|

시장보고서

상품코드

1911333

펜스 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Fencing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

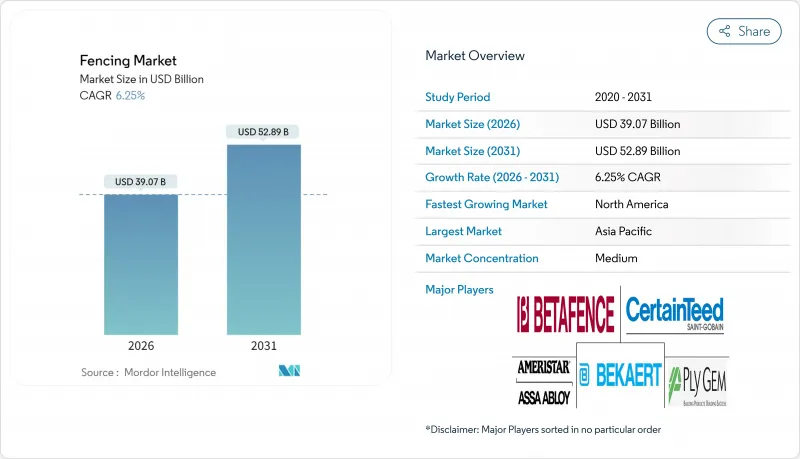

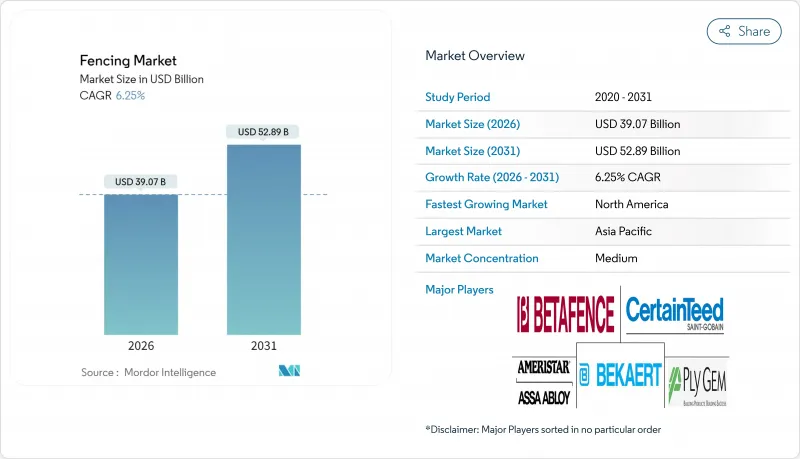

2026년 펜스 시장의 규모는 390억 7,000만 달러로 평가되었고, 2025년 367억 7,000만 달러에서 성장하여, 2031년에는 528억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지는 CAGR 6.25%로 확대될 전망입니다.

이 확장은 전력망, 데이터센터, 국경 강화 의무화, 스마트 경계 하드웨어의 급속한 상업화, 정부의 꾸준한 인프라 투자를 반영합니다. 내구성과 라이프사이클 비용의 이점을 바탕으로 금속품은 대규모 프로젝트에서 계속 주류를 차지하지만, 기후 변화에 강한 설계 요건 하에서 복합재료 및 PVC 대체품이 급속히 보급되고 있습니다. 주택 수요는 견조한 상태를 유지하는 반면, 농업 및 재생에너지 시설은 가장 빠르게 성장할 수 있는 기회 영역으로 부상하고 있습니다. IoT 대응 시스템에 의한 기술적 장애물 증가에 따라 전문 계약자가 수익의 대부분을 차지하고 있지만, 성숙한 주택 시장에서는 DIY 키트 수요도 확대하고 있습니다. 지역별로는 연방 정부의 지출 패키지에 의해 북미가 주도권을 유지하고 있지만, 수십억 달러 규모의 국경 및 산업 프로그램을 배경으로 아시아태평양이 다른 모든 지역을 웃도는 성장이 전망되고 있습니다.

세계의 펜스 시장의 동향 및 인사이트

정부 인프라 지출이 경계 안전 수요를 촉진

국가 안보의 우선순위는 국경 요새화 및 중요 자산 보호를 위한 다년도에 걸친 대규모 예산에 반영됩니다. 인도는 2034년까지 민감한 국경을 따라 펜스와 도로 건설에 32,500캐롤 루피(38억 9,000만 달러)를 할당하고 절단 방지 및 월담 방지 기능을 갖춘 강철 설계를 지정하고 있습니다. 북미 신뢰도위원회(NERC)의 개정 가이드라인에서는 영향도가 높은 송전망 제어센터에 충돌내성 게이트가 의무화되어 전력회사는 노후화된 경계선의 업그레이드를 요구받고 있습니다. 미국 연방 건축 기준에는 현재 다층 장벽과 전자 접근 제어를 규정하는 "환경 설계에 의한 범죄 방지(CPTED)"의 원칙이 포함되어 있습니다. 이러한 규제는 고사양 장비 수요를 촉진하고 보안 클리어런스를 가진 공급업체를 우대합니다.

스마트 센서 대응 펜스 시스템의 보급 확대

IoT 통합으로 수동 펜스는 능동적인 위협 감지 네트워크로 변모하고 있습니다. IEEE의 연구에 따르면 멀티 센서가 장착된 스마트 펜스는 기존의 빔 감지기와 비교하여 오경보를 60% 줄입니다. 미국 국방부의 통신 표준은 최근 안전한 IoT 인터페이스를 통합하기 위해 업데이트되었으며 상용 제품의 로드맵에 영향을 미칩니다. 미국 National Safe Skies Alliance의 모범 사례를 준수하는 공항에서는 현재 영상 분석, 레이더 및 인증 데이터베이스를 통합한 경계 솔루션을 지정하고 있습니다. 국토 안보부의 검증 프로토콜은 조달 주기를 가속화하는 통일적인 성능 지표를 확립했습니다.

강재, 목재, PVC 수지의 가격 변동

에너지 비용과 전기 수요에 의해 금속 및 수지 시장은 계속 부족 상태가 지속되고 있습니다. 세계은행 금속지수는 2024년 4월에 9% 상승했으며 2025년 기준으로 금속 가격의 추가 상승을 시사합니다. 센츄리 알루미늄의 국내 생산 감소는 알루미늄 공급에서의 비용감응도의 높이를 드러내고 있습니다. 보이시 캐스케이드의 2024년 수익 감소는 주택 시장의 침체 기간 동안 목재 가격 전가의 과제를 나타냈습니다. 제조업체는 자주 추가 요금을 부과하지만 가격 변동은 여전히 수익률을 압박하고 입찰 가격 설정을 복잡하게 만듭니다.

부문 분석

금속품은 2025년 매출액의 50.05%를 차지하였으며 확실한 강도와 영구적인 가치로 펜스 시장을 뒷받침하고 있습니다. 철강은 방위 및 유틸리티 프로젝트에서 주도권을 잡는 한편, 알루미늄은 내식성으로 인해 주택 분야에서의 도입이 진행되고 있습니다. 목재는 자연미를 중시하는 건축규제지역에서 인기를 유지하고 있지만, EU의 포름알데히드 규제 강화로 대체 리스크가 발생하고 있습니다. 콘크리트 패널은 틈새 시장이지만 폭풍에 대한 대비책이 필요한 현장에서는 필수적입니다.

복합재 및 PVC 시스템은 설계자가 유지보수가 적은 대체품과 무연 지침을 준수하도록 요구하는 가운데 CAGR 8.25%로 확대되고 있습니다. 사용한 PVC의 회수나 바이오 베이스 안정제를 추구하는 제조업체는 그린 조달 프리미엄의 획득이 전망됩니다. 아그리볼타이크(농업과 태양광 발전의 복합) 파일럿 사업은 경량 복합재가 태양광 패널의 서브구조로서도 기능하고, 다기능 자산으로서 펜스 시장의 규모를 확대할 가능성을 나타내고 있습니다.

2세대 복합재는 강도 중량비와 재활용성을 양립시켜 공급업체에게 장기적인 우위를 제공합니다. EU의 납 규제 강화 및 신규 SVHC 지정 물질 리스트는 아연 안정화 PVC와 재생 HDPE 블렌드로의 전환을 가속화하고 있습니다. 압출 성형 능력과 산업 폐기물 순환 시스템을 갖춘 공급업체는 버진 수지 제조업체를 가격면에서 능가할 수 있습니다. 지속가능성 공개는 많은 공공조달에서 필수 요건이 되어 이러한 전환을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 세계 매출의 35.10%를 차지하였고 도로, 송전망, 그리고 퇴역 군인 시설 업그레이드에 대한 연방 보조금에 의해 견인되었습니다. NERC(북미 신뢰도위원회)의 개정 규정에 따라 전력회사는 변전소의 경계 강화가 의무화되고 '바이 미국' 조항이 국내 성형업자 및 가공업자에 대한 지출을 유도하고 있습니다. 확대되는 주택 개수 수요는 이 지역의 단기 전망을 뒷받침합니다.

아시아태평양은 현재 규모는 작지만 2031년까지 7.05%라는 가장 높은 CAGR로 추이할 전망입니다. 인도는 국경 펜스에 4억 달러 이상의 예산을 할당하고 있으며, 고위험 회랑을 따라 월담 방지 강제 그레이팅이 설치됩니다. 중국에서는 부동산 부문의 역풍에도 불구하고 인프라 자극책과 도시 재생 프로젝트가 펜스 수요를 뒷받침합니다. 일본과 한국은 스마트 센서 도입을 추진하고 있으며 호주의 광업 부문은 격오지 캠프를 위한 가설 장벽 조달을 계속하고 있습니다.

유럽 시장은 엄격한 에코디자인법과 순환형 경제 목표에 의해 규정됩니다. 무연 PVC 도입 기한과 2026년 EU 포름알데히드 기준치는 재료 대체를 촉진하고 혁신 기업에 경쟁력의 차이를 가져왔습니다. 신재생에너지의 확대와 특히 육상풍력발전의 업그레이드가 유틸리티 수요를 뒷받침하고 있습니다. 동유럽은 EU 결속기금의 조성금을 교통회랑에 투입하는 혜택을 받고 있어 장거리에 걸친 방음 및 방범 펜스가 요구되고 있습니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- 정부의 인프라 지출이 경계 안전 대책 수요를 촉진

- 스마트 센서 탑재 펜스 시스템의 보급 확대

- 기후 변화에 강한 복합재 및 PVC 재료의 보급

- 성숙경제권에서의 DIY 주택 개보수 문화 확대

- 중요자산(유틸리티, 데이터센터) 강화에 관한 의무적 규제

- 아그리볼타이크 및 수직 농법 시설에서의 경계 경비 수요

- 억제요인

- 강재, 목재, PVC 수지의 가격 변동성

- 저비용 비조직적 제조업체에 의한 경쟁

- 목재 방부제 및 PVC 첨가제에 대한 환경 규제 강화

- 물리적 장벽을 대체하는 전자 감시 시스템에 대한 대체 지출 증가

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- 업계의 매력도 - Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 재료 분석

- 지정학이 펜스 시장에 미치는 영향

제5장 시장 규모 및 성장 예측

- 재료별

- 금속

- 강철

- 알루미늄

- 목재

- 플라스틱 및 복합재료

- 콘크리트

- 기타 소재

- 금속

- 최종 사용자별

- 주택

- 농업

- 군 및 방위

- 정부

- 광업

- 석유 및 화학제품

- 에너지 및 전력

- 기타 최종 사용자

- 설치 유형별

- 전문 계약자

- 기타 - 제조업체, DIY 및 모듈러 키트

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타 유럽

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 기타 아시아태평양

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- CertainTeed

- Bekaert

- Betafence

- Ameristar Perimeter Security

- Ply Gem

- Long Fence

- Gregory Industries

- A-1 Fence Products

- Specrail

- Jerith

- Trex Company

- Barrette Outdoor Living

- Master Halco

- ActiveYards

- Fortress Building Products

- Allied Tube & Conduit

- Eastern Wholesale Fence

- Merchants Metals

- ITOCHU Corporation(Sakura)

- Gentek Building Products

제7장 시장 기회 및 미래 전망

제8장 부록

- 거시경제지표

- 주요 생산, 소비 및 수출입 통계

Fencing market size in 2026 is estimated at USD 39.07 billion, growing from 2025 value of USD 36.77 billion with 2031 projections showing USD 52.89 billion, growing at 6.25% CAGR over 2026-2031.

This expansion reflects mandatory hardening of power grids, data centers and borders, the rapid commercialization of smart perimeter hardware, and steady government infrastructure outlays. Metal products continue to dominate large-scale projects because of durability and life-cycle economics, while composite and PVC alternatives are scaling quickly under climate-resilient design mandates. Residential demand remains robust, yet agriculture and renewable-energy installations are emerging as the fastest-moving opportunity set. Professional contractors capture most revenue as IoT-enabled systems raise the technical bar, although DIY kits are expanding in mature housing markets. Regionally, North America retains leadership because of federal spending packages, but Asia-Pacific is set to outpace all other regions on the back of multibillion-dollar border and industrial programs.

Global Fencing Market Trends and Insights

Government Infrastructure Spend Boosting Perimeter Safety Demand

National security priorities are translating into sizeable multiyear budgets devoted to border fortifications and critical-asset protection. India has earmarked INR 32,500 crore (USD 3.89 billion) for fencing and road construction along sensitive borders through 2034, specifying anti-cut and anti-climb steel designs. Updated North American Electric Reliability Corporation guidance requires crash-rated gates at high-impact grid control centers, prompting utilities to overhaul outdated perimeter lines. United States federal building standards now embed Crime Prevention Through Environmental Design principles that specify layered barriers and electronic access control. These mandates are fueling demand for high-specification installations and favoring suppliers with security clearances.

Rising Adoption Of Smart, Sensor-Enabled Fencing Systems

IoT integration is converting passive fences into active threat-detection networks. IEEE studies show multi-sensor smart fences cut false alarms by 60% relative to legacy beam detectors. The U.S. Department of Defense telecommunication standard, recently updated to incorporate secure IoT interfaces, is shaping commercial product roadmaps. Airports adhering to National Safe Skies Alliance best practices are now specifying perimeter solutions that merge video analytics, radar, and credential databases. Department of Homeland Security validation protocols have created uniform performance metrics that accelerate procurement cycles.

Volatile Steel, Timber & PVC Resin Prices

Metal and resin markets remain tight due to energy costs and electrification demand. The World Bank metals index rose 9% in April 2024 and indicates further upside for base metals in 2025. Century Aluminum's curtailed domestic output underscores cost sensitivity in aluminum supply. Boise Cascade's 2024 revenue dip illustrates timber price pass-through challenges during soft housing cycles. Manufacturers are issuing more frequent surcharges, but volatility still squeezes margins and complicates bid pricing.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Critical-Asset Hardening Regulations

- Climate-Resilient Composite & PVC Materials Gaining Traction

- Competition From Low-cost Unorganised Manufacturers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal products generated 50.05% of 2025 revenue, anchoring the fencing market through proven strength and lifecycle value. Steel commands defense and utility projects, while aluminum gains residential traction for corrosion resistance. Wood keeps a loyal following where planning codes favor natural aesthetics, though upcoming EU formaldehyde caps create substitution risk. Concrete panels stay niche but indispensable at blast-critical sites.

Composite and PVC systems are scaling at an 8.25% CAGR as specifiers seek low-maintenance alternatives and compliance with lead-free directives. Manufacturers pursuing post-consumer PVC recovery and bio-based stabilizers stand to secure green-procurement premiums. Agrivoltaic pilots highlight how lightweight composites double as solar-panel sub-structures, expanding the fencing market size for multifunctional assets.

Second-generation composites position vendors for long-run advantage by balancing strength-to-weight ratios and recyclability. Restrictive EU rules on lead and novel SVHC listings are accelerating the pivot to zinc-stabilized PVC and recycled HDPE blends. Suppliers with extrusion capacity and closed-loop post-industrial scrap streams can undercut virgin-resin incumbents. Sustainability disclosures are now prerequisites for many public tenders, reinforcing the shift.

The Fencing Market Report is Segmented by Material (Metal, Wood, Plastic & Composite, Concrete, Other Materials), by End-User (Residential, Agricultural, Military & Defense, Government, Mining, and More), by Installation Type (Professional Contractor, Others - Fabricators, DIY / Modular Kits), and by Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 35.10% of 2025 global sales, propelled by federal grants for road, grid, and veterans facility upgrades. Updated NERC rules obligate utilities to fortify substation perimeters, while Buy-America provisions steer spend toward domestic roll-formers and fabricators. An expanding residential remodeling base supports the region's near-term outlook.

Asia-Pacific, though smaller today, is set to post the fastest 7.05% CAGR through 2031. India has budgeted more than USD 400 million for border fencing, including anti-climb steel grating along high-risk corridors. China's infrastructure stimulus and urban renewal projects cushion fencing demand despite property-sector headwinds. Japan and South Korea champion smart-sensor adoption, while Australia's mining sector continues to procure temporary barriers for remote camps.

Europe's market is framed by stringent eco-design laws and circular-economy targets. Lead-free PVC deadlines and the 2026 EU formaldehyde threshold spur material substitution, opening a competitiveness gap for innovators. Renewables build-out, particularly onshore wind repowering, sustains utility demand. Eastern Europe benefits from EU cohesion fund grants channelled into transport corridors that require long miles of acoustic and security fencing.

- CertainTeed

- Bekaert

- Betafence

- Ameristar Perimeter Security

- Ply Gem

- Long Fence

- Gregory Industries

- A-1 Fence Products

- Specrail

- Jerith

- Trex Company

- Barrette Outdoor Living

- Master Halco

- ActiveYards

- Fortress Building Products

- Allied Tube & Conduit

- Eastern Wholesale Fence

- Merchants Metals

- ITOCHU Corporation (Sakura)

- Gentek Building Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government infrastructure spend boosting perimeter safety demand

- 4.2.2 Rising adoption of smart, sensor-enabled fencing systems

- 4.2.3 Climate-resilient composite & PVC materials gaining traction

- 4.2.4 Surging DIY home-improvement culture in mature economies

- 4.2.5 Mandatory critical-asset hardening (utilities, data-centres) regulations

- 4.2.6 Demand for perimeter security in agrivoltaics & vertical farming sites

- 4.3 Market Restraints

- 4.3.1 Volatile steel, timber & PVC resin prices

- 4.3.2 Competition from low-cost unorganised manufacturers

- 4.3.3 Stricter environmental rules on wood preservatives & PVC additives

- 4.3.4 Rising substitute spend on electronic surveillance in lieu of physical barriers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Materials Analysis

- 4.9 Impact of Geopolitics On Fencing Market

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material

- 5.1.1 Metal

- 5.1.1.1 Steel

- 5.1.1.2 Aluminium

- 5.1.2 Wood

- 5.1.3 Plastic & Composite

- 5.1.4 Concrete

- 5.1.5 Other Materials

- 5.1.1 Metal

- 5.2 By End-User

- 5.2.1 Residential

- 5.2.2 Agricultural

- 5.2.3 Military & Defense

- 5.2.4 Government

- 5.2.5 Mining

- 5.2.6 Petroleum & Chemicals

- 5.2.7 Energy & Power

- 5.2.8 Other End-Users

- 5.3 By Installation Type

- 5.3.1 Professional Contractor

- 5.3.2 Others - Fabricators, DIY / Modular Kits

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Netherlands

- 5.4.3.7 Rest of Europe

- 5.4.4 Middle East and Africa

- 5.4.4.1 Saudi Arabia

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 South Africa

- 5.4.4.4 Nigeria

- 5.4.4.5 Rest of Middle East and Africa

- 5.4.5 Asia-Pacific

- 5.4.5.1 China

- 5.4.5.2 India

- 5.4.5.3 Japan

- 5.4.5.4 South Korea

- 5.4.5.5 Australia

- 5.4.5.6 Indonesia

- 5.4.5.7 Rest of Asia-Pacific

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 CertainTeed

- 6.4.2 Bekaert

- 6.4.3 Betafence

- 6.4.4 Ameristar Perimeter Security

- 6.4.5 Ply Gem

- 6.4.6 Long Fence

- 6.4.7 Gregory Industries

- 6.4.8 A-1 Fence Products

- 6.4.9 Specrail

- 6.4.10 Jerith

- 6.4.11 Trex Company

- 6.4.12 Barrette Outdoor Living

- 6.4.13 Master Halco

- 6.4.14 ActiveYards

- 6.4.15 Fortress Building Products

- 6.4.16 Allied Tube & Conduit

- 6.4.17 Eastern Wholesale Fence

- 6.4.18 Merchants Metals

- 6.4.19 ITOCHU Corporation (Sakura)

- 6.4.20 Gentek Building Products

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

8 Appendix

- 8.1 Macroeconomic Indicators

- 8.2 Key Production, Consumption, Export & Import Stats