|

시장보고서

상품코드

1910933

프로테이나제 K - 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Proteinase K - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

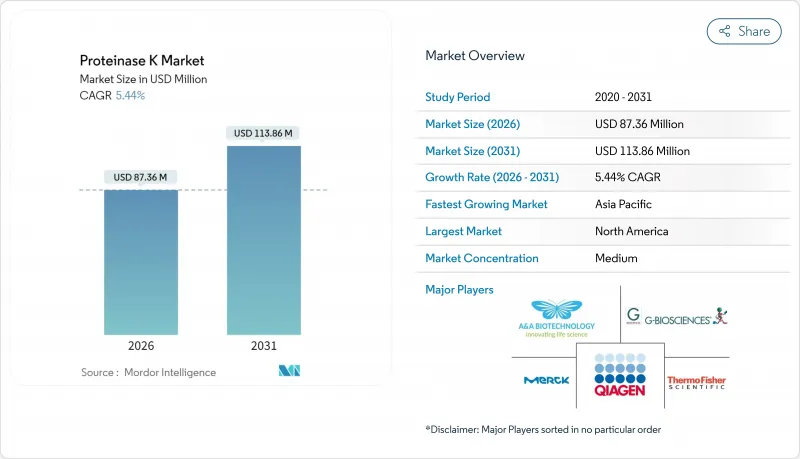

프로테이나제 K 시장은 2025년 8,286만 달러에서 2026년 8,736만 달러로 성장하고, 2026년에서 2031년까지 연평균 복합 성장률(CAGR) 5.44%를 나타낼 전망입니다. 2031년까지 1억 1,386만 달러에 이를 것으로 예측됩니다.

견고한 분자진단 파이프라인, 확대되는 법의학 DNA 프로그램, 재조합 제조로의 전환이 수요 가속을 지원하는 한편, 정밀의료 및 환경 중시의 eDNA 모니터링에 대한 투자가 추가 성장 경로를 제공합니다. 동결건조품은 상온 운송을 견디기 위해 여전히 주류이지만, 원활한 자동화가 필요한 포인트 오브 케어 워크플로우에서는 즉시 사용 가능한 액체 제품이 주목을 받고 있습니다. 또, 공급망이 새로운 규제 감시에 대응하는 동물 유래 성분을 포함하지 않는 원료를 요구하는 움직임으로부터, 재조합 프로테이나제 K도 진전하고 있습니다. 북미가 수익면에서 주도권을 유지하는 한편, 아시아태평양에서는 정부가 바이오프로세싱 파크나 정밀 진단 능력에 대한 자금 투입을 진행함으로써 가장 급속한 확대를 기록하고 있습니다.

세계의 프로테이나제 K 시장 동향과 인사이트

확대되는 분자진단 파이프라인

정밀의료 프로그램의 진전에 의해 검사 메뉴는 감염증 영역을 넘어 확대해, 검사 기관은 2020년 이전의 기준치를 40% 웃도는 핵산 처리 능력의 유지를 강요되고 있습니다. 다중 PCR 및 디지털 PCR 플랫폼의 보급으로 고객은 뉴클레아제 프리 로트와 종합적인 품질 데이터를 제공하는 프로테이나제 K 공급업체에 중점을 두어 QIAGEN과 뉴잉글랜드 바이오랩의 기존 우위를 강화하고 있습니다.

COVID 시대의 DNA/RNA 추출 키트 급증

유행기간 동안 추출을 자동화한 실험실에서는 시료 소화에 프로테이나제 K를 필요로 하는 고용량 시스템을 유지하고 있으며, 호흡기 검사가 정상화된 후에도 주문량은 높은 수준을 유지하고 있습니다. 동결건조 RT-LAMP 키트는 상온 수송의 틈새 시장을 개척하여 신속한 재구성에 적합한 동결건조 대응 효소를 공급하는 제조업체에 이익을 가져오고 있습니다.

콜드체인 중단시 효소 활성 저하

단백질 분해 효소는 지속적인 열에 노출되면 촉매 효율이 떨어집니다. 브로멜라인 연구는 27℃에서 1개월 후에 활성이 90% 저하되는 것으로 나타났으며, 유통 도중의 프로테이나제 K에도 유사한 리스크가 존재하는 것을 뒷받침하고 있습니다. 공급업체는 트레할로스와 같은 동결보호제를 배합함으로써 대응하고 있지만, 안정성이 높은 제제의 도입은 비용 증가로 이어져 자원의 제한된 환경에서의 보급을 방해하고 있습니다.

부문 분석

천연 유래 프로테이나제 K가 최대의 점유율을 유지하고 있지만, 규제 당국이 동물 유래가 아닌 원료 조달과 일관된 당쇄 구조를 중시하는 가운데, 재조합형은 CAGR 6.47%를 나타낼 것으로 전망되고 있습니다. 재조합형 프로테이나제 K 시장 규모는 대폭 확대될 것으로 예측되며, 미생물 숙주를 이용한 제조법에서는 천연 효소 발효법에 비해 1.8배의 활성 향상이 실현되고 있습니다. 기존 제조업체는 확장성을 강조하는 한편, 신흥 기업은 정밀 발효 플랫폼을 활용해, 내열성을 높이는 커스텀 변이를 도입하고 있습니다. 천연형은 카탈로그 가격이 재조합형보다 최대 25% 저렴하기 때문에 교육병원이나 미생물학 부문에서의 대량 판매가 보장되며, 학술연구소용으로는 여전히 수요가 있습니다.

시장 차별화는 순도, 엔도톡신 수준, 뉴클레아제 오염의 검증된 부재가 열쇠입니다. 초고순도 등급을 판매하는 공급업체는 임상 진단이 엄격한 GMP 문서화를 요구하는 경우 30-40%의 프리미엄 가격을 설정합니다. 프로테이나제 K 시장은 단일 청소년 생물반응기를 통합하는 재조합 개발자의 혜택을 누리고 있습니다. 이렇게 하면 배치 간 오염 위험이 줄어들고 전환 시간이 단축되므로 급증하는 검사 수요에 대응하는 고객에게 배달주기가 가속화됩니다.

2025년에는 동결건조 분말이 60.52%의 점유율을 차지했습니다. 이는 상온에서 최대 3년간 안정성을 유지하는 특성 때문이며, 조달 사이클이 부정기인 집중 검사 거점에 있어서 중요한 이점입니다(LabMedica). 그러나 병원이 카트리지식 PCR 장비를 도입함에 따라 사전 분주 시약 블리스터가 훈련을 단순화하고 턴 어라운드를 가속화하기 때문에 즉각적인 액체 수요가 증가하고 있습니다. 액체 제형은 프로테이나제 K 시장에서 증가하는 경향이 있습니다. 글리세롤과 소르비톨을 이용한 안정화 완충액은 4℃에서 6개월 후에도 90% 이상의 활성을 유지하기 때문에 임상 화학 검사실에서 일반적인 냉장 보관 조건을 충족하기 때문입니다.

자동 핵산 워크스테이션에서는 정확한 피펫팅을 보장하기 위해 점도 범위 지정이 증가하고 있습니다. 이것에 수반해, 제조업체는 발포 억제 효과도 아울러 가지는 첨가제 블렌드에 의해 액체의 점도를 미조정하고 있습니다. 동결건조 적합성을 유지하는 하이브리드형 「동결건조 대응 액체」는 브릿지 제품으로서 기능하고 OEM 검사 키트 개발자가 설계 사이클의 후반 단계에서 분말 제제와 최종 충전 액체의 선택을 가능하게 합니다(ThermoFisher사).

세계의 프로테이나제 K 시장은 제품 유형(천연 프로테이나제 K 및 재조합 프로테이나제 K), 형태(동결건조 분말 및 액체 용액), 용도(DNA/RNA 추출·정제, 인시츄 하이브리드화 등), 최종 사용자(바이오테크놀러지·제약 기업 등), 지역(북미, 유럽 등)에 의해 세분화되어 있습니다. 위 부문 시장 규모는(백만 달러)로 표시됩니다.

지역별 분석

아시아태평양은 정부의 높은 처리량 시퀀싱 거점과 국내 백신 제조 시설의 조성으로 2031년까지 연평균 복합 성장률(CAGR) 7.14%라는 가장 급격한 확대를 기록할 전망입니다. 한국의 생명과학 전략에는 머크사의 3억 유로 규모의 시설이 포함되어 있어 지역용 바이오프로세싱 효소를 공급함으로써 의약품 품질 관리 워크플로우에 있어서 프로테이나제 K 시장 수요를 확대하고 있습니다. 중국과 인도도 마찬가지로 바이오 의약품 생산 능력을 확대하고 있지만, 콜드체인의 과제에 직면하고 있으며, 이것이 상온 안정 제제의 연구를 촉진. 현지 진단 키트 기업과 다국적 시약 공급업체간의 제휴를 촉구하고 있습니다.

북미는 확립된 생명공학 클러스터, 국립위생연구소(NIH)의 자금 제공, 검증된 시약을 필수로 하는 견고한 법의학 DNA 인프라를 통해 2025년 매출의 33.11%를 차지하여 주도권을 유지했습니다. 병원 네트워크에서의 자동 추출 로봇 기술과 민간계보·소비자 유전체 해석 서비스의 조합이 높은 기준선 수요를 지지하고 있습니다. 규제의 엄격화로 ISO-13485 인증 취득 프로테이나제 K 로트에 대한 수요가 높아져 프리미엄 가격대가 유지되고 있습니다.

유럽은 이어 확립된 제약 제조와 선진 차세대 시퀀싱(NGS) 및 마이크로바이옴 연구를 주도하는 대학 컨소시엄과의 균형을 유지하고 있습니다. 호라이즌과 유럽 보조금은 많은 양의 효소가 필요한 국경을 넘어 생물 다양성과 고대 DNA 연구를 지원합니다. 그러나 동물 유래 시약에 대한 이 지역의 신중한 자세는 재조합 변이체의 채용을 촉진하고 프로테이나제 K 시장에서 공급자 포트폴리오를 재구성하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 분자진단 파이프라인 확대

- COVID-19 시대에 있어서 DNA/RNA 추출 키트 수요 급증

- 유전체 워크플로우에 대한 바이오제약 R&D 지출

- 법의학·범죄학 분야에서의 응용 확대

- PoC(Point-of-Care) 검사용 소형 동결 건조 포맷

- 생물다양성 평가를 위한 eDNA 모니터링

- 시장 성장 억제요인

- 콜드체인의 단절에 의한 효소 활성의 저하

- 동물 유래 원료공급 변동성

- 대체가 되는 설계 프로테이나제의 출현

- 동물 유래 효소에 대한 규제 동향

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액 기준, 2020-2030년)

- 제품 유형별

- 천연 프로테이나제 K

- 재조합 프로테이나제 K

- 형태별

- 동결건조 분말

- 액상 용액

- 용도별

- DNA/RNA 추출 및 정제

- In-Situ Hybridisation

- 차세대 시퀀싱(NGS) 라이브러리 준비

- 진단 검사 불활성화

- 기타

- 최종 사용자별

- 바이오테크놀러지 및 제약기업

- 학술 및 연구 기관

- 임상 진단 실험실

- 법의학 실험실

- 식품 검사 실험실

- 환경 검사 시설

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- QIAGEN NV

- Merck KGaA(Sigma-Aldrich)

- Thermo Fisher Scientific Inc.

- Promega Corporation

- New England Biolabs Inc.

- Takara Bio Inc.

- F. Hoffmann-La Roche AG

- Agilent Technologies Inc.

- Bio-Rad Laboratories Inc.

- Macherey-Nagel GmbH

- GenScript Biotech Corp.

- Enzymatics Inc.

- Worthington Biochemical Corp.

- Codexis Inc.

- MP Biomedicals

- Fujifilm Wako Pure Chemical Corp.

- Bioline(Meridian Bioscience)

- A&A Biotechnology

- Nordmark Pharma GmbH

- VWR International LLC

제7장 시장 기회와 향후 전망

KTH 26.01.26The Proteinase K market is expected to grow from USD 82.86 million in 2025 to USD 87.36 million in 2026 and is forecast to reach USD 113.86 million by 2031 at 5.44% CAGR over 2026-2031.

Robust molecular diagnostics pipelines, expanding forensic DNA programs, and the shift toward recombinant manufacturing underpin demand acceleration, while investments in precision medicine and environmentally focused eDNA monitoring provide additional growth avenues. Lyophilized formats remain dominant because they withstand room-temperature shipping, yet ready-to-use liquids are gaining traction in point-of-care workflows that require seamless automation. Recombinant Proteinase K is also progressing because supply chains seek animal-free inputs that satisfy emerging regulatory scrutiny. North America sustains revenue leadership, but Asia-Pacific records the fastest expansion as governments channel funding into bioprocessing parks and precision-diagnostics capacities.

Global Proteinase K Market Trends and Insights

Expanding Molecular Diagnostics Pipelines

Precision-medicine programs have broadened testing menus beyond infectious disease, compelling laboratories to maintain nucleic-acid throughput that exceeds pre-2020 baselines by 40%. As multiplex PCR and digital PCR platforms multiply, customers favor Proteinase K suppliers offering nuclease-free lots and exhaustive quality files, which strengthens incumbent positions held by QIAGEN and New England Biolabs.

Surge in COVID-Era DNA/RNA Extraction Kits

Laboratories that automated extraction during the pandemic retain high-capacity systems that rely on Proteinase K for sample digestion, keeping order volumes elevated even after respiratory testing normalised. Lyophilised RT-LAMP kits have opened room-temperature shipping niches, rewarding manufacturers that supply lyo-ready enzymes tailored to rapid reconstitution.

Enzyme Activity Loss in Cold-Chain Gaps

Proteolytic enzymes lose catalytic efficiency when exposed to sustained heat. Bromelain studies illustrate a 90% activity drop at 27 °C after one month, underscoring similar threats for Proteinase K during distribution lapses. Suppliers counter by embedding trehalose and other lyoprotectants, yet implementing stable formulations increases cost and limits adoption in low-resource settings.

Other drivers and restraints analyzed in the detailed report include:

- Biopharma R&D Spending on Genomic Workflows

- Growth in Forensic & Criminology Applications

- Animal-Origin Raw-Material Supply Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural Proteinase K retains the largest share, yet recombinant formats are slated for a 6.47% CAGR as regulators highlight animal-free sourcing and consistent glycosylation patterns. The Proteinase K market size for recombinant variants is projected to widen meaningfully, with microbial hosts delivering 1.8-fold activity improvements over native enzyme fermentations. Established producers emphasize scalability, while start-ups leverage precision-fermentation platforms to introduce custom mutations that raise thermal tolerance. Natural variants still appeal to academic labs because catalog prices remain up to 25% lower than recombinant equivalents, ensuring volume sales across teaching hospitals and microbiology departments.

Market differentiation pivots on purity, endotoxin levels, and validated absence of nuclease contamination. Suppliers marketing "ultrapure" grades command premiums of 30-40% where clinical diagnostics stipulate stringent GMP documentation. The Proteinase K market benefits from recombinant developers who integrate single-use bioreactors that reduce cross-batch contamination risks and compress changeover times, thereby accelerating fulfillment cycles to customers engaged in surge testing scenarios.

Lyophilised powder provides 60.52% share in 2025 because it remains stable for up to three years at ambient temperature, a key advantage for centralized testing hubs with intermittent procurement cycles LabMedica. However, demand for ready-dispense liquids is advancing as hospitals deploy cartridge-based PCR instruments where pre-dosed reagent blisters simplify training and accelerate turnaround. Liquid formulations represent a rising fraction of the Proteinase K market as stability buffers using glycerol and sorbitol retain >90% activity after six months at 4 °C, satisfying cold-room storage common in clinical chemistry labs.

Automated nucleic-acid workstations increasingly specify viscosity windows to guarantee accurate pipetting; consequently, producers fine-tune liquid viscosity through excipient blends that also mitigate foaming. Hybrid "lyo-ready liquids" that retain lyophilization compatibility offer a bridge product, enabling OEM test-kit developers to decide between powder or final-fill liquid late in the design cycle ThermoFisher.

Global Proteinase K Market is Segmented by Product Type (Natural Proteinase K and Recombinant Proteinase K), by Form (Lyophilised Powder and Liquid Solution), by Application (DNA/RNA Extraction & Purification, In-Situ Hybridisation and More), by End User (Biotechnology & Pharmaceutical Companies and More) and Geography (North America, Europe, and More). The Value is Provided in (USD Million) for the Above Segments.

Geography Analysis

Asia-Pacific records the steepest expansion at 7.14% CAGR through 2031 as governments subsidize high-throughput sequencing hubs and domestic vaccine manufacturing campuses. South Korea's life-science roadmap includes a EUR 300 million Merck facility that will supply regional bioprocessing enzymes, amplifying Proteinase K market demand in pharmaceutical QC workflows. China and India likewise scale biologics capacity, yet face cold-chain gaps that stimulate research into room-temperature-stable formulations, prompting partnerships between local diagnostic kit firms and multinational reagent suppliers.

North America maintains leadership with 33.11% 2025 revenue due to entrenched biotechnology clusters, National Institutes of Health funding, and a robust forensic DNA infrastructure that mandates validated reagents. Automated extraction robotics in hospital networks, combined with private ancestry and consumer genomics services, anchor high baseline volumes. Regulatory stringency drives users toward ISO-13485 certified Proteinase K lots, sustaining premium pricing tiers.

Europe follows closely, balancing established pharma manufacturing with university consortia that spearhead advanced NGS and microbiome programs. Horizon Europe grants finance cross-border biodiversity and ancient DNA studies that necessitate large enzyme quantities. Nevertheless, the bloc's cautious stance on animal-derived reagents pushes recombinant variant adoption, reshaping supplier portfolios within the Proteinase K market.

- QIAGEN

- Merck

- Thermo Fisher Scientific

- Promega

- New England Biolabs

- Takara Bio

- Roche

- Agilent Technologies

- Bio-Rad Laboratories

- Macherey-Nagel GmbH

- GenScript Biotech Corp.

- Enzymatics Inc.

- Worthington Biochemical Corp.

- Codexis

- MP Biomedicals

- Fujifilm Wako Pure Chemical Corp.

- Bioline (Meridian Bioscience)

- A&A Biotechnology

- Nordmark Pharma GmbH

- VWR International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding molecular diagnostics pipelines

- 4.2.2 Surge in COVID-era DNA/RNA extraction kits

- 4.2.3 Biopharma R&D spending on genomic workflows

- 4.2.4 Growth in forensic & criminology applications

- 4.2.5 Miniaturised lyophilised formats for PoC tests

- 4.2.6 eDNA monitoring for biodiversity assessments

- 4.3 Market Restraints

- 4.3.1 Enzyme activity loss in cold-chain gaps

- 4.3.2 Animal-origin raw-material supply volatility

- 4.3.3 Emergence of alternate engineered proteases

- 4.3.4 Regulatory moves against animal-derived enzymes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, 2020-2030)

- 5.1 By Product Type

- 5.1.1 Natural Proteinase K

- 5.1.2 Recombinant Proteinase K

- 5.2 By Form

- 5.2.1 Lyophilised Powder

- 5.2.2 Liquid Solution

- 5.3 By Application

- 5.3.1 DNA/RNA Extraction & Purification

- 5.3.2 In-Situ Hybridisation

- 5.3.3 NGS Library Preparation

- 5.3.4 Diagnostic Assay Deactivation

- 5.3.5 Others

- 5.4 By End User

- 5.4.1 Biotechnology & Pharmaceutical Companies

- 5.4.2 Academic & Research Institutes

- 5.4.3 Clinical Diagnostics Laboratories

- 5.4.4 Forensic Laboratories

- 5.4.5 Food Testing Laboratories

- 5.4.6 Environmental Testing Facilities

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 QIAGEN N.V.

- 6.3.2 Merck KGaA (Sigma-Aldrich)

- 6.3.3 Thermo Fisher Scientific Inc.

- 6.3.4 Promega Corporation

- 6.3.5 New England Biolabs Inc.

- 6.3.6 Takara Bio Inc.

- 6.3.7 F. Hoffmann-La Roche AG

- 6.3.8 Agilent Technologies Inc.

- 6.3.9 Bio-Rad Laboratories Inc.

- 6.3.10 Macherey-Nagel GmbH

- 6.3.11 GenScript Biotech Corp.

- 6.3.12 Enzymatics Inc.

- 6.3.13 Worthington Biochemical Corp.

- 6.3.14 Codexis Inc.

- 6.3.15 MP Biomedicals

- 6.3.16 Fujifilm Wako Pure Chemical Corp.

- 6.3.17 Bioline (Meridian Bioscience)

- 6.3.18 A&A Biotechnology

- 6.3.19 Nordmark Pharma GmbH

- 6.3.20 VWR International LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment