|

시장보고서

상품코드

1910911

섬유 브래그 그레이팅 센서 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Fiber Bragg Grating Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

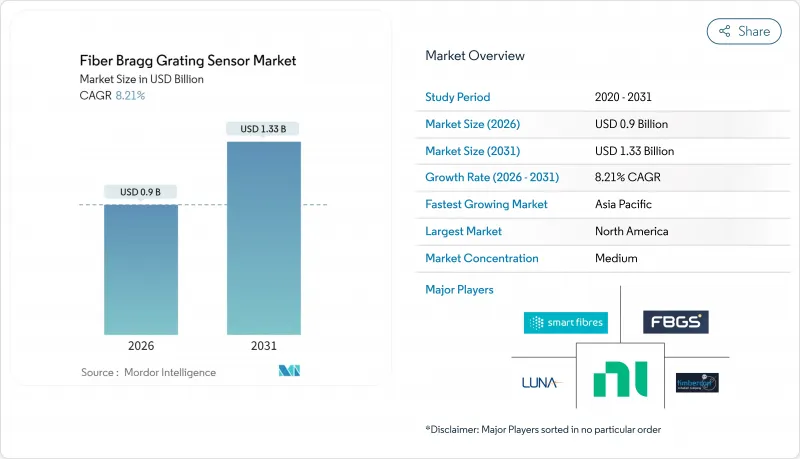

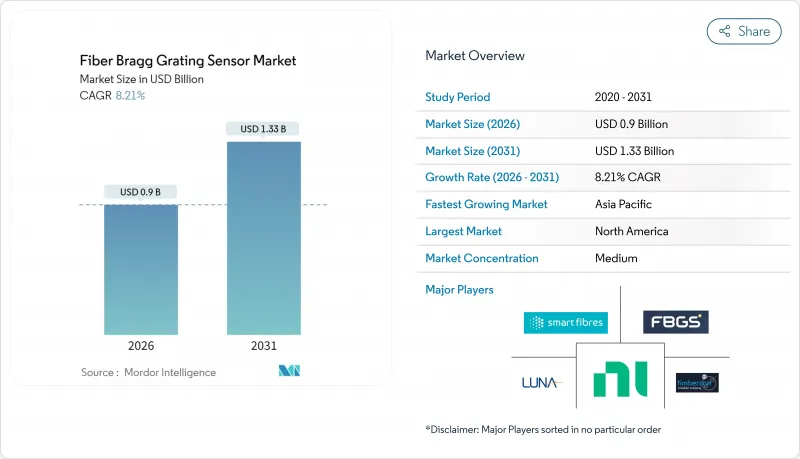

섬유 브래그 그레이팅 센서 시장은 2025년 8억 3,000만 달러에서 2026년 9억 달러로 성장하고 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 8.21%를 나타낼 전망입니다. 2031년까지 13억 3,000만 달러에 이를 것으로 예측됩니다.

구조 건전성 감시, 수소 파이프라인, 스마트 광업, 5G 백홀 인프라의 채용이 급증하고 있는 것이 이 꾸준한 성장 궤도의 기반이 되고 있습니다. 경쟁 차별화는 파장 고밀도 센서 네트워크, 다중 파라미터 측정 능력, 인공지능(AI) 기반 신호 처리에 중점을 둡니다. 인프라 투자 증가, 안전중시의 규제, 기존 전기식 게이지의 운용 한계가 더해져, 광센싱 기술이 유리하게 일하고 있습니다. 그러나 온도와 스트레인 사이의 교차 감도와 초기 설치 비용의 높이는 가격에 민감한 도입 환경에서 단기 보급을 계속 억제하고 있습니다.

세계의 섬유 브래그 그레이팅 센서 시장 동향 및 인사이트

실시간 구조 건전성 모니터링 수요 증가

노후화된 교량, 터널, 고층 빌딩은 현재 고밀도로 배치된 섬유 브래그 격자(FBG)에 의해 지속적으로 모니터링되고 있으며, 구조물이 파손되기 전에 피로 균열 및 하중 재분배 패턴을 드러냅니다. 2024년 프랜시스 스콧 키 브릿지 붕괴 사고를 겪고 미국에서는 교통량이 많은 회랑에서 지속적인 감시의 연방 지령이 가속되었습니다. 자릿수 전체에 따른 분산형 센싱은 완전한 변형 프로파일을 생성하여 초기 단계의 이상을 놓치기 쉬운 산재하는 전기 게이지를 대체합니다. 유럽에서도 비슷한 규제로 공공 자금을 통한 인프라 업데이트가 광 감지 도입과 연관되어 있으며, 섬유 브래그 그레이팅 센서 시장은 토목 자산에 대한 장기적인 수요가 예상됩니다.

수소 파이프라인 네트워크에 도입

유럽의 수소 백본 구상에서는 수소 취화의 영향을 받지 않는 누설 감지 시스템이 요구되고 섬유 브래그 격자(FBG)가 안전 기준으로 자리매김하고 있습니다. 음향 및 왜곡의 이중 모드 감지로 운영자는 미세 누설과 기계적 변형을 동시에 감지할 수 있으며, 이는 부식성 수소 환경 하에서 전기 시스템에서 실현할 수 없는 기능입니다. 독일의 H2-Netz가 신규 전송 라인용으로 책정한 사양은 북미 및 아시아태평양의 프로젝트가 추종하기 시작하고 있는 재현 가능한 템플릿이 되어, 에너지 수송 인프라에서의 섬유 브래그 그레이팅 센서 시장의 발자취를 확대하고 있습니다.

온도와 변형의 상호 감도

기계적 변형과 열적 영향을 분리하기 위해서는 여전히 높은 비용의 이중 격자 구성과 계산에 의한 보정이 필요하며, 항공우주·에너지 분야에서는 5-10%의 측정 불확도를 발생시킵니다. ±1%의 정확도를 요구하는 고객은 중복 센서 구성을 채택하지 않을 수 없으며, 프로젝트 예산을 밀어 올려 온도 변동이 심한 환경에서의 도입을 방해하고 있습니다. 이 기술적 과제로 고급 보정 설계가 가격 경쟁력을 얻기 전까지는 섬유 브래그 그레이팅 센서 시장의 확대가 일시적으로 억제될 전망입니다.

부문 분석

스트레인 센서는 2025년 섬유 브래그 그레이팅 센서 시장에 3억 1,000만 달러(37.78%의 수익 점유율)를 공헌해, 교량·항공기 날개·콘크리트 구조물 등 폭넓은 분야에서의 보급도를 뒷받침했습니다. 음향 센서는 절대액이야말로 작은 것, 분산형 음향 센싱이 경계 경비나 누설 검지로 보급됨에 따라 CAGR 9.12%를 나타내고 있습니다. 스트레인 디바이스는 주요 인프라 프로젝트의 기반이 되고 있는 반면, 음향 시스템은 고성장을 이루는 보완 기술이 됩니다.

단일 섬유에 스트레인과 온도 격자를 공존시키는 다중 파라미터 하이브리드 기술은 보상 오차를 줄이고 채널 수를 줄입니다. 유전 서비스 제공업체는 갱정 완성의 복잡화를 줄이기 위해 복합 센서를 적극적으로 채용하고 있으며, 전자 게이지가 작동하지 않는 갱내 환경에서도 섬유 브래그 그레이팅 센서 시장의 적용 범위가 확대되고 있습니다.

통신 등급 부품 공급과 검증된 계측 하드웨어에 의해 지원되는 주요 C 밴드 부문은 2025년에 약 3억 7,000만 달러 시장 규모를 창출했습니다. 네트워크 규모의 프로젝트에서는 사용 가능한 C 밴드 채널이 고갈되고 있으며, L 밴드로의 전환이 진행되고 있습니다. L 밴드는 9.32%라는 가장 빠른 CAGR을 기록했으며, 메가 프로젝트가 단일 섬유에서 수백 개의 감지 포인트를 요구함에 따라 L 밴드용 섬유 브래그 그레이팅 센서 시장 규모가 크게 확대될 것으로 예측됩니다.

첨단 인터로게이터는 현재 C 밴드와 L 밴드를 동시에 스캔할 수 있어 부품 비용과 채널 밀도를 양립시키는 혼합 아키텍처를 실현하고 있습니다. 연구 컨소시엄은 틈새 생체의료 및 수중 응용 분야를 위한 광대역 O-밴드 어레이의 테스트를 진행하고 있지만, 주류 파장에 비해 상업화는 여전히 제한적입니다.

지역별 분석

북미의 수익 주도는 교량의 중대 사고를 계기로 한 구조물 감시의 의무화에 기인합니다. 노후화된 강철 아치교에의 설치는 연방 보조금으로 지원되고, 미국 해군의 잠수함 선체 건전성 프로그램이 군사 수요를 확대하고 있습니다. 캐나다의 극단적인 온도 변동은 빙결 부하를 받기 쉬운 원격 송전선로에서 광 센서를 합리적인 선택으로 삼고 있습니다. 멕시코는 자동차 공장에서 파이버 어레이를 도입하여 예기치 않은 가동 중지 시간을 줄이고 지역 시장에 새로운 산업층이 추가되었습니다.

아시아태평양의 활황은 중국의 복수성에 걸친 고속철도의 전개에 현저하고, 각 고가교에는 수천의 그레이팅이 설치되어 회전 미끄럼이나 접합부의 변위를 검지하고 있습니다. 일본의 엄격한 내진 기준은 신칸센의 새로운 역에서 실시간 감시를 추진하고 있으며, 한국에서는 5G 간선에 센서를 통합하여 광섬유의 절단 개소를 수 미터 단위로 특정하고 있습니다. 인도의 스마트시티계획은 도로길 어깨에 분산형 음향센싱기술을 이용한 교통감시그리드의 파일럿 사업에 자금을 제공하여 대응 가능한 수요를 확대하고 있습니다.

유럽에서는 IEC 61757 등의 틀 안에서 수소·풍력·철도 프로젝트를 통일하는 표준화된 규제가 정비되고 있습니다. 독일의 H2 대응 파이프라인 기준에서는 음향 누설 감지가 디폴트로 규정되며, 영국 크라운 에스테이트는 고정식·부체식 풍력 자산에 대한 광학 모니터링을 의무화하고 있습니다. 남유럽에서는 부흥 자금을 지진대를 횡단하는 고속철도에 투입해, 터널 라이너의 변형 측정에 광학 어레이를 의무화하는 것으로, 지역의 섬유 브래그 그레이팅 센서 시장 전망을 지지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 실시간 구조 건전성 모니터링에 대한 수요 증가

- 수소 파이프라인 네트워크에서의 도입 상황

- 스마트광업 운영에 대한 투자 증가

- 5G 광 백홀 인프라 확장

- 고전압 직류(HVDC) 케이블에서의 이용 확대

- 상태 기반 항공기 정비에 대한 방위 분야의 중점

- 시장 성장 억제요인

- 온도와 변형에 대한 교차 감도

- 전기식 게이지와의 비교에 있어서 초기 설치 비용의 높이

- 초고속 이벤트에 있어서 동적 범위의 제한

- 숙련된 광섬유 기술자의 부족

- 업계 밸류체인 분석

- 규제 상황

- 기술 전망

- 거시경제 요인의 영향

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 온도 센서

- 변형률 센서

- 압력 센서

- 음향 센서

- 기타 유형

- 격자 파장 범위별

- C 밴드(1,530-1,565nm)

- L 밴드(1,565-1,625nm)

- O 밴드(1,260-1,360nm)

- 기타 격자 파장 범위

- 최종 사용자 산업별

- 통신

- 항공우주 및 방위

- 건설 및 인프라

- 에너지 및 전력

- 석유 및 가스

- 광업

- 기타 최종 사용자 산업

- 용도별

- 구조물 건강 모니터링

- 온도 모니터링

- 진동 및 음향 모니터링

- 압력 모니터링

- 하중 및 중량 모니터링

- 기타 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- FBGS International NV

- Smart Fibres Ltd

- Micron Optics Inc-Luna Innovations

- Timbercon Inc

- National Instruments Corporation

- Hottinger Bruel and Kjaer HBM Inc

- Broptics Technology Inc

- ITF Technologies Inc

- Advanced Optics Solutions GmbH

- Technica Optical Components LLC

- Opsens Inc

- TeraXion Inc

- FISO Technologies Inc

- Optromix Inc

- Shenzhen Fibersail Technology Co Ltd

- Neoptix Inc

- Lightwave Logic Inc

- Smart Sensing Solutions GmbH

- Blue Road Research

- Cinogy Technologies GmbH

제7장 시장 기회와 향후 전망

KTH 26.01.22The Fiber Bragg Grating Sensor market is expected to grow from USD 0.83 billion in 2025 to USD 0.9 billion in 2026 and is forecast to reach USD 1.33 billion by 2031 at 8.21% CAGR over 2026-2031.

The surging adoption of structural health monitoring, hydrogen pipelines, smart mining, and 5G backhaul infrastructure underpins this steady trajectory. Competitive differentiation centers on wavelength-dense sensor networks, multi-parameter measurement capabilities, and artificial intelligence-based signal processing. Rising infrastructure investments, safety-centric regulations, and the operational limits of traditional electrical gauges jointly favor optical sensing. Nevertheless, cross-sensitivity between temperature and strain, as well as higher upfront installation costs, continue to moderate near-term adoption in price-sensitive deployments.

Global Fiber Bragg Grating Sensor Market Trends and Insights

Growing Demand for Real-Time Structural Health Monitoring

Aging bridges, tunnels, and high-rise buildings are now monitored continuously with dense arrays of fiber Bragg gratings that reveal fatigue cracks and patterns of load redistribution before structural failure. The 2024 Francis Scott Key Bridge collapse accelerated federal mandates for continuous monitoring on high-traffic corridors in the United States. Distributed sensing along entire girders creates a complete strain profile, replacing scattered electrical gauges that overlook early-stage anomalies. Similar regulations in Europe tie public-funded infrastructure upgrades to the adoption of optical sensing, positioning the Fiber Bragg Grating Sensor market for long-term demand in civil assets.

Adoption in Hydrogen Pipeline Networks

Europe's Hydrogen Backbone initiative requires leak detection systems immune to hydrogen embrittlement, elevating fiber Bragg gratings as a safety standard. Dual-mode acoustic and strain detection enables operators to spot micro-leaks and mechanical deformation simultaneously, a capability that electrical systems cannot deliver in the corrosive hydrogen environment. Germany's H2-Netz specifications for new transmission lines create a replicable template that North American and Asia-Pacific projects are beginning to follow, widening the Fiber Bragg Grating Sensor market footprint in energy transport infrastructure.

Cross-Sensitivity to Temperature and Strain

Separating mechanical strain from thermal effects still necessitates costly dual-grating configurations or computational compensation that introduce 5-10% measurement uncertainty in aerospace and energy applications. Customers seeking +-1% accuracy often resort to redundant sensor schemes, which raises project budgets and hinders adoption in environments with wide thermal swings. This technical hurdle temporarily tempers the expansion of the Fiber Bragg Grating Sensor market until advanced compensation designs become price-competitive.

Other drivers and restraints analyzed in the detailed report include:

- Rising Investments in Smart Mining Operations

- Expansion of 5G Fiber Backhaul Infrastructure

- High Upfront Installation Cost versus Electrical Gauges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Strain sensors contributed USD 0.31 billion to the Fiber Bragg Grating Sensor market in 2025, retaining a 37.78% revenue share, which underscores their ubiquity across bridges, aircraft wings, and concrete structures. Acoustic variants, while smaller in absolute terms, show a 9.12% CAGR as distributed acoustic sensing gains traction in perimeter security and leak detection. Strain devices will continue to anchor flagship infrastructure projects, but acoustic systems provide a high-growth complement.

Multi-parameter hybrids that co-locate strain and temperature gratings on a single fiber are shrinking compensation errors and lowering channel counts. Oilfield service providers are increasingly favoring combined sensors to reduce wellbore completion complexity, thereby broadening the reach of the Fiber Bragg Grating Sensor market across downhole conditions where electronic gauges fail.

The dominant C-Band segment generated nearly USD 0.37 billion in 2025, driven by telecom-grade component availability and proven interrogation hardware. Network-scale projects exhaust available C-Band channels, driving migration to the L-Band, which is posting the fastest 9.32% CAGR. The Fiber Bragg Grating Sensor market size for L-Band devices is forecast to expand significantly as mega-projects demand hundreds of sensing points on a single fiber.

Advanced interrogators now sweep across C- and L-Bands simultaneously, enabling mixed architectures that balance component cost with channel density. Research consortia are testing broader O-Band arrays for niche biomedical and underwater applications, although commercialization remains modest compared to mainstream wavelengths.

The Fiber Bragg Grating Sensor Market Report is Segmented by Type (Temperature Sensor, Strain Sensor, and More), Grating Wavelength Range (C-Band, L-Band, and More), End-User Industry (Telecommunication, Aerospace and Defense, and More), Application (Structural Health Monitoring, Temperature Monitoring, Vibration and Acoustic Monitoring, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North American revenue leadership stems from mandated structural monitoring after catastrophic bridge failures. Federal grants subsidize installation on aging steel arches, and the U.S. Navy's submarine hull integrity program extends military demand. Canada's extreme temperature swings make optical sensors a logical choice for remote transmission lines prone to ice loading. Mexico adopts fiber arrays in automotive factories to reduce unplanned downtime, adding a nascent industrial layer to the regional Fiber Bragg Grating Sensor market.

Asia-Pacific's dynamism is evident in China's multi-province high-speed rail rollout, with each viaduct equipped with thousands of gratings to detect rotational slip and joint displacement. Japan's stringent seismic codes drive real-time monitoring on new Shinkansen stations, while Korea integrates sensors into 5G trunk lines to localize fiber cuts within meters. India's smart-city program funds pilot traffic-monitoring grids using distributed acoustic sensing on roadway shoulders, thereby expanding the addressable demand.

Europe benefits from standardized regulations that align hydrogen, wind, and rail projects under frameworks like IEC 61757. Germany's H2-Ready pipeline criteria specify acoustic leak detection by default, and the United Kingdom's Crown Estate requires optical monitoring on fixed and floating wind assets. Southern Europe channels recovery funds into high-speed rail that crosses seismic zones, mandating optical arrays for tunnel liner strain measurement, buttressing the regional Fiber Bragg Grating Sensor market outlook.

- FBGS International NV

- Smart Fibres Ltd

- Micron Optics Inc - Luna Innovations

- Timbercon Inc

- National Instruments Corporation

- Hottinger Bruel and Kjaer HBM Inc

- Broptics Technology Inc

- ITF Technologies Inc

- Advanced Optics Solutions GmbH

- Technica Optical Components LLC

- Opsens Inc

- TeraXion Inc

- FISO Technologies Inc

- Optromix Inc

- Shenzhen Fibersail Technology Co Ltd

- Neoptix Inc

- Lightwave Logic Inc

- Smart Sensing Solutions GmbH

- Blue Road Research

- Cinogy Technologies GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Real-Time Structural Health Monitoring

- 4.2.2 Adoption in Hydrogen Pipeline Networks

- 4.2.3 Rising Investments in Smart Mining Operations

- 4.2.4 Expansion of 5G Fiber Backhaul Infrastructure

- 4.2.5 Increasing Use in High-Voltage Direct Current (HVDC) Cables

- 4.2.6 Defense Focus on Condition-Based Aircraft Maintenance

- 4.3 Market Restraints

- 4.3.1 Cross-Sensitivity to Temperature and Strain

- 4.3.2 High Upfront Installation Cost versus Electrical Gauges

- 4.3.3 Limited Dynamic Range in Ultra-Fast Events

- 4.3.4 Scarcity of Skilled Fiber-Optic Technicians

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Temperature Sensor

- 5.1.2 Strain Sensor

- 5.1.3 Pressure Sensor

- 5.1.4 Acoustic Sensor

- 5.1.5 Other Types

- 5.2 By Grating Wavelength Range

- 5.2.1 C-Band (1530-1565 nm)

- 5.2.2 L-Band (1565-1625 nm)

- 5.2.3 O-Band (1260-1360 nm)

- 5.2.4 Other Grating Wavelength Ranges

- 5.3 By End-User Industry

- 5.3.1 Telecommunication

- 5.3.2 Aerospace and Defense

- 5.3.3 Construction and Infrastructure

- 5.3.4 Energy and Power

- 5.3.5 Oil and Gas

- 5.3.6 Mining

- 5.3.7 Other End-User Industries

- 5.4 By Application

- 5.4.1 Structural Health Monitoring

- 5.4.2 Temperature Monitoring

- 5.4.3 Vibration and Acoustic Monitoring

- 5.4.4 Pressure Monitoring

- 5.4.5 Load and Weight Monitoring

- 5.4.6 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 FBGS International NV

- 6.4.2 Smart Fibres Ltd

- 6.4.3 Micron Optics Inc - Luna Innovations

- 6.4.4 Timbercon Inc

- 6.4.5 National Instruments Corporation

- 6.4.6 Hottinger Bruel and Kjaer HBM Inc

- 6.4.7 Broptics Technology Inc

- 6.4.8 ITF Technologies Inc

- 6.4.9 Advanced Optics Solutions GmbH

- 6.4.10 Technica Optical Components LLC

- 6.4.11 Opsens Inc

- 6.4.12 TeraXion Inc

- 6.4.13 FISO Technologies Inc

- 6.4.14 Optromix Inc

- 6.4.15 Shenzhen Fibersail Technology Co Ltd

- 6.4.16 Neoptix Inc

- 6.4.17 Lightwave Logic Inc

- 6.4.18 Smart Sensing Solutions GmbH

- 6.4.19 Blue Road Research

- 6.4.20 Cinogy Technologies GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment