastics

- 6.4.8 FORVIA Faurecia

- 6.4.9 HTI Plastics

- 6.4.10 Husky Technologies

- 6.4.11 IAC Group

- 6.4.12 Magna International Inc.

- 6.4.13 Marelli Holdings Co. Ltd

- 6.4.14 Naber Plastics BV

- 6.4.15 Quantum Plastics

- 6.4.16 SCHAUENBURG Industrietechnik

- 6.4.17 SEKISUI CHEMICAL CO., LTD.

- 6.4.18 Silgan Holdings Inc.

- 6.4.19 The Rodon Group

- 6.4.20 TOYOTA BOSHOKU CORPORATION

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment