|

시장보고서

상품코드

1910944

레이저 마킹 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Laser Marking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

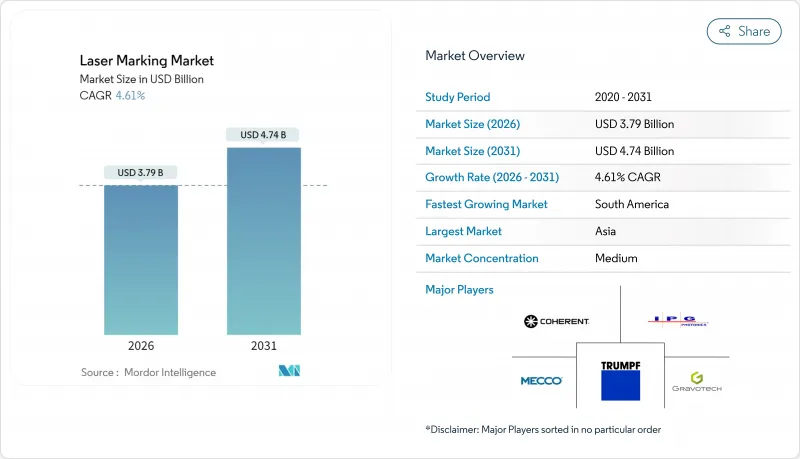

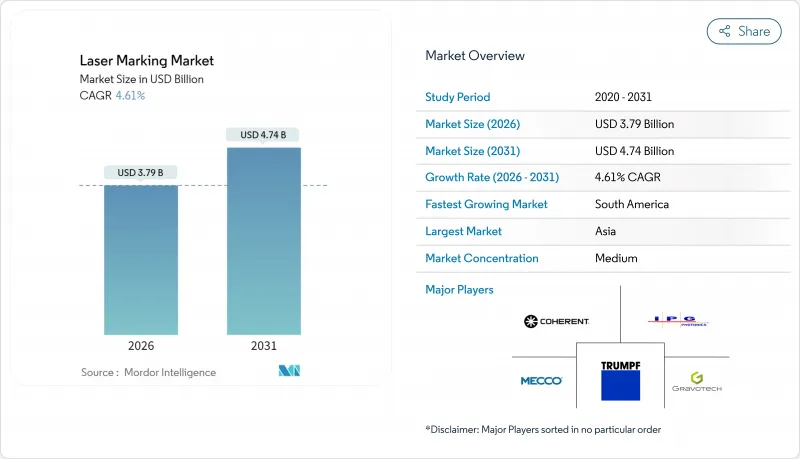

레이저 마킹 시장은 2025년 36억 2,000만 달러에서 2026년에는 37억 9,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 4.61%로 성장을 지속하여 2031년까지 47억 4,000만 달러에 달할 것으로 예측되고 있습니다.

성장의 기반은 영구적인 기기 식별을 의무화하는 세계 규제, 전기자동차 배터리 생산에서의 수요 증가, 소형화 전자기기 및 지속가능한 포장 분야에서의 정확도 요구 증가에 있습니다. 아시아에서는 국내 공급업체에 의한 진입 비용 절감에 의해 설치 대수면에서 계속 우세하지만, 북미와 유럽에서는 서비스 주도의 비즈니스 모델이 기세를 늘리고 있습니다. 중국의 파이버 레이저 제조업체의 가격 압력으로 하드웨어 이익률은 압박되고 있지만, 소프트웨어 및 예측 서비스는 수익성을 유지하고 있습니다. 항공우주 복합재, 보석품 홀마크, 산업 자동화에서의 새로운 이용 사례가 고객 기반을 확대하는 한편, 높은 자본 요건이 일부 소규모 제조업체를 제한하고 있습니다.

세계의 레이저 마킹 시장의 동향 및 인사이트

의료기기의 UDI(고유 장치 식별) 및 추적성 규제의 의무화는 영구 마킹의 도입을 촉진

미국 FDA 및 EU 의료기기규정(MDR)에 의한 엄격한 UDI(의료기기 식별) 프레임워크의 구축은 영구적이고 대비 효과가 높은 기기 코드를 법적 요건으로 삼았습니다. 병원에서는 장비를 반복적으로 멸균하기 때문에 마킹은 마모, 화학제품, 열을 견뎌야 합니다. 파이버 레이저 및 UV 레이저 시스템은 티타늄 임플란트, 폴리머 카테터 및 세라믹 부품에서 이러한 내구성 요구사항을 충족합니다. 또한 제조 실행 시스템에 직접 연결하면 컴플라이언스 감사가 단순화됩니다. 의약품 직렬화 규정에 따라 수요가 증가하고 소모품 없이 복잡한 2D 매트릭스를 인쇄하는 레이저 시스템에 대한 라인 통합 수요가 전반적으로 증가하고 있습니다. 마킹 하드웨어와 검증 소프트웨어를 결합하는 공급업체는 고객의 인증주기를 단축하고 리콜 위험을 줄입니다.

EV 배터리 생산 급증으로 비접촉 마킹 수요 가속

기가팩토리에서는 현재 리콜 및 리사이클 관리를 위해 각 셀, 모듈, 팩에 고유 코드를 각인하고 있습니다. 레이저 기술은 민감한 하우징과 접촉하지 않고 라인 속도로 식별을 수행하여 미립자 오염과 기계적 스트레스를 방지합니다. 파이버 레이저는 알루미늄 인클로저를 표시하고 UV 빔은 폴리머 분리기와 플렉서블 회로에 코드를 각인합니다. 중국, 한국, 미국에서는 시간당 수천 점의 마킹이 가능한 고속 비전 가이드식 유닛에 대한 수요가 급증하고 있습니다. 배터리 라인 인테그레이터는 용접 및 검사 스테이션과 병행하여 추적성 모듈을 패키징하고 엔드 투 엔드 프로세스 시각화를 실현하는 경우가 늘고 있습니다.

신흥 시장에서 중소기업 도입의 장벽이 되는 고액의 설비 투자

비전과 IoT 연결을 통합하는 산업용 등급 시스템은 150,000달러를 초과하는 가격 설정이 일반적이며 중남미와 아프리카 규모의 작은 제조업체의 현금 흐름 능력을 초과합니다. 통화 변동이 수입 비용을 밀어 올리는 반면 현지 대출 금리가 추가 부담을 가하고 있습니다. 휴대형 저비용 파이버 유닛은 도입 가격을 억제하지만, 자동차나 의료 라인에서 요구되는 정밀도나 가동 시간의 보증에는 부족합니다. 임대 및 마크별 과금 계약이 보급되고 있지만, 타사의 서비스 네트워크가 성숙할 때까지 도입은 완만한 페이스로 진행될 전망입니다.

부문 분석

2025년 시점에서 파이버 레이저는 매출의 61.95%를 차지하였으며, 신뢰성, 높은 전원 효율, 그리고 대부분의 금속을 고속으로 마킹할 수 있는 능력을 반영하고 있습니다. 자동차 파워트레인 부품, 수술 기구, 항공우주 패스너는 가혹한 사용 환경에도 견딜 수 있는 선명한 각인을 위해 파이버 빔에 의존합니다. 레이저 마킹 시장에서의 파이버 시스템 부문의 규모는 아시아와 유럽의 인더스트리 4.0 대응 개조와 함께 꾸준히 확대될 것으로 예측됩니다. UV 레이저는 현재의 매출은 작지만 플렉서블 회로 기판이나 유리 커버 등의 미세한 기재에 대한 마이크로 마킹 수요에 의해 2031년까지 연평균 복합 성장률(CAGR) 6.6%로 확대될 전망입니다. 소비자용 전자기기의 수율 향상에 따라, 공장에서는 UV 가공 능력 업그레이드가 진행되고, 반도체 팹에서는 웨이퍼 레벨 ID용으로 355 nm 광원이 지정되고 있습니다.

그린 레이저 및 초단 펄스 솔루션은 실리콘 웨이퍼 가공 및 유리 인터포저의 드릴링에 틈새 역할을 합니다. Coherent사, TRUMPF사, IPG Photonics사는 빔 특성을 계속해서 개량하고 있지만, 중국 벤더는 기술 격차를 줄이고 가격면에서 우위에 서 있습니다. 현재는 빔 출력 자체보다 비전 가이드에 의한 정렬이나 인라인 검증 소프트웨어의 통합이 공급자 간의 차별화 요인이 되고 있습니다.

2025년에는 깊은 변조 방지 마킹을 필요로 하는 자동차 및 항공우주 분야 수요에 견인되어 조각 가공이 시장 수익의 38.15%를 차지했습니다. 파이버 시스템은 재료를 신속하게 제거하고 높은 대비 효과와 내구성을 보장합니다. 동시에 집진 모듈과 비전 검증 모듈은 처리량을 유지합니다. 어닐링 처리는 CAGR 6.85%로 가장 급속히 확대되는 공정입니다. 의료기기 제조업체는 표면을 부드럽고 무균 상태로 유지하는 산화층의 색 변화를 선호하기 때문입니다. 스테인레스 스틸 공구 및 임플란트 부품에는 완벽한 마무리가 필요하며 레이저 마킹 시장에서의 어닐링 처리의 점유율이 상승합니다.

에칭과 발포는 얕은 마킹으로 충분한 소비재 및 포장 라인에 의해 유지되고 있습니다. 유기 재료 중에서도 특히 골판지 및 가공 목재에는 탄소화가 여전히 주요 기술입니다. 공장이 유연한 생산 라인을 요구하는 가운데 조각, 어닐링, 에칭을 단일 사이클로 전환 가능한 멀티 프로세스 헤드에 대한 수요가 높아지고 있습니다.

지역별 분석

2025년 아시아 지역은 세계 매출의 46.05%를 차지했습니다. 중국의 전자기기 및 자동차 산업 클러스터가 기반이 되고, 스마트 공장용 대규모 정부 지원책이 뒷받침하고 있습니다. Han's Laser와 HGTECH 등 국내 공급업체들이 경쟁력 있는 가격의 파이버 유닛을 판매하여 지역 가공업자와 1차 부품 제조업체의 접근 확대에 기여하고 있습니다. 일본과 한국은 반도체나 EV 배터리 모듈용 틈새 정밀 가공 분야를 추구하고 인도에서는 홀마크 제도와 의약품 코드화 정책이 새로운 중견 시장을 개척하고 있습니다. 제조업체가 예측 가능한 비용과 규제 준수를 요구하는 가운데, 서비스 계약 증가는 지속적인 수익원을 창출하고 있습니다.

북미 수요는 성숙하며 품질 중시 경향이 현저하고, 항공우주, 의료기기, 자동차 VIN 코딩을 중심으로 전개하고 있습니다. 규제 및 보증 위험은 검증된 프로세스 모니터링 기능을 갖춘 고급형 시스템의 도입을 촉진합니다. 캐나다 기업은 광산기계를 위한 레이저 코딩을 활용하고 멕시코의 자동차 수출 공장은 미국 자동차 플랫폼의 추적성 기준을 충족하기 위해 인라인 마킹을 통한 현대화를 추진하고 있습니다. 가동 시간 보증 계약이 노동력 부족을 보완하기 때문에 서비스 보급률은 높은 수준입니다.

유럽에서는 지속가능성 목표와 엄격한 안전 규제가 균형을 이룹니다. 독일의 파워트레인 및 기계 제조업체는 깊은 각인 가공을, 프랑스의 항공우주 공장은 경량 복합재용으로 초단 펄스 빔을 도입하고 있습니다. 영국 및 북유럽의 브랜드는 잉크 사용 폐지 및 탄소 풋프린트 감소를 위해 레이저 코딩을 선택하고 있습니다. GS1 디지털 링크 도입이 진행됨에 따라 유럽의 포장 라인용 레이저 마킹 시장의 규모는 꾸준히 확대되고 있습니다. 동유럽에서는 니어 쇼어링의 혜택을 받아 폴란드와 체코 공화국에서 신규 도입이 진행되고 있습니다.

남미는 2031년까지 연평균 복합 성장률(CAGR) 5.88%로 가장 빠르게 성장할 것으로 예상되는 지역으로 브라질의 자동차 수출과 칠레의 광업 자동화가 견인하고 있습니다. 소규모 경제권에서는 고액의 자본 비용과 숙련 기술자 부족이 도입 속도를 둔화시키고 있지만, 임대 모델이 장벽 해소의 단서가 되고 있습니다. 아르헨티나와 콜롬비아의 디지털 제조에 대한 정부 지원책은 거시경제의 안정화에 따라 도입 가속화가 기대됩니다. 중동 및 아프리카는 완만한 성장을 보이고 있으며, 석유 및 가스 자산의 식별과 걸프 국가의 정부 지원에 의한 산업 단지가 수요 클러스터를 형성하고 있습니다. 그러나 정치적 리스크가 장기적인 예측을 억제하는 요인이 되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 의료기기의 UDI(고유 장치 식별) 및 추적성 규제의 의무화(미국, EU, 중국)

- EV용 전지 생산 급증에 따른 비접촉 마킹 수요 증가

- 소형화된 소비자용 전자기기가 아시아의 마이크로 마킹을 견인

- 지속 가능한 포장으로의 전환 및 유럽에서의 잉크젯 인쇄에서 레이저 코딩으로의 전환

- 북미의 자동차 공장에서 Industry 4.0의 인라인 통합

- 인도의 보석품 홀마크 디지털화 정책 추진

- 억제요인

- 신흥 시장에서 중소기업에게 필요한 고액 설비투자(15만 달러 이상)

- 항공우주용 복합재료의 인증 지연(열영향부(HAZ)에 관한 우려)

- 라틴아메리카 공장에서의 숙련 인력 부족

- 저가 중국 파이버 레이저 공급업체에 의한 마진 압력

- 업계 생태계 분석

- 규제와 기술 전망

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 레이저 유형별

- 파이버 레이저

- CO2 레이저

- 고체(Nd:YAG, Nd:YVO4)

- UV 레이저

- 그린 레이저

- 기타(다이오드, YAG, 하이브리드)

- 마킹 프로세스별

- 어닐링

- 에칭

- 조각

- 발포

- 탄소화

- 제공별

- 하드웨어

- 독립형 시스템

- 통합 및 인라인 시스템

- 소프트웨어

- 서비스

- 하드웨어

- 최종 사용자 업계별

- 자동차 및 항공우주

- 전자기기 및 반도체

- 의료기기 및 의료

- 식품 및 음료 포장

- 산업기계 및 공작기계

- 보석품 및 고급품

- 기타 산업(석유 및 가스, 방위 등)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Coherent Corp.

- IPG Photonics Corp.

- TRUMPF Group

- Han's Laser Technology Co. Ltd.

- Keyence Corp.

- Novanta Inc.(FOBA)

- Videojet Technologies Inc.

- Gravotech Group

- Mecco Partners LLC

- Epilog Laser Inc.

- Trotec Laser GmbH

- LaserStar Technologies Corp.

- SIC Marking Group

- Rofin-Sinar UK Ltd.

- Panasonic Connect Co. Ltd.

- Omron Corporation

- Domino Printing Sciences plc

- SATO Holdings Corp.

- TYKMA Electrox Inc.

- Nichia Corp.

- Control Laser Corp.

제7장 시장 기회 및 미래 전망

CSM 26.01.23The laser marking market is expected to grow from USD 3.62 billion in 2025 to USD 3.79 billion in 2026 and is forecast to reach USD 4.74 billion by 2031 at 4.61% CAGR over 2026-2031.

Growth is anchored in global regulations that require permanent device identification, expanding demand from electric vehicle battery production, and rising precision needs across miniaturised electronics and sustainable packaging. Asia continues to dominate installations as domestic suppliers cut entry costs, while service-led business models gain traction in North America and Europe. Pricing pressure from Chinese fiber-laser producers compresses hardware margins, but software and predictive-maintenance services preserve profitability. New use-cases in aerospace composites, jewellery hallmarking, and industrial automation widen the customer base even as high capital requirements constrain some small manufacturers.

Global Laser Marking Market Trends and Insights

Mandatory UDI and Traceability Regulations in Medical Devices Drive Permanent Marking Adoption

Stringent UDI frameworks created by the US FDA and the EU MDR make permanent, high-contrast device codes a legal necessity. Hospitals sterilise instruments repeatedly, so marks must resist abrasion, chemicals, and heat. Fiber and UV systems meet these durability needs on titanium implants, polymer catheters, and ceramic components, while direct connectivity to manufacturing execution systems simplifies compliance audits. Pharmaceutical serialization rules add volume, increasing overall line-integration demand for laser systems that print intricate 2D matrices without consumables. Suppliers that couple marking hardware with validation software shorten customer certification cycles and cut recall exposurre.

Surge in EV Battery Production Accelerates Contact-less Marking Demand

Gigafactories now stamp unique codes on every cell, module, and pack to manage recalls and recycling. Laser technology performs this identification at line speed without touching sensitive housings, avoiding particulate contamination and mechanical stress. Fiber lasers mark aluminum casings, while UV beams code polymer separators and flexible circuits. Demand for high-speed, vision-guided units capable of thousands of marks per hour is escalating across China, Korea, and the United States. Battery line integrators increasingly package traceability modules alongside welding and inspection stations for end-to-end process visibility.

High CAPEX Requirements Constrain SME Adoption in Emerging Markets

Industrial-grade systems with integrated vision and IoT connectivity often list above USD 150,000, exceeding the cashflow capacity of smaller Latin American and African manufacturers. Currency volatility inflates import costs, while local financing rates add further burden. Portable low-cost fiber units reduce entry price yet lack the precision and uptime guarantees demanded by automotive or medical lines. Leasing and pay-per-mark contracts are gaining popularity, but adoption remains gradual until third-party service networks mature

Other drivers and restraints analyzed in the detailed report include:

- Miniaturised Consumer Electronics Drive Micro-marking Precision Requirements

- Sustainable Packaging Shift Favors Laser Coding Over Inkjet Systems

- Qualification Delays for Aerospace Composites Create Validation Challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber lasers held 61.95% of revenue in 2025, reflecting their reliability, high wall-plug efficiency, and ability to mark most metals at high speed. Automotive powertrain parts, surgical instruments, and aerospace fasteners rely on fiber beams for deep, legible engravings that survive harsh service. The laser marking market size for fiber systems is projected to expand steadily alongside Industry 4.0 retrofits in Asia and Europe. UV lasers, though smaller in revenue today, are advancing at a 6.6% CAGR through 2031 thanks to demand for micro-marking on sensitive substrates such as flexible circuits and glass covers. Rising yields in consumer electronics push factories to retrofit UV capabilities, while semiconductor fabs specify 355 nm sources for wafer-level ID.

Green and ultrashort-pulse solutions occupy niche roles in silicon wafer processing and glass interposer drilling. Coherent, TRUMPF, and IPG Photonics continue to refine beam characteristics, but Chinese vendors narrow the technology gap and undercut on price. Integration of vision-guided alignment and inline verification software now differentiates suppliers more than raw beam power.

Engraving accounted for 38.15% of market revenue in 2025, driven by automotive and aerospace requirements for deep, tamper-proof marks. Fiber systems remove material quickly, ensuring high contrast and durability, while dust extraction and vision verification modules sustain throughput. Annealing is the fastest-expanding process at a 6.85% CAGR because medical device makers prefer oxide-layer color changes that leave surfaces smooth and sterile. The laser marking market share for annealing rises whenever stainless tools or implantables demand pristine finishes.

Etching and foaming continue to support consumer goods and packaging lines where shallow marks suffice. Carbonisation remains a go-to method for organic materials, especially cardboard and engineered wood. Multi-process heads capable of switching between engraving, annealing, and etching in a single cycle gain popularity as factories seek flexible cells.

The Laser Marking Market Report is Segmented by Laser Type (Fiber Laser, CO2 Laser, Solid-State, UV Laser, and More), Marking Process (Annealing, Etching, Engraving, Foaming, and Carbonisation), Offering (Hardware, Software, and Services), End-User Industry (Automotive and Aerospace, Electronics and Semiconductors, Medical Devices and Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia generated 46.05% of global revenue in 2025, anchored by China's electronics and automotive clusters and supported by large state incentives for smart factories. Domestic suppliers such as Han's Laser and HGTECH sell competitively priced fiber units, widening access for regional job shops and tier-one components firms. Japan and South Korea pursue niche precision applications in semiconductors and EV battery modules, while India's hallmarking and pharmaceutical coding policies open new mid-tier opportunities. Rising service contracts create recurring income streams as manufacturers seek predictable costs and regulatory compliance.

North America's demand is mature and quality-driven, centred on aerospace, medical devices, and automotive VIN coding. Regulations and warranty risk drive adoption of high-end systems with validated process monitoring. Canadian firms leverage laser coding for mining equipment while Mexico's automotive export plants modernise with inline marking to satisfy traceability standards for US vehicle platforms. Service penetration is high as uptime contracts offset labour shortages.

Europe balances sustainability objectives with strict safety regulations. German powertrain and machinery builders rely on deep engraving, while French aerospace plants adopt ultrashort-pulse beams for lightweight composites. Brands across the United Kingdom and the Nordic region choose laser coding to eliminate ink and lower carbon footprints. The laser marking market size attributed to European packaging lines grows steadily as GS1 Digital Link rollouts progress. Eastern Europe benefits from near-shoring, prompting new installations in Poland and the Czech Republic.

South America is the fastest-growing region at a 5.88% CAGR to 2031, led by Brazilian automotive exports and Chilean mining automation. High capital costs and a shortage of trained technicians slow the pace in smaller economies, yet leasing models are starting to remove barriers. Government incentives for digital manufacturing in Argentina and Colombia could accelerate adoption once macroeconomic stability improves. The Middle East and Africa register moderate growth, with oil and gas asset identification and government-backed industrial parks in the Gulf creating demand clusters, although political risk tempers longer-term forecasts.

- Coherent Corp.

- IPG Photonics Corp.

- TRUMPF Group

- Han's Laser Technology Co. Ltd.

- Keyence Corp.

- Novanta Inc. (FOBA)

- Videojet Technologies Inc.

- Gravotech Group

- Mecco Partners LLC

- Epilog Laser Inc.

- Trotec Laser GmbH

- LaserStar Technologies Corp.

- SIC Marking Group

- Rofin-Sinar UK Ltd.

- Panasonic Connect Co. Ltd.

- Omron Corporation

- Domino Printing Sciences plc

- SATO Holdings Corp.

- TYKMA Electrox Inc.

- Nichia Corp.

- Control Laser Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory UDI and traceability regulations in medical devices (US, EU, CN)

- 4.2.2 Surge in EV battery production contact-less marking demand

- 4.2.3 Miniaturised consumer electronics driving micro-marking in Asia

- 4.2.4 Sustainable packaging shift ? laser coding over inkjet in Europe

- 4.2.5 Industry 4.0 inline integration in North-American automotive plants

- 4.2.6 Jewellery hallmarking digitisation policy boost in India

- 4.3 Market Restraints

- 4.3.1 High CAPEX (Above USD 150 k) for SMEs in emerging markets

- 4.3.2 Qualification delay for aerospace composites (HAZ concerns)

- 4.3.3 Skilled-operator shortage in Latin-American factories

- 4.3.4 Margin pressure from low-cost Chinese fiber-laser suppliers

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Laser Type

- 5.1.1 Fiber Laser

- 5.1.2 CO? Laser

- 5.1.3 Solid-State (Nd:YAG, Nd:YVO?)

- 5.1.4 UV Laser

- 5.1.5 Green Laser

- 5.1.6 Others (Diode, YB:YAG, Hybrid)

- 5.2 By Marking Process

- 5.2.1 Annealing

- 5.2.2 Etching

- 5.2.3 Engraving

- 5.2.4 Foaming

- 5.2.5 Carbonisation

- 5.3 By Offering

- 5.3.1 Hardware

- 5.3.1.1 Stand-Alone Systems

- 5.3.1.2 Integrated/In-line Systems

- 5.3.2 Software

- 5.3.3 Services

- 5.3.1 Hardware

- 5.4 By End-User Industry

- 5.4.1 Automotive and Aerospace

- 5.4.2 Electronics and Semiconductors

- 5.4.3 Medical Devices and Healthcare

- 5.4.4 Food and Beverage Packaging

- 5.4.5 Industrial Machinery and Machine Tools

- 5.4.6 Jewellery and Luxury Goods

- 5.4.7 Other Industries (Oil and Gas, Defence, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Coherent Corp.

- 6.4.2 IPG Photonics Corp.

- 6.4.3 TRUMPF Group

- 6.4.4 Han's Laser Technology Co. Ltd.

- 6.4.5 Keyence Corp.

- 6.4.6 Novanta Inc. (FOBA)

- 6.4.7 Videojet Technologies Inc.

- 6.4.8 Gravotech Group

- 6.4.9 Mecco Partners LLC

- 6.4.10 Epilog Laser Inc.

- 6.4.11 Trotec Laser GmbH

- 6.4.12 LaserStar Technologies Corp.

- 6.4.13 SIC Marking Group

- 6.4.14 Rofin-Sinar UK Ltd.

- 6.4.15 Panasonic Connect Co. Ltd.

- 6.4.16 Omron Corporation

- 6.4.17 Domino Printing Sciences plc

- 6.4.18 SATO Holdings Corp.

- 6.4.19 TYKMA Electrox Inc.

- 6.4.20 Nichia Corp.

- 6.4.21 Control Laser Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment