|

시장보고서

상품코드

1911268

의약품 수탁 포장 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Pharmaceutical Contract Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

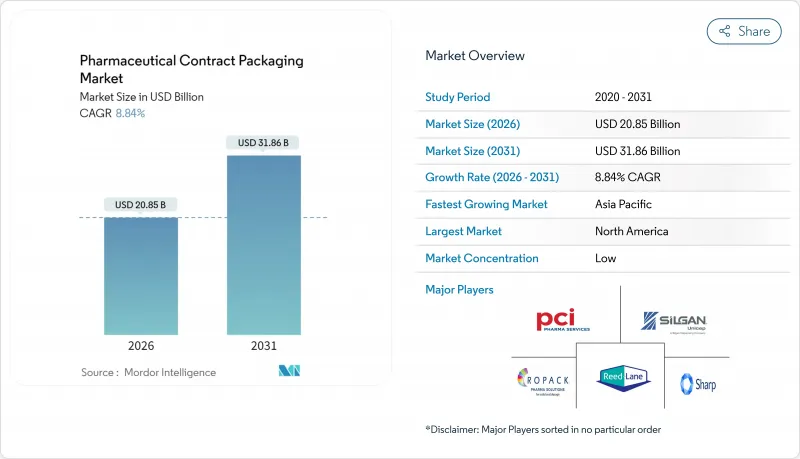

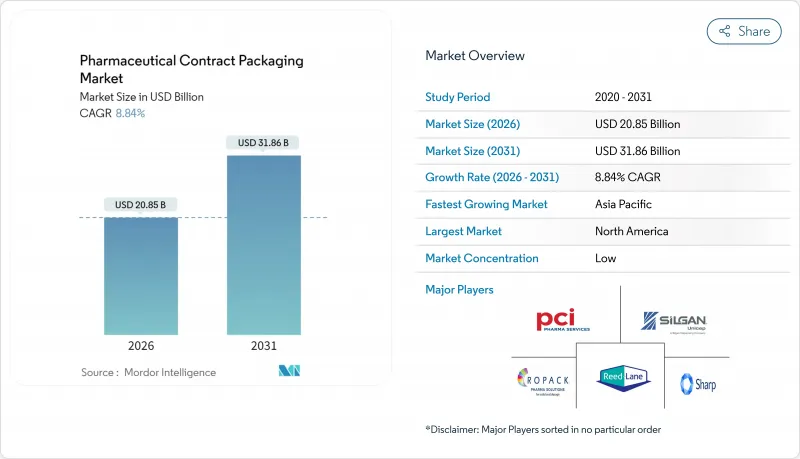

2026년 의약품 위탁 포장 시장의 규모는 208억 5,000만 달러로 평가되었고, 2025년 191억 6,000만 달러에서 성장이 예상됩니다.

2031년까지는 318억 6,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 8.84%로 확대될 전망입니다.

직렬화 의무화 증가, 바이오 의약품 파이프라인의 급성장, 통합 CDMO 모델에 대한 선호도 증가에 따라 제약 기업은 깊은 기술 노하우와 자본 집약적인 능력을 제공하는 외부 포장 파트너로 향하고 있습니다. 특히 무균 1차 용기, 프리필드 전달기기, 추적 대응 2차 포장에 대한 수요가 강하며, AI 대응 전환 시스템은 검증 사이클을 단축하여 라인 생산성을 향상시키고 있습니다. 미국 및 유럽 연합의 지역 니어쇼어링 계획은 투자 우선순위를 변화시키고 있으며, 아시아태평양 공급업체는 수출 지향 제네릭 의약품 성장에 대응하기 위해 생산 능력을 확대하고 있습니다.

세계의 의약품 위탁 포장 시장의 동향 및 인사이트

직렬화 의무화가 가져온 전례 없는 포장 변혁

2024년 11월 DSCSA의 전면 시행에 따라 계약 포장업자는 각 포장 레벨에 고유한 일련 번호, 바코드, 집계 데이터를 임베딩하게 되었으며 종래 라인은 매일 수백만의 일련 번호를 관리 및 조합하는 데이터 집약형 오퍼레이션으로 변모를 이루었습니다. 도입 초기에 발생한 오류율 30% 급증은 독자적인 하드웨어의 종속을 해소하는 오픈 아키텍쳐를 갖춘 '직렬화 2.0' 플랫폼의 필요성을 부각했습니다. 엣지에서 클라우드까지 라인 컨트롤러에 대한 투자가 가속화되고 공급업체는 현재 실시간 EPCIS 데이터 교환 기능을 번들로 제공합니다. 이를 통해 다운스트림 도매업체는 수초 안에 포장의 진위성을 검증할 수 있게 되었습니다. 이탈리아, 캐나다 및 걸프 국가에서 컴플라이언스 유예 기간이 단축되는 가운데 조화로운 시스템을 갖춘 세계 포장업체는 경쟁 우위를 얻고 있습니다.

생물학적 제형의 급증으로 멸균 포장 인프라를 재구성

세계의 무균의약품 생산량은 2027년까지 연평균 복합 성장률(CAGR) 15%로 증가할 전망이며, 부속서 1의 개정에 의해 오염 관리가 기업 전체의 우선 과제가 되었습니다. 즉시 사용할 수 있는 네스티드 바이알, 앰풀 및 폴리머 주사기는 유리 세척 공정이 필요하지 않으며 최신 용기 밀봉 시험은 파괴적인 무균 샘플링 대신 헬륨 질량 분석법과 진공 감쇠법을 채택했습니다. Syntegon의 SPC 1000과 같은 자동 침강 플레이트 체인저는 수작업을 80% 줄이고 배치 릴리스까지 시간을 단축합니다.

추적 관리 규정 준수 비용으로 영업 이익 압박

시장마다 다른 직렬 데이터 형식으로 포장업자는 여러 스키마에 대응하는 IT 스택을 운용하지 않을 수 없으며, 멀티마켓 SKU당 최대 20%의 검증 및 지원 예산 증대를 초래하고 있습니다. 2025년 2월 이탈리아에서 시작된 EU FMD 집계 시스템은 라인 개조와 창고 업그레이드를 요구하는 규제 강화의 흐름을 상징합니다.

부문 분석

2025년 의약품 수탁 포장 시장에서 1차 포장은 45.10%의 점유율을 차지하였고 의약품 접촉 재료에 대한 용출물 및 추출물의 감시 강화에 따라 10.05%의 연평균 복합 성장률(CAGR)로 확대하고 있습니다. 생물학적 제제의 화학적 적합성을 보장하기 위해, 유형 I 붕규산 유리 바이알, 환형 올레핀 폴리머 카트리지, 고차단성 블리스터 필름이 투자 계획의 중심을 차지합니다. 성장 기세는 많은 관할 구역에서 1차 포장층에서 시작되는 단위 수준에서의 직렬화 의무화를 반영합니다.

무균 용기 및 폐쇄 시스템의 혁신이 경쟁 우위성을 재정의하고 있습니다. 위탁 포장업자는 현재 레이저식 헤드스페이스 분석과 헬륨 질량 분석법을 사용하여 포장 무결성을 검증하고 파괴 시험으로 인한 폐기물을 줄이면서 부속서 1의 요건을 충족하고 있습니다. 2차 및 3차 서비스는 후기 단계의 커스텀 키트 조립과 특수 콜드체인 물류를 통해 부가가치를 계속 제공하고 있지만, 규제의 복잡성에 의해 수익의 중심은 1차 포장층에 머물고 있습니다.

경구 고형 제제의 주류화에 의해 병이 최대 실적의 포맷으로 유지되고 있습니다. 그러나 프리필드 주사기 및 카트리지는 2031년까지 연평균 복합 성장률(CAGR) 11.05%를 나타낼 전망이며, 의약품 수탁 포장 시장에서 가장 급속히 확대하는 분야가 되고 있습니다. 수요는 자가주사용 생물학적 제제, 펜형 주사기의 보급, 바늘의 취급을 금지하는 병원의 안전 대책에 의해 견인되고 있습니다.

환형 올레핀 폴리머제 배럴의 기술 혁신에 의해 약제의 안정성과 창의 투명성이 높아져, 안전 바늘 실드나 전자식 용량 카운터는 종래 디바이스 제조업체에 국한되었던 사용 용이성 기능을 추가했습니다. 통합 플런저 설치, 질소 퍼지 및 자동 주사기 조립 서비스를 제공하는 위탁 포장업체는 턴키 솔루션을 추구하는 전문 의약품 고객과 장기 공급 계약을 획득했습니다.

지역별 분석

북미는 2025년 수익의 39.10%를 차지하였으며 FDA의 직렬화 의무화, 강력한 바이오 의약품 파이프라인, 대규모 니어쇼어링 자본 유입에 뒷받침되고 있습니다. 노보 노디스크사의 41억 달러를 투자한 클레이튼 복합시설과 같은 투자는 충전 및 마무리, 검사, 최종 조립을 일원화하고 공급 라인을 단축하여 국내의 회복력을 강화하고 있습니다. 캐나다의 온타리오 주에서 무균 의약품 회랑과 멕시코의 마킬라도라 확장은 미국의 생산 능력을 보완하고 지역 내 조달 요구사항을 충족하여 관세 효율적인 크로스보더 유통을 가능하게 하고 있습니다.

유럽은 혁신의 기반이 되고 있으며, 재료 연구 개발을 가속화하는 PPWR 지속가능성 규정과 최고 수준의 클린룸 성능을 요구하는 무균 가이드라인(부속서 1)이 견인 역할을 하고 있습니다. 독일의 엔지니어링 에코시스템은 고정밀 기기 공급의 기반이 되고, 이탈리아와 프랑스에서는 희귀의약품 생산에 대응하여 풍부한 경험을 보유한 충전 및 마무리 시설이 입지하고 있습니다. 영국의 포장업자는 선진적 치료법용으로 전환하여 브렉시트 이후 MHRA의 유연성을 활용하여 세계의 임상 프로그램을 유치하고 있습니다.

아시아태평양은 10.10%라는 가장 높은 CAGR을 나타내고 있으며 중국과 인도의 CDMO가 제네릭 의약품 붐과 바이오시밀러 도입에 연동한 생산 능력 확대를 추진하고 있습니다. 일본에서는 바이알 충전에서 고속 로봇 기술을 선도하고, 한국은 항체 약물 복합체 프로젝트를 주도하며, 싱가포르는 세포 치료 시설에의 세제 우대를 확대하고 있습니다. 지역 각국 정부는 PIC/S 하에서 GMP의 수렴을 추진하여 여러 국가에서의 승인 절차를 간소화함과 동시에 국경을 넘는 공급 네트워크를 촉진하고 있습니다. 호주 및 뉴질랜드는 틈새 시장인 무균 개발 서비스를 제공하여 이 지역의 밸류체인에 대한 지위 향상을 뒷받침합니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 직렬화 의무화와 위조 방지 규제의 급증

- 생물학적 제제 및 특수 의약품 붐이 멸균 포장 수요를 확대

- CDMO의 원스톱 숍 수요(제조와 포장의 통합)

- 미국 및 유럽의 제약 대기업에 의한 공급 체인 니어쇼어링

- AI를 활용한 라인 전환에 의한 검증 시간 단축

- 억제요인

- 진화하는 세계의 추적 관리 기준에 따라 컴플라이언스 비용 증가

- 복합재료의 지속가능성에 관한 규제가 플라스틱의 이익률을 압박

- 고속 무균 충전 라인용 숙련 노동자의 부족

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 서비스 유형별

- 1차

- 병

- 바이알 및 앰풀

- 블리스터

- 2차

- 판지

- 라벨 및 인서트

- 3차

- 1차

- 포장 형태별

- 병

- 페트병

- 유리병

- 바이알 및 앰풀

- 블리스터

- 샤쉐 및 스틱 팩

- 프리필드 주사기 및 카트리지

- 병

- 약제 형태별

- 고형 제제

- 정제

- 캡슐

- 경구액제

- 주사제

- 소용량 주사제

- 대용량 주사제

- 고형 제제

- 치료영역별

- 종양학

- 순환기계

- 중추신경계

- 감염증

- 기타 치료 영역

- 최종 사용자별

- 제약 대기업(수익 100억 달러 이상)

- 제네릭 의약품 및 바이오시밀러 기업

- 신흥 생명공학 기업 및 스타트업 기업

- CRO 및 CDMO 파트너

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 기타 아프리카

- 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- PCI Pharma Services

- Catalent Inc.

- Sharp Packaging Services

- Almac Group

- Wasdell Group

- Ropack Inc.

- Reed-Lane Inc.

- Jones Healthcare Group

- Recipharm AB

- Tjoapack Netherlands BV

- AmeriPac(Veritiv Corp)

- Silgan Unicep

- Nelipak

- Aphena Pharma Solutions

- Central Pharma Contract Packing

- Quantrelle Packaging Solutions

- Variopack GmbH

- Sepha Ltd.

- Assemblies Unlimited

- DaklaPack Group

- Tripak Pharmaceuticals

- MPH Co-Packing

- Southwest Packaging

- MJS Packaging

- Jam Jams Group

- Asiapack(Elanders Group)

- Finishing Services

제7장 시장 기회 및 미래 전망

CSM 26.01.23pharmaceutical contract packaging market size in 2026 is estimated at USD 20.85 billion, growing from 2025 value of USD 19.16 billion with 2031 projections showing USD 31.86 billion, growing at 8.84% CAGR over 2026-2031.

Rising serialization mandates, a booming biologics pipeline and growing preference for integrated CDMO models are steering pharmaceutical companies toward outsourced packaging partners that offer deep technical know-how and capital-intensive capabilities. Demand is particularly strong for sterile primary containers, pre-filled delivery devices and track-and-trace ready secondary packs, while AI-enabled changeover systems are trimming validation cycles and boosting line productivity. Regional near-shoring programs in the United States and the European Union are shifting investment priorities, and Asia-Pacific suppliers are scaling capacity to meet export-oriented generic drug growth.

Global Pharmaceutical Contract Packaging Market Trends and Insights

Serialization Mandates Drive Unprecedented Packaging Transformation

Full DSCSA enforcement in November 2024 forced contract packagers to embed unique serial numbers, barcodes and aggregation data at every packaging level, transforming legacy lines into data-rich operations that manage and reconcile millions of serial numbers daily. Error-rate spikes of 30% in early roll-outs underscored the need for "Serialization 2.0" platforms with open architectures that remove proprietary hardware lock-ins. Investments in edge-to-cloud line controllers accelerated, and vendors now bundle real-time EPCIS data exchange, enabling downstream wholesalers to verify pack authenticity in seconds. As compliance windows tighten in Italy, Canada and Gulf states, global packagers with harmonized systems gain a competitive edge.

Biologics Surge Reshapes Sterile Packaging Infrastructure

World-wide sterile medicinal product output is climbing at 15% CAGR to 2027, and Annex 1 revisions have elevated contamination control to an enterprise-wide priority. Ready-to-use nested vials, ampoules and polymer syringes eliminate glass washing steps, while modern container-closure integrity testing replaces destructive sterility sampling with helium mass-spectrometry and vacuum decay methods. Automated settle-plate changers, such as Syntegon's SPC 1000, cut manual interventions by 80% and drive faster batch-release timelines.

Track-and-Trace Compliance Costs Strain Operational Margins

Divergent serial data formats across markets oblige packagers to operate multi-schema IT stacks, inflating validation and support budgets by up to 20% per multi-market SKU. Italy's February 2025 go-live for EU FMD aggregation illustrates the continuing regulatory drumbeat that forces line retrofits and warehouse upgrades.

Other drivers and restraints analyzed in the detailed report include:

- CDMO Integration Accelerates End-to-End Service Adoption

- Supply-Chain Near-Shoring Transforms Geographic Manufacturing Patterns

- Skilled Labor Shortage Constrains Sterile Manufacturing Expansion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary packaging held a 45.10% share of the pharmaceutical contract packaging market in 2025 and is expanding at 10.05% CAGR as drug-contact materials face tighter leachables and extractables scrutiny.Type I borosilicate glass vials, cyclic olefin polymer cartridges and high-barrier blister films dominate investment plans because they assure chemical compatibility for biologics. Growth momentum also reflects mandatory unit-level serialization, which starts at the primary layer in many jurisdictions.

Sterile container-closure innovation is redefining competitive positioning. Contract packagers now validate package integrity using laser-based headspace analysis and helium mass-spectrometry, reducing destructive testing waste while meeting Annex 1 expectations. Secondary and tertiary services continue to add value through late-stage custom kitting and specialty cold-chain logistics, yet regulatory complexity keeps the revenue center anchored in the primary tier.

Bottles remain the largest format owing to oral solid dosage dominance. However, pre-filled syringes and cartridges show 11.05% CAGR through 2031, making them the fastest-expanding slice of the pharmaceutical contract packaging market. Demand is fuelled by self-injection biologics, pen-injector proliferation and hospital safety mandates that curb needle handling.

Technical advances in cyclic olefin polymer barrels improve drug stability and window clarity, while needle-safety shields and electronic dose counters embed usability features once reserved for device makers. Contract packagers offering integrated plunger placement, nitrogen purging and auto-injector assembly services secure long-term supply agreements with specialty-pharma clients seeking turnkey solutions.

The Pharmaceutical Contract Packaging Market Report is Segmented by Service Type (Primary, Secondary, Tertiary), Packaging Format (Bottles, Vials and Ampoules, and More), Drug Formulation (Solid Dosage, and More), Therapeutic Area (Oncology, Cardiovascular, and More), End-User (Big Pharma, Generics/Biosimilar Companies, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.10% of 2025 revenue, supported by FDA serialization mandates, strong biologics pipelines and sizeable near-shoring capital flows. Investments such as Novo Nordisk's USD 4.1 billion Clayton complex embed fill-finish, inspection and final assembly under one roof, shortening supply lines and augmenting domestic resiliency. Canada's sterile-drug corridor in Ontario and Mexico's maquiladora expansions complement US capacity, enabling duty-efficient cross-border flows that satisfy regional content stipulations.

Europe remains an innovation hub, driven by PPWR sustainability rules that accelerate material R&D and by Annex 1 sterile guidelines demanding best-in-class cleanroom performance. Germany's engineering ecosystem anchors high-precision equipment supply, while Italy and France host seasoned fill-finish sites catering to orphan-drug runs. United Kingdom packagers pivot toward advanced therapy applications, leveraging MHRA agility post-Brexit to attract global clinical programs.

Asia-Pacific shows the fastest 10.10% CAGR as Chinese and Indian CDMOs scale capacities that align with generics booms and biosimilar roll-outs. Japan pioneers high-speed robotics in vial filling, South Korea spearheads antibody-drug conjugate projects and Singapore extends tax incentives for cell-therapy facilities. Regional governments nurture GMP convergence under PIC/S, easing multi-country approvals and encouraging cross-border supply networks. Australia and New Zealand contribute niche sterile development services, reinforcing the region's climb up the value chain.

- PCI Pharma Services

- Catalent Inc.

- Sharp Packaging Services

- Almac Group

- Wasdell Group

- Ropack Inc.

- Reed-Lane Inc.

- Jones Healthcare Group

- Recipharm AB

- Tjoapack Netherlands B.V.

- AmeriPac (Veritiv Corp)

- Silgan Unicep

- Nelipak

- Aphena Pharma Solutions

- Central Pharma Contract Packing

- Quantrelle Packaging Solutions

- Variopack GmbH

- Sepha Ltd.

- Assemblies Unlimited

- DaklaPack Group

- Tripak Pharmaceuticals

- MPH Co-Packing

- Southwest Packaging

- MJS Packaging

- Jam Jams Group

- Asiapack (Elanders Group)

- Finishing Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Serialization mandates and anti-counterfeit regulation surge

- 4.2.2 Biologic and specialty-drug boom amplifying sterile packaging demand

- 4.2.3 CDMO one-stop-shop preference (integrated manufacturing + packaging)

- 4.2.4 Supply-chain near-shoring by Big Pharma in US-EU

- 4.2.5 AI-enabled line-changeover reducing validation time

- 4.3 Market Restraints

- 4.3.1 Evolving global track-and-trace standards raise compliance costs

- 4.3.2 Poly-material sustainability rules squeeze margin on plastics

- 4.3.3 Qualified labor shortage for high-speed sterile filling lines

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Primary

- 5.1.1.1 Bottles

- 5.1.1.2 Vials and Ampoules

- 5.1.1.3 Blister Packs

- 5.1.2 Secondary

- 5.1.2.1 Cartons

- 5.1.2.2 Labels and Inserts

- 5.1.3 Tertiary

- 5.1.1 Primary

- 5.2 By Packaging Format

- 5.2.1 Bottles

- 5.2.1.1 Plastic Bottles

- 5.2.1.2 Glass Bottles

- 5.2.2 Vials and Ampoules

- 5.2.3 Blister Packs

- 5.2.4 Sachets and Stick Packs

- 5.2.5 Pre-filled Syringes and Cartridges

- 5.2.1 Bottles

- 5.3 By Drug Formulation

- 5.3.1 Solid Dosage

- 5.3.1.1 Tablets

- 5.3.1.2 Capsules

- 5.3.2 Oral Liquids

- 5.3.3 Injectable

- 5.3.3.1 Small-volume Parenterals

- 5.3.3.2 Large-volume Parenterals

- 5.3.1 Solid Dosage

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Cardiovascular

- 5.4.3 CNS

- 5.4.4 Infectious Disease

- 5.4.5 Other Therapeutic Areas

- 5.5 By End-user

- 5.5.1 Big Pharma (>USD 10 bn revenue)

- 5.5.2 Generics/Biosimilar Companies

- 5.5.3 Emerging Biotech and Start-ups

- 5.5.4 CRO/CDMO Partners

- 5.5.5 Others End-user

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 United Arab Emirates

- 5.6.4.1.2 Saudi Arabia

- 5.6.4.1.3 Turkey

- 5.6.4.1.4 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Nigeria

- 5.6.4.2.3 Egypt

- 5.6.4.2.4 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 PCI Pharma Services

- 6.4.2 Catalent Inc.

- 6.4.3 Sharp Packaging Services

- 6.4.4 Almac Group

- 6.4.5 Wasdell Group

- 6.4.6 Ropack Inc.

- 6.4.7 Reed-Lane Inc.

- 6.4.8 Jones Healthcare Group

- 6.4.9 Recipharm AB

- 6.4.10 Tjoapack Netherlands B.V.

- 6.4.11 AmeriPac (Veritiv Corp)

- 6.4.12 Silgan Unicep

- 6.4.13 Nelipak

- 6.4.14 Aphena Pharma Solutions

- 6.4.15 Central Pharma Contract Packing

- 6.4.16 Quantrelle Packaging Solutions

- 6.4.17 Variopack GmbH

- 6.4.18 Sepha Ltd.

- 6.4.19 Assemblies Unlimited

- 6.4.20 DaklaPack Group

- 6.4.21 Tripak Pharmaceuticals

- 6.4.22 MPH Co-Packing

- 6.4.23 Southwest Packaging

- 6.4.24 MJS Packaging

- 6.4.25 Jam Jams Group

- 6.4.26 Asiapack (Elanders Group)

- 6.4.27 Finishing Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment